The trillion-dollar tokenization of physical assets is caught on these three key issues.

Written by: Prathik Desai

Translated by: Chopper, Foresight News

Asset tokenization is merging two entirely different financial systems: one is a permissionless network of DeFi operating around the clock with second-level price fluctuations; the other is a traditional fund that settles on a fixed schedule and is only open to qualified investors on a whitelist.

Bridging the fusion process of the two is extremely complex, but whoever can build this connecting infrastructure will capture enormous industry value. This article will break down who is building the middle layer connecting on-chain and traditional finance, and where the value will ultimately flow.

Continued Expansion of RWA Scale

Currently, the total scale of on-chain physical asset tokens has surpassed 33 billion USD, including approximately 15 billion USD in tokenized U.S. Treasury bonds. Interestingly, in just one year, the share of U.S. Treasury bonds in the overall RWA has dropped from 55% to less than 45%. New types of tokenized funds, such as institutional credit (e.g., Apollo's ACRED) and private credit (e.g., J.P. Morgan's JAAA), are growing rapidly.

Asset tokenization is maturing and providing CFOs with layered risk management tools. Institutions seeking low volatility, high liquidity, and low yield can choose Treasury-type token products, while those pursuing high yield and programmability can allocate to higher risk categories. Nowadays, these types of Treasury-backed token products are all verified by traditional Big Four auditing firms, and the safety of returns is no longer the biggest pain point.

If someone asks me what the difference is between on-chain assets and traditional assets, the answer is composability. Relying on composability, the same dollar capital can circulate across multiple tracks to achieve compound returns. Instant redemption and multi-channel reuse of funds make tokenized funds akin to leveraged traditional asset management products.

In the traditional financial system, it is difficult to achieve a balance among returns, liquidity, and capital turnover speed. Well-operated tokenized products can simultaneously consider all three. However, the threshold for "well-operated" is extremely high, and bridging the composability of traditional funds with on-chain DeFi presents many engineering and compliance challenges.

Stitching Two Distinct Worlds Together

Blockchain brings rapid settlement and low-cost advantages to tokenized physical assets, but the essence of tokenized money market funds remains that they are compliant asset management products, not stablecoins.

They still need to update the net asset value once every working day according to the fund manager's schedule. They still need to maintain a KYC-verified holder population. For example, BlackRock's BUIDL has a minimum investment threshold of 5 million USD, while Circle's USYC is only available for non-U.S. persons. They still need to comply with redemption deadlines because the settlement of the underlying treasury securities depends on off-chain infrastructure, which has a settlement deadline of 5 PM Eastern Time.

These are hard requirements that cannot be avoided. If daily net asset value calculation is removed, the product no longer qualifies as a money market fund; if whitelist free trading is allowed, it will directly invite SEC regulatory inquiries.

So how can share tokens achieve internet-level high-speed circulation while retaining fixed net asset value update cycles, limiting qualified holders, and redemption time windows? The industry needs specialized infrastructure to achieve periodic net value calculation, phased settlement, and strict compliance isolation across chains. The joint report from LayerZero and Centrifuge provides this solution.

Three Core Conflicts are Key to Successful Integration

The intermediate scheduling layer must resolve three groups of fundamental contradictions to allow fund assets to circulate rapidly without touching regulatory red lines.

First is pricing.

How should tokens be priced during the daily net asset value update interval? Some issuers directly freeze the previous day's net value, which can easily lead to arbitrage during daytime interest rate fluctuations; real-time dynamic pricing is more market-aligned, but it is hard to match the daily accounting of traditional funds.

Second are compliance factors.

Should whitelist verification be applied at every step of the transaction or unified at the treasury layer? If every transfer requires identity verification, tokens cannot connect to open DeFi at all; if a treasury encapsulation model is used, the treasury holds compliant fund shares, and only KYC users can exchange for circulating receipt tokens, with compliance verification completed once, allowing receipt tokens to freely participate in various DeFi, Centrifuge's deRWA framework embodies this thought.

The third conflict occurs when transferring assets across chains.

