Author: Zen, PANews

Telegram has recently come back into the spotlight due to a financial report directed at investors: while revenue is on the rise, net profit has taken a downturn. The key variable here is not a slowdown in user growth, but rather the decline in the price of TON, which has impacted the asset side and penetrated into the profit statement.

The sale of over $450 million worth of TON tokens has led the public to reassess the relationship and boundaries between Telegram and the TON ecosystem.

Telegram's Revenue Soars Amidst Low TON Prices, Yet Still Reports Net Loss

According to an FT report, Telegram achieved a significant revenue leap in the first half of 2025. The unaudited financial report shows that the company's revenue reached $870 million in the first half of the year, a 65% year-on-year increase, significantly surpassing the $525 million from the first half of 2024; it achieved nearly $400 million in operating profit.

In terms of revenue structure, Telegram's advertising revenue grew by 5% to $125 million; premium subscription revenue surged by 88% to $223 million, nearly double that of the same period last year. However, the key factor driving Telegram's revenue growth primarily comes from an exclusive agreement signed with the TON blockchain—TON has become the exclusive blockchain infrastructure for Telegram's mini-program ecosystem, bringing in nearly $300 million in related revenue.

Overall, Telegram continued to experience strong growth from the mini-game craze that began in 2024—during that year, Telegram achieved its first annual profit of $540 million, with total annual revenue reaching $1.4 billion, far exceeding the $343 million in 2023.

Of the $1.4 billion revenue in 2024, about half came from its so-called "partnerships and ecosystem," roughly $250 million from advertising, and $292 million from its premium subscription services. Clearly, part of Telegram's growth is attributed to the surge in paid users, but even more so from the revenue generated through its cryptocurrency-related collaborations.

However, the high volatility of cryptocurrencies also poses risks for Telegram. Even though it achieved nearly $400 million in operating profit in the first half of 2025, Telegram still reported a net loss of $222 million. Insiders indicated that this was due to the company having to revalue its holdings of Ton token assets. Due to the continued slump of altcoins in 2025, the price of Ton tokens fell continuously, dropping over 73% at its lowest point.

Selling $450 Million: Cashing Out or Upholding Decentralization Principles?

Having witnessed the long-term slump in altcoin prices and the substantial losses of many DAT-listed companies, retail investors are not particularly surprised by Telegram's losses due to the depreciation of virtual assets. What has surprised and displeased the community more is the FT report that Telegram has been selling off its TON tokens, with sales exceeding $450 million. This figure surpasses 10% of the current circulating market value of the token.

As a result, the continuous decline in TON prices, combined with Telegram's sale of a large amount of tokens, has sparked doubts and controversies among some members of the TON community and investors regarding its "selling tokens for cash" and betraying Ton investors.

According to a public statement from Manuel Stotz, chairman of the board of TONStrategy (NASDAQ: TONX), all TON tokens sold by Telegram are set to unlock in four-year installments. This means that these tokens cannot circulate in the secondary market in the short term, preventing immediate selling pressure.

Additionally, Stotz stated that the main buyers Telegram is dealing with are long-term investment entities like his own company, TONX. They are purchasing these tokens for long-term holding and staking. TONX, as a publicly listed investment company focused on the TON ecosystem in the U.S., primarily intends to use the tokens acquired from Telegram for long-term strategic purposes rather than for speculative trading.

Stotz also emphasized that the number of Ton tokens held by Telegram has not significantly decreased after the transactions and may have even increased. This is because Telegram exchanged part of its existing holdings for locked-up token distributions and can continue to generate new TON revenue through advertising revenue sharing and other business activities, maintaining a high level of holdings overall.

