Original author: CryptoVizArt, Glassnode

Original translation: Nan Zhi, OdailyNews

Key Points Summary

- Exchanges remain at the core of the digital asset industry, with the vast majority of trades occurring there.

- Based on entity-adjusted data, our assessment shows that 54% of BTC activity is related to deposits or withdrawals from exchanges.

- Drawing from the lessons of the FTX collapse, we introduce three metrics to assess abnormal exchange activity: internal transfer rate, exchange dependency rate, and whale withdrawal rate.

- Using this exchange risk framework, we evaluate Binance, Coinbase, Huobi, and FTX to provide an overview of various exchange on-chain behaviors.

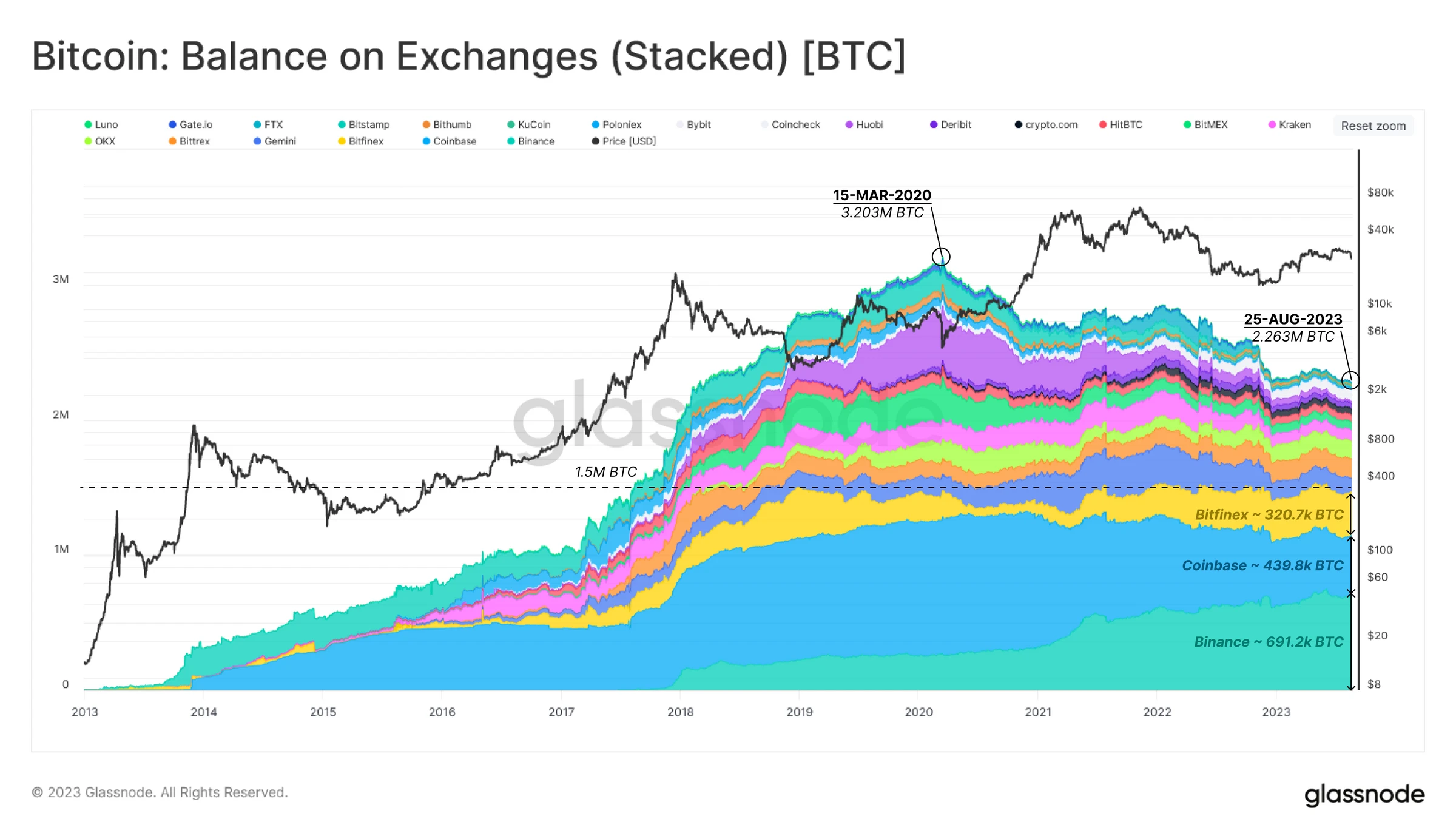

Exchange Balances

CEX holdings peaked at 3.203 million bitcoins in March 2020 and have steadily declined since. This week (end of August), the total exchange balance reached its lowest level in five years, at 2.256 million bitcoins. These exchange balances consider wallets directly related to exchanges, excluding custodians or ETF tools (such as GBTC or Microstrategy, etc.).

A notable feature of this chart is that the top three exchanges have dominated, holding around 1.5 million bitcoins since early 2019. The current estimated holdings for these exchanges are:

- Binance 691.2k bitcoins

- Coinbase 439.8k bitcoins

- Bitfinex 320.7k bitcoins

Excluding the 1.457 million bitcoins considered lost, the exchange reserve amounts to 11.8% of the circulating supply, reaching 2.31 million bitcoins, with a daily on-chain transfer volume of 12.2k bitcoins (0.6%).

