Author | TaxDAO

Current Situation and Prospects of Stablecoin Regulation

Stablecoin is a type of cryptocurrency anchored to fiat currency or other assets, aiming to reduce price volatility, improve payment efficiency, and promote financial inclusion. Due to the linkage of stablecoins to sovereign currencies, they may have implications for financial stability, consumer protection, anti-money laundering, taxation, and even threaten the status of sovereign currencies. This article aims to explore the current status and issues of international stablecoin regulation, analyze the importance of stablecoin regulation, review the regulatory attitudes and policies of various countries towards stablecoins, discuss the relationship and impact of stablecoins on fiat currency and DeFi, and provide suggestions and prospects for future stablecoin regulation.

1. Imperative Stablecoin Regulation: Concepts and Background

1.1 Concept and Classification of Stablecoins

1.1.1 Concept of Stablecoins: Development in Practice

Stablecoin is a type of cryptocurrency anchored to fiat currency or other assets, aiming to reduce price volatility, improve payment efficiency, and promote financial inclusion. The emergence of stablecoins aims to address the issues of high volatility and low liquidity of traditional cryptocurrencies while retaining their advantages of decentralization, transparency, and programmability.

The earliest stablecoin projects appeared in 2014, such as BitUSD and NuBits, which issued stablecoins backed by other cryptocurrencies. Stablecoins issued in this manner have lower stability due to the volatile nature of other cryptocurrencies. In 2015, Tether introduced USDT, a fiat-collateralized stablecoin anchored to the US dollar, which is currently the highest market value and highest trading volume stablecoin.

In 2018, fiat-collateralized stablecoins flourished, with notable stablecoins such as USDC, PAX, and TUSD emerging during this period. They all claim to have sufficient reserves of fiat currency and undergo audits and supervision by third-party institutions. Additionally, there have been some commodity-backed stablecoins, such as PAXG, DGX, which are anchored to physical commodities like gold.

In 2019, Facebook announced the Libra project, which is an algorithmic stablecoin anchored to a basket of fiat currencies and bonds, aiming to create a global payment network. However, due to its scale and influence, it sparked strong opposition and concerns from governments and regulatory agencies worldwide.

From 2020 to the present, algorithmic stablecoins have become a new focus, which do not have any collateral but stabilize prices through adjusting supply using algorithms. Representative algorithmic stablecoins include Ampleforth, Basis Cash, Frax, etc.

1.1.2 Classification of Stablecoins

The historical development of stablecoins also reflects the differences between various types of stablecoins; they can be classified into four categories based on their stability mechanisms: fiat-collateralized stablecoins, crypto-collateralized stablecoins, algorithmic stablecoins, and commodity-backed stablecoins.

- Fiat-collateralized stablecoins: This is the most common type of stablecoin, which is anchored to fiat currency or other traditional assets (such as gold, US dollar bonds, etc.) and is held by centralized issuers or custodial institutions. The price of these stablecoins remains consistent or close to the anchor, with high liquidity and convertibility.

- Crypto-collateralized stablecoins: This type uses other cryptocurrencies (such as Bitcoin, Ethereum, etc.) as collateral and is managed in a decentralized manner through smart contracts or other mechanisms. The price of these stablecoins is negatively correlated with the collateral, meaning that when the collateral price falls, the stablecoin price rises, and vice versa.

- Algorithmic stablecoins: These stablecoins do not have any collateral and stabilize prices by adjusting supply based on market demand using algorithms. The price of these stablecoins is positively correlated with market demand, meaning that when market demand increases, the algorithm increases the supply to lower the price.

- Commodity-backed stablecoins: These stablecoins are anchored to commodities (such as gold, silver, oil, etc.) and are held by centralized or decentralized issuers or custodial institutions. The price of these stablecoins remains consistent or close to the anchor, with high inflation resistance and value storage capabilities.

