Written by: Alice, Foresight Ventures

There is no doubt that Friend.tech has become extremely popular. When you open the news and Twitter, the praise from KOL investors seems to overflow the screen.

There is nothing new under the sun. Twitter fan tokens are not innovative. There was Bitcloud backed by a16z in the past, and there are also communities like Only1 and Monaco, which seem to have not avoided the fate of being short-lived.

What makes the newcomer Friend.tech different? Can it bring new opportunities to the long-silent Web3 Social?

I. Stealcam

The Friend.tech team is anonymous. According to public information, its predecessor was a photo-sharing app called Stealcam.

Stealcam is a photo social sharing app where the photos posted are not freely accessible and require "stealing" (paying a certain fee) to obtain the reveal right to view the specific content of the photos. The reveal right is not indefinite and can only be viewed when you are the most recent person to have revealed the photo. The team's founders are anonymous OG Racer (Twitter handle @0xRacerAlt) and shrimp (@shrimppepe).

a. Economic Model

Each photo can be stolen an unlimited number of times, and each steal increases the price by 10% based on the previous steal price plus 0.001 ETH.

The income generated by each steal will fully refund the previous stealer's purchase cost, and the price difference generated by two steals will be distributed among the creator, the previous stealer, and the protocol, with the creator and the previous stealer receiving 45% each, and 10% allocated to the protocol.

b. User Data

In just two weeks, without relying on airdrops or issuing tokens, the protocol has accumulated a transaction volume of over 313 ETH (approximately $500,000), and the income from the stealcam protocol has reached nearly $100,000. It has attracted a large number of artists, KOLs, and VC partners to join, such as Fred Wilson, co-founder of USV (Union Square Ventures) (ranked 14th on the Leaderboard), Li Jin, co-founder of Variant Fund (ranked 25th), Jess, co-founder of Variant (ranked 79th), and the wallet rainbow (ranked 16th).

(Stealcam Leaderboard- 2023.3.29)

Based on the success of this MVP product, the team decided to upgrade the product, rebranding it as friend.tech and securing seed round investment from Paradigm.

