I. Introduction

On August 7, 2025, Trump signed an executive order allowing 401(k) retirement pension plans to invest in alternative assets, including private equity, real estate, and cryptocurrencies. This move breaks the long-standing practice in the U.S. of limiting pension investments to stocks and bonds, opening the door for massive pension funds to enter the crypto market. The 401(k) plan is the primary corporate retirement system in the U.S., covering nearly 90 million American workers and managing trillions of dollars in assets. It is foreseeable that even a small portion of 401(k) funds flowing into the crypto market could have a significant impact, given the current total market capitalization of approximately $4 trillion for cryptocurrencies. Following this news, combined with the Federal Reserve's anticipated interest rate cuts starting in September, cryptocurrencies such as Bitcoin and Ethereum surged, further fueling the bull market.

This article will comprehensively analyze this significant policy change from multiple dimensions: first, reviewing the current state and investment landscape of the U.S. pension system and 401(k) plans, interpreting the background and potential impacts of the new policy; then, from a global perspective, comparing the experiences of other countries in pension investments in crypto and assessing the lessons for the U.S. model; next, analyzing the potential positive impact of this policy on the crypto market; and finally, based on this, we will also explore the changes in the crypto market landscape in light of the Federal Reserve's shift in monetary policy and discuss the evolving role of crypto assets in future retirement wealth allocation.

II. Understanding the U.S. 401(k) Pension Plan

1. The "Three Pillars" of the U.S. Pension System

The U.S. pension system consists of three main components:

National-level Social Security: Managed by the federal government, it provides basic retirement income security, covering almost all employed individuals, aimed at ensuring a basic standard of living after retirement.

Employer-sponsored corporate pension plans: Represented by 401(k), primarily aimed at private sector employees, it is the most common employer-sponsored retirement savings method in the U.S.

Individual Retirement Accounts and Annuities (IRAs & Private Annuities): Established and funded entirely by individuals, serving as supplementary retirement savings tools.

2. The Scale and Investment Composition of 401(k)

The 401(k) plan is an employer-sponsored retirement savings plan with tax advantages, primarily for private sector employees. The plan is mainly funded by employee contributions, where employees withdraw a portion of their pre-tax wages to deposit into their 401(k) accounts, and employers typically provide a matching contribution, the specific ratio and rules of which are set by the employer. Since its establishment in 1981, the plan has grown from a supplementary savings tool to the core pillar of the U.S. pension system and the largest corporate pension plan.

According to a report released by the Investment Company Institute (ICI) in June, as of the first quarter of 2025, the total retirement assets in the U.S. amounted to $43.4 trillion, accounting for about 34% of household financial assets. Among these, the total assets of U.S. 401(k) plans reached $8.7 trillion, representing about 20% of total retirement assets, covering over 90 million participants. In 401(k) plans, mutual funds manage assets totaling $5.3 trillion, accounting for 61%; of which equity funds account for $3.2 trillion, and mixed funds hold about $1.4 trillion.

Source: https://www.ici.org/statistical-report/ret_25_q1

In terms of investment composition, 401(k) assets are primarily invested through mutual funds, accounting for as much as 61%. Funds are mainly allocated to traditional financial assets, with equities dominating:

Equity Funds: Approximately $3.2 trillion, accounting for 37% of total 401(k) assets, making it the primary allocation category;

Hybrid Funds: Approximately $1.4 trillion, which includes balanced products like Target Date Funds that automatically adjust asset ratios;

The remaining assets are distributed among bond funds, stable value funds, money market funds, and company stocks.

Overall, the core of the 401(k) investment portfolio is publicly traded assets dominated by stocks, with minimal involvement in alternative assets such as private equity, commodities, and real estate, and no direct allocation to cryptocurrencies like Bitcoin. This traditional allocation model is expected to undergo a historic transformation under Trump's new policy.

3. The 401(k) Investment Landscape Enters the "Alternative Asset" Era

On August 7, Trump signed an executive order allowing ordinary retirement investors to access alternative assets. The order requires the Department of Labor to lead a reassessment of the regulatory guidelines for investing in alternative assets under the current Employee Retirement Income Security Act (ERISA) framework, in collaboration with the Treasury Department, the Securities and Exchange Commission, and others to study whether modifications to relevant regulations are necessary. The executive order clearly defines "alternative assets" as: private market investments, direct or indirect real estate interests, commodities and infrastructure projects, and digital assets (i.e., cryptocurrencies) held through actively managed vehicles. In other words, private equity funds, equity in unlisted companies, and digital assets like Bitcoin are all included in the permitted scope.

