Author: Micro Observations and Discussions

The U.S.-Iran conflict has reignited, leading to a strong rise in crude oil and precious metal assets. The recent increase in oil prices mainly reflects geopolitical risk premium rather than actual tightness in spot supply.

Market signals are diverging: Futures prices, freight rates, and risk reversal option prices are rising due to risk concerns, while spot supply-demand reflected in futures contract spreads (calendar spreads) and physical crude oil spreads are weakening. MS analyzed four potential scenarios.

Scenario Analysis

·Base Scenario: Excludes the possibility of continued closure of the Strait of Hormuz as a core scenario, which has a very high threshold and a very low probability. The analytical framework focuses on a range of possibilities from de-escalation to limited friction.

·Scenario 1 (No Supply Disruptions): De-escalation leads to a reduction in risk premiums. It is expected that a risk premium of about $7-9 per barrel will quickly disappear, with Brent crude prices possibly retreating to the low $60 per barrel range.

·Scenario 2 (Limited Strikes and Short-term Logistics Friction): Targeted military actions occur, avoiding energy facilities. This may lead to a supply disruption of 0-0.5 million barrels per day, lasting 1-3 weeks. Oil prices may briefly spike to the mid-$70 range, but China's slowdown in strategic reserve accumulation will become a key balancing mechanism, after which prices will return to the low $60 range.

·Scenario 3 (Local Iranian Export Disruptions): Broader strikes cause localized disruptions in the Iranian export chain but do not affect shipping through the Strait of Hormuz. It could result in supply disruptions of 0.8-1.5 million barrels per day, lasting 4-10 weeks. Price trends will be between Scenario 2 and Scenario 4.

·Scenario 4 (Fleet Efficiency Shock and Shipping Damage): Tail risk. Iran conducts maritime countermeasures, such as harassing ships, leading to decreased shipping efficiency and increased delays. This results in an "effective supply tightening" of 2-3 million barrels per day, lasting several weeks, with price trends potentially similar to the spikes seen in early 2022, but expected to last for a shorter duration.

·Scenario 1 (No Supply Disruptions): De-escalation leads to a decrease in risk premiums. It is expected that a risk premium of about $7-9 per barrel will quickly disappear, with Brent prices possibly reaching the low $60 per barrel range (significant possibility).

The first scenario, "No Supply Disruptions: De-escalation and Reduction of Risk Premiums," is set as a reference scenario with considerable probability. The core assumption of this scenario is that the current significant U.S. military deployment and diplomatic pressure in the Middle East are sufficient to prompt Iran to make negotiating adjustments on the nuclear issue, thus avoiding direct military conflict. In this case, military threats mainly serve as leverage rather than a prelude to actual action; sanctions enforcement may remain strict but will not impose substantial additional restrictions on current Iranian export flows.

As a result, this scenario has no impact on the physical supply of crude oil: Iranian exports remain roughly at recent levels, and regional transportation through the Strait of Hormuz is also unimpeded. The main impact on the market is that the geopolitical risk premium currently embedded in the front-end crude prices will disappear. The report, based on regression analysis of OECD commercial inventories and the Brent M1-M4 calendar spread (i.e., the spread between near-term contracts and long-term contracts) over the past 25 years, points out that the current inventory levels should correspond to a market structure of a flat or slightly positive spread (Contango), rather than the existing backwardation. Currently, the Brent M1-M4 spread is about $1.75 per barrel; if the market clearly realizes that there will be no physical supply disruption, this spread could revert to the level implied by the regression analysis (close to zero).

This means that if the front end of the crude oil futures curve turns to a positive spread while long-term prices remain stable, then the front-end (spot) Brent price could drop from around $70 per barrel to the low $60 range. Thus, an estimated geopolitical risk premium of about $7 to $9 per barrel may dissipate relatively quickly under the scenario of de-escalation. Most price adjustments are likely to happen within days to weeks, rather than months, especially if market participants are confident that regional supply and transport flows will remain uninterrupted.

The report cites the market performance following the Iran-Israel conflict in June 2025 as a precedent, noting that at that time, oil prices soared due to fears of escalation, but within weeks of confirming that energy infrastructure and transport were not substantively impacted, prices quickly returned to pre-conflict levels, reinforcing the idea that when physical supply is not compromised, the establishment and dissipation of risk premiums can be very rapid. Ultimately, volatility will compress, and the dominant factor in market pricing will shift from geopolitical risk back to the fundamentals of physical supply and demand.