II. Friend.tech

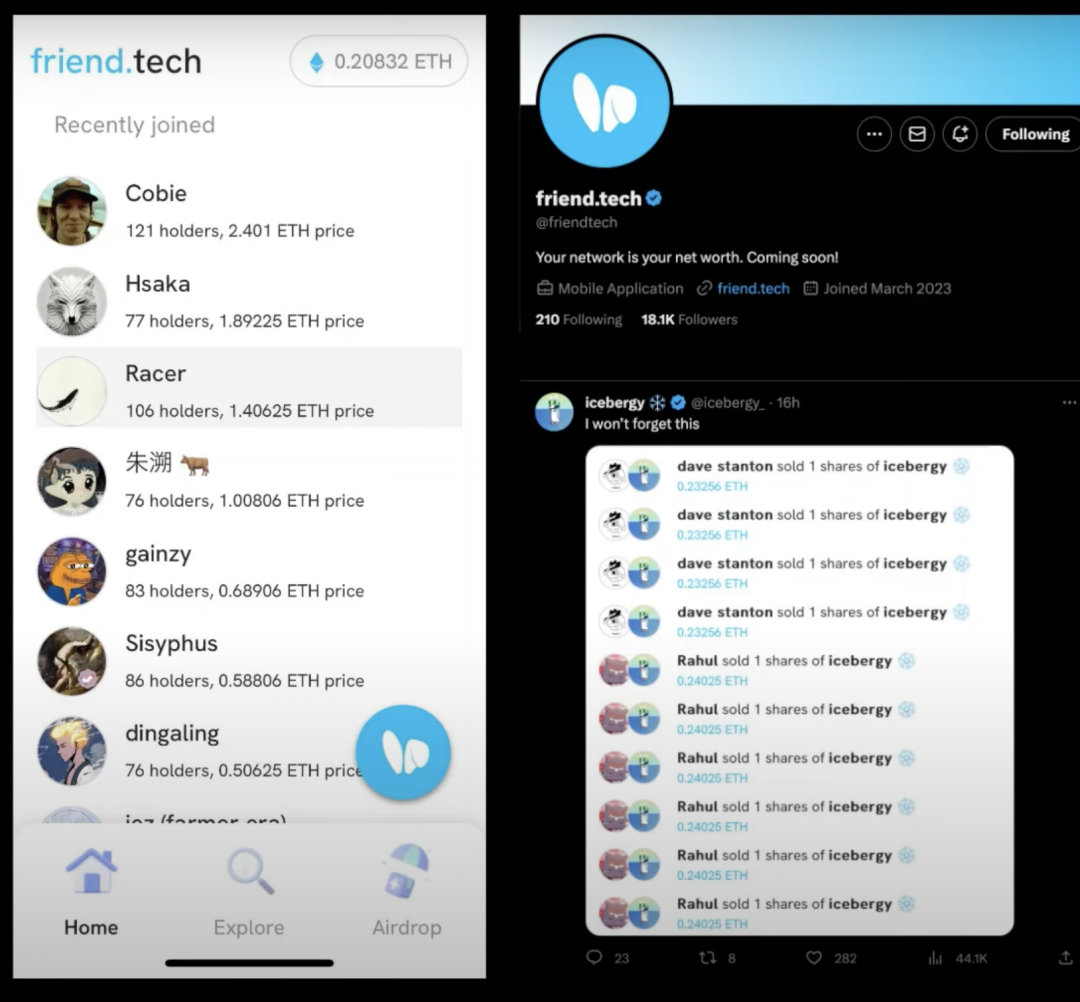

Friend.tech is a decentralized social platform that allows users to purchase shares of any Twitter user on Friend.tech through Ethereum on the Base chain, becoming shareholders and gaining the right to directly communicate with them, and making profits by buying and selling shares.

a. Economic Model

There is currently no clear economic model. The official website is relatively simple and has not yet released a white paper or roadmap. What is currently known is that an increase in shareholders for each token will cause the token to rise in price, and an additional 10% transaction fee is required for trading, with 5% going to the protocol and 5% to the creator.

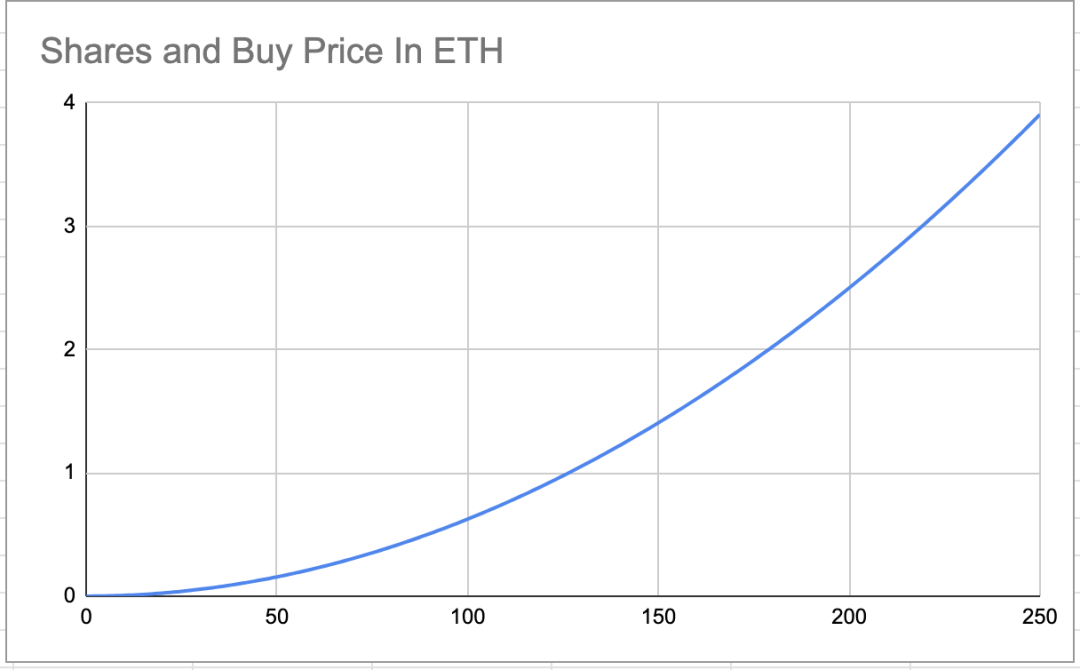

Unlike the linear growth of one dollar in Stealcam, Friend.tech should have modified the model parameters to make the price increase quadratically with the number of shareholders, achieving rapid price increases (calculated by @functi0nZer0 on Twitter, not yet officially confirmed):

The number of shares held by individuals and the price of the next share are determined by a quadratic relationship. The formula for calculating the price of the next share is S^2 / 16000 * 1 ETH, where S represents the current number of shareholders.