However, it is important to note that this executive order does not immediately open up investments but rather initiates a regulatory revision process, with actual implementation expected by 2026. Even so, this policy shift itself conveys a clear message: the U.S. government is willing to endorse the entry of retirement funds into emerging fields like crypto.

III. Attempts by Various Countries to Invest Pension Funds in the Crypto Market

The U.S. initiative to open pension investments in crypto is also symbolically significant on a global scale. Overall, large pension funds in various countries remain very cautious towards crypto assets, but in recent years, there have been some cases of "small trials" and lessons learned.

In Canada, the Ontario Teachers' Pension Plan (OTPP), with approximately $190 billion in assets, invested about $95 million in the crypto exchange FTX through a venture capital fund in 2021-2022. However, FTX's subsequent bankruptcy rendered this investment worthless, accounting for less than 0.05% of the fund's net assets. Although the amount was not large, the incident caused a significant uproar: OTPP not only suffered losses but also faced a class-action lawsuit from its retired members, accusing it of inadequate due diligence. This lesson led OTPP to state that it would avoid any crypto-related investments in the short term. It is evident that negative precedents can make institutions more conservative and serve as a warning to regulators.

In the U.S., a few public pension funds have also attempted to venture into crypto. For example, the Houston Firefighters' Retirement Fund invested $25 million in Bitcoin and Ethereum in October 2021, accounting for about 0.5% of its assets. The fund's management stated that they view cryptocurrencies as a new hedging tool and potential source of growth, not wanting to "ignore" this emerging asset. Due to the small proportion, this investment did not significantly impact the overall portfolio. Similarly, two county-level retirement systems in Fairfax County, Virginia, have gradually allocated small amounts to the blockchain sector since 2018 (approximately 3-5% of their portfolios), involving various forms such as blockchain venture capital funds and crypto yield farms.

In contrast, most mainstream pension plans in Europe and Asia have not yet included cryptocurrencies in their qualified investment scope. On one hand, many countries' pension systems are more focused on government-led or fixed-income assets, with a lower risk appetite compared to corporate pensions in the U.S. and the U.K. On the other hand, regulators in various countries impose strict limits on the investment scope of pensions, emphasizing "responsible investment" of pension assets, with the crypto market being excluded due to issues such as money laundering risks, volatility, and uncertainty. However, some private retirement accounts with autonomous investment authority have begun to dabble in crypto. For example, in Australia, some high-net-worth individuals have allocated Bitcoin through self-managed superannuation funds (SMSF) as part of a diversified investment. In this model, investment decisions are led by individuals, making it more flexible, but it also poses challenges of insufficient expertise and regulatory blind spots. The U.K.'s self-invested personal pensions (SIPP) have also seen cases of purchasing crypto derivatives, but the U.K. financial regulatory authority has imposed strict restrictions on retail investors buying crypto assets.

It is evident that global pensions are still in the exploratory stage regarding crypto assets. The U.S. opening 401(k) investments in crypto will undoubtedly attract the attention and discussion of regulators and the industry in various countries. If the U.S. practice proves successful, other countries may gradually follow suit and relax policies, allowing pensions to share in the benefits of the crypto economy. However, in the short term, it is more likely that only a few forward-looking institutions will attempt small-scale trials, with a long way to go before widespread adoption.

IV. Opportunities and Challenges Brought by 401(k) Funds Entering the Market

Opening the 401(k) pension plan to cryptocurrencies and other alternative assets will significantly enhance the return and diversification of pension portfolios. Supporters point out that in the past, ordinary workers' 401(k) plans could only invest in public funds, while large institutions and wealthy investors could access high-yield areas like private equity and hedge funds, creating an "unfair" situation. Expanding the investment scope of 401(k) plans is expected to allow ordinary investors to "stand on the same starting line as institutions" and share in the appreciation potential of private markets and crypto assets.

For the cryptocurrency market, the entry of 401(k) pensions will not only bring an increase in capital but also symbolize a qualitative change.

