This article aims to provide detailed information for cryptocurrency asset institutions and compliance researchers, assisting them in understanding the regulatory "red lines" and differences across jurisdictions, thereby better managing compliance risks in cross-border operations.

Author: Yang Huiping (Northwest University of Political Science and Law)

01 Introduction

The cross-border liquidity of blockchain and cryptocurrency assets presents regulators in various countries with the challenge of balancing the encouragement of financial innovation and the prevention of systemic risks. Against this backdrop, different jurisdictions have gradually outlined several non-negotiable "regulatory red lines" to regulate public chain asset trading activities and protect investors' rights. For example, anti-money laundering (AML) and know your customer (KYC) requirements have almost become a global consensus, with major jurisdictions generally incorporating virtual asset service providers (VASPs) into their AML legal frameworks[1]. Additionally, trading platforms implementing independent custody and segregation of client assets to ensure that client assets are not harmed by third-party creditors in the event of bankruptcy is also seen as a regulatory baseline requirement. Furthermore, preventing market manipulation, curbing insider trading, and avoiding conflicts of interest between trading platforms and related parties have become common goals for regulators in various countries to maintain market integrity and investor confidence[2][3].

Despite the convergence in these key areas, significant divergences remain among jurisdictions on certain emerging issues. Regulation of stablecoins is a typical example: some countries restrict stablecoin issuance to licensed banks and impose strict reserve requirements, while others are still in the legislative exploration stage[4][5]. In the area of cryptocurrency derivatives, a few jurisdictions (such as the UK) directly prohibit the sale of such high-risk products to retail investors[6]; while some countries regulate trading through licensing systems and leverage limits. The legal status of privacy coins (anonymous cryptocurrencies) also varies greatly: some countries explicitly prohibit exchanges from supporting privacy coin trading, while others have yet to legislate against it but indirectly suppress the circulation of privacy coins through stringent compliance requirements[7]. Additionally, in the regulatory paths for tokenization of real-world assets (RWA) and decentralized finance (DeFi), jurisdictions have differing attitudes: some actively establish sandbox experiments and special regulations to manage such innovations, while others prefer to incorporate them into existing securities or financial regulatory frameworks.

To systematically analyze the aforementioned convergence and divergence, this article selects representative jurisdictions such as the United States, the European Union / United Kingdom, and East Asia to conduct a comparative study of cross-jurisdictional regulatory systems. Chapters two to five focus on specific topics of regulatory red line consensus and institutional divergence, elucidating the regulatory provisions of different jurisdictions by citing actual regulatory article numbers, official documents published by regulatory agencies, and typical institutional practices or cases[2][8]. Chapter six summarizes the similarities and differences in regulatory experiences across jurisdictions and discusses the institutional implications and impacts of this regulatory landscape on the global cryptocurrency asset market. The concluding section of the article presents reflections on future international regulatory coordination and industry compliance development.

Through this research, the article aims to provide detailed information for cryptocurrency asset institutions and compliance researchers, assisting them in understanding the regulatory "red lines" and differences across jurisdictions, thereby better managing compliance risks in cross-border operations, and also providing policymakers with a comparative perspective to explore possible paths for advancing regulatory coordination at the global level.

02 Consensus on Regulatory Red Lines: Fund Compliance and Asset Security

This chapter explores the two most universally agreed-upon bottom lines in global regulation: anti-money laundering (KYC/AML) and client asset segregation. Although there is a general trend towards convergence, there are still notable differences in specific implementation paths.

2.1 Global Standards for Customer Identification and Anti-Money Laundering (KYC/AML)

Since 2018, the extension of anti-money laundering (AML) and combating the financing of terrorism (CFT) requirements to the cryptocurrency sector has become a global regulatory consensus. At the international level, the Financial Action Task Force (FATF) revised Recommendation 15 in 2019, bringing virtual asset service providers (VASPs) under the same strict AML/CFT obligations as traditional financial institutions[1]. The FATF also introduced the "Travel Rule," requiring VASPs to collect and transmit identity information of the transaction initiator and recipient during large cryptocurrency transactions[13]. This global standard has set a benchmark for domestic legislation in various countries. By 2025, the vast majority of major jurisdictions have incorporated VASPs into their national AML regulatory systems, establishing customer identification (KYC), suspicious transaction reporting, and other systems. According to the latest FATF report, 99 jurisdictions worldwide have enacted or advanced relevant regulations to implement the Travel Rule, enhancing the transparency of cross-border virtual asset transactions[14].

In the United States, AML obligations are primarily established by the Bank Secrecy Act (BSA, 1970) and its accompanying regulations. The Financial Crimes Enforcement Network (FinCEN), under the Department of the Treasury, has explicitly recognized since 2013 that most cryptocurrency trading platforms fall under the category of "money services businesses" (MSB) and must register with FinCEN and comply with BSA regulations[2]. Specific requirements include: implementing written customer identification programs (CIP), collecting and verifying basic information such as name, address, and identification number; conducting customer due diligence (CDD) to identify the beneficial owners of corporate clients and understand the purpose of customer transactions[15]; maintaining transaction records and reporting suspicious activities (SAR) to authorities, among others. Additionally, the U.S. included tax reporting obligations for cryptocurrency transactions in the 2021 Infrastructure Bill and is considering legislation to strengthen information collection on non-custodial wallet transactions. In terms of enforcement, U.S. authorities have repeatedly filed lawsuits and imposed penalties on cryptocurrency companies for violating AML regulations: for example, the well-known derivatives exchange BitMEX was deemed a "money laundering platform" for failing to implement KYC/AML, with its founder admitting to violating the BSA and paying a $100 million fine[16][17]; another case involved a former Coinbase employee charged with "profiting by circumventing KYC regulations" in an insider trading case, highlighting the regulatory authorities' crackdown on money laundering and fraud in the cryptocurrency industry.

Since the adoption of the 5th Anti-Money Laundering Directive (5AMLD) in 2018, the European Union has included virtual currency exchanges and custodial wallet service providers within the scope of AML regulation, requiring them to register and fulfill KYC/AML obligations[18]. Member states have revised domestic regulations accordingly (such as Germany's Anti-Money Laundering Act and France's Monetary and Financial Code) to implement identity verification and suspicious reporting for cryptocurrency service providers. In 2023, the EU officially passed the Markets in Crypto-Assets Regulation (MiCA, Regulation No. (EU) 2023/1114), establishing a unified authorization system for cryptocurrency asset service providers (CASP)[19]. MiCA itself primarily focuses on market regulation and investor protection, but in parallel, the EU reached agreements on the Anti-Money Laundering Regulation (AMLR) and amendments to the 6th Anti-Money Laundering Directive (6AMLD) in 2024, imposing higher due diligence and beneficial owner identification requirements on obligated entities, including CASPs[20]. Furthermore, the EU plans to establish a dedicated Anti-Money Laundering Authority (AMLA) to enhance cross-border supervisory coordination. This means that every cryptocurrency trading platform operating within the EU must establish rigorous KYC procedures, continuously monitor customer transactions, and cooperate with law enforcement agencies to combat money laundering activities, or face penalties such as license revocation and hefty fines.

Asian financial centers are also closely following international standards, establishing AML regulatory frameworks for cryptocurrency assets. Regulatory agencies in jurisdictions such as Hong Kong, Singapore, and Japan emphasize that both centralized exchanges and other types of VASPs must establish comprehensive AML compliance mechanisms and must not become conduits for money laundering and illegal fund flows.

Hong Kong revised the Anti-Money Laundering and Terrorist Financing Ordinance (AMLO) in 2022, implementing a mandatory licensing system for virtual asset service providers (VASP) starting in June 2023[21]. According to this ordinance and the guidelines from the Securities and Futures Commission, trading platforms must strictly implement customer identification, risk assessment, transaction monitoring, and regular audits, and comply with the Travel Rule requirements by timely reporting customer and transaction information to counterparties[21].