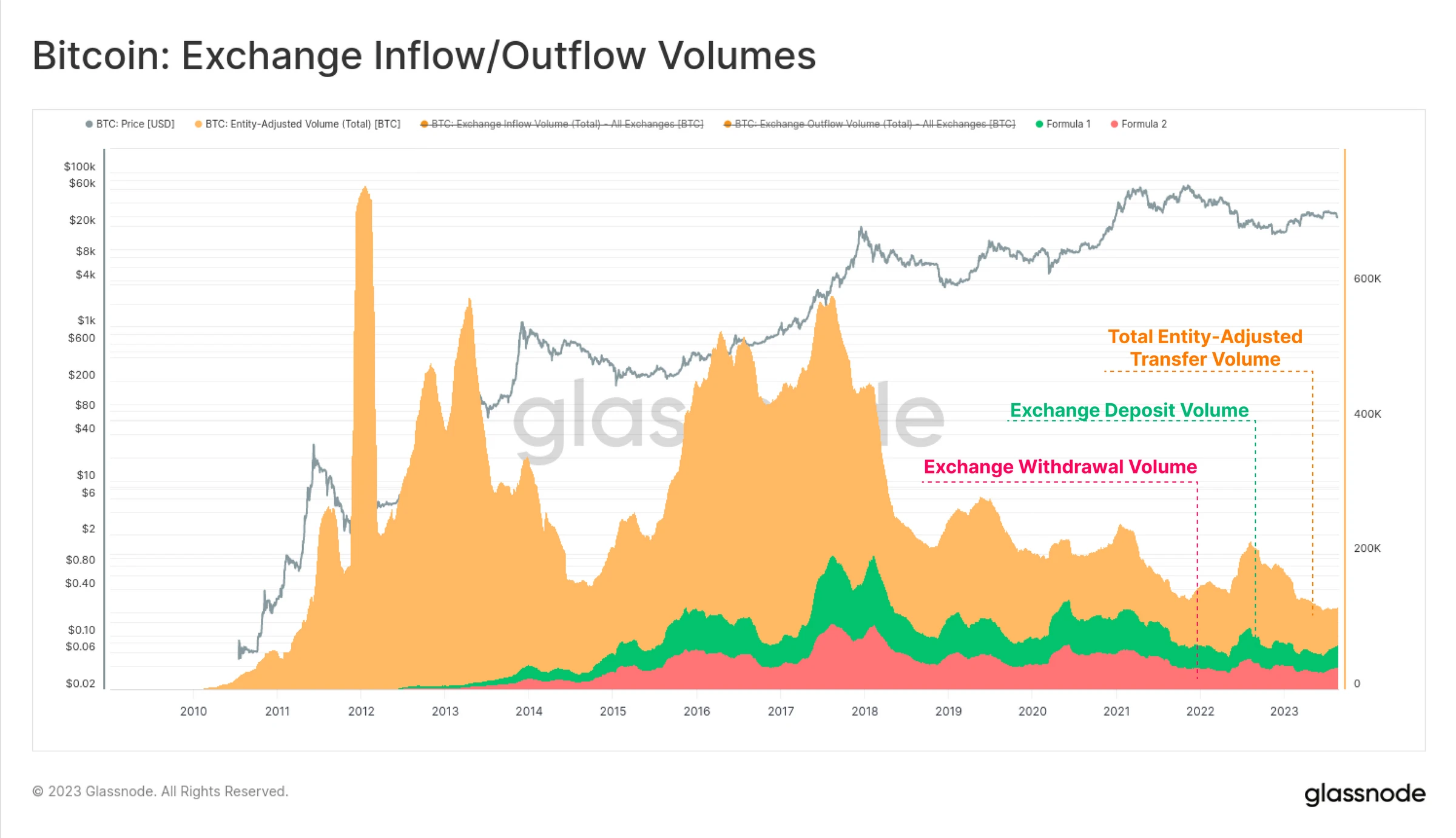

Within this 12.2k bitcoin transaction volume, deposits or withdrawals from exchanges account for over 54% (approximately 6.73k bitcoins per day, typically split evenly between deposits and withdrawals). Therefore, observing the flow of funds into and out of exchanges often contains quite rich information.