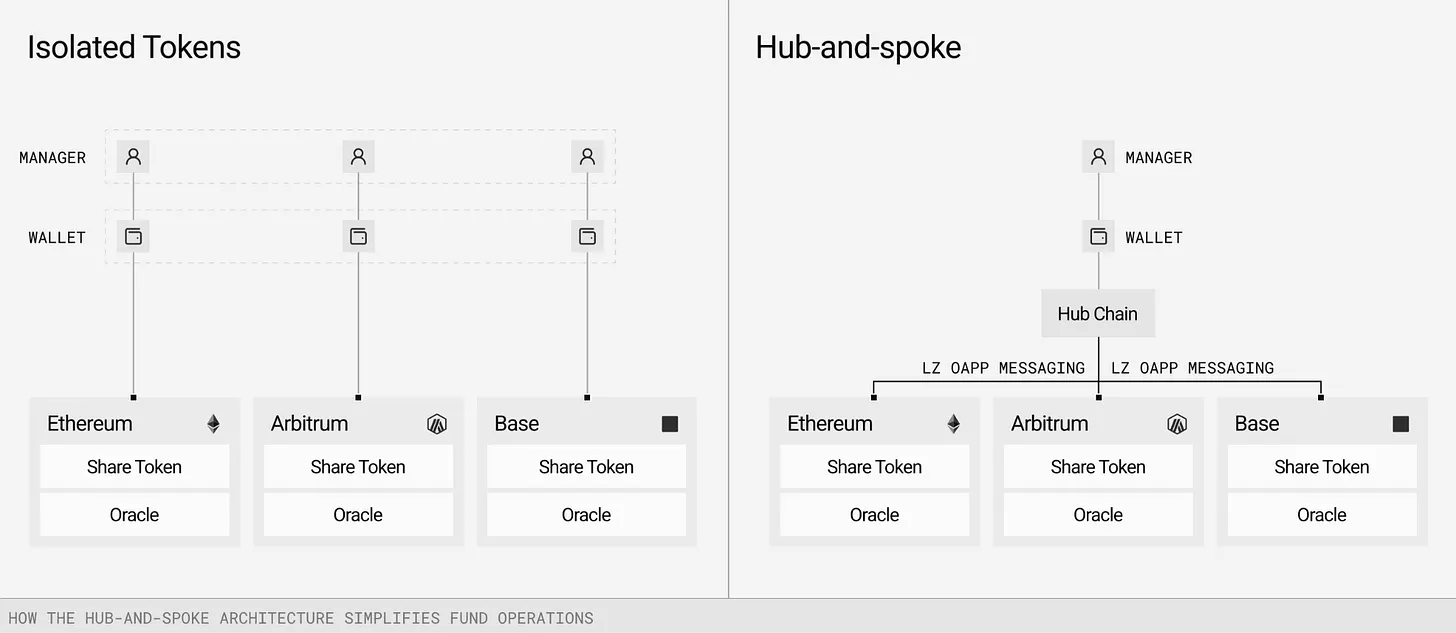

When a fund is deployed across multiple public chains, there must be a unified authoritative data source recording holders and asset valuations. While on-chain data can be updated in real-time, synchronizing across nine chains can easily introduce errors; the more points of failure, the higher the probability of mistakes.

LayerZero and Centrifuge adopt a central radiation architecture to solve this problem. In this model, one authoritative chain is responsible for managing net value, accounting, and compliance. The messaging layer (coordinated by LayerZero in this case) pushes these updates to the radiation chains where the tokens are actually used.

Centrifuge V3 architecture is built based on this model, selecting one hub chain as the sole data source for each asset pool, with branch chains serving only as distribution nodes while also providing open DeFi composability; LayerZero is responsible for cross-chain synchronization of net value, compliance instructions, and user holding data.

This cross-chain scheduling system builds extremely high industry barriers. The authoritative accounts of the funds are maintained by a single set of infrastructure, making them highly irreplaceable. Asset management institutions are responsible for offline net values and compliance rules, while blockchain provides on-chain composability; the intermediate scheduling layer is indispensable, leading to a highly concentrated industry value.

The accounting of assets in transit across chains is the weakest link. During asset transfers across chains, they temporarily fall outside the visible range of the fund's balance sheet. Centrifuge V3 introduces an in-transit asset voucher mechanism, maintaining continuous accounts during the cross-transfer of assets, corresponding to traditional financial transaction ledger standards, seeming basic but is an essential function for institutional entry.

Despite these conflicts, why should institutional investors still consider tokenized funds?