It is worth noting that in version 1.0 of stealcam, if the next player purchases the reveal right from you, your purchase cost will automatically be fully refunded, and you will earn the price difference. In version 2.0 of Friend.tech, adding a shareholder will only benefit the KOL and increase the per share price. As a trader, your paper profit has increased, but to realize the profit, you need to pay a 10% transaction fee and choose the right time to sell.

For users, trading friction has increased, and everyone is more inclined to lock their positions. On the other hand, the project has used this mechanism to create a more cohesive community (no longer just one-off transactions), helping early participants and KOLs achieve high returns and create a perfect wealth creation myth.

In summary, the three parties involved in Friend.tech's earnings are as follows:

- Protocol: Earn 5% transaction fee income for each transaction.

- KOL: Earn the spread between buying and selling prices. Regardless of whether the protocol is rising or declining, the transaction fee is paid by the buyer and seller of each transaction, ensuring that KOLs and the protocol always make a profit.

- Users: Become shareholders. Each increase in shareholders causes the token price to rise rapidly (attracting traffic through the wealth effect, thereby pushing up the token price). Since a 10% transaction fee is required for each transaction, short-term buying and selling cannot generate large profits, indirectly encouraging users to lock their positions. This pricing model has a very significant speed of both increase and decrease, and users bear all the risks.

b. Data Situation

Friend.tech is currently very popular, with a 24-hour protocol fee of $1.12 million, ranking third after Ethereum and Lido, surpassing Tron and Uniswap, and with 20,000 active addresses within 24 hours.

III. Author's Viewpoint

Friend.tech's marketing strategy combines the strengths of many, focusing on short-term, high-frequency, and intensive PR, making it a classic case in terms of content, timing, and community selection. Strategies include: early creation of mystery, KOL endorsement for cold start, hungry marketing with invite codes, and post-endorsement promotion by VCs.

The user growth strategy is also excellent, providing sufficient incentives and future expectations for KOLs and users, and achieving rapid explosive growth through the power of the community.

The Base community generally lacks risk awareness. Apart from the product, the Friend official website has not disclosed any project information. The overwhelming marketing focus is clearly on user growth, transaction volume, and comparison with first-tier communities, with little analysis of its tokenomics economic model. It seems to be intentionally downplaying certain aspects while emphasizing others, apparently aiming to trigger public FOMO sentiment.

Overall, it is a very Ponzi-like model, but it also has a strong wealth creation effect and community foundation. If a community culture and unique discourse system can be established before a collapse, it may continue. Conversely, if everyone buys and sells shares with a speculative mindset, a large number of sell-offs will occur after a critical price threshold or a token collapse, leading to a price collapse.

The introduction of a points system increases user activity, stimulates retail investors to further invest, and engage with their own tokens. However, from the perspective of explosive efficiency, although the Twitter user base is large, interacting with the Base chain and depositing/withdrawing funds is still a high barrier, which will likely need to be optimized in the future.

In terms of financing, it has already raised seed funding from Paradigm. It will be interesting to track the subsequent developments. The team can use this funding to distribute airdrops, allowing shareholders to earn additional income rather than simply engaging in speculative buying and selling of shares.

IV. Future Prospects: Creating a Growth Flywheel with Creator Economy + Tokenomics

It is still too early to judge the success or failure of this project, but Friend.tech's successful community marketing validates that Social+Fi is an extremely effective customer acquisition method. Properly distributing benefits and providing incentives for KOLs and retail investors to promote the community is undoubtedly the fastest and most native way to grow.

In a broader context, within the social race track products, the combination of Token and creator economy is feasible, especially providing token incentives for core creators to leverage their fan base for cold starts. This approach's Product-Market-Fit is beginning to take shape (at least ensuring that the project achieves good results in the first step of cold start breaking the circle). Based on this idea, future directions for further exploration include:

Web3 Only Fans: Users can unlock chat and encrypted images after paying, with fan tokens serving as an entry threshold and DID. Examples include PopPlanet. This model is suitable for the majority of mid-level and even amateur KOLs, with a large user base.

Co-creation of content: A community built around well-known IPs/NFT communities/creator groups, where creators attract more fans to participate, produce co-created works, and consume content to earn token rewards. Examples include storyverse and story protocol.

Fan investment economy: Online male and female idol groups, online esports, etc. Relying on the influence of idols to attract fans to purchase web3 support products, while the artists themselves can earn a higher share of the profits. This model is highly dependent on a single IP and requires high visibility.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。