Author: 168X

TLDR

LayerZero has established a significant network effect of interoperability, on-chain smart money has accumulated at lower levels, and the Fee Switch will be a key event for its valuation framework shift.

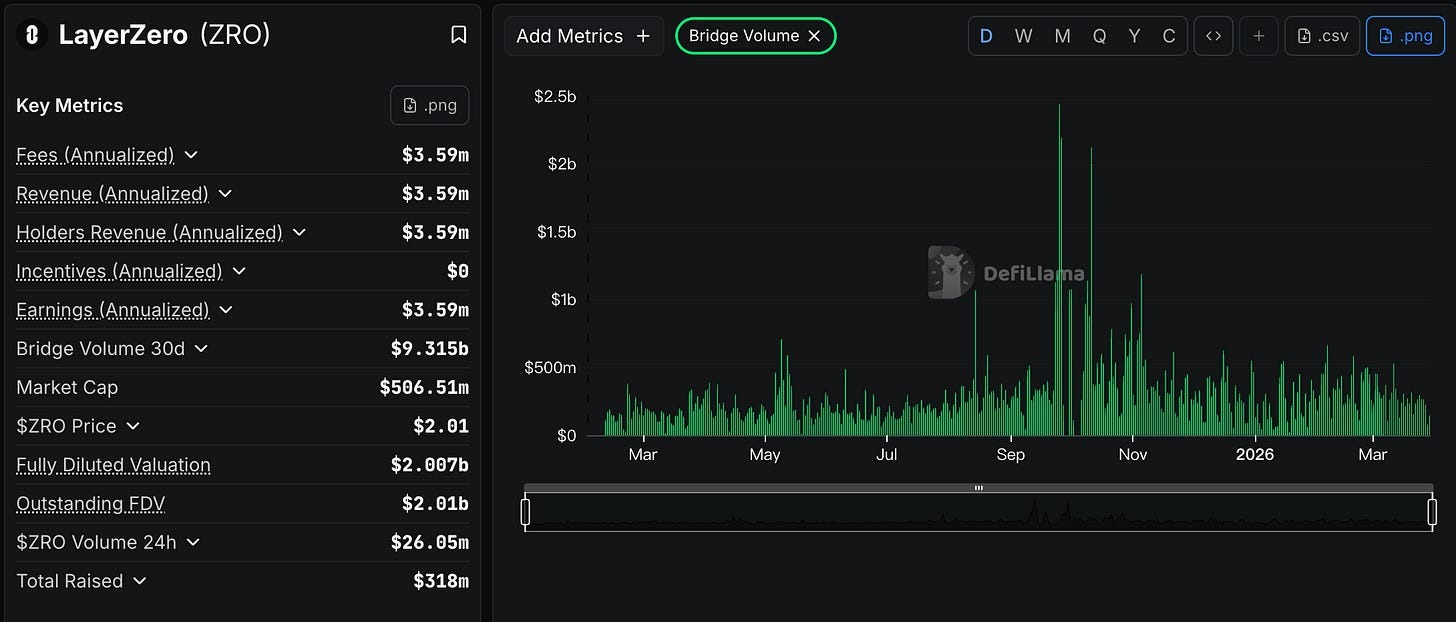

- LayerZero has integrated over 165 chains, with a cumulative cross-chain volume exceeding $225 billion ($225B+), and over 159 million messages sent, making it one of the most scalable interoperable protocols.

- The Canton Network integration becomes a catalyst for institutional narratives: processing over $8T+ RWA monthly, $350B daily in US Treasury repos, with LayerZero becoming the "first and only" interoperable protocol integrated with Canton.

- Starting March 2026, 100% of Stargate's revenue will flow to ZRO buybacks, marking the first time protocol cash flow begins to more directly revert to token holders.

- On-chain data shows several large addresses recently accumulating ZRO in the $1.3 to $2.0 range, reflecting that some institutions and allocators are amassing large amounts.

- LayerZero's protocol has an annualized cross-chain volume exceeding $150B, while foundation revenue remains zero. The true determinant of whether ZRO enters the revaluation range hinges on whether the Fee Switch is activated and whether protocol revenue can stabilize and flow back to token holders.

The market has underestimated the LayerZero story

Many in the current market view LayerZero as a lackluster infrastructure project lacking clear protocol revenue, further assuming that ZRO is more of a narrative token rather than an asset backed by cash flow.

This perspective is partially correct. Currently, the $3.59M in fee revenue shown by DeFiLlama is primarily directed to external participants such as DVN and Executor, and the LayerZero foundation has not yet received direct income, while the value of holders' tokens primarily comes from the buybacks of Stargate income.

However, what is overlooked is that LayerZero’s focus over the past few years has been on integrating more chains, establishing deeper application dependencies and validation networks, rather than prematurely extracting fees at the protocol layer. This is a strategic choice prioritizing market share rather than a permanent economic arrangement.

