Author: Tanay Jaipuria

Translation: Shenchao TechFlow

Senchao Guide: Yushu Robotics is about to IPO on the Science and Technology Innovation Board of the Shanghai Stock Exchange, raising $620 million, and the prospectus unveils the complete financial data of a profitable robotics company for the first time. This company is forecasted to ship 5,500 humanoid robots in 2025, ranking first in the world, but 74% are sold to universities for research, with real industrial scenarios accounting for only 9%—this is the current truth of the robotics industry: hardware has been established, but commercialization is still waiting for AI models to catch up.

Yushu Robotics recently submitted an IPO application to the Science and Technology Innovation Board of the Shanghai Stock Exchange, planning to raise $620 million. This prospectus is quite interesting as it clearly shows us the real state of the current robotics market.

Yushu is profitable, growing rapidly, and ranks first globally in humanoid robot shipments.

This article will discuss:

- What Yushu produces

- The transition of revenue structure toward humanoid robots

- Who is buying robots (and why)

- Vertical integration strategies

- Financial condition

- Aspirations for the model layer

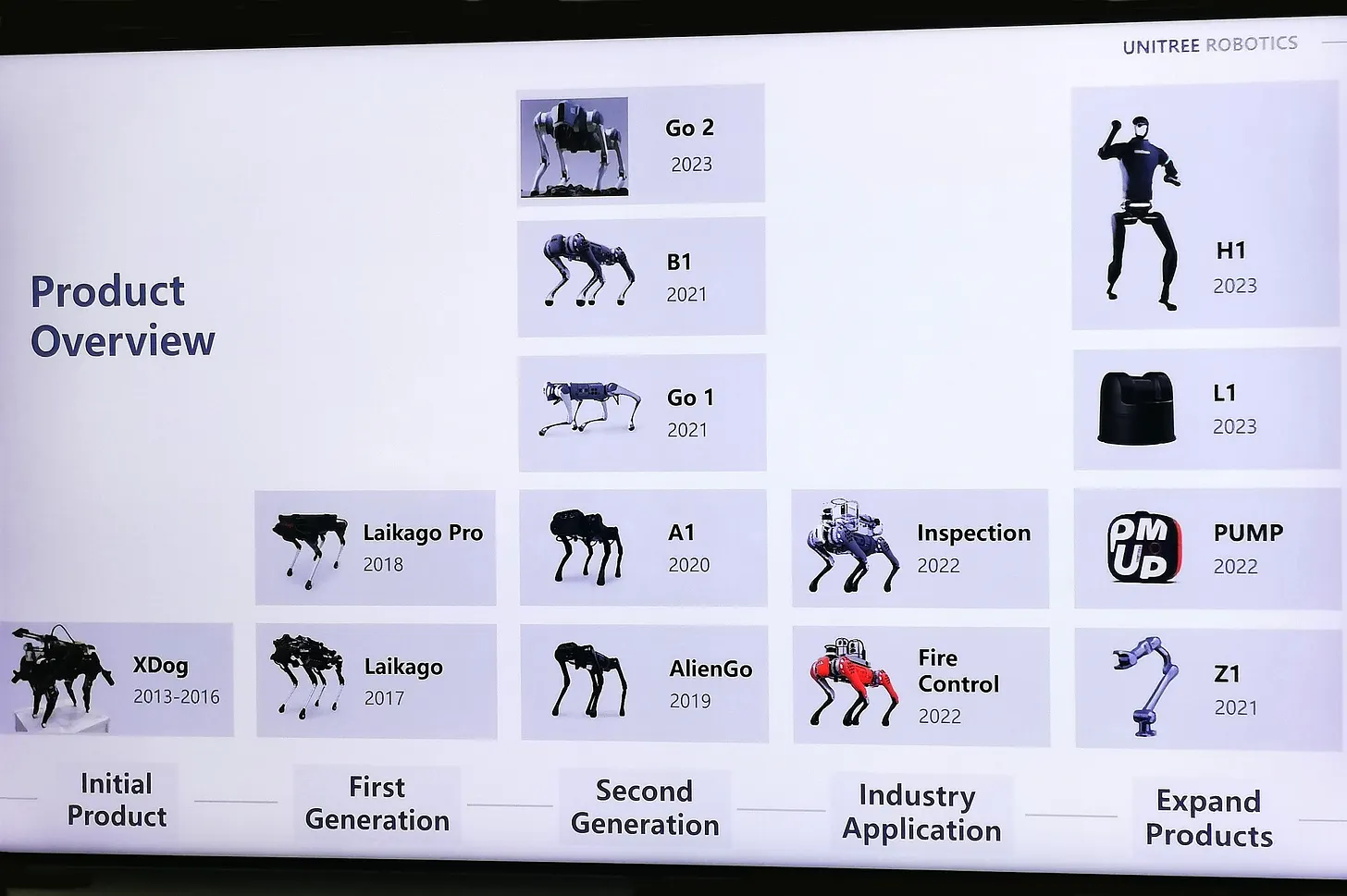

1. What Yushu Produces

Yushu was founded in 2016 and is located in Hangzhou. Its founder, Wang Xingxing, is a self-taught robotics expert who built the first quadruped robot in his apartment. The company currently has 480 employees, of whom about 175 are engaged in R&D.

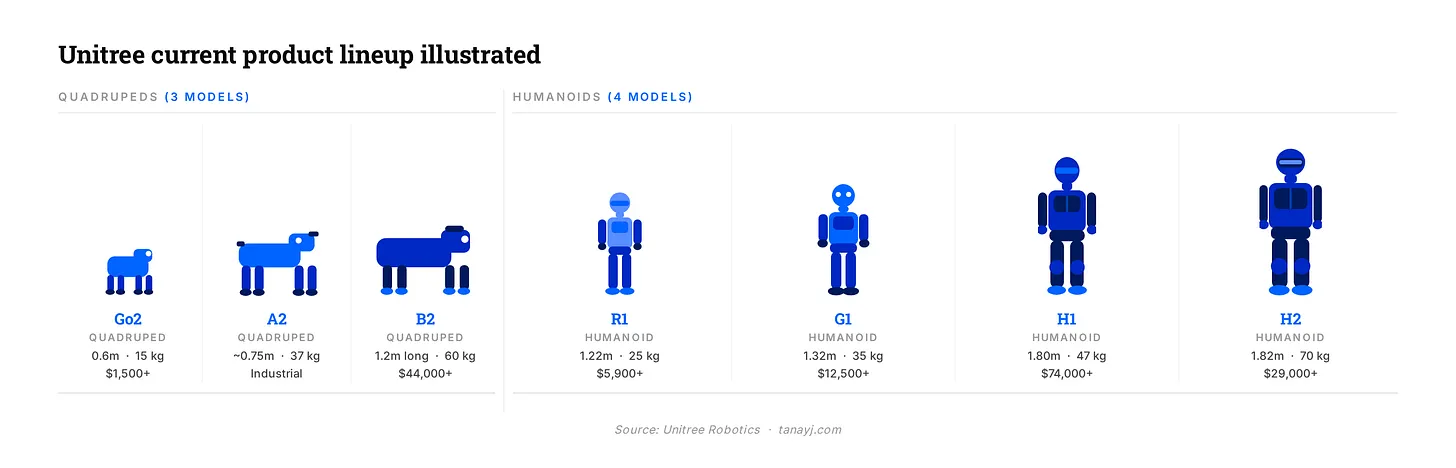

The company sells two categories of product lines:

Quadruped robots: Go2 (consumer and research level), B2 (industrial level), and A2

Humanoid robots: H1, H2, G1, and R1. G1 is the one you may have seen in viral videos, standing 1.32 meters tall and weighing 35 kilograms.

The company began international sales in 2018. Over 35% of its revenue comes from regions outside China, including a large number of academic customers in the United States.

