Author: Chloe, ChainCatcher

In June 2026, more than a dozen of the largest banks in the United States jointly announced their plans to build a shared tokenized deposit network before 2027, directly confronting the erosion of deposits by stablecoins. As of now, this system has not been named; some in the industry refer to it as “the bridge,” while others call it “the chain.”

This reflects a concept that has been overlooked by the market for many years but is now quietly making a comeback: consortium blockchains.

Banks form an Avengers alliance

On June 5, 2026, The Wall Street Journal broke the news that a group of major U.S. banks, led by JPMorgan Chase, Citigroup, and Bank of America, plans to establish a shared tokenized deposit network by the first half of 2027.

Later that day, these banks issued a joint press release, expanding the list from four to more than ten. Wells Fargo is the initiator, followed by BNY, BMO, HSBC, PNC, TD, U.S. Bank, Truist, Citizens, Fifth Third, Huntington, KeyBank, Regions, and Santander.

The operator is The Clearing House, a payment company jointly established by these banks. This system still does not have a formal name; according to The Wall Street Journal, some in the industry call it the bridge, while others call it the chain.

In the past two years, the cryptocurrency space has mainly focused on universal public chains, token issuance, and airdrops. However, the institutional funds and technology that are really moving quietly are taking another direction: dedicated chains that are purpose-driven, led by specific institutions, and may not necessarily issue tokens. This sounds familiar because it embodies the spirit of the "consortium blockchain" of the past; this time, it may be for real.