For this reason, the **Fee Switch** has become one of the most noteworthy potential catalysts for LayerZero. Should governance decide to start charging at the protocol layer in the future, with an estimated 10 bps (0.1%), annualized protocol revenue will exceed $125 million, pushing the corresponding valuation revaluation to $2.5B+.

Before that, the integration of the Canton Network, the launch of the Zero Blockchain, and a series of large on-chain purchases have already made this narrative worth reevaluation.

Thanks for reading 168X! Subscribe for free to receive new posts and support my work.

Core narrative one: LayerZero has established a leading infrastructure position

The advantages of LayerZero come from scale and network effects

Cross-chain interoperability is the TCP/IP of blockchain. TCP/IP won the communication protocol battle so thoroughly that we no longer have to think about this issue.

LayerZero is accomplishing the same thing in the field of cross-chain interoperability.

The ultimate goal of cross-chain depends on who can become the default communication layer for more applications and assets. Based on the current number of on-chain integrations, asset coverage, and message volume, LayerZero has established a significant leading edge in this competition.

Key data as of March 2026:

- 165+ chains integrated: covering mainstream EVM and non-EVM chains such as Ethereum, Solana, BNB Chain, Avalanche, Arbitrum, Base, Aptos, Cardano, and Canton Network.

- $225B+ cumulative cross-chain volume: representing long-term demand for asset transfers in a real production environment.

- Over 159 million cumulative messages: covering various scenarios such as OFT token transfers and cross-chain contract calls, indicating that the use cases for LayerZero extend beyond a single bridging application.

- Continuous increase in OFT standard penetration: Omnichain Fungible Token has gradually become one of the important standards for cross-chain token design, with major assets such as USDC, USDT, and WBTC adopting the OFT format.