Fund Flow Analysis

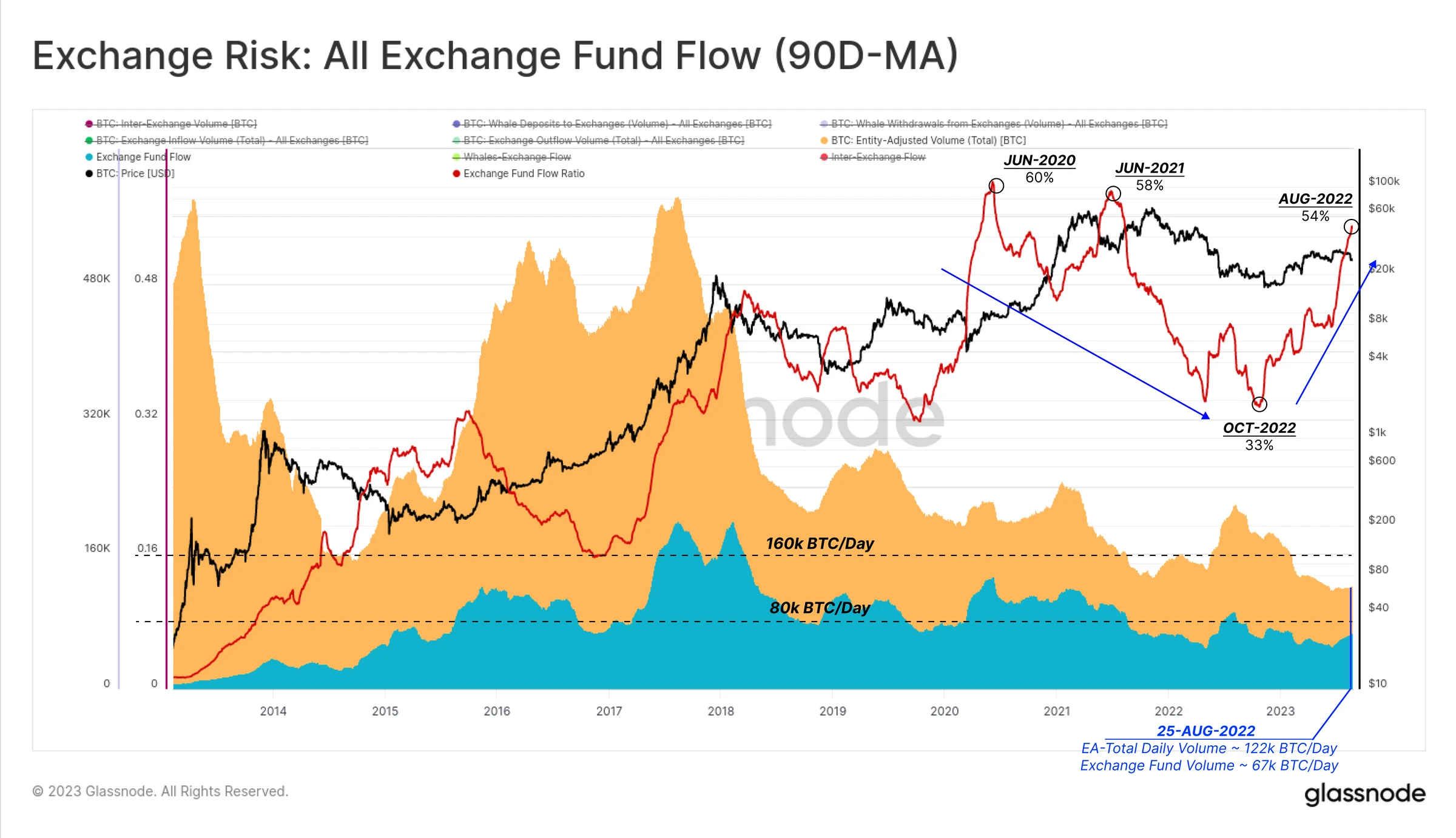

After understanding the scale of the flow, we can delve deeper into the flow of funds between entities and exchanges. In the following chart, we sum the inflow and outflow of exchanges to form a single indicator, the exchange fund flow (taking a 90-day average).

Here, we can see that the exchange fund flow accounts for 54% of the total and is on a macro upward trend. The exchange share reached 58% in June 2021, then sharply declined with the acceleration of global interest rates, liquidity tightening, and subsequent bear market. In October 2022, dominance rose again as global liquidity and markets recovered from the impact of the FTX event.

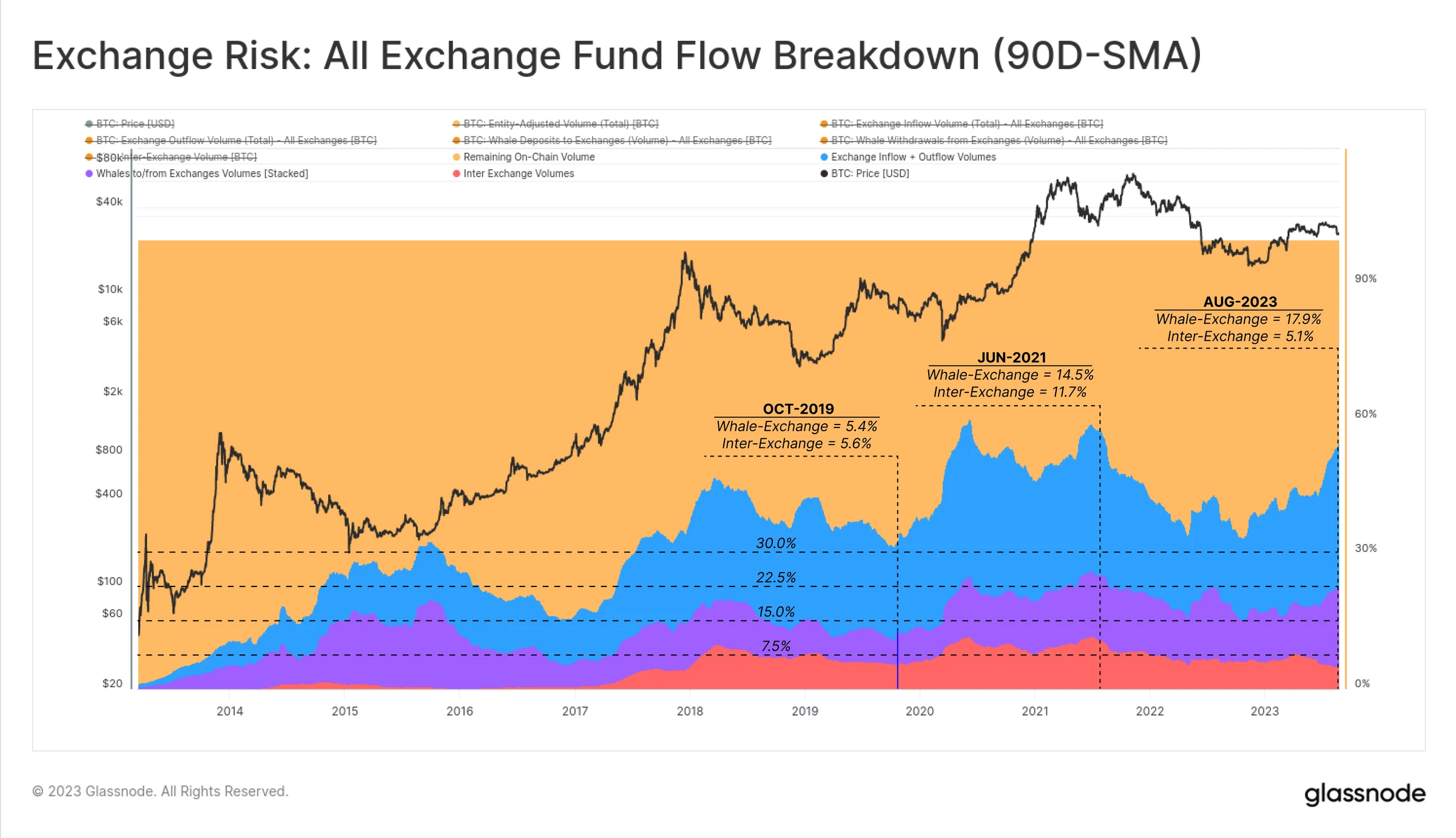

We can decompose the dominance of on-chain transaction flow into four parts:

- On-chain transaction volume unrelated to exchanges (entity-adjusted).