1.2 Current Market Status and Risks of Stablecoins

The market size of stablecoins has rapidly grown in recent years. According to CoinGecko's report, as of September 2023, the global market value of stablecoins is $138.4 billion. Among them, USDT occupies 49% of the market share; USDC and BUSD account for 30.9% and 11.4% of the market share, respectively. At the same time, the importance and influence of stablecoins in the cryptocurrency market are also increasing. In January 2022, stablecoins accounted for 7.3% of the total cryptocurrency market value, which rose to 12.9% in January 2023.

However, behind the rapid growth of the stablecoin market, there are also growing concerns, manifested in several aspects.

First, similar to other cryptocurrencies, stablecoin transactions pose risks in tax regulation and financial operations. The cross-border nature and anonymity of stablecoins increase the risk of tax evasion and tax leakage, and their transactions involve multiple areas of financial operations, posing regulatory challenges for tax authorities in various countries.

Second, the potential credit risk of centralized stablecoins has drawn attention from governments worldwide. Taking USDT as an example, Tether claims that for every 1 USDT issued, it will deposit 1 US dollar in the reserve account to maintain the stability of USDT's value. However, USDT issuance lacks national credit endorsement and sufficient regulatory mechanisms; therefore, Tether is often suspected of the risk of over-issuing USDT for profit. If the collateral deposited by exchanges is insufficient, the value of stablecoins will decouple from their anchored assets, directly leading to a contraction in the financial market.

More importantly, the development of stablecoins brings about risks in monetary policy. If stablecoins (especially global stablecoins) are widely used, they may affect the monetary supply of various countries, thereby influencing the effectiveness of exchange rates, interest rates, and other monetary policy tools, and even threatening the monetary sovereignty and financial stability of various countries.

Considering these risks, the International Monetary Fund (IMF) has called for the establishment of a global unified regulatory system for stablecoins on multiple occasions. In a blog post titled "Crypto Contagion Underscores Why Global Regulators Must Act Fast to Stem Risk" released by the IMF in January of this year, it was stated that without proper regulation, stablecoins could undermine the effectiveness of monetary policy, trigger financial crises, and this applies to both advanced and developing economies. Previously, in the September 2022 Fintech Note, the IMF emphasized the need for robust, comprehensive, and globally consistent regulation of crypto assets.

2. Current Status of Stablecoin Regulation: Seeking Unity in Diversity

2.1 Origin of Stablecoin Regulatory Policies

Overall, stablecoin regulation has gradually gained attention from governments worldwide since 2019; prior to that, stablecoins were typically subject to unified regulation alongside other digital assets, rather than having their own specific regulatory requirements.

In 2019, the issuance plan of Libra sparked global attention and concerns about stablecoins, and financial risk issues related to stablecoins began to "come to the forefront." The G7 Stablecoin Working Group released the "Global Stablecoin Assessment Report" in October 2019, formally introducing the concept of "global stablecoins" for the first time and pointing out their potential challenges to financial stability, monetary sovereignty, consumer protection, and other aspects. Subsequently, the G20 entrusted the Financial Stability Board (FSB) to review the Libra project and released two regulatory recommendations on global stablecoins in April 2020 and February 2021, respectively.