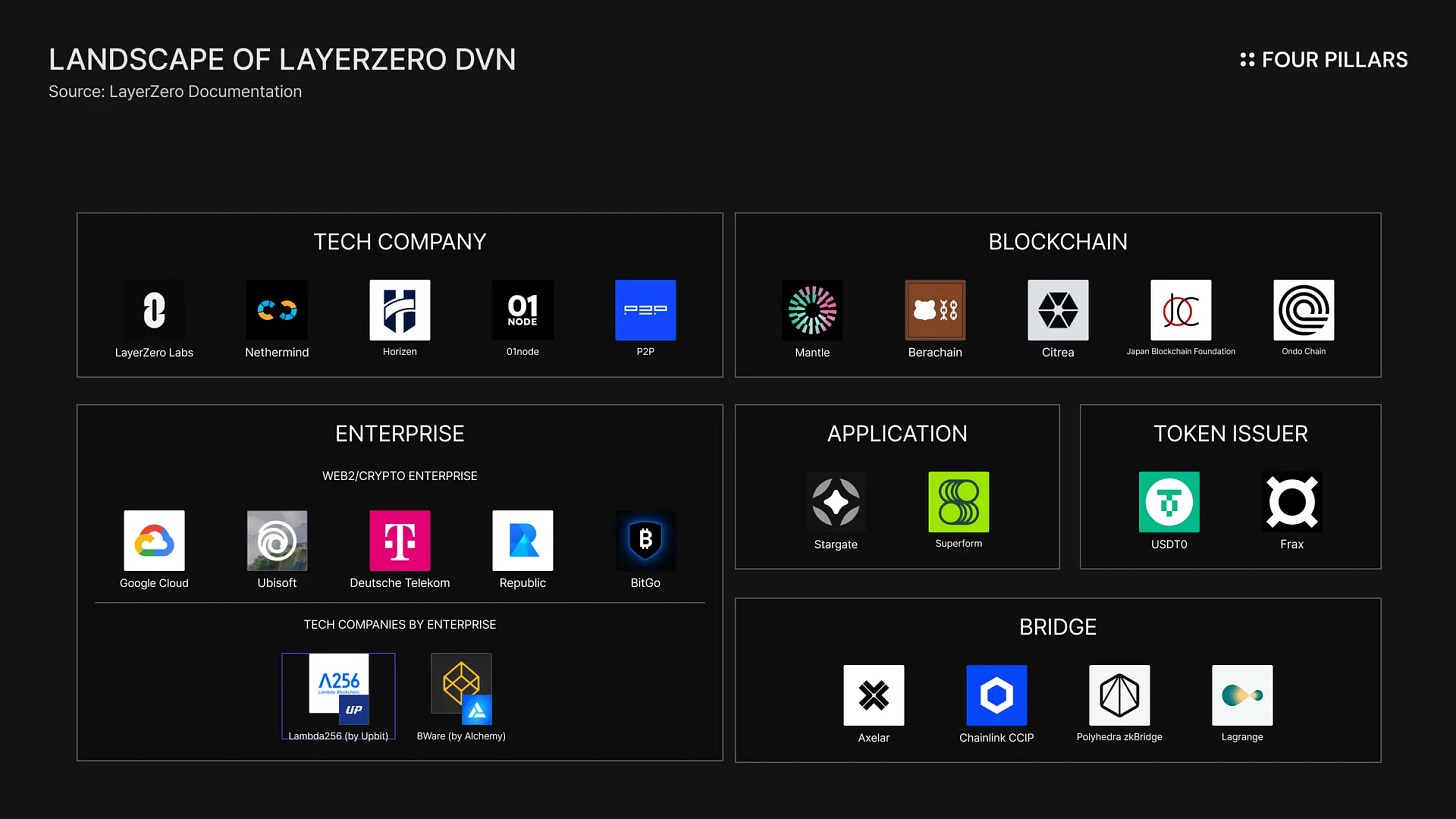

DVN Architecture: The True Source of Competitive Advantage

Many market participants often look at fees, speed, and security when comparing cross-chain protocols. However, for true infrastructure, a more important variable is often the switching cost of the validation network.

LayerZero's DVN (Decentralized Validation Network) allows applications to choose their trust models, using Google Cloud, Polyhedra, LayerZero Labs' own DVN, or freely combining multiple validation sources. This creates higher flexibility and stickiness at the deployment level for LayerZero:

- Institutions find it easier to adopt familiar validation providers: for example, Google Cloud DVN is more friendly for compliance and risk assessment of traditional financial institutions.

- Once OFT is deployed, migration cost is extremely high: re-auditing contracts, rebuilding liquidity, reauthorizing, and re-educating users incur high costs.

- Application layer dependencies have emerged: applications like Stargate, Radiant, and SushiXSwap heavily rely on LayerZero for their cross-chain structure and message delivery.

Therefore, LayerZero's competitive advantage is not just derived from the technology itself, but also from the actual lock-in effect after deployment. This is often more important than short-term fee differences.

Zero Blockchain: From Protocol to Ecosystem

On February 10, 2026, LayerZero announced Zero Blockchain, positioned as an L1 network of "a multi-core world computer," aiming to address the throughput bottleneck of existing public chains, with a core goal of 2 million TPS, and the mainnet is expected to go live in the fall of 2026.

What is more noteworthy is the support behind it: Citadel Securities (the world's largest market maker), ARK Invest, DTCC (the US Depository Trust & Clearing Corporation, handling 99% of global securities settlements), ICE (Intercontinental Exchange, parent company of NYSE), Google Cloud.

The significance of these participants goes far beyond that of typical crypto venture capital firms. Especially DTCC and ICE, which are themselves major operators of global financial infrastructure, represent that LayerZero's narrative has moved beyond purely crypto-native interoperability to the intersection of traditional finance and on-chain infrastructure.

The launch of Zero Blockchain upgrades ZRO from a "governance token" to a mainnet token with multiple utility properties:

- Native Gas token: All transaction fees on the Zero chain are paid in ZRO, directly creating demand for tokens at the protocol level.

- PDPoS staking: Adopting pure Delegated Proof of Stake, anyone can delegate ZRO to participate in validation and earn rewards, with no slashing risk, providing stable low-risk returns to large holders.

- Deflationary mechanism after Fee Switch: According to the roadmap, once the Fee Switch is activated, cross-chain message fees will be used for buybacks and destruction of ZRO, creating deflationary pressure.

This will allow ZRO to transition from "possibly having income" to "having usage and staking demand" as a mainnet asset, a substantial upgrade in the valuation framework.

Canton Network: A Decisive Turning Point in Institutional Narrative

In March 2026, LayerZero completed the integration of the Canton Network, and while the market reaction was relatively calm, its potential significance may have been underestimated.

Built by Digital Asset, the Canton Network is a permissioned blockchain network geared towards institutions. According to public information, this network has connected over 800 financial institutions, including major firms like Goldman Sachs, JP Morgan, BNY Mellon, and Deloitte, processing monthly RWA exceeding $8T and approximately $350B daily in US Treasury repo settlements. LayerZero is currently the first and only interoperable protocol integrated on the Canton Network.

The completion of Canton’s integration does not imply a large-scale asset flow through LayerZero in the short term; the adoption cycle for institutions is typically much longer than the market expects. However, the monthly RWA processed by Canton is approximately 80 times the current total TVL in DeFi—once institutional-grade RWA begins to flow between Canton and public chains, LayerZero is the only pipeline available.

Core narrative two: On-chain smart money is quietly accumulating

The value of on-chain data lies in its ability to allow market participants to observe the allocation direction of large funds earlier. By analyzing ZRO whale addresses, we have gathered several noteworthy findings.