Singapore incorporated digital payment token service providers under the Payment Services Act (PSA) in 2019, with the Monetary Authority of Singapore (MAS) issuing a notice (PSN02) to detail AML/CFT requirements, including applying the Travel Rule to virtual asset transfers exceeding SGD 1,500 and implementing enhanced due diligence for non-custodial wallet transactions[22].

Japan amended the Fund Settlement Act and the Act on Prevention of Transfer of Criminal Proceeds (Anti-Organized Crime Profits Act) as early as 2017, requiring cryptocurrency exchange operators to register with the Financial Services Agency and fulfill KYC and anti-money laundering obligations[23]. Japan mandates that exchanges verify information such as name and address when opening accounts for customers, monitor transactions, and conduct additional reviews for transactions exceeding certain amounts (e.g., equivalent to 100,000 yen)[23]. Notably, Japan is also one of the active promoters of the Travel Rule, having incorporated this requirement into domestic law, mandating the transmission of sender and receiver information for virtual asset transfers exceeding 100,000 yen[24].

From the above comparison, it can be seen that KYC/AML regulation has become a "bottom line" consensus in the global cryptocurrency trading field: although jurisdictions differ slightly in legislative techniques and enforcement intensity, they all recognize that strengthening customer identity verification and transaction transparency is the primary step to protect the financial system from criminal abuse[1]. The formation of this consensus has led to a certain degree of unified compliance thresholds for cross-border cryptocurrency businesses—global institutions must meet the KYC standards of various jurisdictions and cooperate with suspicious fund monitoring, or they will find it difficult to obtain operational licenses. However, at the same time, differences in enforcement intensity and specific rules among jurisdictions still exist (for example, the U.S. criminal prosecution of violators, the EU's strong emphasis on unified regulation, and the Asian region's focus on licensing management), which requires companies to consider regulatory details in different regions when formulating global compliance strategies.

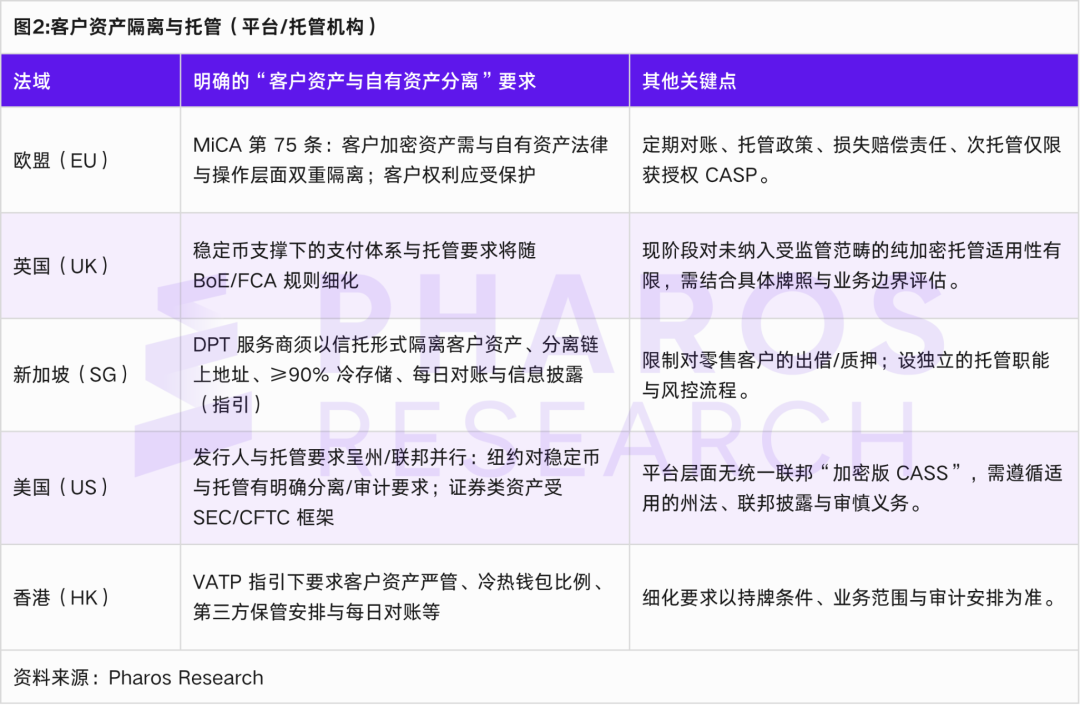

2.2 Independent Custody and Segregation of Client Assets

Client asset segregation is one of the core systems in financial regulation to protect investor interests and prevent the transmission of institutional bankruptcy risks. In the traditional securities and futures sector, many countries already have mature rules (such as the SEC's customer fund protection rules in the U.S. and the FCA's Client Asset Rules in the UK) to ensure that brokers keep client funds separate from their own. For cryptocurrency trading platforms, a series of recent events (including the collapse of a global exchange at the end of 2022 due to the misappropriation of client funds) has increasingly highlighted the importance of client asset segregation. Regulators across jurisdictions generally recognize that platforms must not mix user-held digital assets with their own assets, and it is strictly prohibited to use client assets for lending or investment without authorization; otherwise, in the event of a financial crisis at the platform, investor rights will be severely compromised. This has become one of the regulatory red lines in major jurisdictions.

The European Union has set clear requirements for the custody and segregation of client cryptocurrency assets in the Markets in Crypto-Assets Regulation (MiCA). MiCA stipulates that authorized cryptocurrency asset service providers (CASPs) must legally and operationally segregate client assets from their own when holding cryptocurrency on behalf of clients[3]. Specifically, CASPs should clearly identify client assets on a distributed ledger and ensure that the records distinguish between tokens held by clients and the company's own tokens[3]. MiCA further emphasizes that client assets are legally independent of the CASP's property, meaning that even in the event of platform bankruptcy, creditors have no right to claim the cryptocurrency assets held in custody for clients[25]. In other words, clients have ownership or beneficial rights over their custodial assets, which do not convert to general creditor claims due to platform bankruptcy. This provision is consistent with the existing principle of asset segregation for investors in the EU securities sector. Articles 67 and 68 of the official text of MiCA published in June 2023 (Regulation (EU) 2023/1114) detail the custody obligations and asset segregation measures for CASPs, including achieving separate accounting for client assets and their own assets at both the technical and operational levels, as well as establishing corresponding internal controls and audit mechanisms to ensure effective segregation[26][27]. The EU's move aims to learn from past bankruptcy events of cryptocurrency platforms, eliminate legal uncertainties regarding the ownership of client assets, and provide investors with bankruptcy isolation protection similar to that in traditional finance.

At the federal level in the United States, there is currently no unified legal provision specifically addressing the custody of cryptocurrency assets, but some states and regulatory agencies have begun to take action. Notably, the New York State Department of Financial Services (NYDFS), known for its stringent regulations, issued a guidance statement in January 2023 for institutions holding cryptocurrency custody licenses (i.e., companies holding a New York BitLicense or trust license). NYDFS explicitly requires that cryptocurrency custodians "account separately and segregate client virtual currencies from their own virtual currencies." This can be achieved by establishing independent wallets for each client, maintaining separate internal ledgers, or placing all client assets into a general account that is strictly segregated from their own assets. Regardless of the form adopted, custodians must ensure that client assets are not included in their own balance sheet and must not use them for any purpose other than safe custody. NYDFS also reiterated that custodians must not misappropriate, lend, or encroach upon client assets without explicit instructions from clients. This guidance is seen as NYDFS's regulatory response to recent industry scandals (such as the Celsius and FTX cases), where courts disputed whether client-held cryptocurrency assets belonged to clients or to the bankruptcy estate, resulting in client losses. NYDFS's regulations establish the priority of client assets over other creditor claims. Although the NYDFS guidance only applies to entities with business ties to New York, it is widely regarded as a benchmark for client asset segregation in U.S. practice due to New York's demonstrative role in cryptocurrency regulation. Other states, such as Wyoming, have similar provisions in their Digital Asset Act, confirming the legal status of custodial digital assets as assets held by clients, thereby providing bankruptcy isolation protection.

