Written by: Rita

Trends Guide

On July 2, Morgan Stanley updated its NAND industry supply-demand model, predicting that AI demand will continuously create a gap that will last until 2027, but the situation on the consumer electronics side is quite different. After several rounds of price increases in the second quarter, Morgan Stanley has begun to see actual order reductions from smartphone and PC customers, indicating that the pricing for consumer products may soon reach a ceiling.

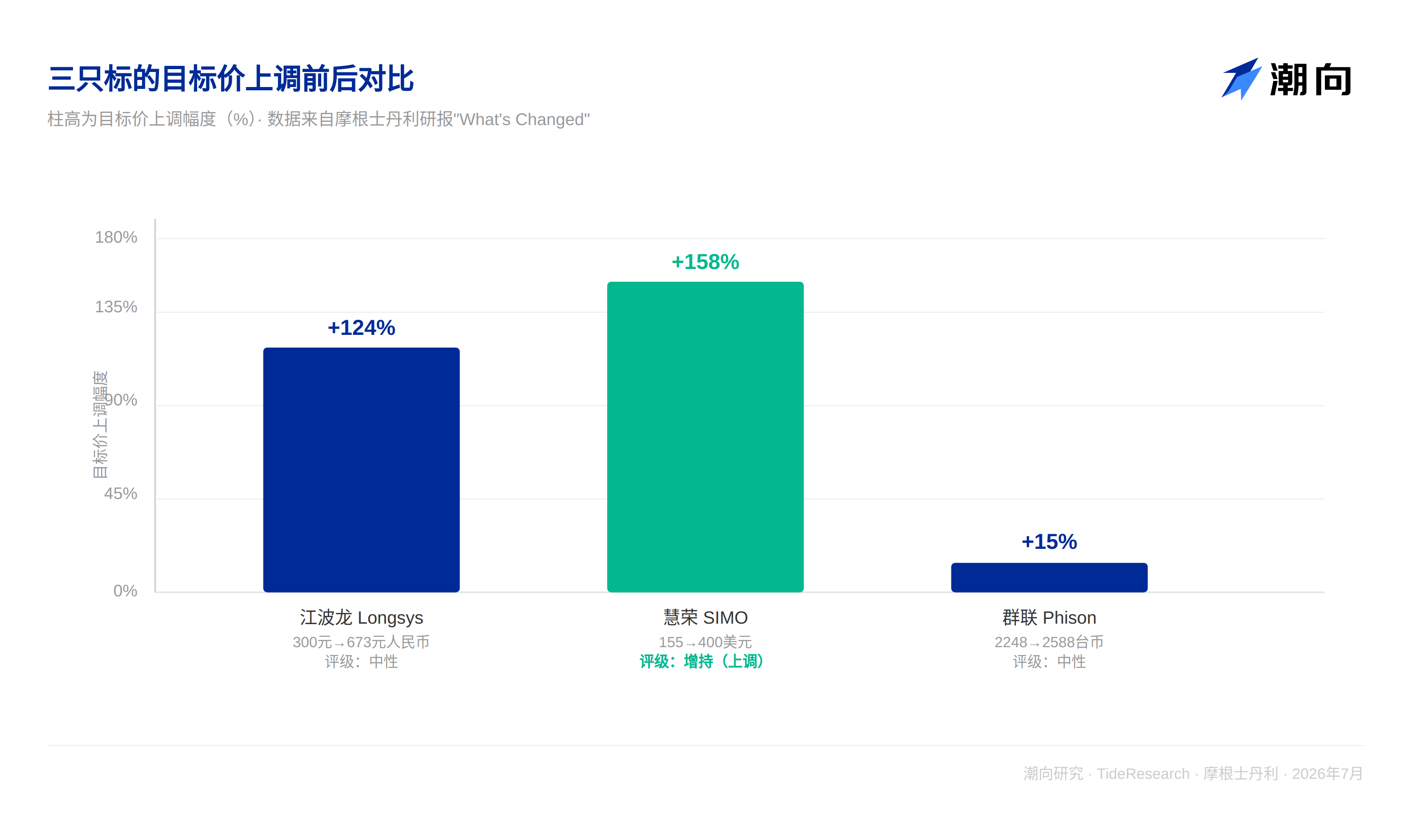

The most direct signal from this update is the significant upward revision of the target prices for three companies: Longsys target price raised from 300 RMB to 673 RMB, Silicon Motion target price from 155 USD to 400 USD, and Phison target price from 2248 TWD to 2588 TWD. Morgan Stanley maintains a neutral rating on Longsys and Phison, the target prices have increased, but the rating remains unchanged, and the reasoning is worth examining.