·Scenario 2 (Limited Strikes and Short-term Logistics Friction): Targeted military actions occur, avoiding energy facilities. This may lead to a supply disruption of 0-0.5 million barrels per day, lasting 1-3 weeks. Oil prices may briefly spike to the mid-$70 range, but China's slowdown in strategic reserve accumulation will become a key balancing mechanism, after which prices will return to the low $60 range (significant possibility).

The second scenario, "Limited Strikes and Short-term Logistics Friction," describes a plausible path of developments. This scenario assumes the U.S. undertakes a targeted military strike, deliberately avoiding energy infrastructure. In response, Iran adopts a calibrated countermeasure aimed at demonstrating deterrence internally while avoiding broader conflict escalation, and regional actors also refrain from direct involvement. In this case, maritime transport through the Strait of Hormuz will continue, without lasting interruptions.

Consequently, any physical supply impact is most likely to stem from secondary logistics friction rather than infrastructure damage. These frictions may include cautious and delayed tanker transport lasting for several days, temporary increases in insurance rates, stricter sanctions enforcement, and traders' limited self-restraining behavior. Based on this, the report assesses the potential scale of supply interruption as relatively mild, around 0 to 500,000 barrels per day, and temporary, expected to last 1 to 3 weeks. There is even the possibility that regional strikes will not translate into lasting export losses as seen in the June 2025 incident.

Under this scenario, even if there were temporary shortages on the scale mentioned, the available idle capacity of Saudi Arabia and the UAE would be sufficient to offset this interruption, thus limiting the risk of long-term physical imbalance. However, the initial market reaction will still focus on front-end prices. Brent prices may be pushed higher to the $75 to $80 per barrel range due to short-term risk premiums, and the spread between near-term and long-term contracts (M1-M4) will also widen from current levels.

However, the more critical balancing mechanism in this scenario will be reflected on the demand side, particularly through adjustments in inventory behavior rather than end consumption. Over the past six months, China's implied crude oil inventory accumulation has averaged about 800,000 barrels per day. In an environment where oil prices are rising, especially with the deepening backwardation in the front end, the speed of such voluntary strategic reserve accumulation is likely to slow.

The report predicts that when oil prices enter the mid-$70 range per barrel, the willingness to accumulate inventories will weaken. Even a slowdown in China's inventory accumulation from recent highs to more normal levels (for example, around 300,000 barrels per day) could compensate for the impact of a 500,000 barrels per day temporary disruption in Iranian exports.

In the second scenario, the market's price reaction will be "high initially, low later." In the beginning, prices will rise due to risk pricing, but as logistics frictions ease, OPEC idle capacity calms the market, and China's inventory demand slows, the futures curve and prices are expected to compress again, ultimately returning to the low $60 per barrel level. This normalization process may take longer than in the first scenario, possibly extending from weeks to months, but will not result in sustained, substantial price increases.

·Scenario 3 (Local Iranian Export Disruption): Broader strikes lead to localized disruptions in the Iranian export chain but do not affect maritime shipping. This may cause disruptions of 0.8-1.5 million barrels per day, lasting 4-10 weeks. Price trends will be between Scenario 2 and Scenario 4 (low probability).

The third scenario, "Local Iranian Export Disruptions: Broader Strikes but No Shipping Damage," is viewed as a low probability escalation path. This scenario assumes that the U.S. launches a broader military action targeting a wider range of strategic assets within Iran, but other regional actors still avoid direct involvement, and the crucial shipping lane through the Strait of Hormuz does not suffer sustained damage — that is, there are no ongoing escort mechanisms or systemic shipping shocks. The primary objective of the military action is not energy infrastructure, but its scale is sufficient to cause significant localized damage to Iran's export chain.

The core transmission channels are operational rather than structural. Possible impacts may include intermittent disruptions to loading operations at key export terminals (such as Khark Island), temporary power or communication outages affecting terminal operations, and short-term constraints in logistics from oilfields to terminals. Meanwhile, the sustained tightening of sanctions enforcement and self-restrictive commercial behavior may keep actual export volumes below normal levels even after military operations cease.

In this scenario, a reasonable outcome would be a significant and prolonged decline in Iranian exports — greater than in Scenario 2, but not reaching the regional shipping efficiency shocks embedded in Scenario 4. The effective supply loss assessed by the report is about 800,000 to 1.5 million barrels per day, lasting approximately 4 to 10 weeks, depending on the nature of operational disruptions and the speed at which export logistics normalize.

Market reactions are likely to focus on the front end of the curve. It is expected that spot spreads will widen, supported for a longer duration than in Scenario 2, reflecting more persistent physical supply tightness. However, due to the lack of sustained shipping damage, the likelihood of the acute mismatch described in Scenario 4 occurring is relatively low. In this scenario, the balancing mechanisms will be more relevant than in Scenario 2 but remain effective: Saudi Arabia and the UAE have the capacity to offset a significant portion of more than a million barrels per day of shortages, but the speed of any response and market confidence in that response will be critical to price dynamics; on the demand side, higher oil prices and a deepening backwardation structure are expected to suppress autonomous inventory demand, especially in China, providing an additional buffer.