2.2 Overview of Stablecoin Regulatory Dynamics in Major Countries and Regions

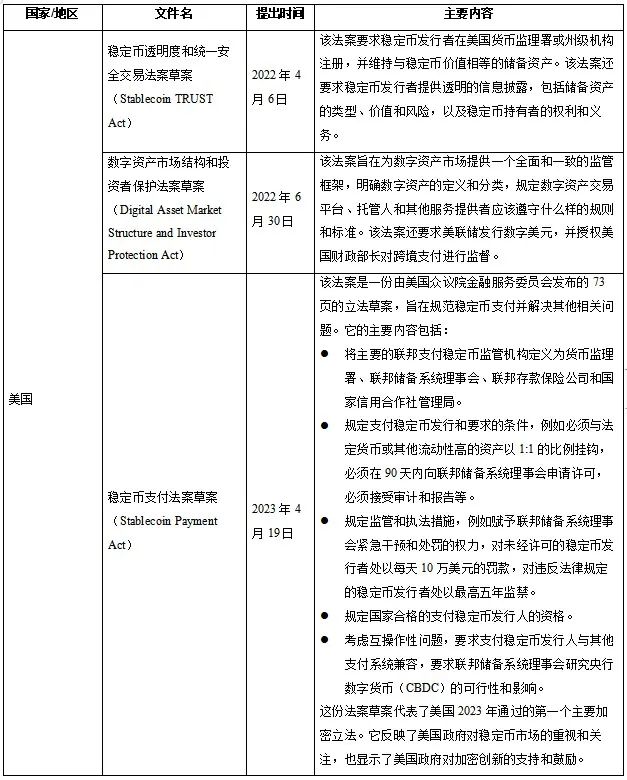

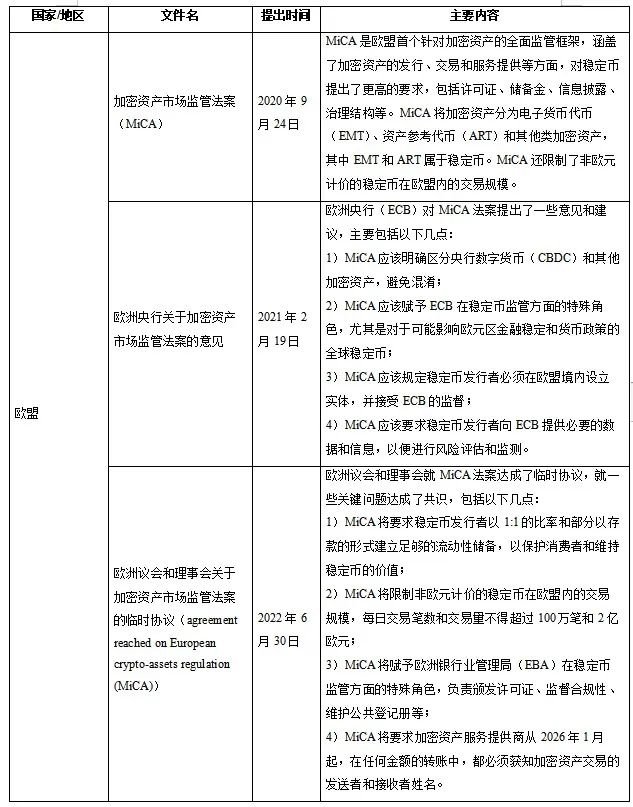

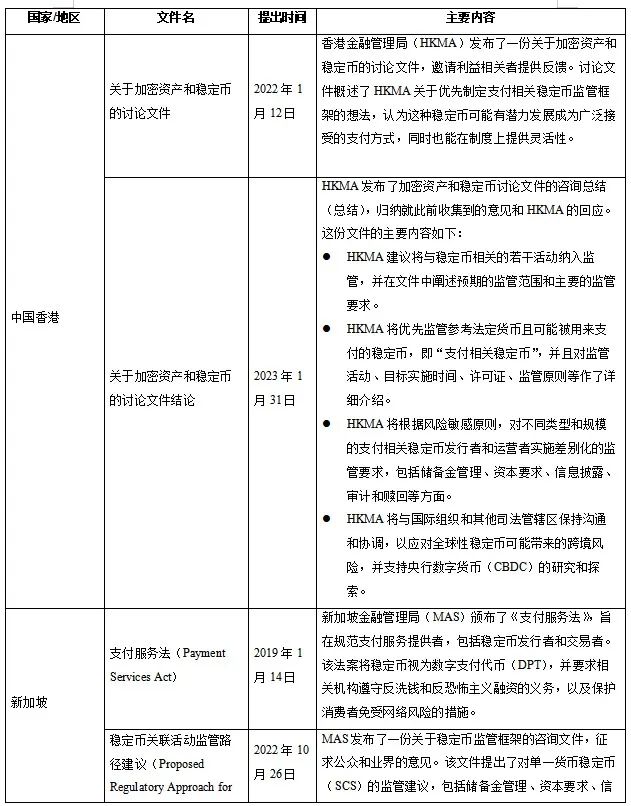

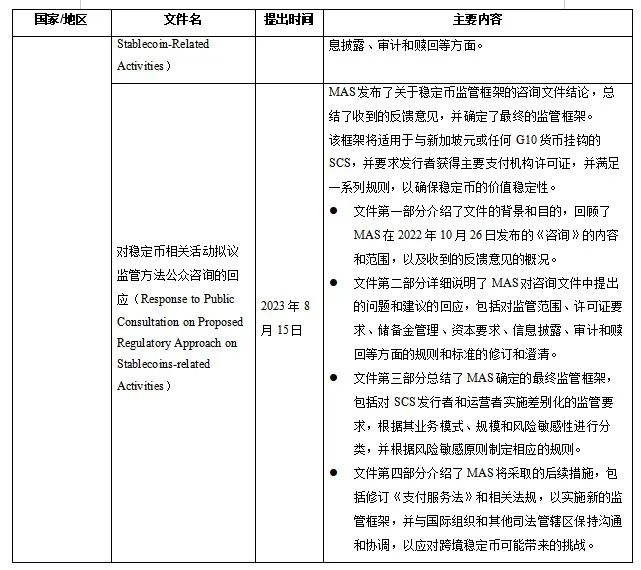

Guided by the FSB's regulatory recommendations, some countries and regions have also put forward their own stablecoin regulatory policies, with the United States, the European Union, Hong Kong (China), and Singapore having relatively advanced regulatory policies. This article has compiled the main regulatory policies of these four countries/regions since 2019, as shown in the table below.

The "Stablecoin Payment Act Draft" in the United States is expected to become the world's first formal legislation specifically regulating stablecoins, while the policy discussions in Hong Kong and Singapore are still some distance away from formal legislation. Looking at the current legislative trends, the commonalities in stablecoin regulation can be summarized as follows:

- Treating stablecoins as special crypto assets and subjecting them to specialized regulation, rather than incorporating them into existing financial regulations;

- Requiring stablecoin issuers and operators to obtain corresponding licenses or registrations and be subject to supervision and audits by relevant institutions;

- Requiring stablecoin issuers and operators to maintain reserves equal to the value of the stablecoin and transparently disclose the type, value, and risks of the reserves;

- Requiring stablecoin issuers and operators to comply with anti-money laundering and counter-terrorism financing obligations, and implementing measures to protect traders and prevent network risks;

- Restricting or prohibiting stablecoins denominated in foreign currencies to maintain the sovereignty and stability of the domestic currency;