Coinbase Prime related addresses: Institutional hallmark behavior

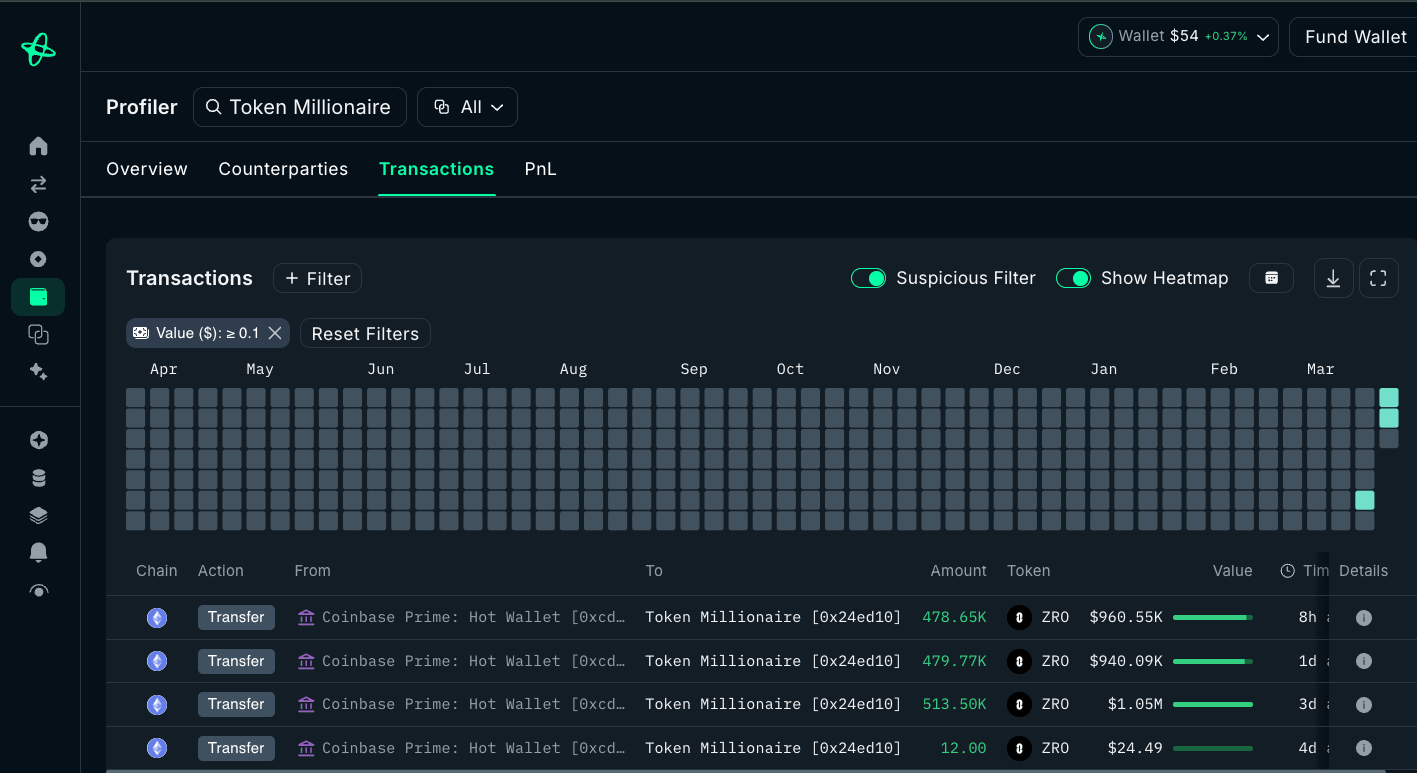

The on-chain analysis platform Nansen's data reveals a noteworthy accumulation pattern: the funds of 9 wallets all point to Coinbase Prime's institutional custody service, having secretly purchased about 24.5 million ZRO, valued at approximately $47.5 million just before a large unlock on March 20, accounting for about 2.6% of the circulating supply.

These addresses exhibit typical institutional characteristics: 8 wallets received funding within the same four-hour window; each wallet holds only ZRO with no other assets; 4 addresses performed a 1 ZRO test transaction before the large transfers (a standard institutional verification step); and throughout the accumulation process, no sell actions were recorded.

Subsequent tracking shows that related activities further expanded to 18 wallets, accumulating a total of $79.7 million in ZRO, with all funds directed through institutional channels.

Coordinated whale buying event on March 22

On March 22, 2026, 5 wallets with no historical connections synchronously purchased, each acquiring 490K ZRO for a total of about $4.9M.

Consistent scale, synchronized timing, and unrelated addresses suggest that this could be the same entity diversifying its holdings or multiple client accounts of the same fund executing the same instruction together. At that time, ZRO's daily trading volume was around $15M to $20M, and the $4.9M coordinated purchase constituted a significant signal.

Other notable whale addresses

- 0x3021B2… (Mar 27): Withdrew 1.641M ZRO from Binance, about $3.3M, moved to a personal cold wallet with no significant sell signs.

- 0x02546E… (Mar 13): Withdrew 5.806M ZRO from a DeFi protocol, about $12M, returned to personal wallet.

- 0x26cc9d… (Dec 31): Purchased 4.7M ZRO in batches over two weeks, about $6.28M, showing behavior more akin to liquid-sensitive large positions.

- 0x313434… (Jan 9): Accumulated 3M ZRO over three months, about $4.28M, continuing to increase positions despite showing paper losses.