Therefore, price trends will be between the short-term spikes of Scenario 2 and the violent surges of Scenario 4. As evidence accumulates showing that the disruptions are operational and reversible, the futures curve will begin to compress; but given the longer duration of the export interruptions and the time needed for the market to validate the sustained recovery of Iranian export volumes, the normalization process will be slower than in Scenario 2.

·Scenario 4 (Fleet Efficiency Shock: Regional Maritime Leverage and Shipping Damage): Tail risk. The main mechanism is tanker delays that reduce effective shipping capacity, thereby reducing global crude oil exports. This translates to a sustained supply loss of 200-300 million barrels per day for several weeks. Price trends may emulate early 2022, although the duration may be significantly shorter (tail risk).

The fourth scenario, "Fleet Efficiency Shock: Regional Maritime Leverage and Shipping Damage," is defined as a low probability but potentially high impact "tail risk" event. This scenario assumes that after a large-scale American strike, Iran undertakes significant countermeasures that exploit its maritime influence in the Gulf region without attempting to completely close the Strait of Hormuz. Such actions could include repeated fast boat harassment, selective seizures of tankers, drone overflights, missile demonstrations, and other measures aimed at significantly increasing navigational risks and uncertainties. While commercial shipping may continue, its pace will be forced to slow, insurance rates will soar, and some shipowners may temporarily withdraw capacity, possibly leading to the reintroduction of naval escorts or convoy operations, all of which will effectively extend the turnaround time for ships.

The main impacts in this scenario do not stem from interruptions in oilfield production, but rather from declines in fleet efficiency. For example, approximately 11 billion ton-miles of crude oil is currently transported via maritime routes each day, with about 1.1 billion of those originating from locations behind the Strait of Hormuz. The average transit time for these cargo flows is around 29 days. If enhanced security protocols, escort operations, and route delays increase the average transit time by, say, 5 days, then the effective productivity of ships operating on these routes would decline by approximately 5/29, or about 17%.

Applied to the cargo flows originating from Hormuz, this means that effective transport capacity would be reduced by nearly 2 billion ton-miles per day, equating to 6% of globally available oil shipping capacity. Given the current maritime crude oil flow of approximately 50 million barrels per day, this could translate to a "effective supply tightening" of 2-3 million barrels per day over several weeks.

From a supply-demand balance perspective, such disruptions are likely to exceed the buffer provided solely by the pause in autonomous inventory accumulation in China, and will test the practical limits of Saudi Arabia and the UAE's idle capacity. In this regard, the price and curve response could begin to mirror the dynamics seen in early 2022, when markets questioned whether the available buffers were adequate to absorb millions of barrels per day in shortages and accordingly re-priced the front end of the curve. Market reactions would likely concentrate on the front end of the curve: Brent prices could sharply spike, as near-term spot spreads widen significantly due to refiners and traders vying for immediately available crude oil.

However, in contrast to 2022, the primary balancing mechanisms may not necessarily require a sustained reduction in end-user consumption: higher prices and steeper backwardation are expected to suppress autonomous inventory demand (particularly in China) and accelerate adaptive adjustments in shipping and operations, thus helping to limit the duration of mismatches.

Expected freight rates will also surge. As operational adjustments take effect, and if transportation can continue under high risk, this effective tightening will gradually ease. However, during the period of shipping damage, prices may soar well above the levels described in Scenario 2, and the normalization process will depend on the restoration of maritime security confidence in the Gulf region.

Price predictions are adjusted but still anchored in Scenarios 1 and 2.

The above scenario framework reflects recent uncertainty surrounding geopolitically driven supply risks. Nonetheless, our core view remains anchored in Scenarios 1 and 2, suggesting that there will be little to no significant disruption to physical supply.

If such an outcome occurs in the coming weeks, our regression framework (linking OECD commercial inventories to the Brent M1-M4 calendar spread) indicates that the geopolitical risk premium of about $7-9 per barrel embedded in near-term Brent oil prices could dissipate, leading the curve to flatten out toward levels implied by current inventory conditions, with spot prices dropping to the low $60 range.