AI Demand Continues to be Short, Consumer Side has Started to Hit the Brakes

Morgan Stanley updated its global NAND supply-demand forecast for 2026 to 2027 and conducted a scenario analysis for capacity expansion and AI demand growth in 2028. The results show that a significant supply shortage will persist until 2027; entering 2028, as processes migrate and new capacities are released, the gap is expected to narrow. If AI-related NAND demand grows 60% year-on-year and capacity expansion is in line with the current baseline scenario, the gap could narrow to around 5%. However, under a pessimistic scenario where China's restrictions are relaxed and supply discipline eases, there is a risk of excess supply.

The overall demand on the server side remains strong, and long-term supply agreements (LTA) provide price protection against declines. The consumer side shows clear differentiation: the inventory levels of module manufacturers and distributors are rising, and smartphone and PC customers are facing increasing pressure in balancing shipment volumes and profit margins. Morgan Stanley points out that this is not a new change, but after price increases in the second quarter, actual order reductions have started to appear. The pricing for consumer-grade products may indeed reach a peak in the short term, and suppliers are shifting production capacity toward AI, which will continue to squeeze the shipment volumes on the consumer side.

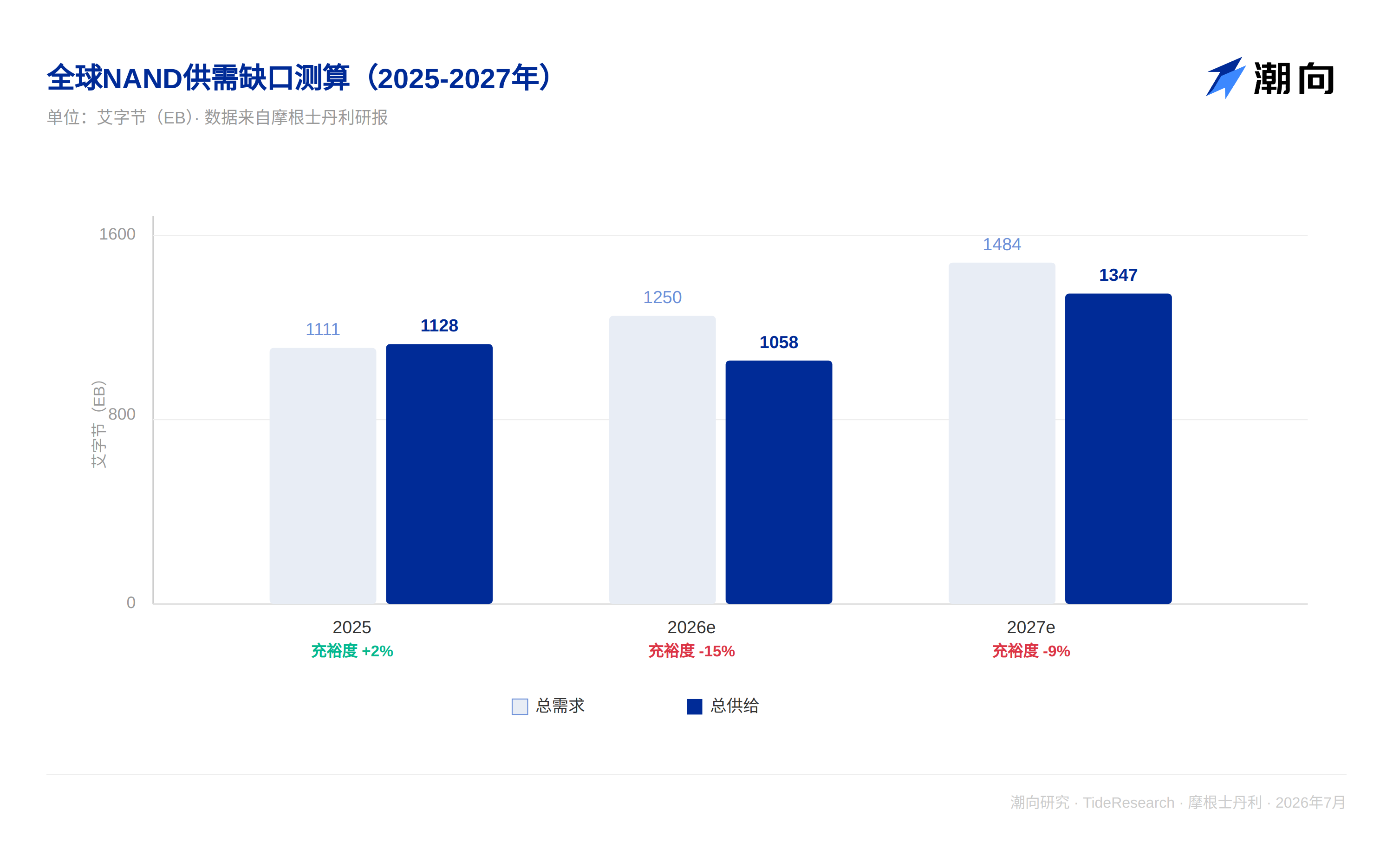

Supply-Demand Model: Gap Not Closed by 2027, 2028 Depends on Yangtze Memory Technologies

Morgan Stanley estimates that AI-related NAND demand will grow approximately 60% year-on-year in 2027, resulting in a 9% supply-demand gap. According to the report's model, global NAND total demand will grow from 1111 EB in 2025 to 1484 EB in 2027, while total supply will grow from 1128 EB to 1347 EB, with supply adequacy dropping from 2% positive in 2025 to -15% in 2026 and -9% in 2027. The share of AI in total NAND demand will also rise from 18% to 41%.