- All flow related to exchanges (inflow and outflow).

- Whale fund flow between exchanges: transfers of funds between whales (1,000 BTC +) and exchanges.

- Inter-exchange flow: transfers of funds from one exchange to another.

Inter-exchange flow has remained relatively stable, accounting for approximately 7.5% of on-chain transaction volume, reaching a peak of 11.7% in June 2021. Meanwhile, whale flow to and from exchanges recently reached a new historical high of 17.9%.

As we can see, exchange-related flow (54%) is currently close to its historical high.

Exchange Risk Analysis Framework

The first part of the report establishes the view that exchanges dominate the Bitcoin ecosystem. However, after the FTX event, exchanges may also become a source of counterparty risk.

In the next section, we aim to establish a framework for analyzing the related risks of individual exchanges. In this section, we will use the FTX dataset as a reference point for future high-risk situations. Considering Coinbase's dominance and recent market commentary on Binance and Huobi, we will provide data related to these exchanges for comparison.

We will use three metrics to build this framework:

- Internal transfer rate - the ratio of internal transfer amount within the exchange over the total reserve balance over a period of time.

- Exchange dependency rate - the degree of flow between exchanges (inter-exchange transfers).

- Whale withdrawal rate - a measure of large entities accelerating fund withdrawals.

Internal Transfer Rate

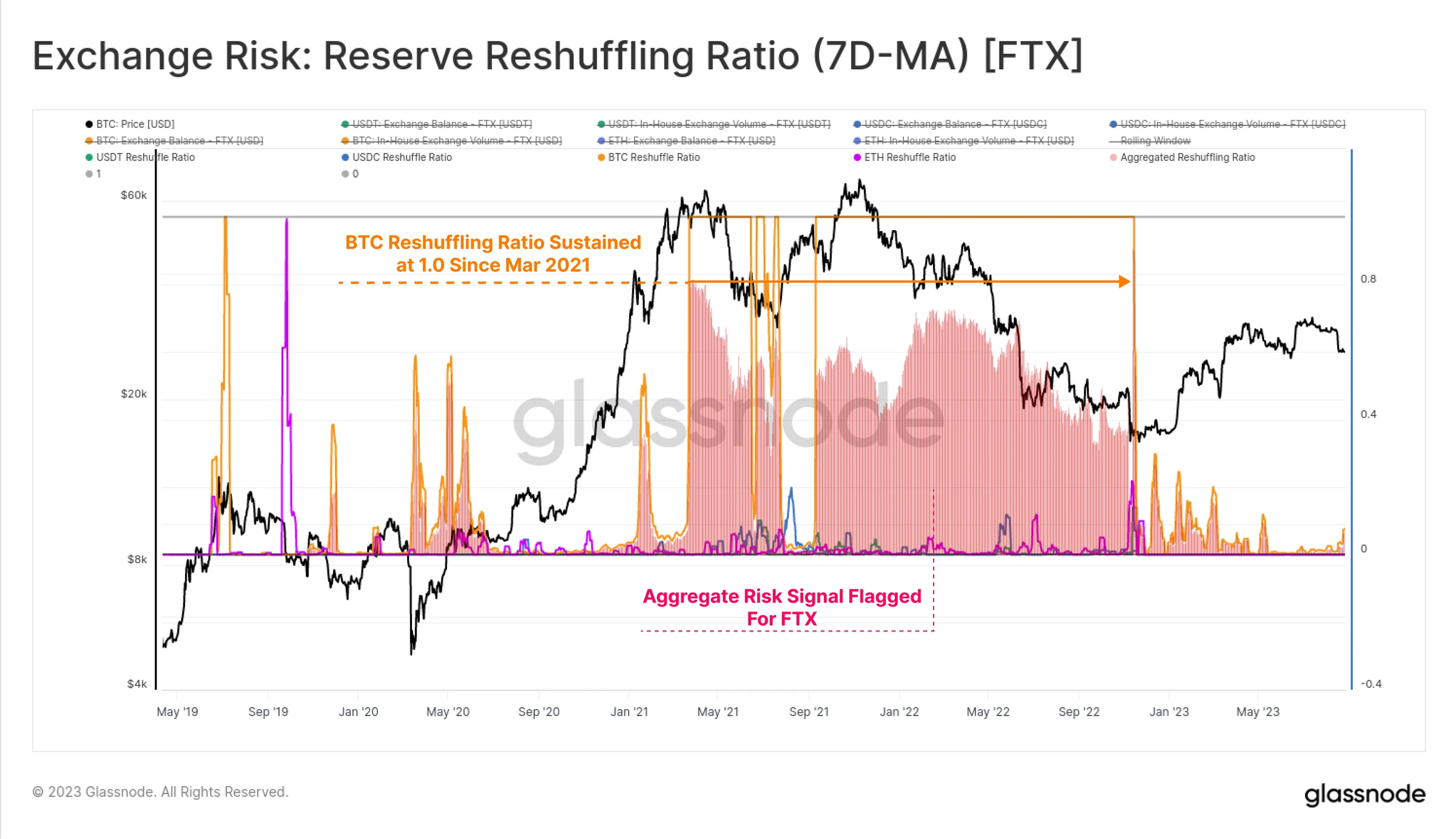

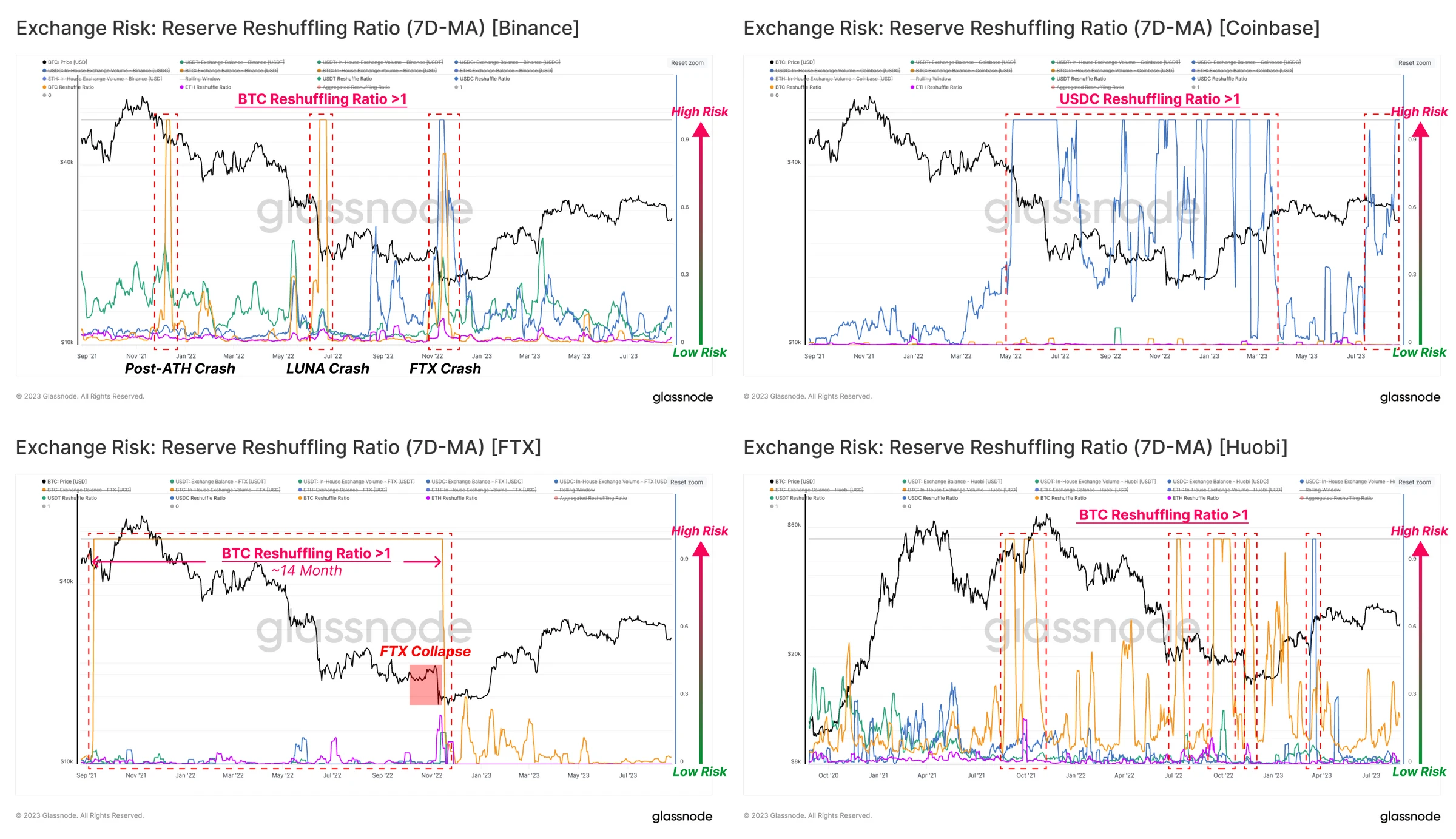

