Witnessing History.

Written by: Zhao Qirui, Lynne

"The digital asset regulatory framework established in Hong Kong, along with its pioneering sandbox use case practices, clearly presents a concrete path for innovation to achieve robust development within a compliant framework. As stated in the 'Hong Kong Digital Asset Development Policy Declaration 2.0', Hong Kong is continuously building a 'trustworthy and innovation-focused digital asset ecosystem' and will continue to consolidate its leading position in the global digital asset field, promoting Hong Kong to become a global innovation center."

Introduction

I. The Development History of Digital Assets in Hong Kong

(1) Prelude: The "Pause Button" in Mainland and the "Fast Forward" Globally (2017-2022)

In 2017, mainland China implemented a comprehensive halt on the virtual asset market, pressing the "pause button" on digital asset development. In September of that year, seven ministries in China jointly issued a notice on preventing risks from token issuance financing, completely halting initial coin offering (ICO) activities and shutting down all domestic virtual currency trading platforms, aiming to effectively clear market risks. Subsequently, the mainland further strengthened its crackdown on "disguised trading" and "over-the-counter trading," and in September 2021, explicitly classified all virtual currency-related businesses (including trading, redemption, intermediaries, advertising, etc.) as illegal financial activities. This series of high-pressure regulatory measures effectively maintained the stability and risk controllability of the financial system.

However, this strict "blockade" inadvertently became a "catalyst" for the global crypto industry, triggering a wave of talent, capital, and projects "going overseas." A large number of Web3 entrepreneurs, technical teams, and funds that were originally active in the mainland began to seek compliant development space overseas, accelerating the sowing and expansion of the Web3 concept globally.

While strict regulations were implemented in the mainland, Hong Kong's role was more cautious and subtle, serving both as a "firewall" to prevent risk spillover and quietly becoming an "observation post" for observing global Web3 development. To encourage fintech innovation while protecting investor interests, the Hong Kong Monetary Authority (HKMA) first launched the "Fintech Regulatory Sandbox" in September 2016, followed by the Securities and Futures Commission (SFC) and the Insurance Authority (HKIA) launching their respective sandboxes, which were upgraded to "Sandbox 2.0" in 2017 for cross-sector coordinated operations. In September of the same year, the SFC issued its first statement on ICOs, indicating that if tokens have "securities" attributes, they may be regulated under the Securities and Futures Ordinance, emphasizing the regulatory principle of "substance over form." Subsequently, the SFC continued to monitor the operations of virtual asset fund managers and trading platforms, and in 2018 launched the fintech regulatory sandbox, allowing companies to test their fintech innovation projects, including those related to virtual assets, in a controlled environment.

On the application level, the Hong Kong government actively explored the practical applications of blockchain technology. For example, in 2020, it completed four blockchain pilot projects covering government service areas such as trademark transfer, environmental impact assessment, pharmaceutical traceability, and company document archiving, to explore the feasibility and benefits of blockchain technology applications. In June 2022, the government further launched a "Shared Blockchain Platform" and planned to develop more general services and reference program modules to assist various policy bureaus/departments in developing more blockchain applications.

In addition, Hong Kong actively explored central bank digital currency (CBDC) and the tokenization of real-world assets (RWA). The HKMA launched the "Digital Hong Kong Dollar" project research in June 2021 and released the "Discussion Paper on Crypto Assets and Stablecoins" in January 2022, proposing a regulatory framework for stablecoins. The HKMA collaborated with the Bank for International Settlements Innovation Hub's Hong Kong Centre to complete the "Project Genesis" project in 2021, aimed at testing the issuance of tokenized green bonds in Hong Kong. In 2022, the Hong Kong government also personally participated in the NFT issuance trial program during Hong Kong Fintech Week, aiming to test the technological benefits brought by virtual assets.

During this period, it is hard not to wonder why Hong Kong, standing firmly with the Chinese people on the financial and economic front, quietly prepared and researched the regulatory framework for virtual assets while the mainland imposed strict regulations. Although it started relatively slowly in terms of policy, its deep foundation as an international financial center, strong traditional financial industry base, and professional financial service capabilities laid the groundwork for a more proactive layout in the future.