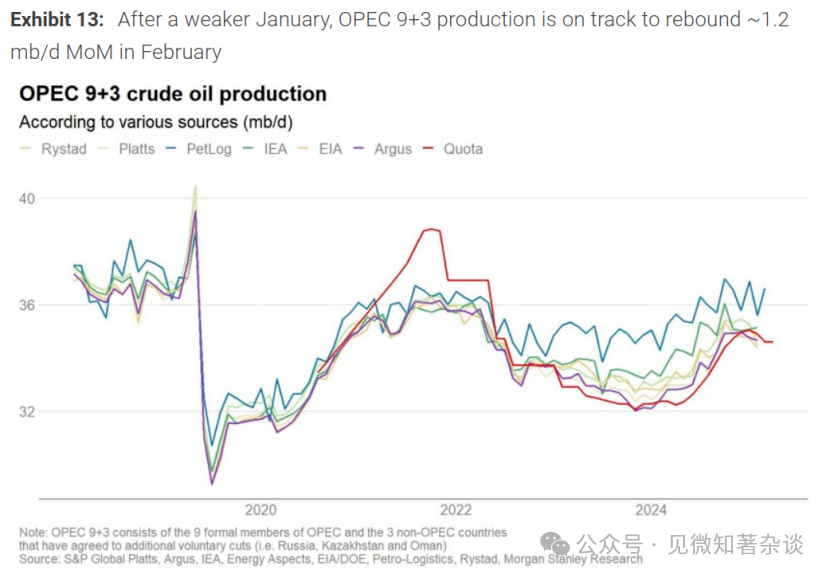

However, beyond the immediate future, our fundamentals remain weak. Due to temporary supply disruptions (including from Kazakhstan and the U.S.), the supply-demand balance in January was tighter than we expected, but these interruptions appear to be reverting. Additionally, early tracking data from Petro-Logistics indicates that OPEC+ production is expected to rebound by about 1.2 million barrels per day month-on-month in February.

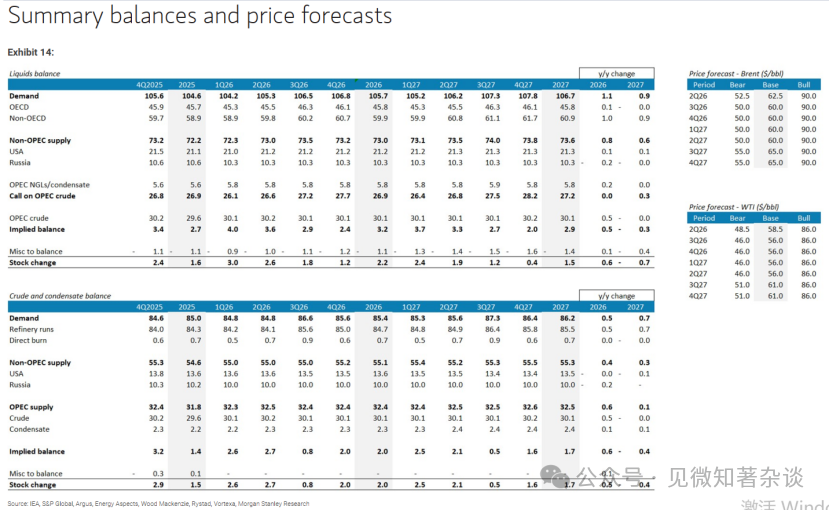

Consequently, our crude oil balance still points towards a surplus of about 2.5 million barrels per day in the first half of 2026 and a surplus of about 1.4 million barrels per day in the second half of 2026.

We assume that approximately 800,000 barrels per day of surplus will be absorbed through inventories in China, but we do not assume that floating inventory at sea will increase significantly as it did in 2025. This means an estimated surplus of 600,000 to 1.7 million barrels per day will need to be absorbed by land-based inventories outside of China, including a substantial portion in the commercial stocks of the OECD/Atlantic basin pricing centers.

Historically, such a scale of inventory absorption may require Brent futures curve front ends to revert to modest contango later in the year. Applying our regression relationship to the projected inventory trajectory suggests that while recent de-escalation may pull Brent prices back to the low $60 range, inventories accumulating in the second half of the year in the OECD, under purely fundamental conditions, could be consistent with deeper contango and front-month prices near the high $50 range.

However, in practice, prices are unlikely to be dictated purely by fundamentals. Recent weeks have again highlighted that geopolitical risk premiums can provide substantial support on the front end, particularly when prices soften, creating a negative feedback loop when prices decline.

On this basis, our baseline expectation is that as we move into 2026, the near-term Brent oil price will gradually slide toward around $60 per barrel, but we believe that unless there is clearer and more sustained relief from geopolitical risks, there is limited room for prices to remain significantly below this level.

Figure 13: Following weaknesses in January, OPEC 9+3 production is expected to rebound by about 1.2 million barrels per day in February.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。