The first metric is the ratio of internal wallet transfers within the exchange to the total exchange reserve balance. To provide comparable metrics across all exchanges and assets, the output value ranges from 0 to 1.

The core idea is to identify situations where internal transfers within the exchange exceed 100% over a period of 7 days. If this situation persists for a long time and across multiple asset types, it may be a warning signal of improper fund management.

For FTX, we can see that their Bitcoin internal transfer rate remained at 1.0 from March 2021 until the collapse in November 2022. We also show a "comprehensive risk" score considering the four largest assets: BTC, ETH, USDC, and USDT.

When compared with the other three exchanges, some exchange-specific subtle differences can be seen:

- Binance (top left): During periods of market volatility, there were sudden peaks in internal transfer rates across all assets, followed by rapid declines. This seems to be a market reaction and is not persistent, likely a result of new deposit and withdrawal processing.

- Coinbase (top right): Except for USDC, there were few internal transfer events that lasted for a long time. This is likely due to Coinbase's collaboration with issuer Circle and its significant involvement in USDC inflows and outflows.

- FTX (bottom left): The internal transfer rate of Bitcoin entered the high-risk zone in the 14 months before the exchange collapse. In hindsight, this was likely the result of Alameda misappropriating client funds.

- Huobi (bottom right): This exchange exhibited volatility similar to Binance's due to gradually decreasing exchange asset balances (reducing the denominator).