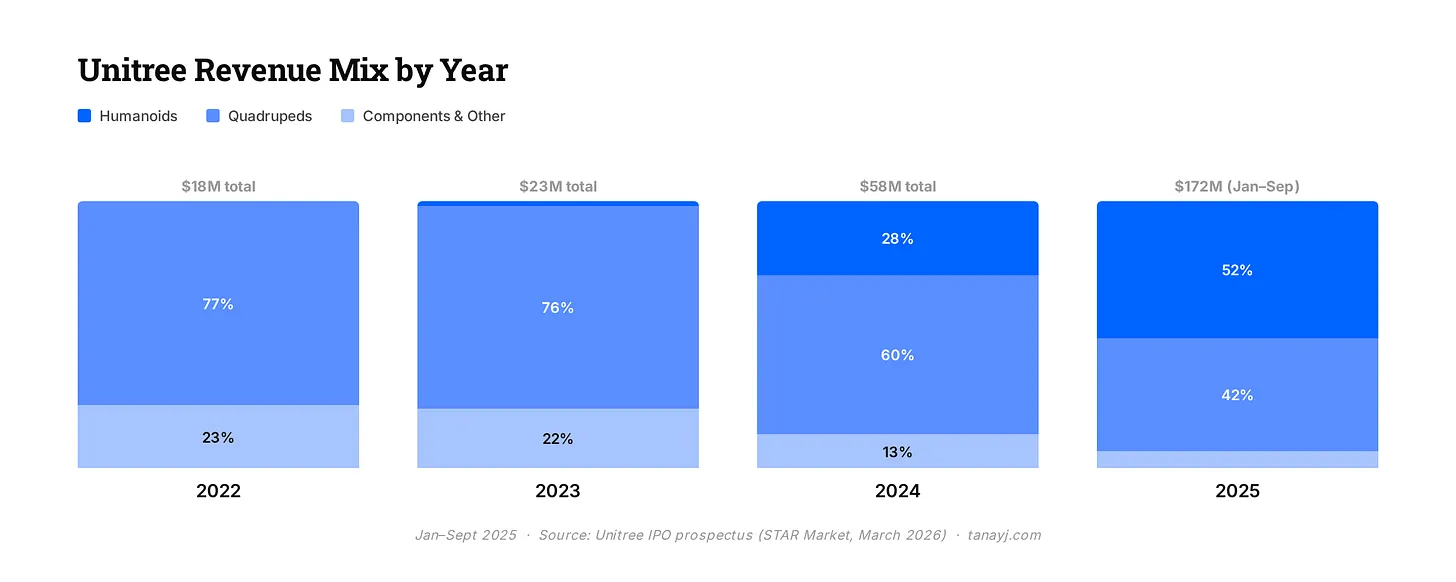

2. Transition of Revenue Structure toward Humanoid Robots

Two years ago, Yushu was essentially a robotic dog company, primarily selling quadruped robots. In 2023, humanoid robots accounted for only 1.9% of revenue.

By the first three quarters of 2025, humanoid robots will account for more than half of core revenue.

This shift is driven by improved product-market fit and proactive marketing strategies. The company’s humanoid robots have appeared on CCTV’s Spring Festival Gala for two consecutive years, one of the highest-rated programs globally. Huang Renxun brought Yushu Robotics onto the stage at the 2024 GTC conference.

This brand exposure has translated into commercial and research demands, something most Chinese hardware companies have never truly achieved.

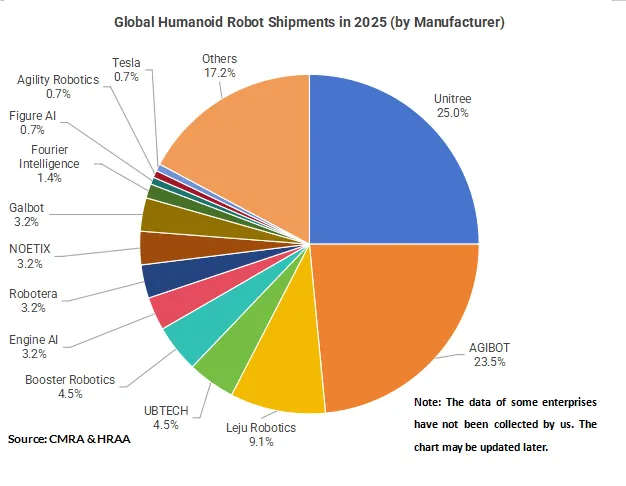

The shipment data for humanoid robots is particularly striking. Yushu is expected to ship about 5,500 humanoid robots in 2025, making it the largest humanoid robot manufacturer in the world by shipment volume. The closest competitor in China is Zhiyuan Robotics. In contrast, well-known American companies like Figure AI and Agility Robotics have shipment numbers only in the hundreds.

The prospectus outlines a five-year target of producing 75,000 humanoid robots and 115,000 quadruped robots annually, which is approximately 14 times the projected humanoid robot shipments in 2025. The goal is aggressive but also underscores how early we still are in this stage.