(2) The Key Move in the Chess Game: Hong Kong's "Move" and Strategic Intent (2023-2025)

From the end of 2022 to 2023, Hong Kong's digital asset regulatory policy welcomed a landmark turning point, seen as a key "move" in Hong Kong's strategy in the global digital economy chess game. On October 31, 2022, the Hong Kong SAR government released the "Policy Declaration on the Development of Virtual Assets in Hong Kong," for the first time clearly proposing to "actively promote" the development of the virtual asset ecosystem, marking a shift in regulatory thinking from "risk-oriented" to "opportunity-oriented." Subsequently, on December 7, 2022, the "Anti-Money Laundering and Counter-Terrorist Financing (Amendment) Bill 2022" was passed by the Hong Kong Legislative Council, officially establishing a mandatory licensing system for virtual asset service providers (VASP). This system took effect on June 1, 2023, allowing licensed virtual asset trading platforms (VATP) to provide services to retail investors under strict investor protection measures. Thereafter, Hong Kong further approved virtual asset spot ETFs, making it the largest virtual asset ETF market in the Asia-Pacific region. As of June 2025, the SFC has officially licensed 10 VATPs, with another 11 institutions in the application process. Additionally, the Hong Kong SAR government designated the "Stablecoin Ordinance" to officially take effect on August 1, 2025, further improving the regulatory framework for digital assets.

Choosing to "open the door" at this time, I interpret it as a high-level strategic choice at the national level. After the global crypto market experienced a round of wild growth and risk exposure (such as the FTX and LUNA incidents), the market's demand for compliance, transparency, and trust became unprecedentedly strong. At this moment, with Hong Kong as a "bridgehead," representing China to enter the market in a "compliant" and "controllable" manner, consolidating global digital asset resources and competing for the discourse power of the next generation of financial technology is undoubtedly the best timing. Hong Kong's unique "one country, two systems" framework allows it to balance the mission of an international financial center with considerations of financial security in the mainland. HKMA Chief Executive Eddie Yue pointed out that the ordinance establishes a "risk-based, pragmatic, and flexible regulatory environment," providing healthy, responsible, and sustainable development conditions for Hong Kong's stablecoins and broader digital asset ecosystem. Its goal is to significantly enhance the attractiveness to global Web3 talent, capital, and projects through a sound regulatory framework and ecosystem, empowering the real economy and providing new quality momentum for economic development. Thus, Hong Kong is transitioning from a traditional international financial center to a global leading digital asset innovation center, consolidating its strategic position as a bridgehead for the internationalization of the renminbi and a "super connector." Hong Kong's Financial Secretary Paul Chan emphasized that Hong Kong's attitude towards Web3.0 is not just regulatory but aims to achieve a balance, ensuring market integrity while not stifling innovation.

Hong Kong's "first-mover" policy has also received positive responses and interactions from mainland cities, indicating a potential model of "Hong Kong pilot, mainland linkage." For example, Ant Group has listed Hong Kong as its overseas headquarters and successfully passed regulatory sandbox tests. Its RWA (real-world asset) tokenization practices have been validated, such as the collaboration between Longshine Technology and Ant Group to complete the first domestic RWA project based on new energy physical assets, as well as the collaboration between GCL-Poly and Ant Group to complete RWA based on photovoltaic physical assets, all of which were announced through the HKMA's Ensemble project sandbox. These cases demonstrate that Hong Kong's regulatory clarity and international openness are providing important channels for mainland enterprises to participate in the global digital asset market under compliance. A report released by the Bank of China Shenzhen Branch's Greater Bay Area Financial Research Institute and the Bank of China Hong Kong Financial Research Institute suggests summarizing Hong Kong's stablecoin pilot experience to strengthen research on offshore renminbi-linked stablecoins. Furthermore, the Hong Kong SAR government itself has played a guiding role, such as issuing NFTs in 2022, subsequently becoming the first region in the country to issue tokenized government green bonds in 2023, and issuing a second batch of tokenized government green bonds in 2024. This strategic synergy not only promotes the development of Hong Kong's digital asset ecosystem but also builds a new bridge for connecting the mainland with international capital markets.

Long Chart: Major Events in Hong Kong from 2015 to August 2025

II. Hong Kong's "Twin Peaks" Regulatory Framework for Digital Assets

Hong Kong's digital asset regulatory system is characterized by its "Twin Peaks" model, where the Securities and Futures Commission (SFC) and the Hong Kong Monetary Authority (HKMA) collaborate to create a regulatory environment that encourages financial innovation while strictly adhering to risk limits. The essence of this model lies in the clear division of responsibilities: the SFC focuses on the "investment" attributes of virtual assets, while the HKMA concentrates on their "payment" functions. The table below systematically clarifies the functions, legal basis, jurisdiction, and regulatory tone of the two regulatory agencies, providing a clear guide to understanding Hong Kong's regulatory blueprint.

Table: Comparison of Core Regulatory Agencies' Responsibilities

The SFC and HKMA have formed a complementary regulatory pattern through clear functional division and close cooperation (such as signing memorandums of understanding). As the guardian of the securities market, the SFC extends mature investor protection principles to the virtual asset investment field; while the HKMA, as the central body of the financial system, ensures that the innovation of payment tokens does not undermine Hong Kong's monetary foundation. This dual-peak structure, with clear responsibilities, collectively forms a solid institutional guarantee for Hong Kong to develop into a global leading virtual asset center.