- Maintaining communication and coordination with international organizations and other jurisdictions to address cross-border stablecoin issues.

3. Stablecoin Regulation: Policy Prospects

3.1 Stablecoins and Fiat Currency: Entanglement and the Future

In the cryptocurrency trading market, the primary role of stablecoins is to "act as" fiat currency, serving as a value scale for the trading of other assets. This is because the exchange between fiat currency and cryptocurrencies usually requires centralized exchanges or other third-party institutions, which increases the time, cost, and risk of transactions, while stablecoins can facilitate decentralized transactions on the blockchain, improving transaction efficiency and security.

Stablecoins are dependent on fiat currency, but fiat currency is also influenced by stablecoins. On one hand, fiat-collateralized stablecoins rely on fiat currency as the anchor to maintain their value stability, and are also subject to fiat currency regulatory policies. For example, according to the "Stablecoin Act" in the United States, fiat-collateralized stablecoins require centralized issuers and custodians to hold fiat assets and provide a reserve proof mechanism to demonstrate that they have sufficient collateral assets. However, on the other hand, stablecoins also have the potential to challenge the status of fiat currency, as they offer higher transaction efficiency, anonymity, and transparency, which may attract more users and capital inflows. If a certain stablecoin (such as USDT) is widely accepted, it could potentially play a role similar to M0 or M1 in the national currency system, thereby affecting the money supply— at this point, the money supply is no longer solely determined by the central bank, but is jointly determined by the central bank and stablecoin issuers, effectively leading to a partial loss of coinage rights by the country.