3. Who is Really Buying Robots

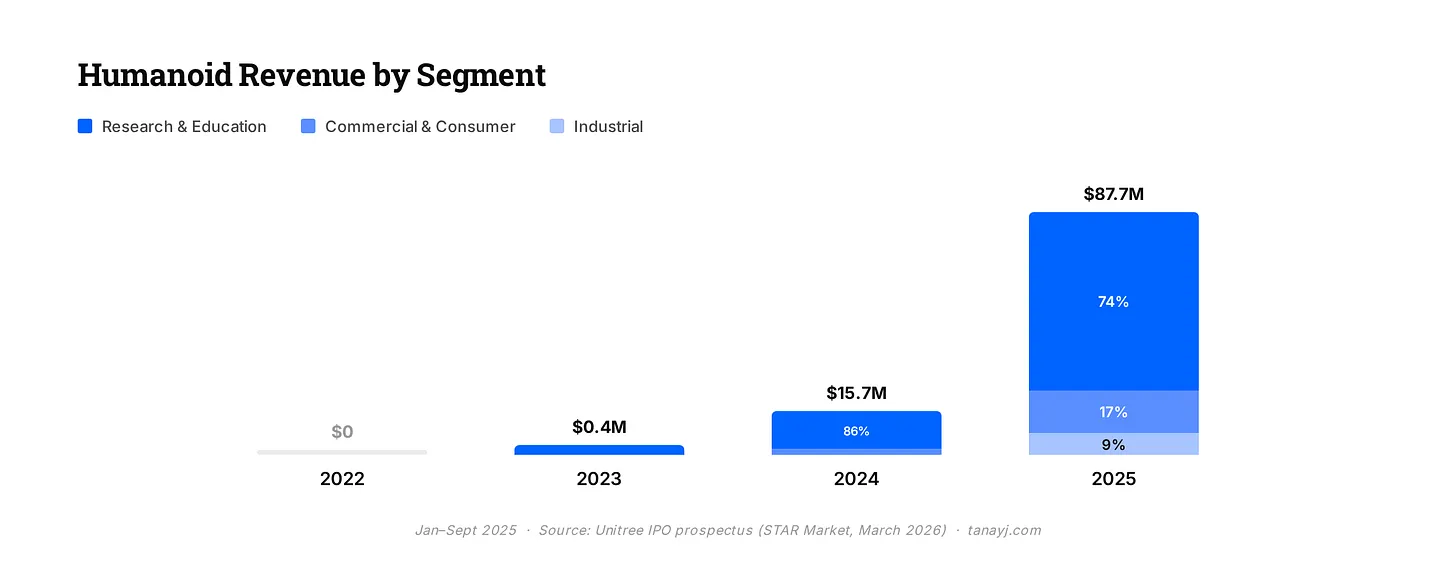

The prospectus categorizes buyers into three groups: research and education, commercial consumer, and industrial applications.

The reality is that most of the current demand for humanoid robots comes from research and education purposes.

1/ Research and education account for 74% of humanoid robot revenue/shipment volume. Academic buyers have been the core support for Yushu since at least 2022 and remain the largest source of income for the company.

2/ Commercial consumer sales account for 17% of humanoid robot shipments. These non-academic consumers mainly use these robots for "show": acting as eye-catching promoters in retail locations, tourist attractions, performances, and exhibitions. In the first nine months of 2025, consumer revenue grew nearly fourfold year-on-year, which sounds impressive, but the base is actually quite small. In reality, this $25,000 humanoid robot is mainly used today to stand at the entrance of a store in Shenzhen to attract tourists.

3/ Industrial applications account for only 9% of humanoid robot shipments. Yushu acknowledges that industrial deployment is more limited because the technology is not yet mature, which reflects the current technological state. Among this 9% of shipments, about 50-70% are used for enterprise reception and guided tours, indicating that only around 3-4% of humanoid robots are actually deployed for tasks like enterprise reception and inspection.

In terms of quadruped robots, the situation is somewhat better: only about one-third of revenue comes from research, over 40% from commercial use, and the remainder from industrial use. The productive use cases there are relatively mature. Customers include State Grid, Southern Grid, Sinopec, PetroChina, Baowu Group, and JD (Yushu's largest customer). These companies use quadruped robots for real inspection scenarios in chemical plants, substations, coal mines, and pipelines.