The Hong Kong Securities and Futures Commission (SFC) has listed "proper asset custody" as one of the core principles that licensed platforms must follow in its 2023 Guidelines for Virtual Asset Trading Platform Operators[5]. According to these guidelines, platforms should take measures to ensure the safe custody of client virtual assets, including using high-security cold wallets to store the majority of client assets and setting strict withdrawal limits and multi-signature permissions for hot wallets. Additionally, the guidelines require "separate holding of client assets," meaning that platforms must clearly distinguish client virtual assets from their own assets. In practice, licensed platforms in Hong Kong typically store client fiat currency in independent trust accounts, while client cryptocurrency assets are kept in dedicated wallet addresses or custody accounts to achieve legal and operational segregation. For example, some platforms claim that 98% of client assets are stored in cold wallets managed by independent custodians, with only 2% used to meet daily withdrawal needs, and they regularly report asset reserves to regulators. These measures aim to prevent platforms from misappropriating client assets for proprietary trading or other uses and to reduce the risk of client losses in extreme situations such as platform bankruptcy or hacking. At the end of 2023, the SFC further issued a notice emphasizing that client asset custody requires strong governance and auditing, requiring executives to regularly review custody arrangements and private key management processes, and to introduce external audits to verify client asset holdings, enhancing transparency. These requirements highlight the importance that Hong Kong regulators place on the safety of client assets, striving to avoid repeating the failures of overseas platforms and maintaining Hong Kong's reputation as a compliant cryptocurrency market.

In Singapore, the Monetary Authority of Singapore (MAS) also examines whether applicants have reliable custody solutions and internal controls during the licensing approval process for digital payment token service providers to ensure that client assets are not misused. Although Singapore has not yet enacted specific regulations for client asset segregation, MAS recommends in its guidelines that licensed institutions store client tokens in independent on-chain addresses, separate from operational funds, and establish daily reconciliation and asset verification mechanisms. In Japan, the Financial Services Agency urged cryptocurrency exchange operators to implement "trustification" of client assets as early as 2018, meaning that client fiat deposits should be entrusted to third-party trust institutions for safekeeping, while requiring that at least 95% of client cryptocurrency assets be stored in offline environments. The 2019 amendment to Japanese law (amendment to the Financial Instruments and Exchange Act) further categorized cryptocurrency assets as financial instruments and formally stipulated that trading operators must verify client assets daily to ensure that the quantity of client assets is not below the required amount, and if it falls below, they must report to regulators immediately. This effectively established a client asset reserve system and is a special form of segregation requirement.

In summary, client asset segregation has become a common bottom line in regulatory practices across jurisdictions. Whether in Europe, the United States, or the Asia-Pacific region, regulatory agencies require cryptocurrency trading platforms to independently custody and manage client assets, and they must not treat them as company property or use them for other purposes[25]. The implementation of this requirement helps protect investors from the risk of internal misappropriation by platform insiders or asset division by creditors, thereby enhancing market confidence. However, when operating across jurisdictions, institutions still need to pay attention to the specific compliance detail differences in different regions. For example, some regions require the introduction of third-party independent custodians, while others allow platforms to self-custody but must meet capital or insurance requirements. These differences will be discussed in related chapters later. Nevertheless, "not misappropriating client assets" has become the red line of all red lines, and any deviation may lead to severe regulatory penalties or even criminal liability.

03 Consensus on Regulatory Red Lines: Combating Market Manipulation and Preventing Conflicts of Interest

This chapter explores two bottom lines related to market fairness: anti-market manipulation and conflict of interest prevention.

3.1 Anti-Market Manipulation: Market Integrity and Manipulation Prevention

The price volatility of the cryptocurrency market and the relative lack of traditional market infrastructure make it susceptible to manipulative behaviors, including wash trading, pump and dump schemes, insider trading, and market manipulation. If market manipulation is allowed to proliferate, it not only infringes on investor rights but may also undermine the market's pricing function and weaken public trust in the cryptocurrency market. Therefore, major regulatory agencies across jurisdictions generally regard combating market manipulation and insider trading as regulatory red lines, requiring trading platforms and related intermediaries to take measures to monitor and prevent suspicious trading activities and report to regulatory authorities when necessary, ensuring a fair and orderly market[4]. Legally, many countries classify severe market manipulation as a criminal offense, applying the same penalties as those in traditional financial markets.

In the United States, the legal framework for anti-manipulation in the securities and derivatives markets is relatively well-developed. For digital tokens classified as securities, the Securities Exchange Act of 1934, Section 10(b), and SEC Rule 10b-5 prohibit any manipulative practices or securities fraud; insider trading is also prohibited and punished under federal securities law and case law. For digital assets considered commodities (such as Bitcoin and Ethereum as recognized by U.S. regulators), the Commodity Exchange Act (CEA) grants the Commodity Futures Trading Commission (CFTC) jurisdiction over manipulation in the derivatives market and allows it to take enforcement actions against fraudulent manipulation in the spot market. In recent years, U.S. law enforcement has actively utilized these laws to combat illegal activities in the cryptocurrency market: for example, in 2021, the U.S. Department of Justice prosecuted a case involving insider trading related to cryptocurrency, accusing an employee of a trading platform of profiting by buying tokens ahead of listing announcements; the SEC concurrently filed securities fraud charges, asserting that the relevant tokens were securities. This was the first enforcement action for "insider trading" in the cryptocurrency sector, demonstrating that the U.S. will not relax its punishment of unfair trading due to differences in asset forms. It is also noteworthy that the CFTC filed a lawsuit in 2021 against an executive of a cryptocurrency trading platform, accusing them of allowing users to engage in wash trading, thereby creating false liquidity to mislead the market, and holding them accountable under the anti-manipulation provisions of the Commodity Exchange Act. Although there is currently no specific legislation targeting manipulation in the cryptocurrency spot market in the U.S., regulatory agencies have initiated multiple enforcement actions using existing laws (securities law, commodity law, and anti-fraud provisions). Additionally, state attorney general offices, such as New York, have utilized broad anti-securities fraud authorities under the Martin Act to investigate trading platforms suspected of manipulation (e.g., the 2018 NYAG investigation report on trading volume fraud at several exchanges). Overall, the U.S. emphasizes the principle of "neutral application of the law," meaning that even emerging cryptocurrency assets may face corresponding regulatory sanctions if they engage in manipulative behaviors similar to traditional securities or commodities.

The European Union has established a comprehensive ban on insider trading and market manipulation in the traditional securities sector through the Market Abuse Regulation (MAR). However, MAR primarily applies to financial instruments on regulated markets and does not directly cover most cryptocurrency assets. To fill this gap, the EU has introduced market integrity obligations for cryptocurrency assets in MiCA. Article 80 of MiCA requires that anyone professionally engaged in cryptocurrency trading must not use insider information to trade related assets and must not engage in manipulative behavior. Additionally, MiCA mandates that CASPs operating trading platforms establish market monitoring mechanisms capable of identifying and addressing market abuse[4]. Specific measures include: trading systems must incorporate monitoring algorithms to detect signs of manipulation, such as abnormal large orders and frequent order cancellations; maintaining trading order during sharp price fluctuations to prevent market manipulation; setting thresholds for price changes or trading volumes to automatically reject orders that exceed reasonable limits; and promptly reporting any suspicious manipulation or insider trading to the competent authorities. Furthermore, MiCA requires platforms to continuously disclose bid and ask quotes and depth information, as well as timely publish transaction data to enhance market transparency and reduce the space for opaque operations. These provisions essentially draw on the EU's experience in the securities market, applying the principles of "same business, same risks, same rules" to cryptocurrency trading. In 2025, the EU is also considering new anti-money laundering regulations (AMLR) that propose to ban anonymous trading and privacy coins (as discussed later), which is also a measure to prevent market manipulation (increasing traceability). In terms of enforcement, with the implementation of MiCA, securities regulatory authorities in member states (such as France's AMF and Germany's BaFin) will have clear authority to address manipulation in the cryptocurrency market. For example, if someone incites collective buying of a token in a Telegram group to inflate the price and then sells for profit, it may be deemed a violation of market manipulation prohibitions and subject to penalties. This indicates that the EU is gradually extending market abuse regulation to the cryptocurrency sector, achieving regulatory extension and equitable consistency.