What banks are afraid of is stablecoins stealing deposits

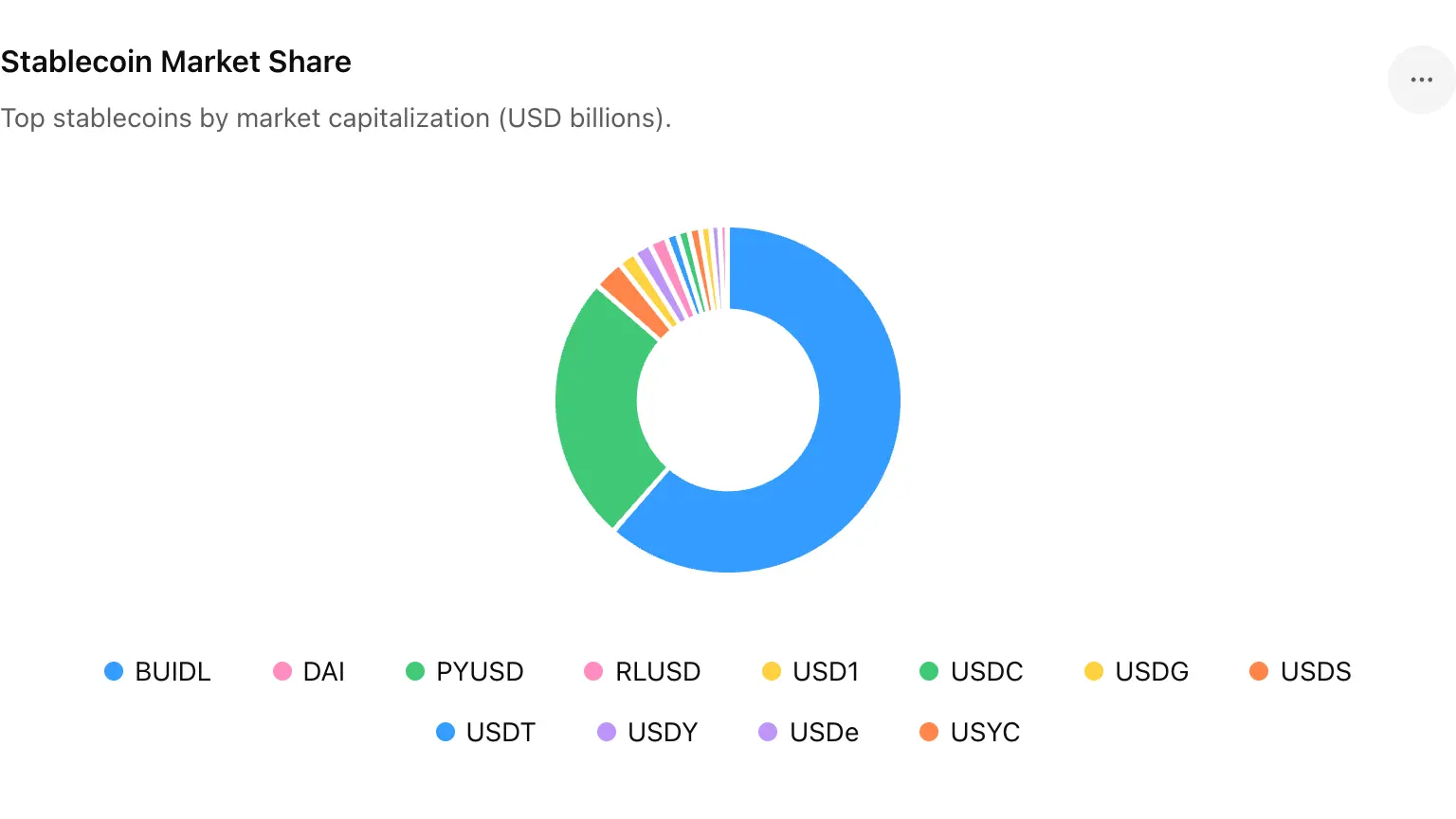

To understand this counterattack, one must first know what traditional finance is guarding against: stablecoins. According to DeFiLlama data, as of June 2026, the total market capitalization of stablecoins worldwide is approximately $316 billion. USDT alone accounts for about 62%, with a market cap of around $186 billion, while USDC has about $75 billion; together, these two account for about 80% of the entire market.

According to Bitrue, stablecoins handled approximately $46 trillion in transaction volume throughout 2025, which is more than 20 times that of PayPal and nearly three times that of Visa. By the first quarter of 2026, stablecoins accounted for approximately 75% of the overall cryptocurrency trading volume. The stablecoin sector is no longer merely a chip for speculative trading but rather a global payment and settlement pipeline that operates daily.

For traditional bankers, this pipeline directly threatens their lifeline: deposits. How much banks can lend is determined by how much they have in deposits. Once customers become accustomed to moving their money from bank accounts to crypto wallets in stablecoins, the foundation for banks to lend disappears. Mark Monaco, the global payments head at Bank of America, stated that this system is being prepared for the day when demand truly arises.

What truly compels banks to take proactive action is the deregulation. The U.S. GENIUS Act has been enacted, requiring 1:1 adequate reserves for stablecoins, along with regular audits. The implementation details are set to take effect on July 18, 2026. The significance of this legislation lies not in its constraints on stablecoins but in legitimizing them. As stablecoins transition from a gray area to a licensed, audited, and bank-custodian tool, their substitutive nature for traditional deposits is no longer hypothetical.

Banks are not suddenly in love with blockchain; they are being pressured by someone who has already laid the tracks at their doorstep, forcing them to lay down their own.

Bridge or Chain? What exactly is this network

Back to that yet-to-be-named chain. Its technical name is the Regulated Settlement Network (RSN). The approach involves converting bank deposits into tokens recorded on the blockchain, facilitating year-round, 24/7 real-time settlements without waiting for the next business day.

“Tokenized deposits” are not a new digital asset; rather, they are the same deposits recorded in a different way. They carry the same credit risks, are subject to the same regulations, and remain within the bank system protected by deposit insurance. This is the fundamental difference between them and stablecoins: stablecoins move money out of the banking system, whereas tokenized deposits keep money within the system but gain the velocity and programmability similar to cryptocurrencies.

David Watson, CEO of The Clearing House, mentioned that this is a significant move for banks, describing blockchain payments as heading towards a completely different future; Max Neukirchen, co-head of global payments at JPMorgan Chase, offered a more pragmatic view, stating that maintaining stability and resilience in the payment ecosystem requires a regulated market infrastructure to settle these tokenized deposits.

As of the time of this disclosure, the network has not yet determined which blockchain to use. The technology has not been finalized, nor has a name been firmly established, oscillating between bridge and chain. However, more than a dozen of America’s largest banks are willing to print their names together on the same press release. At this stage, more than technology, what has been agreed upon first is governance: who will operate, who can enter, and who decides the rules. The answers to these three questions encapsulate the essence of consortium blockchains.

Reviewing the failure of consortium blockchains last time

From 2016 to 2022, that was the first wave of enthusiasm for enterprise blockchains. JPMorgan Chase experimented on Ethereum as early as 2016, later developing its private chain Quorum; IBM and the Linux Foundation promoted Hyperledger Fabric, and R3 led Corda, but then almost everyone fell silent.

The reasons are not complicated. At that time, consortium blockchains were stuck for two reasons: first, there was no compelling reason to cooperate, and each bank built a closed chain that did not connect with others, ultimately turning into a collection of isolated islands; second, permissioned ledgers, in many scenarios, were essentially a database with enhanced cryptography. They had technology first and then looked for problems afterward. By 2020, the market narrative had completely shifted toward public chains, DeFi, and liquidity mining; consortium blockchains were labeled as “on-chain but not in the right place,” gradually fading from the central discussion.