4. Vertical Integration Strategy

One unique aspect of Yushu is that it independently designs and manufactures most key components: high-torque motors, precision reducers, encoders, joint modules, intelligent controllers, high-precision sensors, dexterous hands, LiDAR, and cameras. According to McKinsey data, the drive system (motors, reducers, and the joint system that actually moves the robots) typically accounts for 40-60% of the total material costs of humanoid robots.

Most companies in this field source these components externally, but Yushu manufactures them in-house. Outsourced components account for only about 14-18% of total costs. They only outsource generic components like batteries and flash storage, as well as differentiated parts like core computing boards.

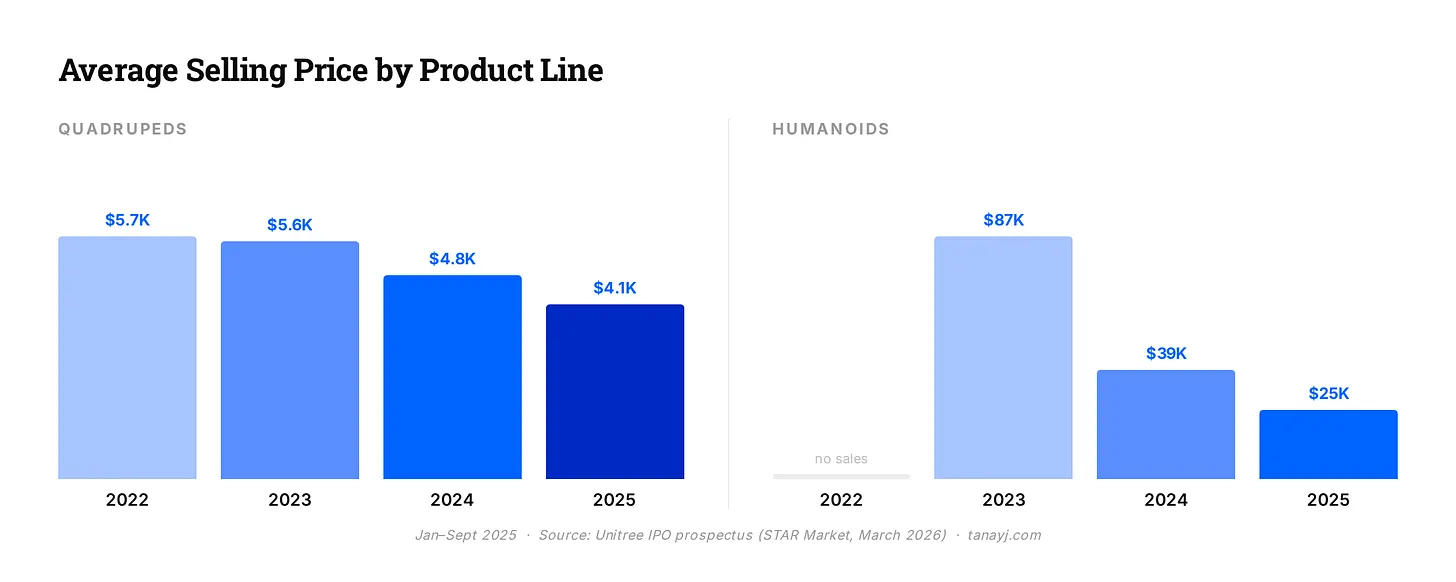

The unit manufacturing cost of quadruped robots has decreased from about $3,300 in 2022 to about $1,800 in mid-2025, a reduction of 46%. The cost of humanoid robots has also decreased, from about $10,800 during the same period to $9,200.