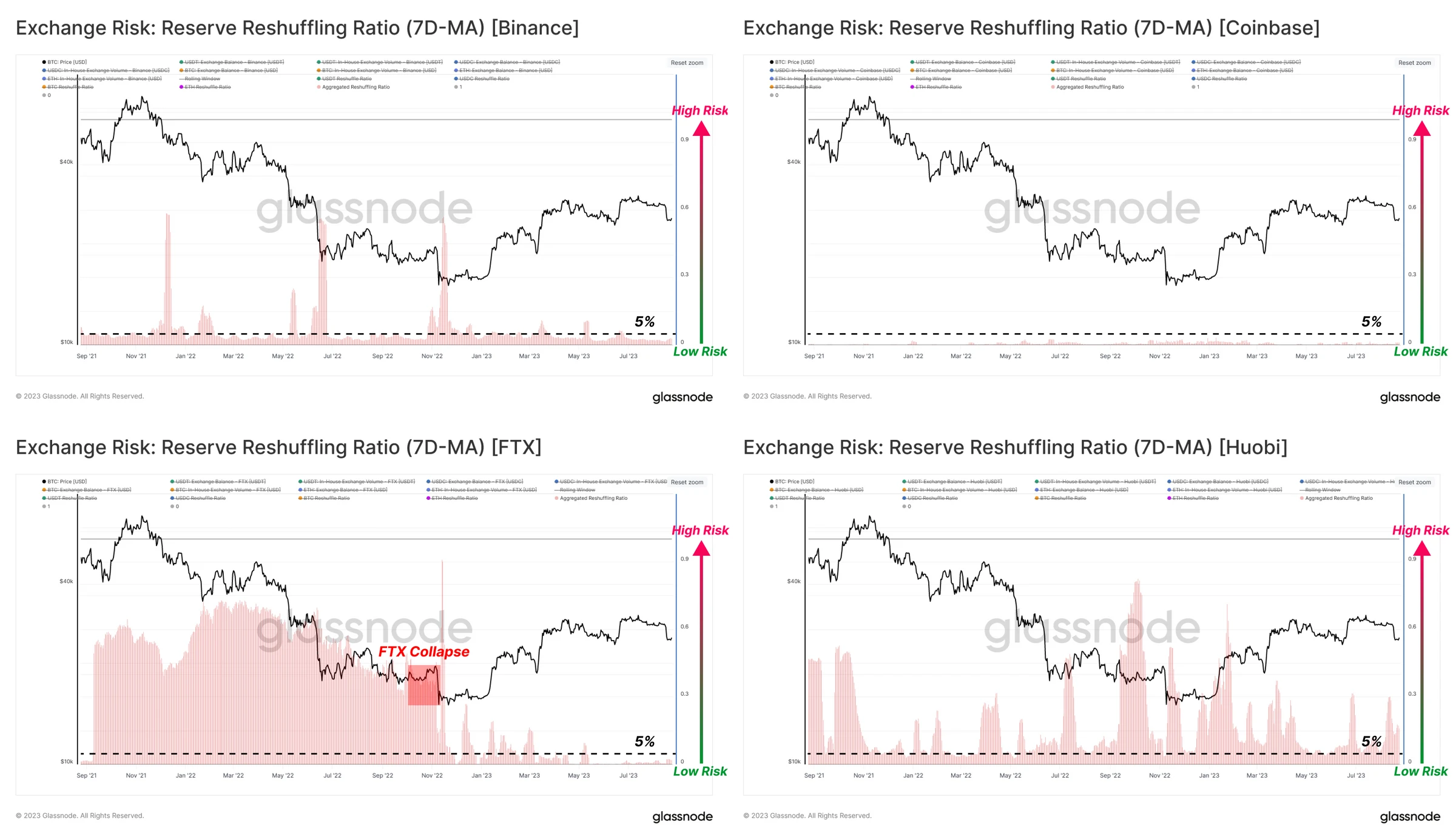

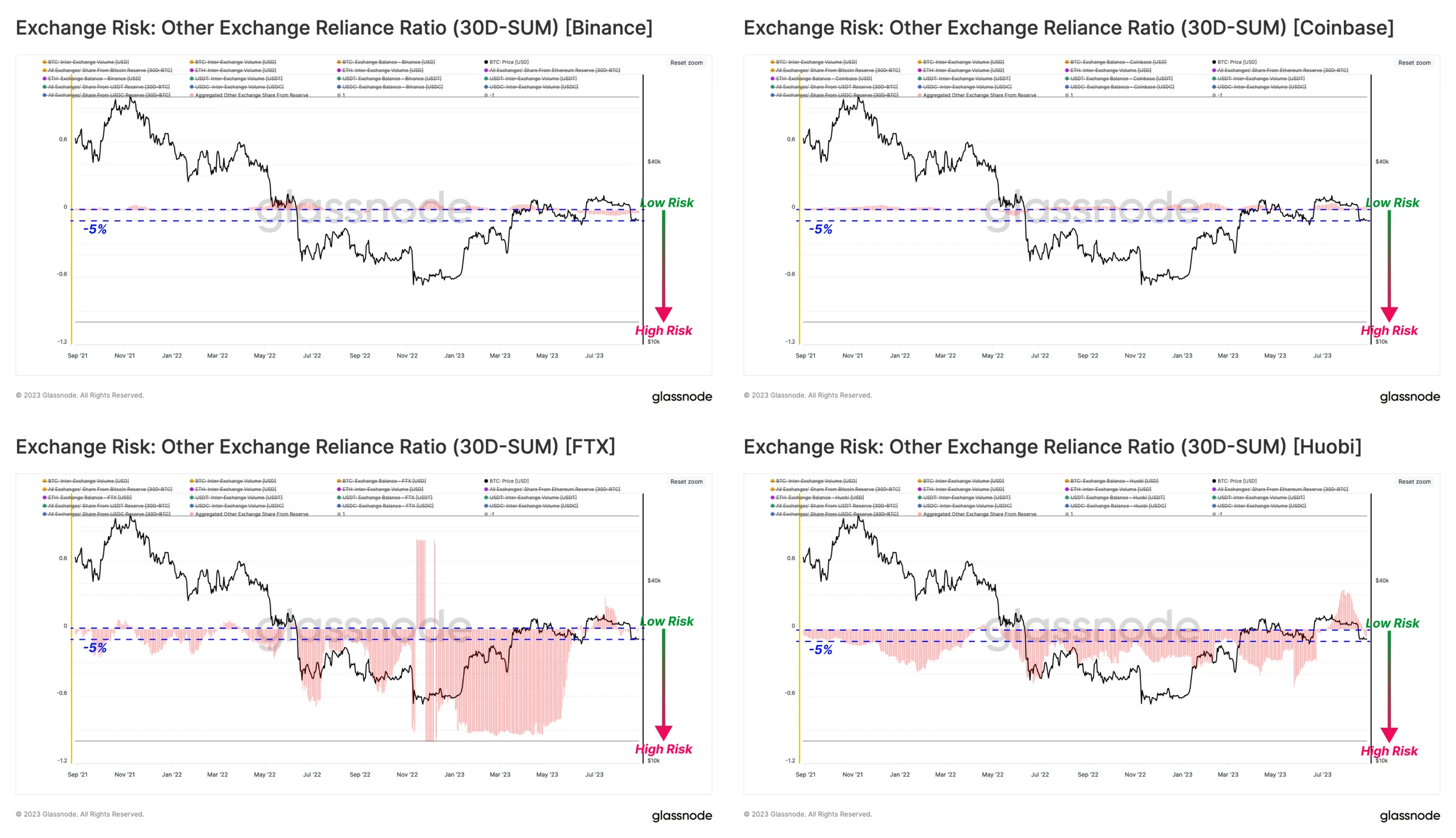

The following chart compares the internal transfer rates of these four exchanges across the four assets. Here, we use a 5% threshold to mark potential high-risk events. From this perspective, Binance and Coinbase have almost no internal "changes".