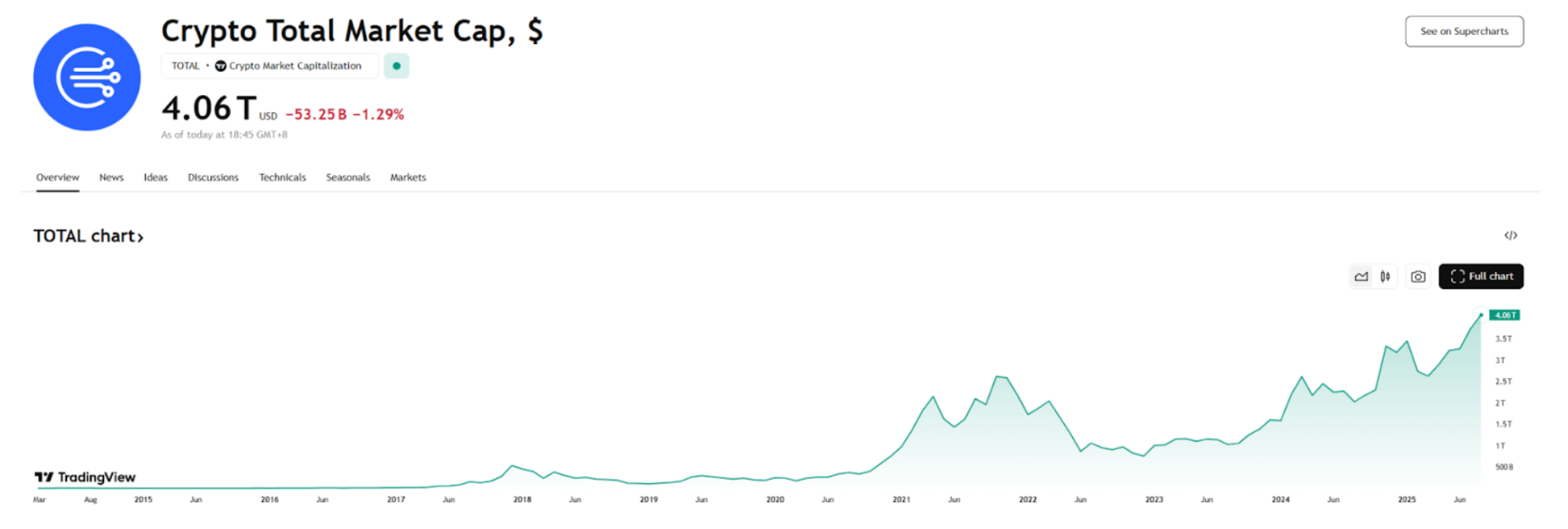

- Increase in Capital: Once the policy is implemented, it means that a dam of U.S. retirement savings will open a gap, allowing some funds to flow into crypto assets. Considering that the 401(k) plan manages nearly $9 trillion in assets, while the current total value of cryptocurrencies is $4 trillion, if 10% of the funds are allocated to the crypto sector, it would equate to nearly $900 billion in potential incremental capital inflow, representing 22% of the current total market capitalization of cryptocurrencies, which would significantly support prices. This change in capital dynamics is undoubtedly a major boon for the long-term development of the crypto market.

Source: https://www.tradingview.com/symbols/TOTAL

Increased Recognition from Institutional Investors: The 401(k) plan is overseen by company trustees and professional advisors, who typically exercise caution in asset selection. Once crypto assets are officially included in mainstream pension options, it will greatly enhance the status of cryptocurrencies like Bitcoin as mainstream investment products, attracting more previously hesitant institutions to participate, thus creating a positive feedback loop. Fidelity Investments announced as early as 2022 its plan to offer Bitcoin investment options to its 401(k) clients (which was temporarily halted due to regulatory concerns), and now that policy barriers have been removed, these products are expected to be rapidly brought to market. It is anticipated that crypto investment tools specifically designed for retirement plans will gradually emerge, such as Bitcoin trust funds for 401(k)s, crypto index funds, and even embedding a small amount of crypto exposure in target date funds.

Improvement of Investor Structure: Pension funds have long-term stability characteristics, which are expected to improve the investor structure in the crypto market and reduce extreme volatility. Unlike retail investors chasing short-term gains, pension allocations emphasize long-term steady appreciation and risk diversification, avoiding large-scale frequent trading. This means that if a portion of 401(k) assets is allocated to Bitcoin, it will exist as "long-term holders," reducing circulation and enhancing market stability. Of course, this effect will take considerable time and sufficient scale to manifest, but it is a positive direction.

Promoting the Integration of Traditional Finance and Crypto Finance: As retirement advisors, custodial banks, and fund companies begin to develop crypto products for 401(k)s, the infrastructure for compliance, custody, and security in the crypto industry will also improve. For example, to meet 401(k) requirements, custodians must address issues such as private key custody and theft risks, as well as liquidity arrangements needed for transactions. The entry of traditional financial institutions will accelerate the establishment of unified standards and best practices in the industry, such as valuation models, performance reporting formats, and fee standards. All of these will enhance the friendliness of crypto assets to mainstream capital.