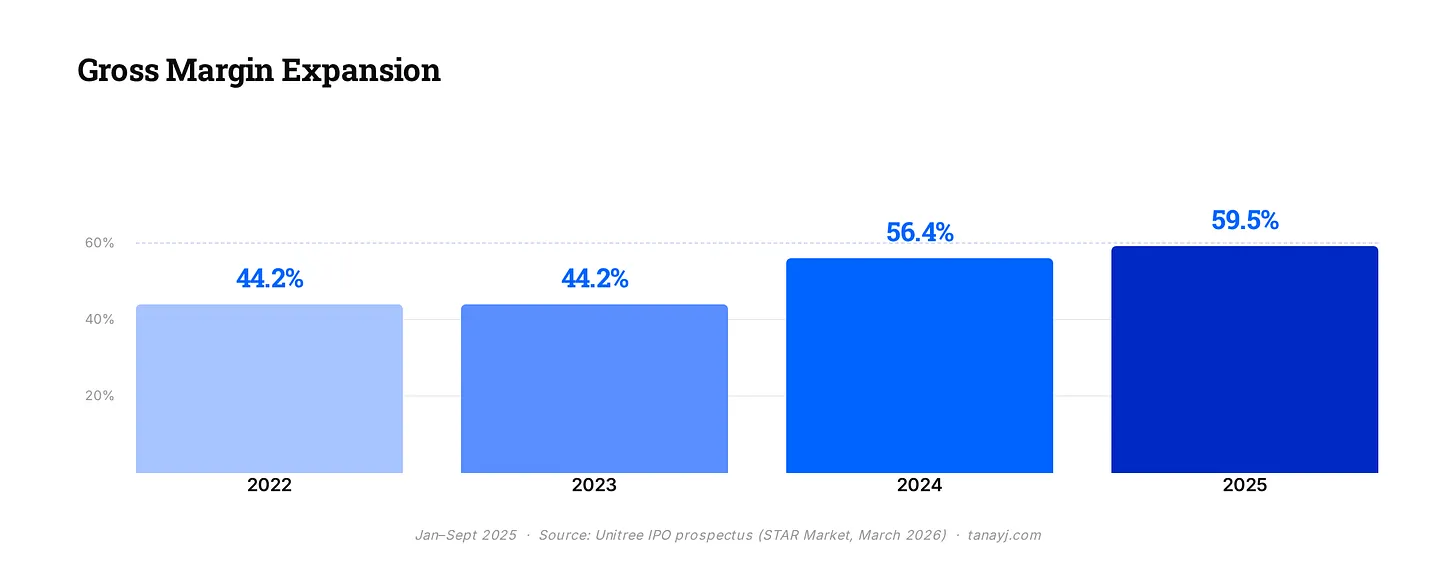

Interestingly, as shown in the figure below, the average selling prices of quadruped and humanoid robots have also significantly decreased each year. However, gross margins have, in fact, expanded over the entire period, increasing from more than 40% in 2022-2023 to nearly 60% in 2025, largely due to their vertical integration strategy.