As we now know, FTX stood out for various reasons, all of which were negative.

Huobi's situation is in the middle, with internal transfer rates similar to Binance's, but with greater volatility due to gradually decreasing exchange asset balances (reducing the denominator).

Exchange Dependency Rate

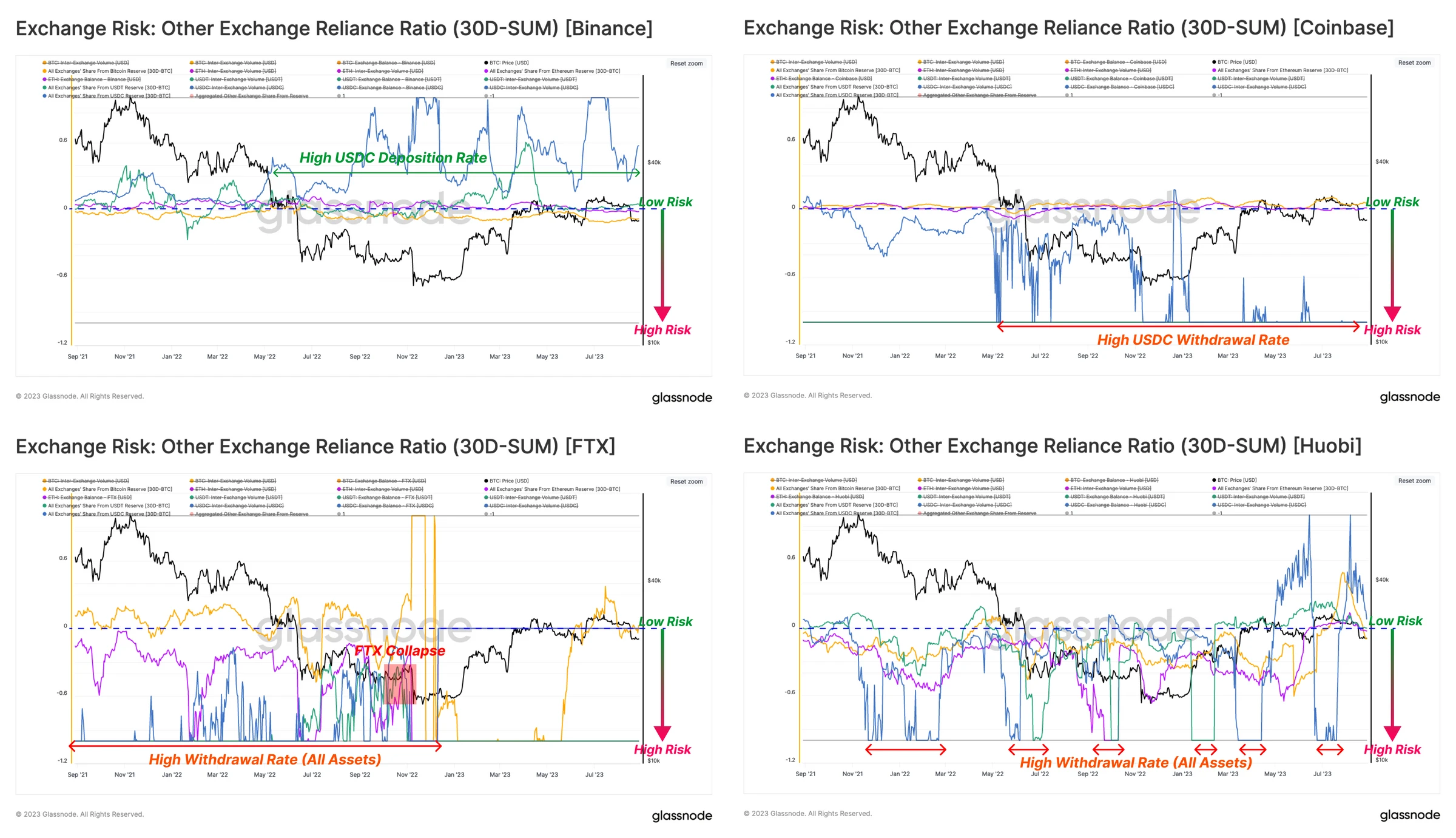

Another indicator of potential exchange risk is the frequency with which exchange tokens are transferred in or out from another exchange. This may indicate a high degree of liquidity dependence between these exchanges.

Similar to the previous metric, we calculated this rate for the top four assets in the market and limited the output values to a range of -1 to 1. We can also determine the direction of funds, whether the ratio is positive (net inflow) or negative (net outflow), and investigate the source and destination of funds.

Significantly negative values in this metric indicate that assets are rapidly flowing out of the exchange and into another. If this situation persists for a period of time, it may trigger an alert.

Reviewing the top four assets of the aforementioned exchanges:

- Binance (top left): All assets have neutral or near-zero dependency rates, indicating relatively small funds flowing in or out from other exchanges compared to Binance's balance. Since September 2022, the inflow rate of USDC has been high, likely due to obtaining USDC from Coinbase.

- Coinbase (top right): Similar to Binance, all assets show neutral dependency rates. However, since September 2022, the outflow rate of USDC has been high. This indicates that a large amount of USDC supply has migrated from Coinbase to Binance over the past 12 months.