The Hong Kong Securities and Futures Commission (SFC) requires licensed platforms to establish market monitoring departments or systems to monitor abnormal trading in real-time when issuing virtual asset trading platform licenses. According to SFC guidelines, platforms should promptly identify and prevent attempts to manipulate the market, such as wash trading through related accounts and false order cancellations, and maintain logs for regulatory inquiries. If significant suspicious manipulation is detected, the platform must report it to the SFC and law enforcement. Although Hong Kong has not yet classified cryptocurrency assets under the market manipulation offenses in the Securities and Futures Ordinance (since most cryptocurrencies are not defined as securities), licensed platforms still have a compliance obligation to ensure market fairness. This is a practice of "implementing regulatory objectives through licensing conditions." In Singapore, the Monetary Authority of Singapore (MAS) applies the market manipulation and insider trading provisions of the Securities and Futures Act (SFA) to digital tokens listed on regulated markets (such as recognized exchanges) if they are classified as securities or derivatives. However, for pure cryptocurrency trading that is not included in the definition of financial instruments, Singapore currently mainly relies on industry guidelines to require traders to self-monitor. Nevertheless, MAS has issued multiple warnings emphasizing the risks of money laundering and manipulation in the cryptocurrency market, reminding investors to be vigilant. In 2025, Singapore is also considering amending relevant laws to include certain token trading behaviors that involve public interest under the Financial Market Conduct Act, such as prohibiting the dissemination of false or misleading information that affects token prices, to address the lack of enforcement basis.

Notably, to assist regulation and platforms in fulfilling monitoring obligations, some specialized blockchain analysis companies and market regulatory technology solutions have begun to be applied in anti-manipulation efforts. For instance, some trading platforms use on-chain analysis tools to monitor the rotation of funds among multiple accounts to determine whether "multi-account collusion manipulation" exists; some institutions have developed AI models capable of identifying abnormal price patterns and order book behaviors. Regulatory agencies are increasingly relying on such technologies to enhance monitoring efficiency. For example, the U.S. SEC has established a dedicated cryptocurrency monitoring team that utilizes big data analysis of exchange trading records to detect abnormal fluctuations and investigate whether they are due to manipulation. The EU's ESMA and various national regulators are also exploring the establishment of a cross-platform cryptocurrency trading reporting database to identify cross-market manipulation.

In summary, combating market manipulation and insider trading is a common regulatory red line across jurisdictions, although the specific execution methods differ due to variations in regulatory scope and legal authority. As the trend indicates, with the deepening integration of the cryptocurrency market and traditional finance, countries are increasingly inclined to incorporate cryptocurrency trading behaviors into existing market regulatory frameworks to achieve equal constraints. For instance, the Financial Stability Board (FSB) proposed recommendations in 2023 emphasizing that countries should ensure "effective regulation and supervision of the cryptocurrency market to maintain market integrity," including equipping sufficient enforcement tools to curb manipulation and fraud. This global guiding principle is expected to translate into clearer regulatory requirements across jurisdictions, making manipulation of the cryptocurrency market subject to legal accountability whether in New York, London, or Singapore. For market participants, this means creating a fairer and more transparent trading environment, which is also a necessary condition for the long-term healthy development of the industry.

3.2 Conflict of Interest Prevention: Business Segregation and Internal Governance

Preventing conflicts of interest is a fundamental requirement to ensure that financial institutions fulfill their fiduciary responsibilities and protect client interests. In the cryptocurrency trading sector, potential conflicts of interest include: trading platforms acting as market operators while also engaging in proprietary trading or controlling affiliated market makers, potentially profiting from client order information; platforms issuing their own tokens and listing them for trading, leading to price maintenance and information asymmetry issues; executives or employees engaging in personal trading (insider trading) based on sensitive market information, among others. If left unregulated, these conflicts of interest can harm client interests and market fairness, and even trigger systemic risks (as seen when certain exchanges collapsed due to affiliated companies engaging in high-risk trading that encroached on client assets). Therefore, regulatory agencies in various countries regard the prevention and management of conflicts of interest as one of the red lines, requiring cryptocurrency service providers to establish internal controls and institutional arrangements to identify, mitigate, and disclose potential conflicts.

MiCA sets forth clear and mandatory provisions for CASPs regarding conflict of interest management. According to Article 72 of MiCA[28], cryptocurrency service providers must develop and maintain effective policies and procedures to identify, prevent, manage, and disclose potential conflicts of interest. These conflicts may arise between: (a) the service provider and its shareholders, directors, or employees; (b) different clients; or (c) when the service provider and its affiliates engage in multiple business functions. MiCA requires service providers to assess and update their conflict of interest policies at least annually and to take all appropriate measures to address conflicts. Additionally, service providers must prominently disclose the nature, sources, and mitigation steps of general conflicts of interest on their official websites to keep clients informed. For CASPs operating trading platforms, MiCA further stipulates that they should have particularly robust procedures to avoid conflicts of interest in trading with clients, including preventing transactions with proprietary orders in the matching system and restricting platform personnel from trading based on undisclosed information. MiCA also authorizes regulatory technical standards to refine disclosure formats, indicating that the EU views conflicts of interest as a key area requiring strong regulatory intervention. One of the considerations behind MiCA is to learn from the risks posed by proprietary and affiliated transactions in some past exchanges, ensuring "fair play in the same arena": platforms cannot operate a casino while simultaneously betting themselves and misleading other gamblers. It is worth mentioning that MiCA not only requires service providers to manage conflicts themselves but also includes similar provisions for asset-referenced stablecoin issuers, such as requiring the disclosure of potential conflicts arising from managing reserve assets, reflecting the EU's unified regulatory demand for various entities to establish firewalls against conflicts of interest.

The traditional financial markets in the U.S. have long had systems in place to address conflicts of interest (such as the separation of exchanges and broker-dealer proprietary trading, and firewall regulations for banks). Currently, there are no specific regulations mandating trading platforms to separate their businesses or prohibit proprietary trading in the cryptocurrency sector, but regulatory officials have repeatedly expressed concerns about the risks of "vertical integration." For example, a commissioner of the U.S. Commodity Futures Trading Commission (CFTC) publicly stated in 2024 that exchanges like FTX, which combine multiple roles such as exchange, broker, market maker, and custodian without external oversight, create significant conflicts of interest and risks, and that regulators should establish rules to limit such vertically integrated structures. The statement noted that the collapse of FTX "highlighted the severe dangers posed by the lack of regulation on conflicts of interest." Although FTX was not fully regulated in the U.S. at the time, its failure prompted U.S. lawmakers and regulators to reflect on whether similar provisions to "separate trading and advisory businesses" in the Securities Act should be established for cryptocurrency exchanges. Currently, some proposals in the U.S. Congress (such as the draft Digital Commodity Consumer Protection Act of 2022) have considered prohibiting cryptocurrency trading platforms from engaging in certain activities that conflict with client interests, such as prohibiting exchanges from lending out client assets or restricting their affiliates from participating in platform trading, but these bills have not yet passed. On the other hand, U.S. regulatory agencies have advocated for conflict of interest prevention through enforcement actions. For instance, the U.S. Securities and Exchange Commission (SEC) mentioned in warnings to platforms like Coinbase that allowing executives to sell tokens in advance and the platform's own investments in listed token projects could constitute conflicts of interest and harm investors, necessitating adequate disclosure and control. Additionally, the U.S. Department of Justice has prosecuted certain practitioners for allegedly profiting from trading based on undisclosed token listing information, which also falls under the punishment for insider conflicts. Furthermore, at the licensing level, the New York State Department of Financial Services requires BitLicense holders to submit conflict of interest policies that outline personal trading restrictions for directors and executives, as well as mitigation measures for potential conflicts arising from the company's multiple business activities. These measures indicate that while the U.S. does not have a comprehensive regulatory framework like MiCA, enforcement and regulatory actions are gradually incorporating conflict of interest prevention into the compliance focus for cryptocurrency platforms.

