L1 is now innovating and becoming more specialized, while L2 seems to be following the old path of L1s - attracting fork protocols for airdrop farming, but lacking innovation and diversification.

Written by: DefiIgnas

Translated by: DeepTechFlow

The more L2s there are, the more bullish I am on the previous new public chains (alt-L1).

The last bull market was the beta phase for non-Ethereum L1s:

Alt-L1s competed by offering liquidity mining rewards on the same fork protocols as Aave and Uniswap V2, attracting degens who were extremely eager for returns.

But there was almost no innovation at the application layer outside of Ethereum.

Even non-EVM chains launched EVM sidechains: Near's Aurora, Polkadot's Moonbeam, and Cosmos's Kava. EOS EVM and Solana's Neon arrived late, missing out on this party.

The only distinguishing factors for the aforementioned L1s are:

1) Lower gas fees; 2) Speed; 3) Brand; 4) How much liquidity mining rewards they can offer.

However, as the bear market begins, liquidity mining rewards decrease, and TVL returns to the embrace of Ethereum.

To make matters worse, a new narrative for Ethereum L2 has emerged with the appearance of Optimism and Arbitrum, promising scalability without compromising security.

Furthermore, these L2s are also using potential airdrops to attract users.

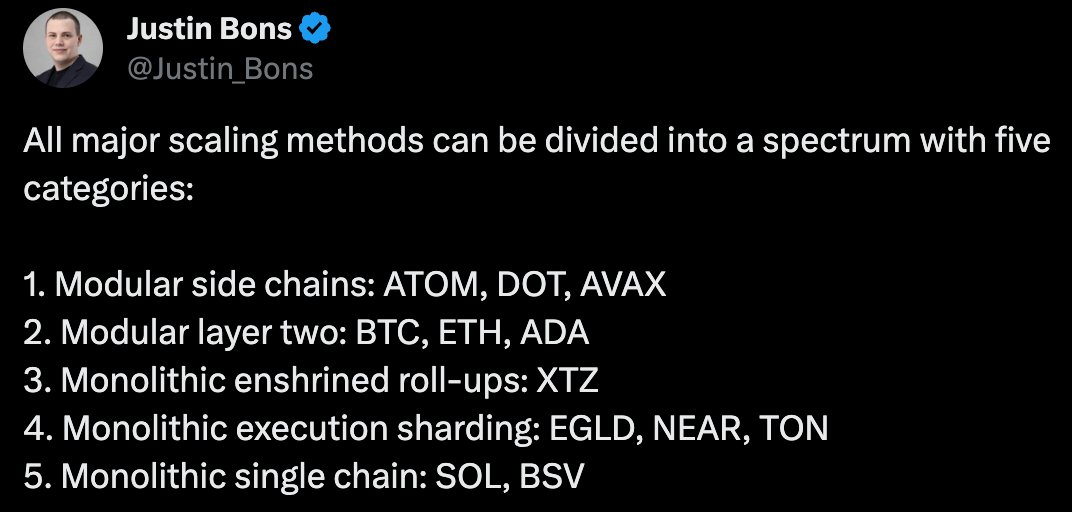

L1s need to reshape themselves, and I am glad to see that they have:

- Avalanche: Doubling down on scalability through subnets, focusing on asset tokenization, bringing more stablecoins to become forex trading chains, etc.

Polygon: Becoming an L2 harbor for applications with any specific purpose. The recent event attracting OKX was a major success.

Near: Positioning itself as a monolithic and modular blockchain. Near is collaborating with Polygon to extend Ethereum at the data availability layer, but Near also provides chain abstraction for L2 through a unified UI (BOS) and L2 account aggregation.

- Solana: Leading the wave of monolithic scaling, providing fast transactions; fast, but without the cumbersome modular user experience. I will share more information about Ethereum VS Solana in tomorrow's blog post.