5. Financial Condition

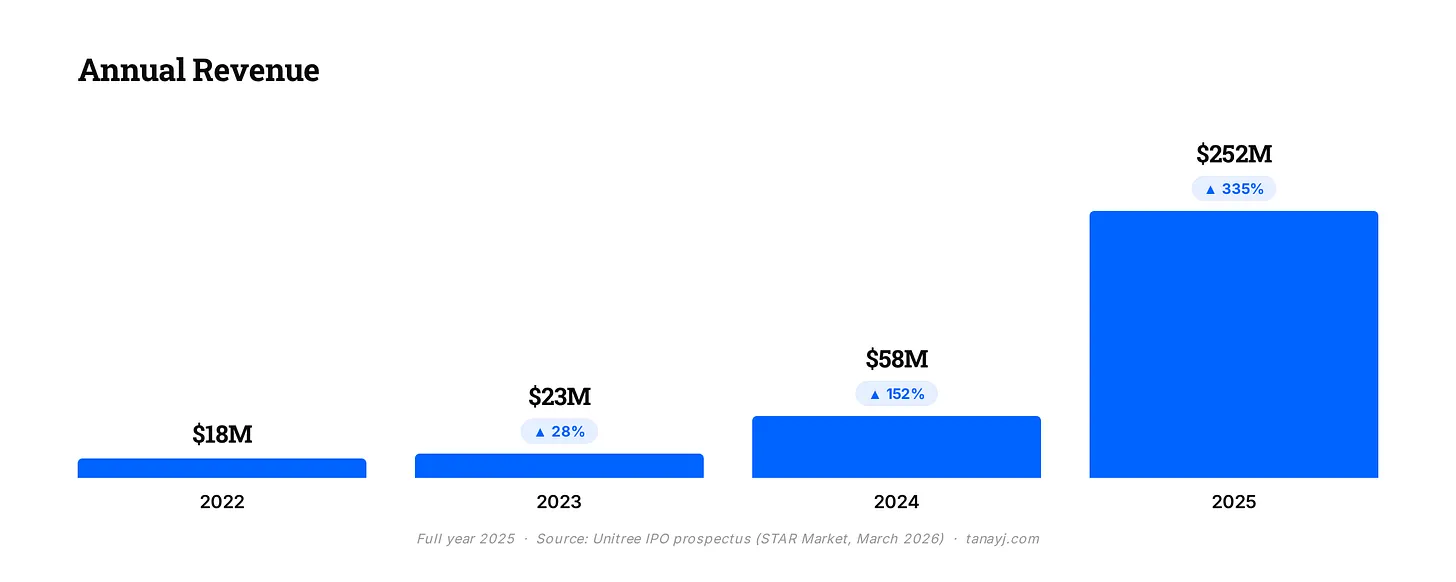

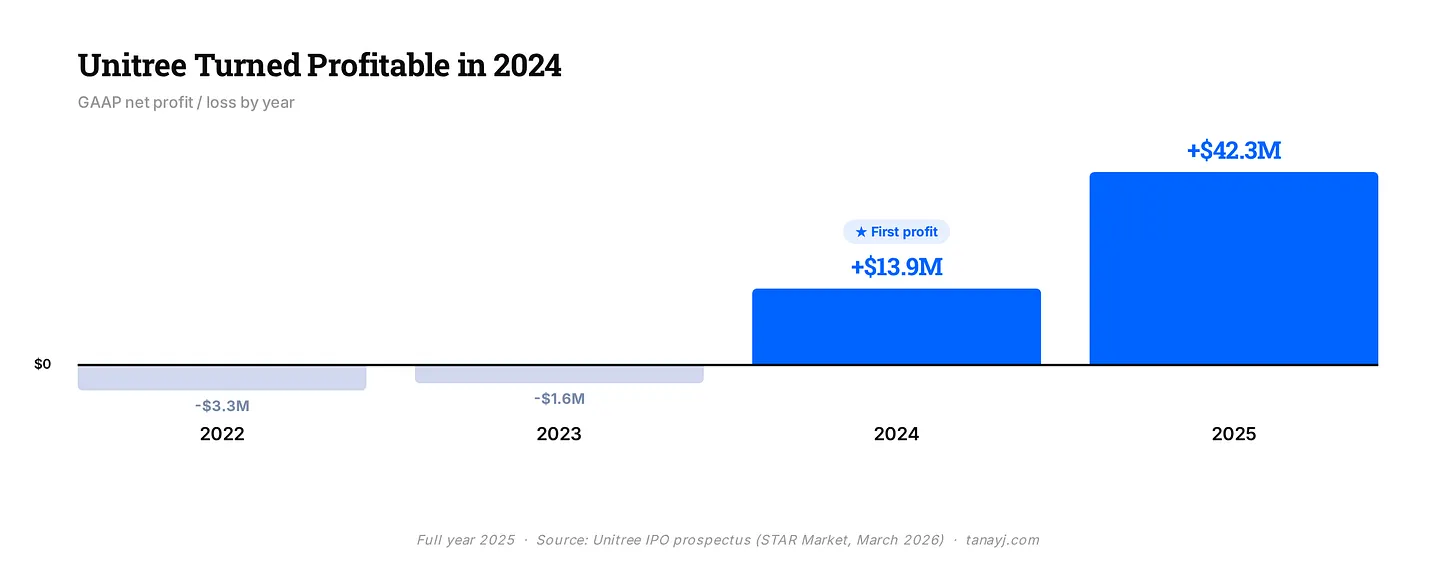

Revenue is expected to grow from $58 million in 2024 to about $252 million in 2025, a 335% increase, driven primarily by strong performance in humanoid robots. For most of the company's history, international sales have accounted for over 55% of revenue. In 2025, the domestic market in China is expected to surpass exports for the first time, although the absolute value of export revenue is still expected to more than double year-on-year.

Gross margin is nearly 60% and has been consistently expanding over the years.

For comparison: most hardware companies have gross margins of 30-40%. Software companies can often achieve 70-80%. For a company selling physical robots, Yushu's gross margin is relatively high, thanks to their vertical integration strategy and currently relatively differentiated products.

The company became profitable under GAAP standards in 2024, with a profit margin of about 18% and nearly 35% on an adjusted basis.

The target valuation for Yushu's IPO is approximately $6-7 billion.