The Hong Kong SFC explicitly requires licensed platforms to avoid conflicts of interest in its Guidelines for Virtual Asset Trading Platforms. Specific measures include: platforms must not engage in any form of proprietary trading for their own accounts (i.e., they cannot act as "market makers"); if there are affiliated companies within the platform group engaged in market-making activities, they must report to the SFC and ensure strict information barriers (Chinese Walls) to prevent insider information leaks; personal cryptocurrency trading by platform executives and employees is also subject to restrictions, requiring disclosure and internal compliance approval. Additionally, if a platform intends to list tokens that have a vested interest (such as tokens from projects the platform has invested in or native tokens issued by the platform), the SFC requires full disclosure and may deny approval for listing to prevent the platform from "listing with one hand and profiting at the expense of clients with the other." This practice in Hong Kong aligns with its regulatory norms in the securities market, such as separating proprietary trading from brokerage activities and avoiding conflicts between agency trading and proprietary trading. After the SFC issued licenses in 2023, the first batch of licensed platforms publicly declared in their materials that they do not engage in proprietary trading or compete with clients for profits to gain investor trust. This institutionally creates a red line: platforms act solely as intermediaries facilitating transactions, rather than as market counterparties, thereby reducing conflicts of interest by design.

International organizations are also paying attention to this issue. The Financial Stability Board (FSB) explicitly stated in its high-level recommendations on cryptocurrency regulation released in July 2023 that jurisdictions should "ensure that cryptocurrency service providers combining multiple functions are subject to appropriate regulatory oversight, including requirements for conflict of interest and certain functional separations" [26]. This effectively calls for countries to regulate the business models of cryptocurrency trading platforms at a global level, mandating the separation of certain conflicting functions (such as separating trading from custody, and brokerage from market making) when necessary, to prevent a single entity from acting as both athlete and referee. The FSB's position is supported by organizations like IOSCO: in a 2022 consultation report, IOSCO also recommended that regulators require cryptocurrency exchanges to disclose proprietary trading activities, limit improper trading by employees, and possibly draw on structural separation regulatory experiences from traditional finance to reduce conflicts of interest. It is foreseeable that, with the push from the FSB and IOSCO, the principle of "same risks, same functions, same rules" will gradually be implemented in the field of conflict of interest management, and unified international standards may emerge in the near future.

In summary, conflict of interest prevention has been incorporated into the basic requirements for regulating the cryptocurrency industry in various countries. From the mandatory rules of the EU's MiCA to the licensing conditions in places like Hong Kong and Singapore, and to the statements and enforcement actions of U.S. regulators, a clear signal is being conveyed: intermediary institutions such as trading platforms must establish sound internal control mechanisms to eliminate the exploitation of client adverse information for improper benefits, and any discovered violations must be promptly disclosed and stopped. The establishment of this red line helps restore market confidence damaged by several scandals and promotes the industry towards a more transparent and trustworthy direction. For operating institutions, more resources need to be invested in internal governance, such as introducing independent compliance officers to oversee trading, conducting regular conflict of interest risk assessments, and training employees on ethical standards, in order to meet regulatory expectations and maintain their reputation.

04 Regulatory System Discrepancies: Differences in Stablecoin Regulation Paths

Stablecoins, as cryptocurrency tokens pegged to the value of fiat currencies or other assets, have rapidly developed globally, attracting significant attention from regulatory authorities. On one hand, stablecoins are expected to enhance payment efficiency and promote financial inclusion, but on the other hand, their widespread use may impact financial stability and monetary sovereignty, especially when the issuance of stablecoins lacks sufficient reserves or transparency, which poses a risk of collapse (as seen in the 2022 collapse of the algorithmic stablecoin UST). Consequently, countries are exploring regulatory paths for stablecoins. However, due to differences in legislative philosophies and financial systems, stablecoin regulation has become one of the most contentious issues across jurisdictions. The main discrepancies are reflected in areas such as the licensing of issuers, reserve and capital requirements, investor protection measures, and restrictions on trading and usage.

4.1 Licensing and Limits for Fiat-Collateralized Stablecoins

The EU distinguishes stablecoins into two categories in MiCA: first, electronic money tokens (EMT), which are stablecoins pegged to a single fiat currency; and second, asset-referenced tokens (ART), which are stablecoins pegged to a basket of assets or non-fiat values. MiCA imposes strict entry and regulatory requirements for both categories. For EMTs, issuers must obtain a license as a credit institution (bank) or electronic money institution and issue tokens under the supervision of regulatory authorities. Issuers are required to hold high liquidity reserve assets equivalent to the value of the issued tokens (mainly corresponding fiat currency deposits or high-quality government bonds) to ensure 1:1 redemption capability. MiCA also prohibits paying interest to EMT holders to prevent competition with deposits. Notably, to prevent stablecoins outside the Eurozone from impacting monetary policy, MiCA introduces limits on trading usage: for non-euro-pegged stablecoins (such as USDT pegged to the dollar), their daily trading volume must not exceed €200 million or 1 million transactions; otherwise, the issuer must take measures to restrict usage (including suspending issuance or redemption if necessary). This dual threshold of "€200 million/day" and "1 million transactions/day" aims to prevent any single stablecoin from becoming overly popular and replacing the euro for payments. This is a unique preventive regulatory measure in the EU that has garnered significant attention (referred to as the "stablecoin trading hard cap"). Additionally, MiCA imposes higher requirements on issuers identified as significant stablecoins (Significant EMT/ART), including more frequent reporting, stricter liquidity management, and reserve custody rules. Starting in 2024, the provisions regarding stablecoins in MiCA will take effect, and issuers must fully comply after a transition period; otherwise, they will not be allowed to provide stablecoin-related services within the EU. This framework represents the most comprehensive and stringent stablecoin regulation globally, benchmarked against the regulatory standards for payment instrument issuance in traditional finance.

In contrast to the EU, the U.S. currently lacks federal-level regulations specifically for stablecoins, creating a significant regulatory vacuum. In recent years, the U.S. Congress has issued several reports and draft bills regarding stablecoins. The 2021 President's Working Group (PWG) report recommended that stablecoin issuance should be limited to regulated deposit-taking institutions (such as banks) and called for congressional legislation. Subsequently, proposals such as the "Stablecoin Transparency and Protection Act" and the "Digital Commodity Stablecoin Act" emerged, but none passed due to differing opinions. As a result, under current laws, stablecoin issuers can only operate within existing frameworks: some companies regulated under trust charters (such as Paxos and Circle through state trust licenses) issue stablecoins under the supervision of state financial regulators; other unlicensed offshore companies (such as Tether) issuing USDT operate outside U.S. regulation, only subject to some constraints due to their bank custody accounts being influenced by U.S. laws. Federal regulatory agencies can only exert indirect pressure; for example, the Office of the Comptroller of the Currency (OCC) allowed national banks to issue stablecoins in 2021 but attached prudential conditions, while the Federal Reserve and FDIC warned banks to be cautious in participating in stablecoin reserve activities. At the state level, the New York Department of Financial Services (NYDFS) was the first to implement reserve and audit requirements for stablecoins under its regulation (such as NYDFS-approved BUSD and USDP), and in 2022, NYDFS issued guidelines requiring that dollar stablecoins issued in New York must be 100% backed by cash or short-term U.S. Treasury securities, with daily redemption and no interest. Wyoming has also passed innovative laws allowing digital asset reserve banks (SPDIs) and newly established stablecoin institutions to issue stablecoins, but there have been no successful cases yet.