These addresses together present a noteworthy phenomenon: during the most pessimistic market phase with significant unlock pressure, there have not only been outright sell-offs, but also medium to large funds consistently absorbing the supply.

Institutional holdings: Bets spanning from VC to traditional finance

LayerZero’s funding history is itself top-notch: Sequoia Capital and a16z co-led the $135M A+ round in 2022 and subsequently co-participated in the $120M B round in 2023, with these two top Silicon Valley VCs heavily invested in consecutive rounds. Multicoin Capital has been involved since the early $6.3M A round, being one of the first native crypto fund bets. Binance Labs, Coinbase Ventures, and PayPal Ventures have also participated.

Entering 2025-2026, LayerZero's investor structure has qualitatively changed:

- a16z (April 2025): Publicly added $55M in ZRO from the open market, locked for three years.

- Citadel Securities (February 2026): Strategic acquisition of ZRO, amount not disclosed.

- ARK Invest (February 2026): Simultaneously invested in equity and ZRO, with Cathie Wood joining the advisory board.

- Tether Investments (February 2026): Strategic investment, amount not disclosed.

These funds are not short-term traders; their holding cycles are measured in years, and exit requires sufficient liquidity accumulation. Before that, they have ample motivation to ensure that the LayerZero story remains valid.

Stargate income buyback: Redirecting cash flow to token holders

In August 2025, LayerZero acquired Stargate for $110M. The key to this deal is not just expanding ecological control, but also partially converting the previously independent protocol cash flow into a value return mechanism for ZRO.

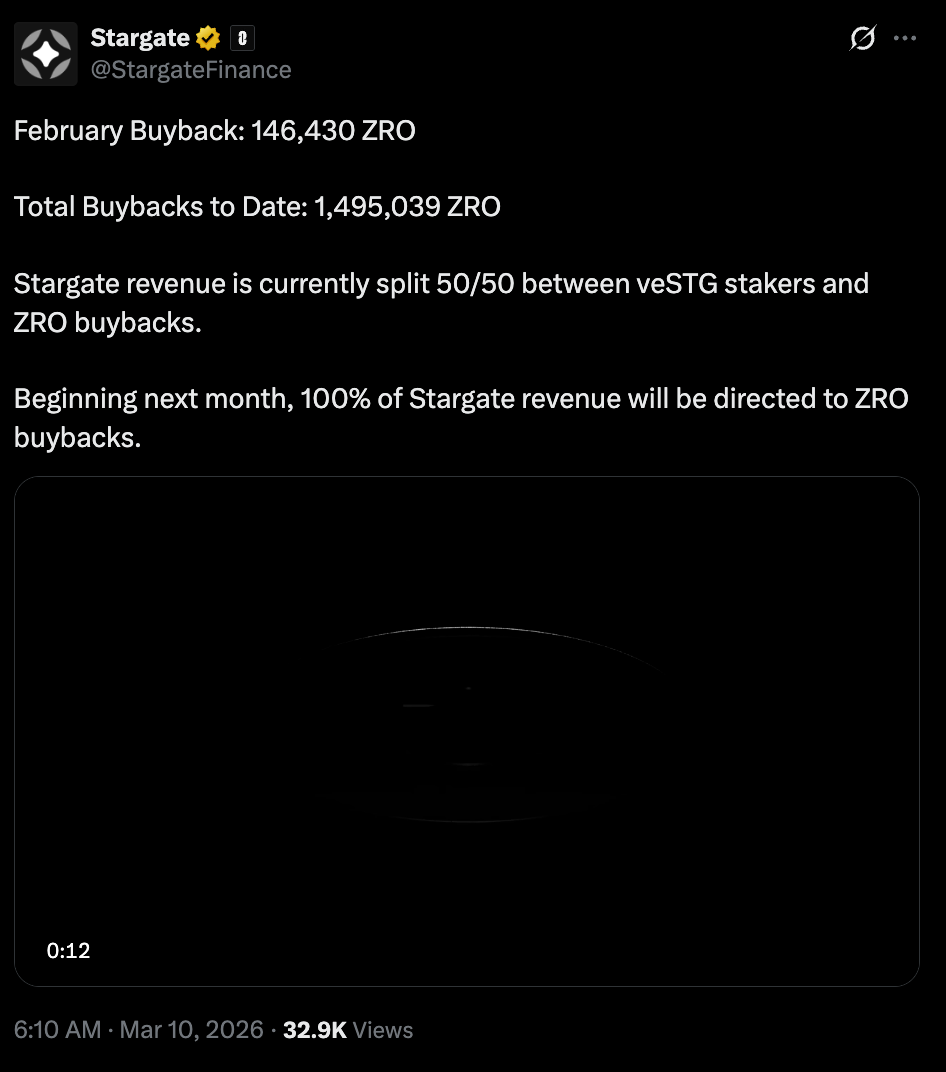

Starting March 2026, 100% of Stargate's revenue will be directed to ZRO buybacks. According to public data, as of March 10, 2026, a total of 1,495,039 ZRO has been repurchased, including 146,430 ZRO repurchased in February 2026 alone.