6. Aspirations for the Model Layer

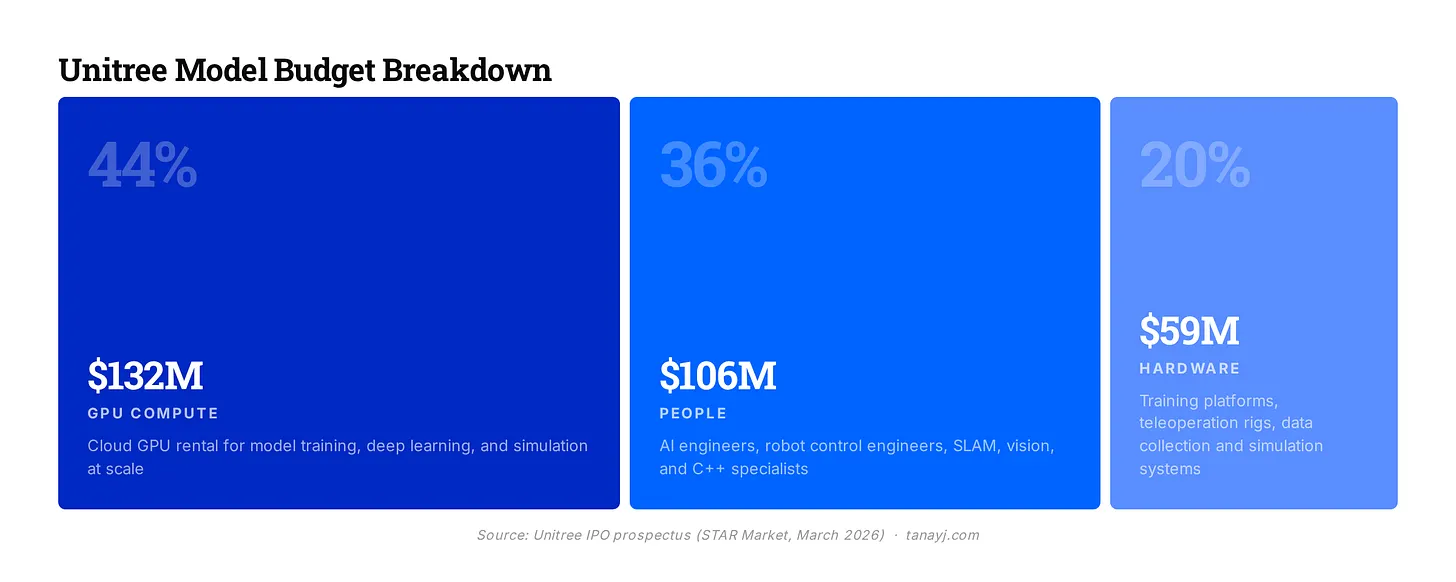

Yushu plans to allocate nearly half of the proceeds from the IPO to software. Of the $620 million in fundraising, about $300 million will be used for AI model training over the next three years, with about $100 million each year invested in what the company refers to as "embodied large models."

The prospectus describes two parallel model architectures. The first is VLA (Visual-Language-Action): a model that directly maps visual and language inputs to motor instructions, allowing robots to generalize in unfamiliar tasks without manually coding instructions. The second is WMA (World Model + Action), which is the direction they are more optimistic about. The WMA model builds an internal simulation of the physical reality. The robot predicts what will happen before taking action, rather than purely learning through trial and error.

They have already released initial versions of both. UnifoLM-WMA-0 was open-sourced in September 2025; UnifoLM-VLA-0 was released in January 2026.

They have also outlined their approximate expenditure allocation for models, as shown below:

Yushu's current hardware leadership is real, but the company understands that a lasting advantage in the robotics field may require mastering the model layer: the system that determines what robots do and how they move. Software ambitions also act as a hedge against commoditization. Yushu has built a moat in hardware manufacturing.

However, if drive and joint modules eventually become standardized components, much like batteries in electric vehicles, then defensiveness will shift to the model layer.

7. Conclusion

Yushu has a profitable hardware business, a real manufacturing moat, and more humanoid robots shipped than anyone else, at prices others cannot reach. But as shown by the actual usage of humanoid robots, the broad commercial application story is still in its early stages. "Showcasing" use cases dominate consumer demand, and the scope for industrial deployment is narrow.

Yushu shows us the current state of the robotics market, with a lot of work still to be done in terms of models, hardware, and use cases. If you are an entrepreneur in the robotics and embodied AI field, feel free to contact me at tanay at wing.vc.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。