In the absence of unified rules, the U.S. stablecoin market is highly fragmented: major players like Tether and Circle self-regulate to maintain high reserves and regularly disclose asset proofs, but vulnerabilities still exist (as seen with the collapse of the TerraUSD algorithmic stablecoin in a regulatory vacuum). This regulatory gap has raised alarms among U.S. lawmakers, and in the second half of 2023, Congress attempted to push the "Stablecoin Regulatory Act" again, aiming to establish a federal licensing system and grant the Federal Reserve oversight authority over non-bank stablecoin issuances. However, the legislative process remains uncertain. In this context, U.S. authorities are temporarily managing risks through enforcement actions: for example, the SEC has issued warnings regarding certain stablecoins suspected of being securities (such as a dollar stablecoin issued by a social media platform), while the Commodity Futures Trading Commission (CFTC) has classified mainstream stablecoins as commodity assets and reserved enforcement rights. Overall, U.S. stablecoin regulation is currently in a state of "regulatory lag, state-level self-regulation, and scattered federal guidance," significantly differing from the EU's comprehensive legislative model.

Japan has taken a relatively conservative approach to stablecoin regulation. In June 2022, the Japanese Diet passed amendments to laws such as the Fund Settlement Act, which clarified the legal status and issuance qualifications of stablecoins for the first time. The new law classifies stablecoins as "electronic payment instruments," requiring that they can only be issued by regulated legal entities: including registered banks in Japan, restricted remittance businesses (which must have high capital), or trust companies [6]. This provision excludes general private enterprises, meaning entities like Tether cannot legally issue stablecoins in Japan. The new law also stipulates that qualified stablecoins must be pegged to the yen or other fiat currencies and can be redeemed at face value by holders. Additionally, the issuance of algorithmic stablecoins and other non-collateralized forms is prohibited. Regarding reserves, a requirement for 100% fiat collateral deposits with regulated institutions is mandated.

Moreover, the Japanese Financial Services Agency is very cautious about the entry of foreign stablecoins into the Japanese market; currently, major overseas stablecoins (such as USDT) are basically not listed on Japanese exchanges, while yen-pegged coins issued by trust companies (such as the "Progmat Coin" issued by Mitsubishi UFJ Trust) are under testing. In 2024, Japan is discussing further restrictions: for example, the Financial Services Agency proposed not allowing ordinary banks to issue stablecoins directly on public blockchains (considering the risks to be high, only trust banks, etc., can issue), and requiring comprehensive application of KYC/travel rules for stablecoin transfers. Under the Japanese model, stablecoins resemble a substitute for bank deposits, strictly constrained by banking laws and payment regulations, reflecting a high emphasis on financial stability and consumer protection. The advantage of this model is high security, but the downside is that it suppresses non-bank innovation. Currently, there has not been large-scale circulation of stablecoins in Japan, but if major banks plan to issue yen stablecoins, they will operate entirely within the regulatory framework, with relatively controllable risks.

The Hong Kong Monetary Authority (HKMA) released a discussion paper in 2022, clearly stating that algorithmic stablecoins are not allowed and planning to focus on regulating payment-type stablecoins pegged to fiat currencies. The "Stablecoin Ordinance" (draft name) was completed in 2023 and is set to take effect in August 2025 [7]. This ordinance requires that any stablecoin issued or circulated in Hong Kong that is pegged to a fiat currency must be issued by an entity licensed by the HKMA. The license application must meet strict conditions: including establishing a physical presence in Hong Kong, having a certain statutory capital, and implementing risk management and technical audits. The ordinance requires issuers to hold 100% reserve assets (limited to high liquidity assets) and redeem stablecoins at face value when requested by holders. It also grants the HKMA supervisory inspection rights, allowing it to review reserve status and operations. A unique aspect of Hong Kong's regulation is that it is not limited to banks issuing stablecoins but ensures that any issuer is subject to similar prudential regulation as banks. This may leave some space for non-bank fintech companies to issue stablecoins, but the regulatory costs are also not low. Hong Kong plans to complete the first batch of license approvals in 2024-25, emphasizing a gradual approach with a small number of initial licenses. It is noteworthy that the Hong Kong ordinance includes stablecoins under the scope of anti-money laundering regulations, requiring issuers and dealers to implement KYC/AML obligations. This move by Hong Kong signifies the establishment of a stablecoin regulatory benchmark in another financial center in the Asia-Pacific region, differing from Singapore, which has not yet legislated and primarily relies on guidance. For the market, Hong Kong's framework provides a pathway for compliant issuance and operation of stablecoins, likely attracting stablecoin issuers seeking licensed operations to apply.

4.2 Capital and Reserve Requirements for Non-Fiat-Collateralized Stablecoins (Asset-Referenced Tokens)

In addition to stablecoins pegged to a single fiat currency, some stablecoins are backed by a basket of fiat currencies, commodities, or cryptocurrency assets (such as the early concept of Libra, which was pegged to multiple reserve assets), or maintain their peg through algorithmic collateralization. These are referred to as "asset-referenced tokens" (ART), and their value stabilization mechanisms are more complex, with higher risks. Regulators in various countries tend to adopt a more cautious attitude towards ARTs. Especially after the Libra project (later renamed Diem) triggered a global regulatory backlash in 2019, most jurisdictions have clearly stated that such multinational basket currencies may threaten financial sovereignty and stability and should be subject to strict regulation.

The EU's MiCA includes asset-referenced tokens (ART) within its regulatory scope, requiring issuers to obtain licenses and comply with a series of requirements similar to those for electronic money tokens (EMT), including white paper disclosures, reserve custody, capital, and liquidity plans. However, given that ARTs are pegged to non-single fiat currencies, MiCA imposes stricter regulations: first, ART issuers must hold a relatively higher minimum capital (at least €350,000 or reserves worth 2%), which is higher than the requirements for EMT issuers. At the same time, ART issuers must establish clear reserve asset custody policies to ensure that reserve assets are completely segregated from the issuer's own assets and cannot be misappropriated. MiCA stipulates that reserve assets can be held by qualified custodians (such as licensed CASP custodians or banks) and requires that reserves be highly diversified to reduce correlation risks. Additionally, ART issuers must establish a regular audit mechanism, disclosing reserve composition and audit reports quarterly to enhance transparency. For significant ARTs, MiCA authorizes regulatory authorities to impose additional requirements, such as limiting business scale or requiring more detailed risk analyses. The EU also prohibits issuers from providing any additional profit incentives to ART holders, aiming to prevent ARTs from effectively becoming investment products. Overall, MiCA's requirements for ART encompass governance, risk management, and user protection, with the hope of bringing their risks down to a controllable level.

In the U.S., following the Libra incident, multiple departments jointly pressured the project, forcing it to modify its design or even terminate it. Although no specific laws have been enacted, it can be inferred that if a similar ART were to emerge, the U.S. might invoke the Dodd-Frank Act's Title I (systemically important payment instruments) or securities laws to regulate it. For example, if an ART involves a basket of securities as reserves, the SEC might classify it as an ETF fund share, requiring registration; if it involves payment functions and is of significant scale, the Financial Stability Oversight Council (FSOC) might designate the issuer as a systemically important institution under the Federal Reserve's supervision. Currently, there are no large-scale ART operations in the U.S. market (most mainstream stablecoins are single-coin pegged), so regulatory discrepancies mainly manifest in positions. Federal Reserve officials have indicated that multi-currency stablecoins may require special central bank scrutiny. Some U.S. think tanks suggest that such stablecoins should be treated as "shadow banking currencies," requiring their issuers to comply with strict asset composition limits and reserve requirements similar to money market funds. However, due to a lack of practical cases, the U.S. has not formed a fixed path for this. In terms of enforcement, if an ART leads to investment losses, regulatory agencies may invoke commodity or securities laws. For instance, the algorithmic stablecoin Ampleforth was investigated by the SEC for potentially selling securities through an ICO, as its algorithmic nature (pegging to a basket of assets or algorithmic formulas) did not exempt it from securities law constraints. These instances reflect the "principle-driven" nature of U.S. regulation: there are no specific laws, but relevant laws will be applied as needed.

