作者: Lacie Zhang, Bitget Wallet 研究员

导语: 美东时间2025年8月7日,一纸来自白宫的行政令,可能将成为继比特币现货ETF之后,引爆加密市场的又一个历史性奇点。美国总统特朗普签署行政令,指示劳工部着手修订规则,拟将加密货币、房地产、私募股权等另类资产(Alternative Assets)正式纳入401(k)养老金计划的投资选项。

这不仅关乎高达8.7万亿美元的美国“国民养命钱”,更可能为机构资本的第二次大规模入场,铺设一条前所未有的合规高速公路。当数千万美国人的退休账户与加密资产直接挂钩,一场深刻的变革已在酝酿之中。

接下来跟Bitget Wallet研究院一起走进这场变革中一探究竟。

一、8.7万亿美元的“金钥匙”:为何401(k)是关键变量?

要理解这场变革的威力,首先需要看懂401(k)在美国养老金体系中的“C位”角色。美国的养老金体系如同一座三足金鼎,共同支撑着国民的退休生活:

| 美国现存三支柱养老金体系——政府+雇主+个人 | |||

| 项目 | 政府社会保障 | 雇主赞助计划 (401(k)等) | 个人退休金计划 (IRA等) |

| 性质 | 由政府运营的公共养老保险 | 雇主提供的退休储蓄计划 | 个人自主开设的退休投资账户 |

| 参与方式 | 强制性,符合条件的员工必须参与 | 自愿性 | 自愿性 |

| 资金来源 | 工资税(由员工和雇主共同缴纳) | 雇员税前供款,雇主按比例匹配 | 个人自有资金存入 |

| 资金管理 | 政府统一管理 | 由个人管理账户 | 由个人管理账户 |

| 投资选择 | 无个人选择权 | 雇主提供的有限投资选项 | 个人可以自由选择投资 |

| 提前取款 | 不允许 | 允许,但需缴纳10%罚金 | 允许,但需缴纳10%罚金 |

| 金额 | 8.9万亿美元 | 12.2万亿美元 | 16.8万亿美元 |

资料来源:Fintax ,此处未考虑保险公司的企业年金储备、私人部门固定收益型保障

- 第一支柱: 政府主导的社会保障(Social Security),类似中国的基本养老保险,具有强制性,但个人没有投资选择权。

- 第二支柱: 雇主发起的退休计划,而401(k)正是其中的绝对主力。它由雇员和雇主共同出资,虽投资选项由雇主预设,但覆盖面广、资金流稳定,是美国中产阶级积累退休财富的核心工具。

- 第三支柱: 个人退休账户(IRA),完全由个人自愿开设和管理,赋予个人极大投资自由度,更像一个“开放的专业市场”,需要参与者主动研究、自行决策。

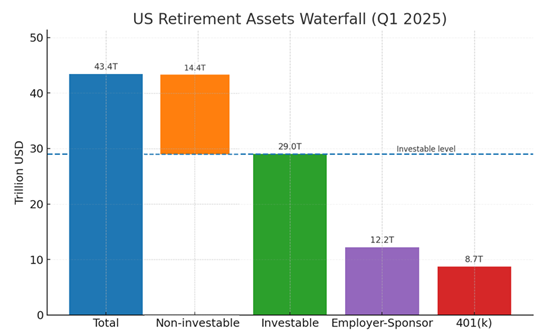

根据美国投资公司协会(ICI)2025年第一季度的数据,美国养老金市场总规模高达43.4万亿美元。在这片广阔的资金海洋中,真正可由个人进行投资决策的部分约为29万亿美元。而在这29万亿美元中,401(k)计划独占8.7万亿美元,占比高达30%。这笔巨额资金,正是此次新政瞄准的“金矿”。

美国401(k)账户分年龄段余额情况(截至2024年)

| 年龄段 | 平均数401(k)余额 | 中位数401(k)余额 |

| 25岁以下 | $6,899 | $1,948 |

| 25至34岁 | $42,640 | $16,255 |

| 35至44岁 | $103,552 | $39,958 |

| 45至54岁 | $188,643 | $67,796 |

| 55至64岁 | $271,320 | $95,642 |

| 65岁及以上 | $299,442 | $95,425 |

数据来源:先锋集团《How America Saves 2024》

先锋集团(Vanguard)在2024年的报告中描绘了401(k)的国民画像:所有参与者的账户平均余额已达148,153美元。尤其值得注意的是,随着年龄增长,账户余额呈指数级上升,65岁以上人群的平均余额接近30万美元。这意味着,401(k)不仅资金体量庞大,其持有者更囊括了美国社会最有购买力的中老年群体。

此前,这笔巨资一直被严格限制在传统的股票、债券和共同基金等领域。如今,特朗普政府打算为它装上一把能开启加密世界大门的“金钥匙”。

二、撬动未来的三重浪:新政如何重塑加密市场格局?