The current monthly buyback scale of about 150,000 ZRO is still small compared to the $48M monthly unlock pressure. Stargate's buyback is not yet sufficient to hedge against the unlock; a true valuation revaluation must await scaled revenue following the activation of the Fee Switch, rather than the current early buybacks. However, the economic structure has undergone significant changes: the protocol layer has begun to directly provide value back to token holders, establishing a precedent for the return mechanism.

Core narrative three: The Fee Switch will reshape the overall valuation framework

$150B+ scale, with zero protocol revenue

LayerZero is currently in a state of "having large traffic but no direct charges." According to DeFiLlama data, the $3.59M in fees shown by LayerZero primarily goes to external nodes like DVN and Executor, which are operational outsourcing costs for the protocol rather than protocol revenue.

This structure has its reasoning: in the early stage of market share expansion, letting applications and users feel a "near-zero cost" cross-chain experience quickly establishes network effects. After four years of accumulation, the scale of LayerZero's processing is large enough that the Fee Switch becomes a meaningful revenue mechanism.

The core of the valuation misalignment lies in the current market pricing based on $0 revenue, yet an annualized volume of over $150B already exists (recent monthly volume around $14B, annualizing over $150B). Once the market starts believing that its revenue side is likely to open up, the valuation framework for ZRO could undergo a significant transformation.

It is worth noting that the current pricing of ZRO is completely based on future optionality, rather than existing revenue. What the market is currently buying is a combination of three option premiums: the launch of the Zero Blockchain mainnet, the maturation of the Canton institutional pipeline, and the revenue revaluation post Fee Switch activation. The significance of the following scenario models lies in quantifying the possible valuation ranges "if the above options are realized."

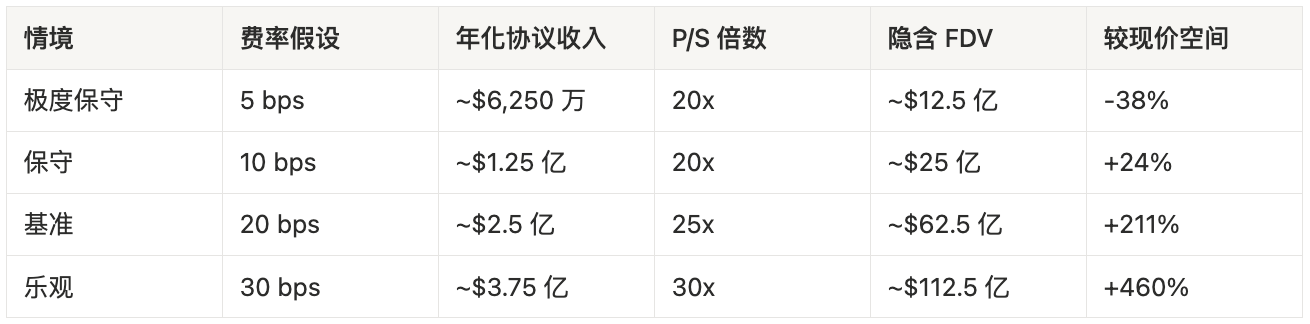

Scenario Analysis

Benchmark data: Current annualized cross-chain volume about $150B+ (estimated based on recent monthly volumes), with protocol revenue nearly zero, current FDV approximately $2.01B. The P/S scenario table uses a conservative benchmark of $125B for calculation, with actual volumes continuously growing.

The following models use annualized cross-chain volume × bps as a simplified proxy variable for protocol revenue, aiming to provide a clear magnitude reference. Actual fee designs depend on governance decisions and may be realized through fixed fees per message, dynamic cost adds, or mixed mechanisms, with final numbers possibly differing from this table.

Scenario model post Fee Switch activation (benchmark annualized volume: $125B, current FDV ≈ $2.01B):

Fee reference: Mainstream cross-chain protocols like Stargate typically charge 5–30 bps, and this table assumes the fee rate aligns with industry practical ranges. The highly conservative scenario (5 bps, close to Stargate's current fee rates) implies an FDV below the current market pricing, indicating that without sufficient fee design, the Fee Switch itself cannot support the existing valuation and relies on volume growth to fill the gap.

The key question has never been "if the Fee Switch is activated," but rather "why hasn't it been activated yet."

Our judgment is that LayerZero is waiting for sufficient volume to ensure that fee adjustments won’t harm competitiveness, while also waiting for the establishment of institutional pipelines like Canton Network and Zero Blockchain. These conditions have started to mature in Q1-Q2 of 2026.