However, the policy relaxation also faces a series of challenges:

Cost and Liquidity Issues: The trend of 401(k) plans over the past few decades has been to lower costs, widely adopting low-fee index mutual funds, with average management fees now down to 0.26%. In contrast, private equity funds typically charge "2% management fee + 20% performance fee," and crypto investment products generally have higher fees, necessitating careful design of how to introduce such assets into 401(k) plans.

Risk and Information Transparency: The information disclosure and regulation of traditional public market investments are relatively well-established, while private markets and crypto assets suffer from more severe information asymmetry and greater volatility.

Legal Liability and Litigation Risks: There is a potential for collective lawsuits from employees; without clear legal protections, plan trustees and asset managers may be reluctant to venture into these highly volatile areas.

Investor Education Challenges: Educating ordinary participants about the risk-return characteristics of assets like Bitcoin, appropriate allocation ratios, and alignment with retirement goals requires ongoing educational guidance; otherwise, issues such as blind following and bearing volatility beyond risk tolerance may arise.

For the crypto industry, welcoming traditional pension funds represents both a significant opportunity and a major test. Whether it can provide investment tools that reassure regulators and investors, and whether it can prove its value within a strict fiduciary responsibility framework, will determine how far and how fast this long-term capital can go. Nevertheless, once this door has been opened even a crack, it is difficult to close it again. Looking ahead to the next decade, as Millennials and Generation Z gradually become the main participants in pensions, their acceptance of digital assets is higher, coupled with advancements in technology and regulation, the proportion of crypto assets in pension portfolios is likely to gradually increase. This will further drive the expansion of the crypto market and the evolution of its ecosystem, and one day, crypto assets may become an indispensable part of retirement wealth allocation, just like gold and real estate.

V. Conclusion and Outlook: Is the Tailwind for the Crypto Market Here?

The market widely expects the Federal Reserve to announce its first interest rate cut of the year at the September meeting. According to trading data, the probability of a 25 basis point cut in September is nearly 100%, with some even betting on a possible 50 basis point cut. The turning point for monetary easing has emerged, and the atmosphere of shifting from "hawkish" to "dovish" is becoming increasingly pronounced. Since this rate cut is seen as the beginning of a long-term trend reversal and the start of a series of policy relaxations, its medium- to long-term supportive effect on risk assets may become more significant. If the Federal Reserve continues to cut rates and expand its balance sheet to provide liquidity, the crypto market may not just experience a "breeze," but rather a prolonged "period of favorable conditions."

The positive news of 401(k) pension plans entering the crypto market coincides with the macro benefits of the Federal Reserve's expected rate cuts, creating a resonant effect in timing. The former brings structural incremental capital and long-term buying power, while the latter creates an overall favorable funding environment and enhances risk appetite. These two forces complement each other and are expected to shape a new upward trend in the crypto market. The potential entry of pension funds means that cryptocurrencies are likely to transition from marginal assets to a part of mainstream asset allocation; while the shift in the interest rate environment provides fertile ground for a new bull market. In the 2025 time window, we may be witnessing a key step towards the maturity of the crypto industry—from speculative products for a few geeks and institutions to becoming part of the pensions of billions of people.

For investors, it is essential to maintain confidence in long-term trends while being cautious of short-term market volatility and uncertainty. The entry of pension funds is still on the eve of policy implementation, and there may be twists and turns in the process; although the Federal Reserve's policy has shifted to easing, the macroeconomic trajectory still has variables. As the market anticipates, perhaps the spring of crypto has arrived, but we must also learn to sow in the spring and reap in the autumn.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tools. Through our "Weekly Insights" and "In-Depth Reports," we analyze market trends for you; leveraging our exclusive column "Hotcoin Selection" (AI + expert dual screening), we help you identify potential assets and reduce trial-and-error costs. Each week, our researchers also engage with you through live broadcasts to interpret hot topics and predict trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize the value opportunities of Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investing carries risks. We strongly recommend that investors fully understand these risks and invest within a strict risk management framework to ensure the safety of their funds.

Website: https://lite.hotcoingex.cc/r/Hotcoinresearch

[Mail: labs@hotcoin.com](mailto:Mail: labs@hotcoin.com)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。