将加密货币纳入401(k)投资范畴,其影响绝非简单的资金流入,而是一场从用户、机构到监管三个层面联动的结构性变革。

1.第一重浪:用户心智的“国家级”破冰

对于加密行业而言,最大的挑战之一始终是“出圈”——如何让主流大众,特别是那些手握重金但思想保守的中老年投资者,接受并配置加密资产。此次改革,堪称一次自上而下的“国家级”市场教育。

试想一下,当一个55岁的美国企业员工在富达(Fidelity)或先锋(Vanguard)提供的401(k)投资菜单上,看到“加密资产配置基金”与“标普500指数基金”、“美国国债基金”并列时,其心理感受将发生颠覆性变化。这不再是社交媒体上遥远而高风险的投机代码,而是经过美国劳工部准许、由顶级资管机构打包、并被自己雇主接纳的合规退休投资品。国家主权信用与顶级金融机构的双重背书,将极大地消除普通人对加密资产的疑虑和抵触情绪,完成一次成本最低、覆盖最广的用户培育。

2.第二重浪:机构资本的“活水”长流

如果说比特币现货ETF的获批,是为机构资本打开了一扇主动式投资的大门,那么401(k)的准入,则是开通了一条源源不断的“自动化输水管道”。ETF的资金流,很大程度上依赖于投资者的主动决策和市场情绪,时而汹涌,时而平缓。而401(k)的资金注入模式则根本不同:它是与美国庞大的国民薪资系统直接绑定的。 这意味着,每个发薪日,都会有数百万份工资的一部分,在持有者几乎无感的情况下,被自动配置到其选定的加密资产投资组合中。这种稳定且庞大的增量资金,将为市场提供前所未有的深度和韧性。

这一确定性的前景,将点燃华尔街巨头们新一轮的产品“军备竞赛”。先锋、富达等机构不会仅仅满足于过去单一的加密产品,而是会转向更多元化、结构化、风险可控的“401(k)定制”加密基金。例如,一个可能包含比特币、以太坊,并辅以部分蓝筹DeFi代币的“一篮子”指数基金,或是一个将加密资产与传统股债结合以平滑波动的“混合配置基金”。这不仅丰富了资本入场的渠道,更将有力推动整个加密资产管理行业走向成熟与规范。

3.第三重浪:跨越党派的“政治护城河”

然而,这项新政最深远的一步,或许隐藏在金融市场的喧嚣之下——它旨在为动荡的加密世界,铸就一道能跨越党派纷争的“政治护城河”。

美国两党轮替带来的政策不确定性,一直是悬在加密行业头上的“达摩克利斯之剑”,从而使得任何长期资本都顾虑重重。民主党与共和党在监管态度上的摇摆,甚至是同一党派不同领导人间的政策差异,都使得行业的长期发展充满变数。而401(k)新政的精妙之处就在于:它将加密资产与数千万美国选民的“养命钱”进行了深度绑定。这釜底抽薪地改变了游戏的性质:加密资产不再是华尔街和技术极客的专属话题,而是变成了每个普通家庭都无法忽视的“全民奶酪”。

设想新政推行开来:任何试图采取严厉打压、甚至推翻现有加密政策的未来政府,都将面临巨大的政治压力,因为任何试图削弱加密市场的举措,都可能被选民直接解读为“动了我的退休金”,从而引发剧烈的政治反弹。这种赤裸裸的利益绑定,使得对加密市场的庇护,从特朗普的个人行为或党派行为,上升为竞选者为拉拢选民、执政者为保护国民财产的“被迫选择”。至此,一道坚固的护城河已然成型,它将迫使两党在加密监管上寻求更稳定的共识,从而让整个行业摆脱因政党轮替而剧烈波动的宿命,将“加密友好”真正焊死在美国的长期金融议程之上。

三、远景与审思:通往万亿蓝海的机遇与挑战

对于这样一项新政,我们有理由保持乐观。正如比特币现货ETF获批后,推动比特币在一年内突破10万美元大关一样:合规产品的巨大发展,势必会引发底层资产的价值重估。即便假设初期只有5%的401(k)资金(约4000亿美元)流入加密市场,这对当前加密行业依旧是一笔巨量资金,更不用说它在用户培育+监管破冰上产生的巨大乘数效应。

长远畅想,如果个人管理的养老金都能投资加密资产,那么由政府代持的、规模更庞大的社会保障基金,未来是否也有可能打开一道门缝?那将是对整个社会财富和金融体系的一次重构。

但同时,乐观不能代替思考,我们也需保持审慎,因为核心挑战依然存在:

- 投资者会买账吗? 目前超过60%的401(k)资产仍集中在传统的共同基金中,要让习惯了几十年投资模式的美国人将退休金投向一个高波动性新兴市场,需要时间和市场的验证。

- 风险如何控制? 加密资产剧烈的周期性波动是退休储蓄的天敌。劳工部、资管机构和雇主三方,将如何划定投资比例、进行风险提示,以保护投资者利益——这些细节将决定政策的成败。

- 产品的形态是什么? 投资范围决定了风险的广度——是坚守在比特币和以太坊,还是向更广阔的代币市场开放。产品设计则决定了风险的深度——如何平滑波动以保护投资者,是悬而未决的关键。

四、结语

特朗普政府的这一行政令,与其说是一个最终答案,不如说是打响了发令枪。它以8.7万亿美元的401(k)为支点,试图撬动的不仅是美国庞大的养老金体系,更是全球加密金融的未来版图。前路有机遇的万顷碧波,亦有未知的暗礁险滩。但无论如何,当退休金这一最传统、最保守的资本开始认真审视加密世界时,一个新时代的大门,正被缓缓推开。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。