Unlock pressure: Real but large funds have not directly sold

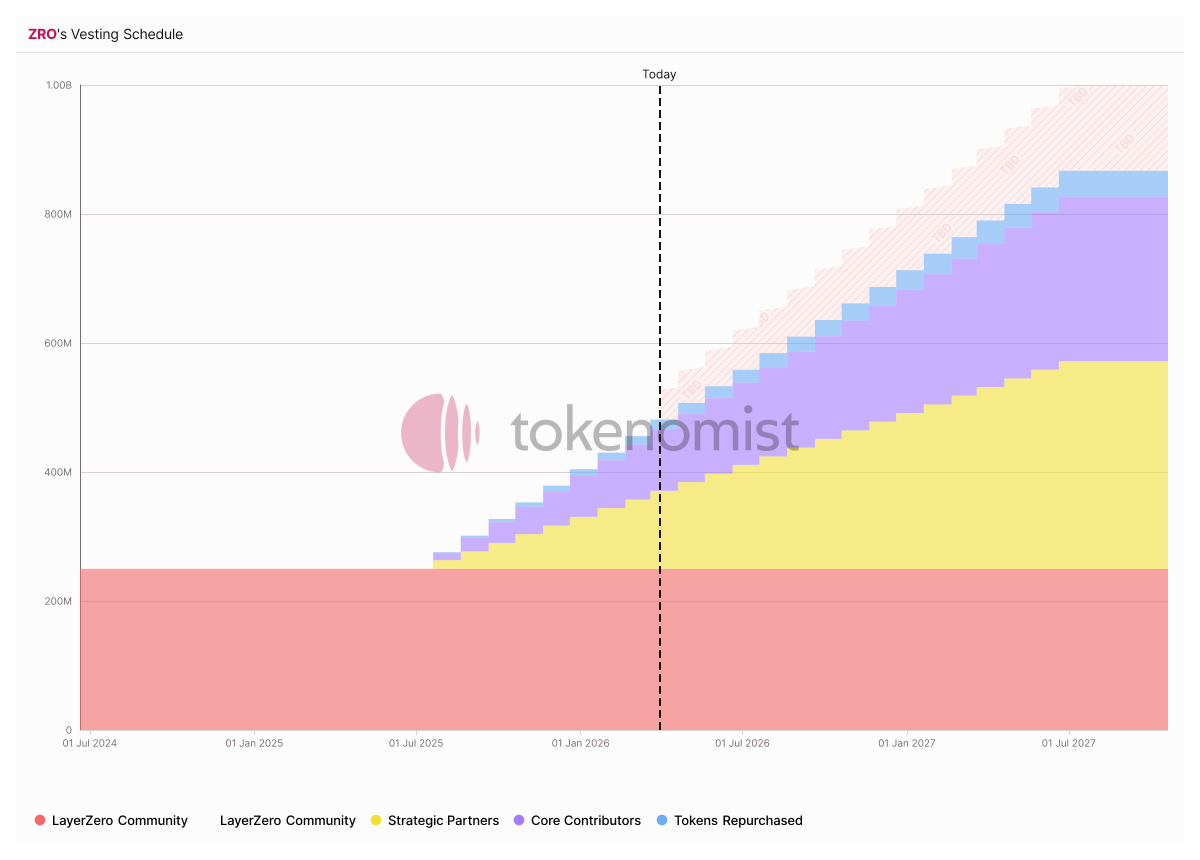

Based on current data, the monthly unlock amount for ZRO is about $48.08M, with strategic partners accounting for about $26.83M and core contributors about $21.25M, slated to continue for about 13 months. In contrast, the current monthly buyback scale is only approximately $0.29M, showcasing a significant disparity between the two.

The risk from unlocking cannot be underestimated, but on-chain data shows that "unlocking does not equate to selling."

The holders among Strategic Partners largely consist of large funds and early investors such as Dragonfly, a16z, and Multicoin, whose exits require sufficient liquidity, as large sell-offs would harm their own position values. On-chain observations show that large amounts of unlocked ZRO have not directly entered exchanges but rather have been transferred to new cold wallets or DeFi protocols. This indicates that the actual release of selling pressure may be slower than the nominal unlock speed.

Additionally, following the launch of Zero Blockchain, ZRO will serve as the on-chain gas token, with the PDPoS staking mechanism locking ZRO in circulation. Once the Fee Switch is activated, the income from cross-chain message fees will be used for the continued buyback and destruction of ZRO—three demand pipelines (Gas, staking, buyback) will simultaneously provide structural demand to counter the unlock pressure.

Overall, while unlock pressure is real, it can be digested by fundamentals in the face of the Fee Switch, the token economics design of Zero Blockchain, and institutional demand from the Canton Network.

Chip structure: Who holds ZRO?

As of March 2026, the distribution of ZRO tokens is as follows:

- Community/Ecosystem (38.3%): Used for staking, liquidity mining, and airdrop distributions.

- Strategic Partners (32.2%): Primarily held by VCs and institutional investors, most of which are still in unlock periods.

- Core Contributors (25.5%): Allocated to teams and advisors.

- Foundation/Reserve (4.0%): For the foundation and protocol reserve allocation; as of now, the accumulated protocol buybacks are about 0.15% (approximately 1.5M ZRO), and continue to increase.