In Singapore, a public consultation on stablecoins was held in 2022, proposing rules for single-currency stablecoins (such as requiring the primary reference currency to be a G10 currency and minimum reserve asset quality requirements), but it tends to discourage multi-asset-backed stablecoins for the time being. The Monetary Authority of Singapore (MAS) believes in first regulating single-currency stablecoins and then deciding whether to allow more complex structures based on international consensus. Currently, Hong Kong's regulations mainly target fiat-pegged coins, directly excluding tokens pegged to non-fiat currencies (such as algorithmic stablecoins and commodity-backed coins) from consideration for licensing. The South Korean Financial Services Commission stated in 2023 that it does not allow trading of algorithmic stablecoins and holds a negative attitude towards any stablecoins with yield or complex mechanisms. Japan, only allowing fiat-pegged stablecoins, naturally has no space for ARTs. In summary, there are significant differences in stablecoin regulation between Europe and the U.S.: the EU has established a detailed framework through MiCA, especially specifying requirements for international basket currencies; the U.S. is still discussing and exploring, with a short-term focus on single-coin stablecoin legislation. Major Asian economies are mostly cautious and positioned tightly. This disparity means that companies engaged in stablecoin business must navigate vastly different compliance requirements when expanding globally. In the EU market, they need to obtain licenses and monitor daily trading volumes to not exceed thresholds; in the U.S. market, although there are no explicit licensing requirements, they face uncertain regulatory risks and potential enforcement; in regions like Japan and Hong Kong, they may directly encounter licensing restrictions or bans. Therefore, regulatory discrepancies are particularly pronounced in this field and have become a key challenge for future international regulatory coordination.

05 Regulatory System Discrepancies: Market Access and Innovation Boundaries

This chapter discusses three other topics with significant cross-jurisdictional regulatory differences: regulation of cryptocurrency derivatives trading, the legality of privacy coins, and regulatory explorations of real-world asset tokenization (RWA) and decentralized finance (DeFi). Due to issues involving investor protection, criminal enforcement, technological anonymity, and the boundaries of financial innovation, countries have adopted different strategies, and no unified international standards have yet been established.

5.1 Market Access and Investor Protection for Cryptocurrency Derivatives

Cryptocurrency derivatives refer to contract products such as futures, options, and contracts for difference (CFD) based on the prices of cryptocurrency assets. These products can be used for hedging and speculation, amplifying both returns and risks. High leverage and volatility make them extremely dangerous for ordinary investors. Traditional financial markets have strict access requirements for derivatives trading (such as exchange and clearinghouse licenses), while in recent years, many cryptocurrency derivatives platforms have operated offshore without licenses, attracting global users. Countries' regulatory attitudes towards this vary: some allow and regulate, some restrict retail participation, and some completely prohibit it. This has become one of the most direct manifestations of regulatory differences in the cryptocurrency market.

The U.S. classifies Bitcoin, Ethereum, and others as commodities, thus their futures and options fall under commodity derivatives, governed by the Commodity Exchange Act (CEA). The Commodity Futures Trading Commission (CFTC) is the primary regulator, requiring any facility providing cryptocurrency derivatives trading to U.S. persons to register as a designated contract market (DCM) or swap execution facility (SEF), and brokers must register as futures commission merchants (FCM), among other requirements. Platforms and intermediaries must also comply with customer asset protection and trading reporting regulations. To date, the U.S. has approved a few compliant exchanges to offer cryptocurrency futures (such as the Chicago Mercantile Exchange's Bitcoin futures launched in 2017), but these markets mainly target institutional and professional investors, and trading volumes are relatively limited. The vast majority of retail investors prefer to access unregistered platforms (such as the former BitMEX, Binance, etc.), which violates U.S. law. The CFTC has conducted strict enforcement against such platforms in recent years: in 2021, the CFTC and FinCEN jointly penalized BitMEX for illegally providing trading to U.S. persons and violating AML rules; in 2023, the CFTC sued Binance and its CEO, accusing them of evading U.S. regulations for years, allowing U.S. users to trade high-leverage derivatives, and failing to fulfill customer identity verification and manipulation monitoring obligations. These actions indicate that the U.S. considers "offshore platform enforcement" an important means of protecting domestic investors. It is worth noting that the U.S. also restricts retail participation in highly complex derivatives: for example, the SEC does not allow retail investors to purchase CFDs or certain over-the-counter derivatives associated with cryptocurrency assets, and the CFTC has not promoted complex swaps to retail. Overall, the U.S. model allows cryptocurrency derivatives, but trading must occur within a regulatory framework, and any attempts to circumvent regulation will be severely punished. This model is consistent with the U.S. approach to other financial derivatives (where "no permission means illegal"). However, for derivatives not classified as commodities (such as options based on security tokens), the SEC may also intervene. For instance, the SEC has warned that certain platforms offering swap contracts based on unregistered security tokens may be illegal. It is evident that the U.S. views different regulatory classifications based on the attributes of the targets, but the core principle is that all derivatives require licensing, with no room for regulatory arbitrage.

The UK's Financial Conduct Authority (FCA) announced in October 2020 a ban on selling or distributing any derivatives and ETNs referencing unregulated cryptocurrency assets to retail customers after assessing the risks of cryptocurrency derivatives to consumers [8][9]. This ban took effect in January 2021 and covers CFDs, futures, options, and exchange-traded notes (ETNs). This move was the first of its kind globally: UK regulators believed that due to the inability to reliably value cryptocurrency assets, frequent market manipulation, extreme volatility, and consumers' lack of understanding, such products were unsuitable for retail investors. The ban is expected to save UK retail investors approximately £53 million annually. After the ban was implemented, UK retail customers were prohibited from gaining any exposure to cryptocurrency derivatives through UK companies. The FCA warned that any company providing such services to UK retail investors would be considered illegal and treated as a scam. However, by October 2025, the FCA announced it would lift the retail ban on cryptocurrency asset ETNs to enhance the competitiveness of the financial center, while still maintaining the ban on CFDs and other derivatives. Thus, the UK allows regulated venues to sell some approved cryptocurrency ETNs to retail investors, but highly leveraged derivatives remain prohibited. This policy change reflects the UK's attempt to balance investor protection with innovative competitiveness. As of now, UK retail investors wishing to trade Bitcoin futures options still cannot do so through local platforms and can only do so through overseas channels. The UK's firm stance on derivatives is particularly prominent among major economies, leading some active traders to shift to Europe or other markets. Looking ahead, the UK may decide to adjust its strategy after the effects of the EU's MiCA become clear. However, in the short term, protecting retail investors from losses associated with complex high-risk derivatives remains a priority for UK regulation.

In the EU, MiCA itself does not directly regulate derivatives, as MiCA targets the spot market and issuance areas. If cryptocurrency derivatives are physically settled and the underlying is not a financial instrument, they could theoretically fall outside current financial directives. However, many member states have classified cryptocurrency derivatives as a type of financial instrument. For example, Germany's BaFin has determined that cryptocurrency CFDs and futures fall under financial derivatives as defined by the Second Markets in Financial Instruments Directive (MiFID II) and require licensing to operate. France's AMF also requires any platform providing cryptocurrency derivative trading to obtain the corresponding investment service provider qualifications. In 2018, ESMA included cryptocurrency CFDs in its product intervention measures for CFDs, setting a leverage cap of 2:1 (lower than the 30:1 for forex) to protect investors. This indicates that the EU overall tends to allow regulated provision while strengthening risk control. Individual member states have considered stricter measures; for instance, Belgium briefly banned the distribution of cryptocurrency derivatives to retail investors. Currently, there is no unified ban at the EU level like that in the UK; the MiFID framework and various national regulatory practices effectively provide a compliance path for derivatives. Therefore, EU retail investors can trade limited-leverage cryptocurrency CFDs through licensed brokers in places like Cyprus or trade cash-settled Bitcoin ETNs on the European Futures Exchange (Eurex). It is expected that with the implementation of MiCA and updates to EU financial regulations, there may be unified regulations specifically targeting cryptocurrency derivatives (ESMA is already researching this area). However, as it stands, the EU maintains a cautiously open attitude: regulated provision is allowed, but abuse and excessive leverage must be prevented, and investors must be given adequate risk warnings.