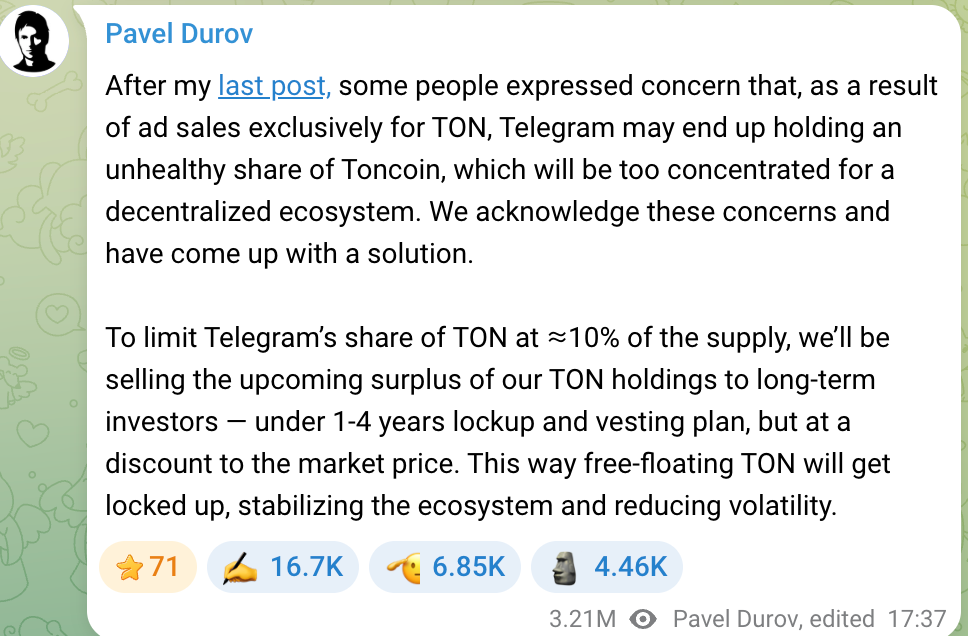

Telegram's long-term business model of acquiring TON tokens has previously raised concerns among some community members—specifically, that the company holds too high a proportion of tokens, which is not conducive to the decentralization of TON. Telegram founder Pavel Durov has taken this concern seriously, stating as early as 2024 that the team would keep Telegram's holdings of TON below 10%. If holdings exceed this standard, the excess will be sold to long-term investors to ensure a broader distribution of tokens while also raising development funds for Telegram.

Durov emphasized that these sales would be conducted at a slight discount to market price, with lock-up and vesting periods set to avoid short-term selling pressure and ensure the stability of the TON ecosystem. This plan aims to prevent the concentration of TON tokens in Telegram from raising concerns about price manipulation and to uphold the project's decentralization principles. Therefore, Telegram's token selling behavior appears more like a part of asset structure adjustment and liquidity management rather than a simple high-price sell-off for profit.

It is worth noting that while the continued decline in TON prices in 2025 has indeed put pressure on Telegram's financial reports, in the long run, the close binding of Telegram and TON has created a situation of shared prosperity and loss.

Through deep involvement in the TON ecosystem, Telegram has gained new revenue sources and product highlights, but it must also bear the financial impacts of cryptocurrency market volatility. This "double-edged sword" effect is also a factor that investors must consider when evaluating Telegram's value as it contemplates an IPO.

Telegram's IPO Prospects

With improved financial performance and business diversification, Telegram's IPO prospects have become a focal point in the market. The company has raised over $1 billion through multiple rounds of bond financing since 2021; in 2025, it issued $1.7 billion in convertible bonds, attracting participation from internationally renowned institutions such as BlackRock and Abu Dhabi's Mubadala.

These financing measures not only provide Telegram with capital but are also seen as preparations for an IPO. However, Telegram's path to going public is not without challenges, as its debt arrangements, regulatory environment, and founder factors will all influence the IPO process.

Telegram currently has two main bonds outstanding: one with a 7% coupon maturing in March 2026, and another with a 9% coupon maturing in 2030. Of the second $1.7 billion bond, approximately $955 million is used to refinance old bonds, while $745 million is new funding for the company.

The unique aspect of the convertible bonds is that they include an IPO conversion clause: if the company goes public before 2030, investors can redeem or convert at about 80% of the IPO price, equivalent to a 20% discount. In other words, these investors are betting that Telegram will successfully IPO and achieve a significant valuation premium.

Currently, Telegram has used the debt refinancing in 2025 to redeem or repay the vast majority of the bonds maturing in 2026 ahead of schedule. Durov has publicly stated that the old debts from 2021 have been largely settled and do not pose a current risk. In response to the impact of the $500 million Russian bond freeze on Telegram, he stated that Telegram does not rely on Russian capital, and there are no Russian investors in the recently issued $1.7 billion bonds.

Therefore, Telegram's main debt now consists of the convertible bonds maturing in 2030, leaving a relatively ample window for an IPO. However, many investors still expect Telegram to seek an IPO around 2026-2027, achieving debt-to-equity conversion and opening new financing channels. If this window is missed, the company will have to bear long-term debt interest pressure and may lose the opportunity to transition to equity financing.

When investors assess Telegram's IPO value, they also focus on its profit prospects and revenue-sharing model. Telegram currently has about 1 billion monthly active users and an estimated 450 million daily active users, providing a large user base that allows for commercial imagination. Although the business has grown rapidly in the past two years, Telegram still needs to prove that its business model can achieve sustainable profitability.

The good news is that Telegram currently has absolute control over its ecosystem. Durov recently emphasized that he remains the sole shareholder of the company, and creditors do not involve company governance.

Thus, Telegram may be able to sacrifice some short-term profits to gain long-term user stickiness and ecosystem prosperity without being constrained by short-sighted shareholders. This "delayed gratification" strategy aligns with Durov's consistent product philosophy and will become a core part of the growth story told to investors along the IPO path.

However, it is important to emphasize that the IPO does not solely depend on financial and debt structures. The FT points out that Telegram's potential listing plans are currently still affected by the judicial proceedings against Durov in France, and the related uncertainties make the timeline for the IPO difficult to clarify. Telegram has also acknowledged in its communications with investors that this investigation may pose an obstacle.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。