For this reason, countries often take a cautious approach to the regulation of stablecoins, especially imposing strict restrictions on sovereign currencies linked to stablecoins. Considering the existing policy directions, the regulation of fiat-collateralized stablecoins is expected to become increasingly stringent.

3.2 DeFi and Stablecoins: Twinning

Stablecoins are the foundational assets and trading medium of DeFi, promoting the development and innovation of DeFi.

Stablecoins are crucial for DeFi. They maintain price stability in the highly volatile world of virtual currencies, separating the risk/reward calculations of DeFi services from the high volatility of digital assets. For DeFi services, financial transactions require stable prices for value exchange. Investors also need a stable unit of account. Stablecoins play various roles in DeFi, such as:

Serving as borrowing or collateral in the lending market, providing low-cost, efficient, and uncollateralized lending services. For example, MakerDAO is a decentralized lending platform based on Ethereum, where users can generate DAI (a decentralized stablecoin pegged to the US dollar) by over-collateralizing crypto assets (such as ETH). Users can use DAI for trading or investment, or redeem collateral at any time.

Acting as trading pairs or liquidity providers in the trading market, offering low slippage, high liquidity, and no market maker risk. For example, Uniswap is a decentralized trading protocol based on Ethereum, where users can deposit tokens into liquidity pools to earn trading fees. Stablecoins occupy a significant portion of the liquidity pools in Uniswap, as they can reduce impermanent loss and improve trading efficiency.

Serving as compensation or insurance funds in the insurance market, providing low-threshold, high-coverage, and no trust risk insurance services. For example, Nexus Mutual is a decentralized insurance platform based on Ethereum, where users can purchase or provide insurance against smart contract failures on the platform based on the Risk Sharing Pool (RSP) mechanism, to earn interest and rewards, or assume responsibility for insurance claims. In Nexus Mutual, stablecoins are the only assets that can be used to purchase or provide insurance.

In summary, stablecoins and DeFi have a mutually reinforcing and interdependent relationship. Stablecoins provide a stable value foundation and trading medium for DeFi, while DeFi offers a broad range of applications and innovation space for stablecoins.

References

[1] CoinGecko. (2023). Global stablecoin market capitalization.

[2] European Banking Authority. (2023). Agreement reached on European crypto-assets regulation (MiCA).

[3] European Central Bank. (2021). Opinion of the European Central Bank on a proposal for a regulation on markets in crypto-assets, and amending Directive (EU) 2019/1937.

[4] Financial Stability Board. (2020). Addressing the regulatory, supervisory and oversight challenges raised by “global stablecoin” arrangements.

[5] Financial Stability Board. (2021). FSB roadmap to enhance cross-border payments: Phase III implementation plan.

[6] G7 Working Group on Stablecoins. (2019). Investigating the impact of global stablecoins.

[7] Hong Kong Monetary Authority. (2022). Discussion paper on cryptoassets and stablecoins.

[8] Hong Kong Monetary Authority. (2023). Response to public consultation on proposed regulatory approach for stablecoin-related activities.

[9] International Monetary Fund. (2022). Crypto contagion underscores why global regulators must act fast to stem risk.

[10] International Monetary Fund. (2022). Fintech notes: Regulatory issues related to crypto-assets.

[11] Monetary Authority of Singapore. (2019). Payment Services Act 2019.

[12] Monetary Authority of Singapore. (2022). Proposed regulatory approach for stablecoin-related activities.

[13] Monetary Authority of Singapore. (2023). Response to public consultation on proposed regulatory approach on stablecoins-related activities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。