Regulatory attitudes towards cryptocurrency derivatives vary significantly across Asian countries. Japan amended its Financial Instruments and Exchange Act in 2019 to classify cryptocurrency derivatives as financial products and implemented registration regulations for businesses engaged in cryptocurrency contracts for difference (CFD) and futures trading. Japanese exchanges can offer cryptocurrency margin trading to customers, but self-regulatory rules have drastically reduced the maximum leverage from 25:1 to 2:1. Therefore, Japanese users can still trade low-leverage Bitcoin contracts, but the market size is limited. South Korea has outright banned domestic exchanges from offering any form of cryptocurrency futures or options, citing excessive risks for retail investors; South Korean investors can only trade through overseas platforms, but the government has strengthened monitoring in recent years, requiring banks to restrict remittances to overseas cryptocurrency derivatives platforms. When Hong Kong introduced its licensing system in 2023, it explicitly prohibited the provision of cryptocurrency derivatives trading to retail investors, allowing only spot trading of the underlying assets; professional investors' participation in derivatives through Hong Kong platforms is also strictly limited. Hong Kong only allows asset management companies approved by the Securities and Futures Commission to issue structured products or ETFs linked to cryptocurrencies for trading in regulated markets (such as cryptocurrency futures ETFs listed on the Hong Kong Stock Exchange, aimed at the public). Singapore's Monetary Authority of Singapore (MAS) takes a cautious stance on derivatives, having approved the listing of Bitcoin and Ethereum swap contracts on the Singapore Exchange (SGX) in 2019, but stipulating that retail investors cannot participate directly, with access limited to institutional and professional investors. Additionally, in 2022, MAS reinforced investor protection guidelines, restricting retail access to high-risk cryptocurrency products, including derivatives, and requiring local service providers not to easily promote any cryptocurrency trading services to the public through ATMs or advertisements. Overall, mainstream markets in Asia largely limit retail access to cryptocurrency derivatives: Japan allows it but with strict regulation and low leverage; Hong Kong, Singapore, and South Korea almost prohibit retail participation, offering limited channels only to institutions/professionals. This contrasts with the more open stance of some Western markets.

The direct impact of the regulatory discrepancies in cryptocurrency derivatives is the "regulatory arbitrage" of global market liquidity. In regions with strict regulations or bans (such as the U.S., U.K., and Hong Kong), many users still access unregulated platforms through VPNs and overseas accounts, creating enforcement challenges. Consequently, trading volumes are concentrated on some large platforms in regions with weak regulation, increasing the risk of accumulation. International regulatory bodies have recognized this issue; in 2023, the Financial Stability Board (FSB) emphasized the need to strengthen cross-border enforcement cooperation in its global cryptocurrency regulatory framework recommendations, urging countries to jointly curb unlicensed cryptocurrency derivatives activities. Additionally, the International Organization of Securities Commissions (IOSCO) released policy recommendations regarding cryptocurrency trading platforms in 2023, which also included regulatory standards for derivatives businesses, such as requiring platforms to disclose leverage settings and liquidation mechanisms. It is foreseeable that the global trend will move towards narrowing these differences: there is a growing consensus to prohibit high leverage for retail investors, while professional markets may develop steadily through licensing. The recent lifting of the ETN ban in the U.K. indicates that a moderate opening of reviewed products may become a trend in balancing protection and development. The EU may not outright ban like the U.K. but will likely strengthen investor protection requirements within frameworks like MiFID, such as mandatory negative balance protection and standardized risk warnings. Some regions in Asia may adjust at the appropriate time; for instance, if Hong Kong verifies the safety of the professional market, it may not rule out limited retail participation in approved derivatives in the future (with accompanying education). In summary, cryptocurrency derivatives regulation is moving from divergence towards convergence, based on international regulatory standards, with jurisdictions gradually tightening their blockade against illegal platforms while balancing market demand within compliant channels.

5.2 The Legal Status of Privacy Coins and Regulatory Challenges

Privacy coins refer to cryptocurrencies that achieve transaction anonymity and address concealment through technical means (such as ring signatures, zero-knowledge proofs, etc.), represented by Monero (XMR), Zcash (ZEC), Dash (DASH), and others. Supporters argue that privacy coins protect financial privacy rights, but regulators are concerned that they are widely used for illegal activities such as money laundering and evading sanctions, as traditional on-chain analysis is nearly ineffective against their transaction flows. Regulatory policies surrounding privacy coins are markedly divergent among countries: some explicitly ban them, some impose strict circulation restrictions, and others have yet to take direct action but indirectly target them through AML rules.

Japan is one of the first countries to ban privacy coin trading. In 2018, influenced by the Coincheck exchange hack (where hackers used anonymous coins to launder assets), the Financial Services Agency (FSA) required domestic registered exchanges to delist all coins with high anonymity features, including Monero and Dash. This requirement was implemented through regulations from the self-regulatory organization, the Japan Virtual Currency Exchange Association (JVCEA), and new exchange licenses cannot list anonymous coins. FSA officials have explicitly stated that anonymous coins violate Japan's anti-money laundering system's "traceability" principle and should not exist in compliant markets. Similarly, after the revision of the Specific Financial Information Act in March 2021, South Korea's Financial Services Commission (FSC) issued guidelines prohibiting virtual asset service providers from handling "anonymous digital assets with untraceable transaction records," leading to the delisting of privacy coins by various South Korean exchanges. South Korea also prohibits the use of mixing services to obscure transaction sources. The Middle East, including Dubai, has followed suit: the virtual asset regulations in Dubai, UAE, in 2023 prohibit the issuance or trading of cryptocurrencies with enhanced anonymity features. The strategies adopted by these jurisdictions are direct prohibitions, believing that such assets do more harm than good and should not be allowed.

The EU has not yet fully banned privacy coins but is moving in that direction. A political agreement reached by the European Parliament and Council on the Anti-Money Laundering Regulation (AMLR) in 2023 proposed to prohibit cryptocurrency service providers from engaging with anonymous wallets or trading anonymous coins starting in 2027. According to information released on May 9, 2025, the EU will require that, starting in July 2027, virtual asset service providers must not offer trading services involving anonymous coins and must perform strict identity verification for transactions involving privately held wallets exceeding €1,000. This means that exchanges operating in the EU will not be able to list privacy coins like Monero and ZEC. Additionally, some EU member states have taken temporary measures: for example, Belgium's financial regulatory authority required local traders in 2022 to report any transactions involving anonymous coins and suggested ceasing support for them. The French AMF has strict licensing regulations, with no privacy coins approved yet. European law enforcement agency Europol has also frequently warned about the obstacles privacy coins pose to tracking criminal funds. This move by the EU has faced criticism from some in the cryptocurrency industry, who argue that it infringes on personal privacy rights. However, from a regulatory perspective, the existence of anonymous coins indeed complicates the enforcement of AML/CFT frameworks, and the FATF has highlighted the risks of anonymity-enhancing technologies in several reports. It is expected that in the years leading up to the implementation of the ban, the EU will gradually reduce the use of privacy coins through softer measures, such as categorizing them as high-risk transactions and requiring increased due diligence, laying the groundwork for the formal ban in 2027. Once the ban takes effect, the EU will become another major jurisdiction, following the U.S., Japan, and South Korea, to exclude privacy coins.