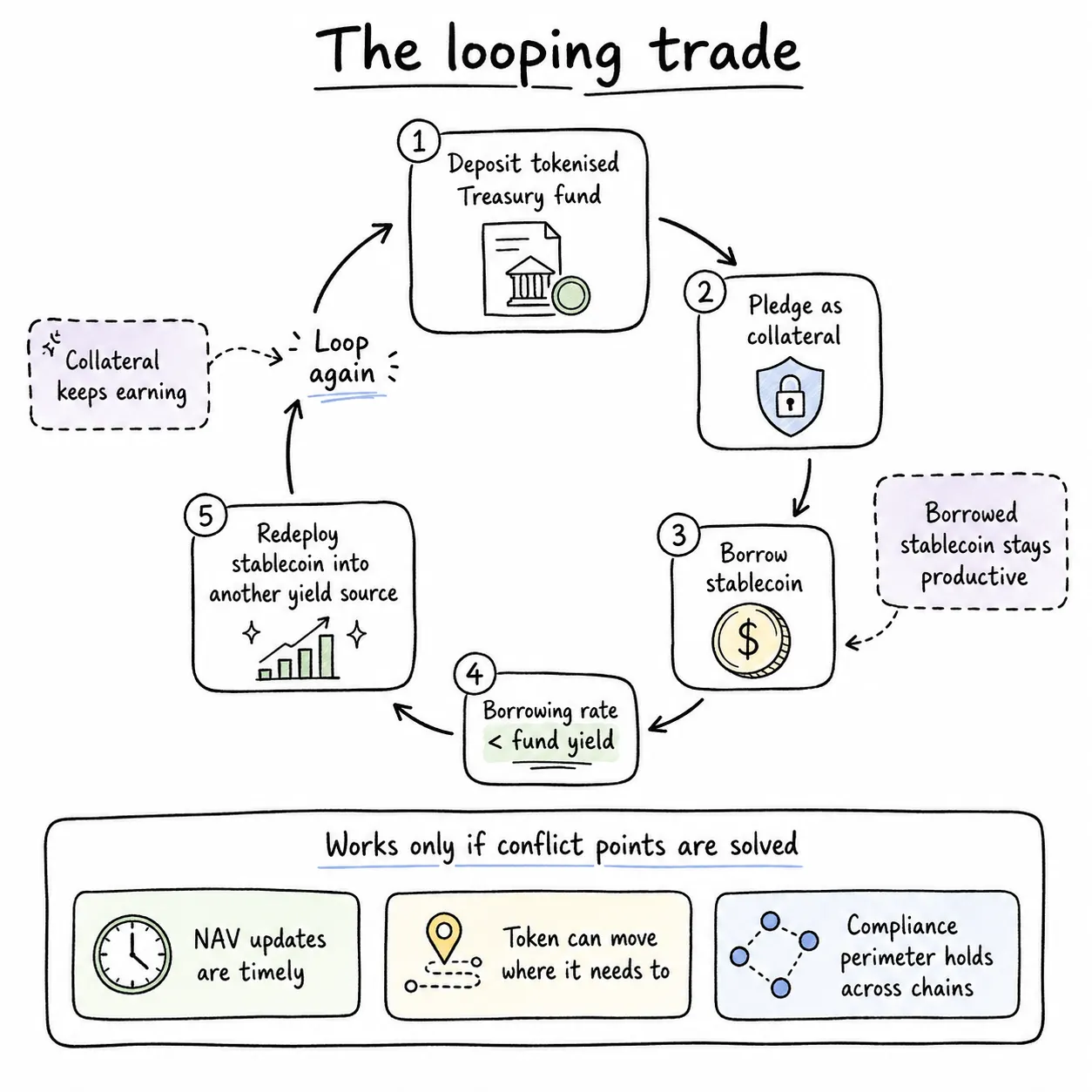

The core advantage is cyclical pledge arbitrage. Corporate financial entities deposit into tokenized U.S. Treasury funds, pledging shares to borrow stablecoins; if the lending rate is lower than the yield of the Treasury fund, the position naturally generates a positive yield spread; the borrowed stablecoins can be reinvested in another yield-generating asset, infinitely magnifying cash flow returns.

The entire set of cyclical arbitrage relies on all three of the previously mentioned conflict points being properly resolved. In the past, the industry experienced significant arbitrage opportunities due to mechanistic loopholes: small token products lagging 2-4 hours in net value updates allowed interest arbitrage funds to enter early. Redemption conflict risks are also not to be ignored, as the underlying assets in the over-the-counter market may hit redemption limits while on-chain smart contracts continue to process instant redemptions, creating numerous unmatched orders.

Currently, large private credit funds and business development companies are facing this situation. Two weeks ago, Apollo's 26 billion USD private credit fund ADS encountered a run, with redemption requests reaching a total of 16.8% of shares; the platform could only set a daily redemption limit of 5%. If that product were to issue tokens simultaneously, the conflict between on-chain real-time redemptions and off-market redemption limits would arise directly. In the second quarter of this year, large private credit funds had redemption requests totaling 15.6 billion USD, higher than 13.9 billion USD in the previous quarter.

Cross-chain communication outages and semi-settlement of assets are also high-frequency risks. Each type of failure in the entire system must have licensed institutions bear regulatory accountability in order to gain the trust of institutional funds.

Tokenization is not merely putting U.S. Treasury bonds on-chain and introducing a new type of digital asset. Infrastructure builders must break traditional shackles, allowing investors not to have to choose between return, liquidity, or capital turnover. If the token system can achieve multiple appreciation uses of a single capital while maintaining the regulatory risk control bottom line, institutions holding trillions in cash will inevitably scale up their investments.

Last week's article mentioned that SWIFT, as the funds scheduling layer, has a value far exceeding both ends of the banks, and the profitability of the Visa system also nearly surpasses all partner banks except JPMorgan Chase. In the iterative process of the financial industry, whoever controls the middle scheduling layer can lock in the capital market dividend for the next decade. Centrifuge is deeply engaged in fund-end infrastructure, while LayerZero builds the foundational cross-chain communication; together they occupy this core track.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。