Morgan Stanley believes that the biggest variable in 2028 is Yangtze Memory Technologies (YMTC). This Chinese NAND manufacturer is currently building both Fab4 and Fab5, each with a planned capacity of 100,000 wafers per month. If all of this is directed toward NAND production, along with the five already announced fabs, it theoretically could capture 24% of the global NAND market share. Scenario testing shows that if YMTC's capacity is controlled at a baseline level of 310,000 wafers/month and AI-related SSD demand grows 60% year-on-year, the supply gap could remain at around 6%; however, if the five fabs are fully ramped up to 470,000 wafers/month while AI demand growth slows to 30%, a near 9% surplus could occur. Whether supply is tight largely depends on whether Chinese manufacturers are willing to hit the brakes.

Target Prices for Three Companies Surge, Ratings Remain Unchanged

Longsys' target price has been raised from 300 RMB to 673 RMB due to pricing trends better than expected. Morgan Stanley is also more confident in the assessment of the gap in 2027, predicting an increase in its earnings per share by 299%, 247%, and 244% for 2026, 2027, and 2028 respectively. Phison's target price has been raised from 2248 TWD to 2588 TWD after second-quarter earnings significantly exceeded expectations, and the third quarter is expected to be the peak of the year. However, Morgan Stanley believes this strength is more cyclical; as low-cost inventory is depleted and consumer electronics weaken in the fourth quarter, revenues and gross margins will likely see a clear decline. Morgan Stanley maintains a neutral rating on both companies, reasoning that module manufacturers have limited bargaining power in this cycle, and suppliers have already tilted production capacity toward cloud vendors, which has limited the growth of shipment volumes for module manufacturers.

Silicon Motion's situation is different. Its target price has been raised from 155 USD to 400 USD, corresponding to a projected price-to-earnings ratio of 23 times for 2027, above its historical average of 20 times since 2019. Morgan Stanley is optimistic about Silicon Motion's expansion from consumer controllers to enterprise SSDs and AI server startup disks, expecting the startup disk and related SSD business to account for 23% and 26% of its total revenue in 2026 and 2027, respectively. The share of its enterprise SSD business MonTitan is expected to increase from 5% in 2026 to 19% in 2028, making it the only one among the three companies whose rating and target price were raised in tandem by Morgan Stanley.

Who Does Morgan Stanley Favor Most?

In the DRAM camp, Morgan Stanley lists Samsung Electronics as the top choice for the Asia tech team due to its market leadership and stronger shareholder return potential; in the NAND camp, Kioxia is the preferred choice of the Japan semiconductor team, with Morgan Stanley expecting its annual free cash flow for FY2027 to FY2028 to reach 400 billion to 500 billion JPY. Management has also hinted at a significant portion of accumulated cash flow could be returned to shareholders. Macronix is the preferred choice of the Greater China semiconductor team, benefiting from a continually tight SLC/MLC NAND supply. Morgan Stanley also maintains "buy" ratings for Micron, SK Hynix, and SanDisk, naming Phison as a key supplier of SanDisk's enterprise SSD controllers, believing it is shifting from a recovery story to a structural growth story.

Trend Perspective

What is most worthy of consideration in this adjustment is that Morgan Stanley has separated the treatment of ratings and target prices. Both Longsys and Phison saw their target prices increase by double digits, yet their ratings remained unchanged, indicating that Morgan Stanley acknowledges that short-term pricing has indeed been better than expected, but they do not believe this will change the bargaining position of module manufacturers in the supply chain. The only company with synchronized upgrades in rating expectations is Silicon Motion, supported by its expansion into new businesses like enterprise SSDs and AI startup disks, rather than merely riding the wave of this round of NAND price increases. For investors, this report conveys the signal that whether the short-term rise in NAND prices can lead to upgrades in individual stock ratings largely depends on whether the company is moving toward more negotiable areas such as AI servers and enterprise storage, rather than simply benefiting from industry cyclical price increases.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by Trend Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the respective brokerage analysts and represent the positions of their affiliated institutions, not the views of Trend Research, nor do they constitute any investment advice.

The market has risks, decisions should be independent. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。