Author: David, Shenchao TechFlow

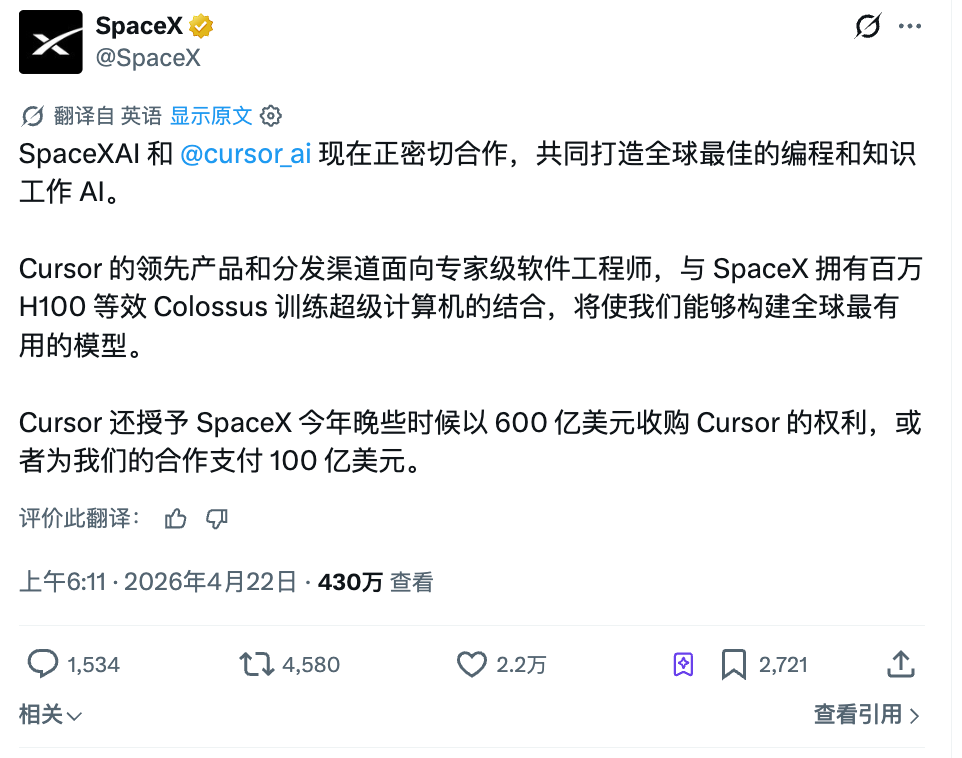

SpaceX posted a message on X last night announcing a partnership agreement with the AI programming tool Cursor.

The agreement gives SpaceX an option: later this year, either acquire Cursor for $60 billion or pay a "partnership fee" of $10 billion.

It's one or the other, but whichever is chosen, it's a significant amount of money.

The situation of Cursor, those who have been following the AI coding track for the past two years should be aware of. It was once the most sought-after coding tool for programmers, with ARR soaring from $100 million at the beginning of last year to $1 billion by the end, and according to Bloomberg, it surpassed $2 billion in February this year.

But this year the tide has changed, with Anthropic's Claude Code entering the market with an annualized revenue of $2.5 billion and over 300,000 corporate clients, and OpenAI has introduced Codex, while Microsoft has directly made its GitHub Copilot free to users.

Cursor now resembles the leading brand that emerged from the previous AI coding boom, but the current table has changed.

For a company like this, SpaceX has offered a $60 billion acquisition price. What does $60 billion even mean? It's more expensive than Disney's acquisition of 21st Century Fox, while the total market size of the AI coding tools market, according to public research, is expected to be less than $10 billion by 2026.

A rocket company offering 6 times the entire industry's scale to buy a code editor that is being chased by competitors?

Looking separately at that $10 billion in the acquisition deal also raises some questions. If an acquisition deal fails to execute, the buyer usually has to pay a breakup fee, which typically ranges from 1% to 3% of the transaction amount. Based on $60 billion, the breakup fee should fall between $600 million and $1.8 billion.

But the announcement from SpaceX states it as $10 billion, nearly 17% of the transaction amount, and it doesn't call it a breakup fee, but a "partnership fee."

For a rocket company with an annual revenue of $16 billion by public financial report standards, paying a "partnership fee" equivalent to more than half a year's revenue, what exactly is the partnership about?

$10 billion, to buy a bullish option for IPO

Why doesn't SpaceX just purchase directly? For a target space company, $60 billion is not astronomical.

In fact, it really can't afford it.

SpaceX is currently a private company, with Musk having previously revealed about $15.5 billion in total revenue for 2025, and it doesn't have $60 billion in cash on hand. So the "or" in this announcement becomes quite clever.

Either $60 billion for acquisition or $10 billion for partnership fee. One of the two, SpaceX gets to choose. Cursor cannot refuse the acquisition nor return that $10 billion. The choice is entirely in SpaceX's hands.

This structure should look familiar to people in finance.