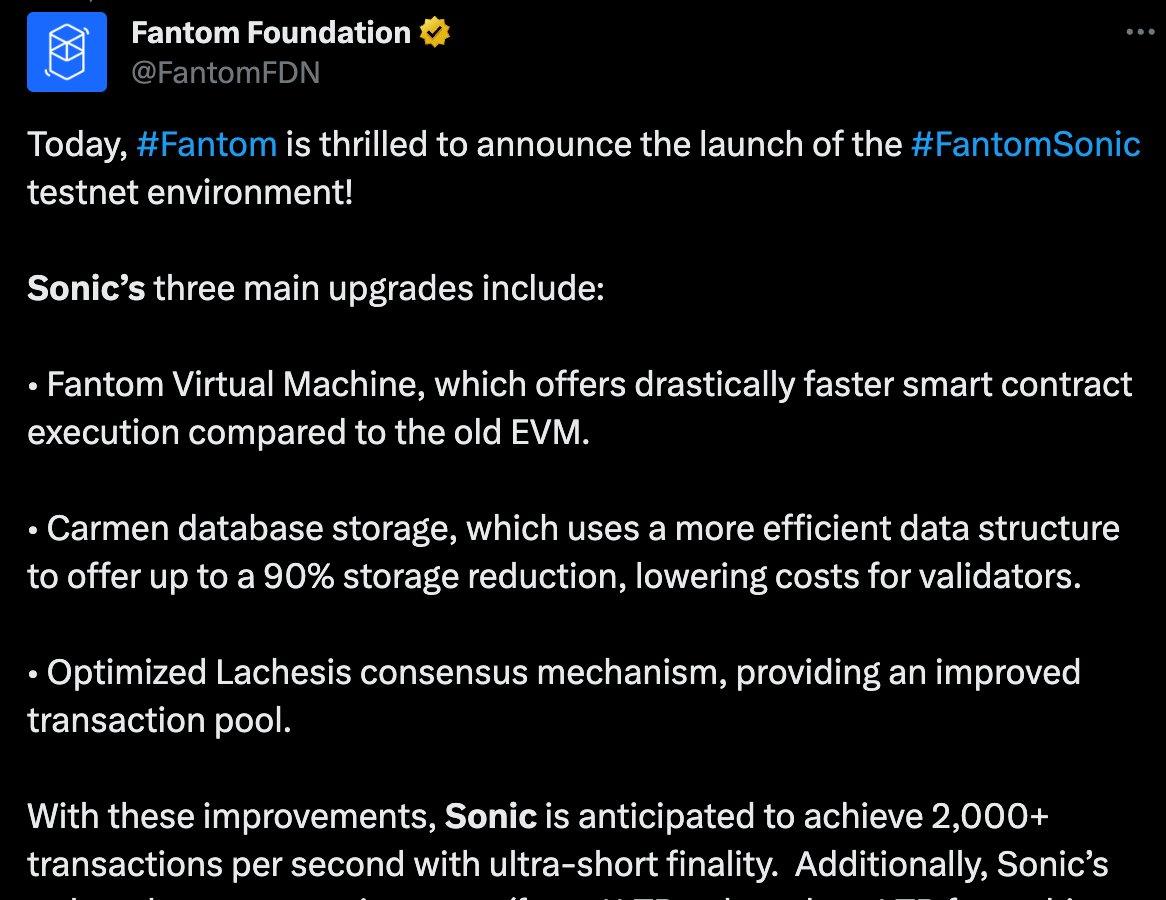

- Fantom: Doubling down on monolithic design through the Sonic upgrade, bringing 2k TPS without sharding or L2. The goal is to attract a new generation of dapps.

BNB Chain: Introducing opBNB L2 to reduce fees, but more importantly, the upgrade is BNB Greenfield, focusing on DataFi for data and IP monetization and decentralized AI (with privacy-preserving large language model training).

Cosmos: The ATOM token seems to have lost its value proposition, but with the thriving ecosystem of Osmosis, Injective, and Kuji, the Cosmos Hub is thriving.

L1 is now innovating and becoming more specialized, while L2 seems to be following the old path of L1s - attracting fork protocols for airdrop farming, but lacking innovation and diversification.

Unfortunately, the token economics of many L2 tokens are poor. Look at the problematic "staking" proposal for the ARB token.

As expected, old but excellent L1 tokens are on the rise. Compared to the previous bull market, they now offer more compelling value propositions.

Is this just a short-term reversal? I hope not.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。