The current circulating volume is about 25.2% (~252M ZRO), with institutional and insider holdings around 57.7%. The true circulating supply of ZRO is far lower than the market's fear of future unlocks. Before there is an exit motivation from institutional holders, the effective circulating supply is limited.

Risk factors

Delay in the Fee Switch: The core logic for investing in ZRO is a change in the market's revenue expectations for LayerZero. Activation requires governance voting, and if the protocol chooses to continue the "market share first" strategy, the valuation catalyst may be delayed.

Post-charging, former volumes may not be maintained: If fee designs are set too high or competitors provide more attractive alternatives, LayerZero's cross-chain volume may also come under pressure.

Accelerated unlock pressure: If market liquidity further tightens, Strategic Partners may choose to exit faster, with the continued selling pressure of $48M/month suppressing short- to medium-term prices.

The institutional adoption cycle is much longer than market expectations: The collaborative narrative from institutions like Canton Network, DTCC, and ICE enhances LayerZero's imaginative space but may not directly translate to revenue or token value capture in the short term.

Competitive risk: Wormhole, Axelar, and Hyperlane remain competitive in specific verticals (Solana ecosystem, Cosmos ecosystem), and although LayerZero's network effect advantages are real, they are not insurmountable.

Regulatory risk: The depth of institutional integration in Canton Network and Zero Blockchain means that any strong regulation targeting cross-chain protocols could impact the institutional narrative.

Conclusion: LayerZero's immense value misalignment

LayerZero stands as the most structurally misaligned high market cap protocol in the current crypto market.

The battle for infrastructure has already concluded, and LayerZero is seen as the winner in the eyes of institutions. With its massive cross-chain volume, the top-tier institutional partners of Zero, and the integration of Canton Network, LayerZero has established clear scale advantages and deployment stickiness. From the perspective of token economics, the Stargate revenue buyback mechanism has begun to establish the most fundamental value return chain. On-chain behaviors have shown that smart money is in allocation.

The only missing element is the catalyst; the Fee Switch is the fuse waiting to be ignited.

If it does not activate soon, ZRO may be viewed for an extended period as an important yet hard-to-value infrastructure token; however, if it activates and the market believes that revenue can stabilize and flow back to token holders, the valuation logic of ZRO will undergo a significant shift from "having usage" to "having income" capability.

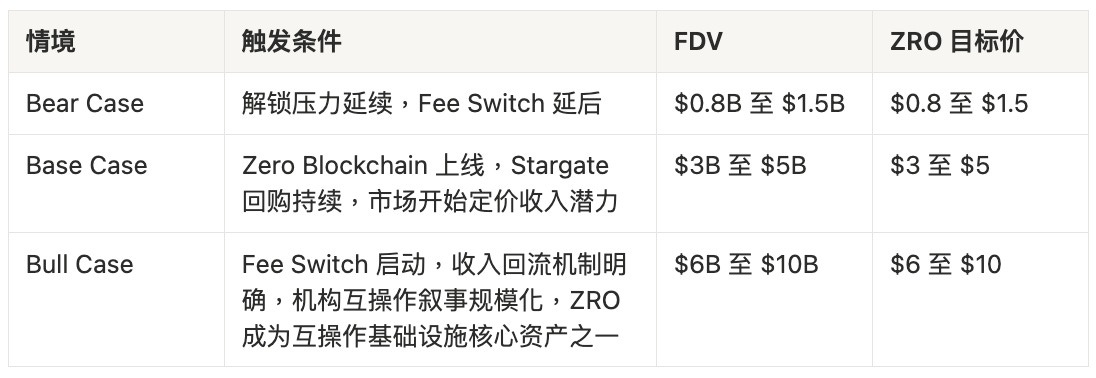

Considering multiple catalysts, the price target framework is as follows:

The probability of scenarios ranging from benchmark to bull market is higher than the levels implied by current market pricing. At $2.01, building a position in ZRO offers asymmetric risk and reward: downside space is supported by the protocol's fundamentals; upside space is jointly driven by the Fee Switch, institutional integration, and Zero Blockchain three catalysts.

Canton Network processes $8T RWA monthly; if 1% flows through LayerZero, the monthly volume will reach $800 billion, approximately 5 to 6 times the current monthly processing volume. At that time, LayerZero's qualitative status will transition from a cross-chain protocol to a monopoly in financial infrastructure.

ZRO may be much closer than the market imagines to truly completing its value capture.

This research report is produced by 168X and does not constitute investment advice. Crypto assets are highly volatile, and investors should conduct their own due diligence. Data is as of March 30, 2026.

Thanks for reading 168X! Subscribe for free to receive new posts and support my work.

About 168X

168X is a research platform for technology and capital that connects Eastern and Western perspectives. Through in-depth research and dialogue, it explores how AI, blockchain, robotics, aerospace technology, and biotechnology are reshaping the future of capital and innovation alongside top founders and investors. Lead by ex-banker Mr. Z.

X | YouTube | Apple Podcasts | Substack

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。