Paying a fee locks in the right to buy in the future, leaving the decision to buy or not at the expiration. The $10 billion paid by SpaceX is essentially an option fee.

But this sort of thing typically does not appear in normal acquisitions. If you want to buy, just buy and negotiate a contract. Why leave yourself a "decide later" window?

The issue may lie in timing.

SpaceX is still a private company, and Musk previously indicated about $15.5 billion in revenue for 2025. It doesn't have $60 billion in cash to acquire anything. But according to multiple media reports, SpaceX is preparing for an IPO targeting a valuation of $17.5 trillion, planning to raise $40 to $75 billion, potentially going public as soon as this June.

Once listed, things change. A company valued at $17.5 trillion can use stock to acquire a $60 billion company, with a dilution rate of 3.4%, which is nearly negligible.

So, the timeline of this transaction is no coincidence. First announcing the partnership with Cursor provides an additional narrative page for the IPO roadshow, such as "We are not just a rocket company; engineers from nearly 70% of the Fortune 500 are using our tools to code every day"...

After the IPO is completed and the stock price stabilizes, they can exercise the acquisition with stock.

This way, the $10 billion option fee has its purpose. SpaceX plans to raise $40 to $75 billion in its IPO, and securing Cursor's acquisition rights with $10 billion amounts to about 15% of the fundraising, buying the exclusive purchasing rights to a leading company in the AI application layer vibe coding track.

In other words, Musk is currently spending money that investors are about to give him to buy something that he will only need to pay in full after going public.

The only variable in this is: whether the IPO can succeed, whether the valuation can reach $17.5 trillion.

If it succeeds, paying $60 billion with stock is essentially spending no money. If it doesn't happen, then that $10 billion cash is the tuition fee.

The whole transaction with Cursor is secured by an IPO that hasn't occurred yet.

Musk's valuation nesting dolls

This approach is not the first time Musk has used it.

In March 2025, xAI acquired the social platform X through an all-stock deal, with third-party estimates valuing X at about $33 billion. A year earlier, Musk spent $44 billion to buy Twitter and rebranded it as X, and its value had already diminished by more than half.

After merging into xAI, X no longer needs to prove how much it's worth separately; it became "xAI's data source and distribution channel."

In February 2026, SpaceX again acquired xAI via an all-stock deal, with a combined valuation of $12.5 trillion, where xAI was valued at $250 billion. Just a few months prior, xAI's self-funding valuation was only $80 billion. After merging into SpaceX, xAI also no longer needs to explain why it's worth $250 billion; it has become "SpaceX's AI capability layer."

In April 2026, SpaceX locks in Cursor, with a $60 billion acquisition option. If completed, Cursor would not need to prove whether its coding tool can outperform Claude Code; it would transform into "the application layer of the SpaceX AI ecosystem"...

Three transactions, all following the same pattern.

Packing a company that cannot maintain its standalone valuation or is losing value into a larger container, allowing it to be priced as a narrative component rather than an independent entity.

If X goes public alone, investors will ask how it makes money and if the advertisements are still running? Within the $17.5 trillion SpaceX, no one asks this question because X only accounts for a tiny fraction of the total valuation.

If xAI goes public independently, investors will ask how Grok compares to ChatGPT? When will the money spent return? But inside SpaceX, this expenditure is overshadowed by Starlink's profits.

I feel that this operation is like a form of asset packaging. Selling each item separately requires accepting market scrutiny for each one; selling it in a package only requires telling a unified story.

A $17.5 trillion valuation supported by rockets and satellites may be believed by investors or not. Adding xAI gives it another leg. Adding Cursor gives it yet another.

The more legs it has, the more stable it appears to stand. Whether each leg can stand independently is a question that needs to be answered before the packaging.

Pricing for position

This year's largest transactions in the AI field are increasingly reflecting a declaration through the prices offered by buyers.

When Amazon invested another $25 billion in Anthropic, no one questioned Anthropic's price-to-earnings ratio; when Meta spent billions acquiring Manus, Manus had only been online for nine months. Now, SpaceX offering $60 billion to Cursor is six times the annual revenue of the entire AI programming market.

These prices share a common characteristic: they are not pricing an existing business of a company; they are pricing a position. Anthropic's position is one of the strongest closed-source models, Manus's position is the AI agent application layer entry, and Cursor's position is the largest AI tool entry for global programmers.

The price of a position is unrelated to income but relates to how close you are to that entry.

If SpaceX's IPO is successful, it achieves a textbook operation. With a single post, an option fee, and an IPO that has yet to happen, it locks in the top assets of the AI programming track. Without spending a dime of its own profit. If it fails, at least Cursor still retains $10 billion.

However, I believe the essence of this event worth remembering is not about whether it succeeds.

The dividend lies in the fact that the prices of AI companies are no longer calculated; they are shouted out. For instance, the $60 billion acquisition figure cannot be derived from any financial model.

As long as you believe that AI programming is the entry point for every programmer in the future, this position must be occupied, and the one who occupies it says how much it is worth, then that is its value.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。