Reflecting on this past, it draws a parallel to today’s situation. Consortium blockchains did not fail due to technology; they failed because no one really needed them. What makes them visible again in 2026 is precisely what was lacking back then: real, urgent, and regulated demands; back then, it was technology trying to force scenarios, but this time it is scenarios looking for technology.

From the data: Institutional-level consortium blockchains are quietly operational

The tokenized deposit network is not an isolated event. Over the past eighteen months, several institution-led dedicated blockchains have accumulated measurable usage scale, among which the most comprehensive data comes from Canton Network.

Canton, developed by Digital Asset, is a public permissioned blockchain that uses Daml to write smart contracts, designed to allow competing financial institutions to share the same settlement infrastructure while preserving privacy; its super validators include Visa, Nasdaq, and BNP Paribas.

In terms of usage scale, by the end of 2025, over 700 institutions had connected to Canton. The network's largest application, Broadridge's Distributed Ledger Repurchase platform (DLR), processes around $40 trillion in tokenized U.S. Treasury repurchase volume each month, equivalent to about $280 billion per day, and this figure doubled in 2025 from $20 trillion per month.

In December 2025, the U.S. central securities depository, DTCC, announced a partnership with Digital Asset to tokenize its U.S. Treasuries on Canton, with an expected scale expansion in the second half of 2026. DTCC is the core institution for U.S. stock and fixed income clearing and settlement, and its participation signifies that institutional-level chains have extended to the underlying infrastructure of the U.S. market.

Data at the level of individual banks is equally specific. JPMorgan Chase's blockchain department, Kinexys, has been processing institutional payments on a private chain using JPM Coin since 2020, currently handling more than $5 billion daily. Citi's Token Services has launched to support real-time cross-border transfers among New York, London, and Hong Kong. BNY also launched a tokenized deposit service for institutions in January 2026.

Taken together, these data point to the positioning of the tokenized deposit network as an interoperability layer connecting existing projects among banks, rather than a brand new chain. The driving force is not technology suppliers, but banks that have accumulated real transaction volumes, seeking a common standard that can link them together.

The line between public chains and consortium blockchains is being blurred by insiders

Examining JPMorgan Chase's layout reveals that while it is deeply cultivating its private chain Kinexys, it also moved its JPM Coin deposit token (JPMD) to the public chain Base on Coinbase in June 2025. Not long after, in January 2026, it deployed JPMD natively on Canton, becoming the second chain to host such institutional digital cash after Base.

The same bank is betting on private chains, public permissioned chains, and public chains all at once.

Earlier, DBS Bank from Singapore and Kinexys also finalized a collaboration in November 2025 to develop an interoperability framework that allows tokenized deposits to transfer across each other’s chain ecosystems. What the industry genuinely cares about is no longer a binary choice between “consortium blockchain or public chain” but rather how “permissioned issuance” aligns with “cross-chain settlement.”

For banks, public chains are a channel to reach funds and users, while consortium blockchains serve as the underlying settlement layer, fulfilling the needs for privacy and compliance. The two are not opponents but rather two segments of the same chain, one before the other. The revival of “consortium blockchains” doesn’t bring back the closed, uncommunicative version of 2018; rather, it reintroduces its governance essence: fixed purposes, institutional dominance, and rule precedence. The difference is that this time, this essence has been translated into a new body capable of connecting with public chains.

Conclusion: What is truly at stake is who controls the infrastructure

The mainstream narrative over the past few years has been “decentralization will eventually replace traditional finance.” However, what is unfolding in 2026 is a different version: traditional finance has not been replaced; it has simply extracted blockchain technology from the realms of public chains, token issuance, and DeFi, and reconnected it back to its most familiar track: regulated, licensed, institution-led logic.

The difference between this logic and that of consortium blockchains lies in the fact that this time, it carries stablecoins’ validated real demands, the regulatory path paved by the GENIUS Act, and the actual transaction volumes generated by Canton and Kinexys; it is no longer just a technical proposition but a set of facts that are already operational.

The question of whether public chains or consortium blockchains will win has never been the focus. When the functional distinctions between tokenized deposits and stablecoins are no longer obvious, the endpoint of competition is not the product itself but whose infrastructure is recognized as the default choice first. The real gamble on this table concerns whose name the financial infrastructure will hang under in the next decade.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。