- FTX (bottom left): The dependency rates of all four assets were significantly negative before the exchange collapse. This indicates that investors (and Alameda) were transferring all major assets to accounts on other exchanges.

- Huobi (bottom right): Evaluating this risk indicator for Huobi, we can see that the dependency rates for all assets are significantly negative, indicating a net outflow from Huobi to other exchanges.

We once again present the comprehensive dependency rate, which shows that Binance and Coinbase have very low dependency, at -5% or higher, indicating that their behavior is largely independent of other exchanges.

On the other hand, FTX and Huobi have negative comprehensive dependency rates, indicating that active entities from other exchanges have been consistently withdrawing funds from these entities.

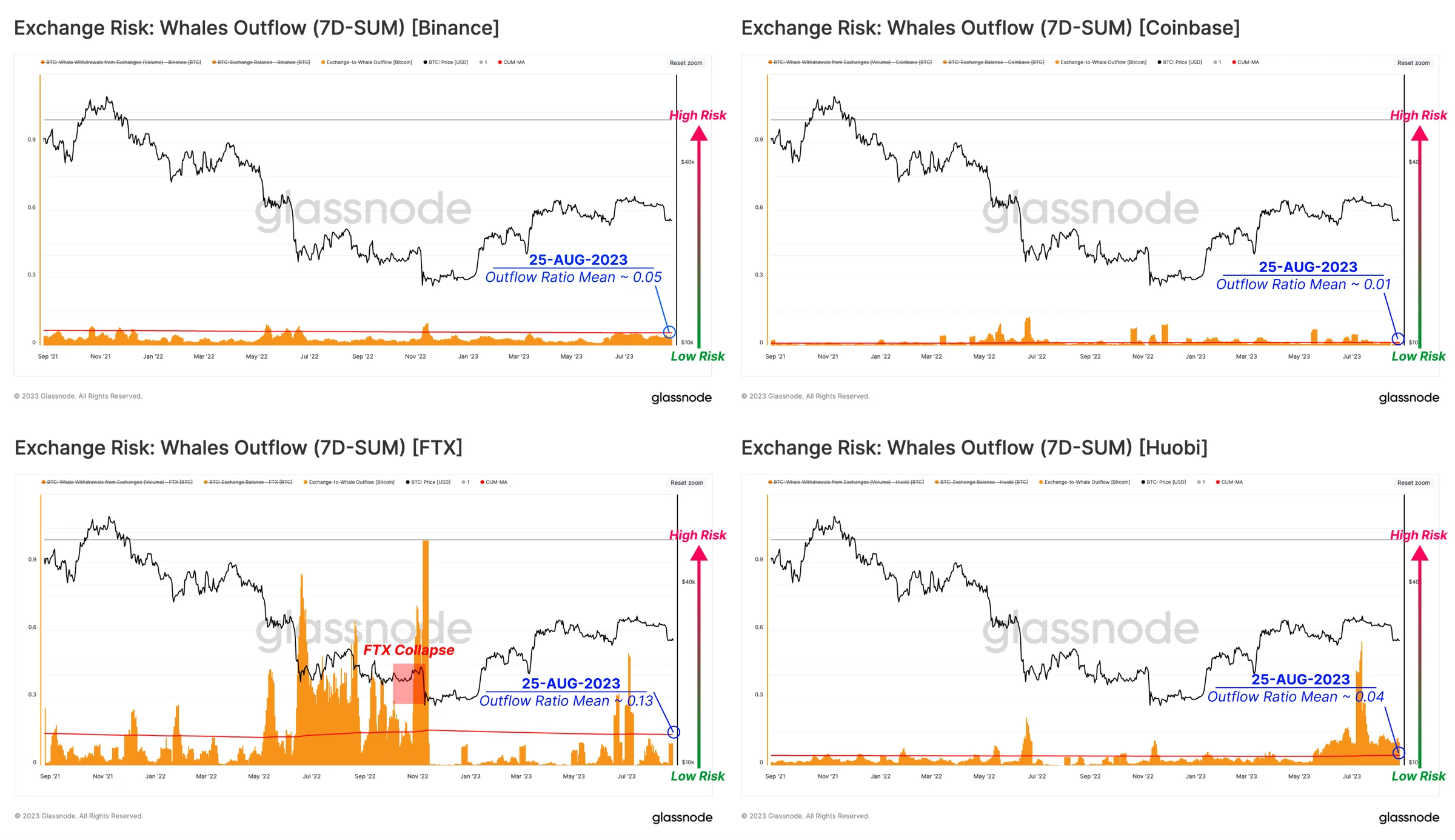

Bitcoin Whale Withdrawal Rate

The final metric is to monitor whether Bitcoin whales are accelerating their withdrawals. This parameter is the ratio of the total weekly whale outflow to the exchange's Bitcoin balance.

In addition to the whale withdrawal rate, we also show the historical average of this metric as a long-term benchmark.

- Over the past two years, the whale withdrawal rates for Coinbase and Binance have been very low, with long-term averages staying below 5%;

- For FTX, the surge in whale withdrawal rates began with the collapse of LUNA and 3AC, and remained at a high level until the exchange's closure;

- For Huobi, the risk was relatively low until June 2023. It is only in recent months that the whale withdrawal rate has been consistently rising relative to the Huobi BTC balance. This will to some extent drive the continued decline in the Huobi BTC balance, making this metric reflexive.

Conclusion

FTX's failure serves as a reminder to the digital asset industry that counterparty risk still exists in CEX and custodians. Guided by hindsight, we have proposed three metrics and provided simple insights into some potential risks within exchanges using our on-chain data and labeled clusters.

We find that Coinbase and Binance exhibit similar and secure on-chain data through the internal transfer rate, exchange dependency rate, and whale withdrawal rate. Unfortunately, FTX is a notable risk indicator, and for Huobi, the continued decline in the balances of the four major assets BTC, ETH, USDT, and USDC will worsen these metrics, indicating a need for some degree of caution.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。