III. Core Analysis of VASP Licensing and Stablecoin Issuance Regulation

The core of Hong Kong's virtual asset regulatory framework consists of two pillars: the virtual asset service provider (VASP) licensing system and the stablecoin issuance regulation. This section will delve into the key points and regulatory logic of these two frameworks.

(1) VASP Licensing System: Defining the Red Line for Trading Platforms

Effective from June 1, 2023, the VASP licensing system is central to Hong Kong's regulation of virtual asset trading. This system requires that all centralized virtual asset trading platforms (VATP) operating in Hong Kong or conducting business with Hong Kong investors must be licensed, regardless of whether they trade security tokens. This initiative aims to bring all relevant platforms under a unified and strict regulatory system.

- Investor Protection: Informed, Aware of Risks, and Able to Bear

To protect retail investors, regulatory agencies have set multiple thresholds. Before opening accounts for retail clients, platforms must assess their knowledge level regarding virtual assets and provide adequate risk disclosures. When recommending trades, platforms must also ensure that the advice aligns with the client's personal circumstances. The underlying logic is clear: to ensure that investors are "informed, aware of risks, and able to bear" them before entering the market, thus avoiding unnecessary losses due to information asymmetry. Additionally, the SFC retains the authority to set investment limits on high-risk virtual assets, adding another layer of protection for retail investors' funds.

- Customer Asset Security and Financial Robustness

In light of the lessons learned from the collapse of platforms like FTX due to the misuse of customer funds, Hong Kong has established globally top-tier strict standards for customer asset security.

Asset "Hard Isolation": The core requirement is that platforms must entrust customers' virtual assets to independent third-party custodians (usually licensed trust companies in Hong Kong) and adhere to industry best practices of 98% cold storage and 2% hot storage, aiming to minimize the possibility of asset misappropriation by the platform. Customers' fiat currency must also be held in independent trust or designated accounts.

High Financial Thresholds: Platforms must not only have a paid-up capital of no less than HKD 5 million and liquid assets of HKD 3 million but must also reserve enough liquidity assets to cover at least 12 months of operating expenses. This ensures that platforms have the capacity to withstand market risks and continue operations, avoiding damage to investors' interests due to their own financial issues. Furthermore, platforms must purchase insurance for customer assets that is recognized by the SFC.

- Anti-Money Laundering/Counter-Terrorist Financing (AML/CFT)

The anonymity and cross-border characteristics of virtual assets make them susceptible to becoming a breeding ground for illegal activities. Therefore, the VASP licensing requirements mandate that platforms strictly implement AML/CFT measures such as "Know Your Customer" (KYC) and Customer Due Diligence (CDD). This includes continuous monitoring of transactions, reporting suspicious activities, and encouraging the use of blockchain analysis tools to enhance tracking capabilities. These regulations aim to improve transaction transparency, combat financial crime, and maintain Hong Kong's reputation as an international financial center and the integrity of its financial system.

- Token Listing and Trading Scope

To control risks from the source, platforms must establish independent token review committees. This committee is responsible for conducting rigorous due diligence on all tokens planned for listing, assessing their legality, security, team background, and technical foundation. Regulations clearly state that only non-security tokens that are included in mainstream indices and have high liquidity can be opened to retail investors. This prudent screening mechanism aims to protect investors (especially retail investors) from inferior or fraudulent projects, ensuring market fairness and transparency.

- Prohibited Business Activities

To ensure the neutrality of platforms, VATPs are prohibited from engaging in proprietary trading for their own accounts, with the core aim of preventing conflicts of interest between the platform and its clients. Additionally, current guidelines still prohibit platforms from issuing or trading virtual asset futures and related derivatives. This reflects the regulatory agencies' cautious attitude towards complex high-risk products, prioritizing market stability. The SFC has stated that it will review the situation in the future and consider the possibility of opening such products to institutional investors.

(2) Stablecoin Regulatory Framework: Establishing Rules for "Quasi-Currency"

Stablecoin regulation is a key step for Hong Kong in building a global virtual asset center, led by the Hong Kong Monetary Authority (HKMA). The relevant bill was passed on May 21, 2025, and will officially take effect on August 1 of the same year.

- Focusing on Fiat-Collateralized Stablecoins

The core goal of the regulatory framework is to focus on "designated stablecoins" that are pegged to one or more fiat currencies, as these assets have payment potential, and their stability directly relates to financial security. Based on the lessons learned from the collapse of Terra/LUNA, algorithmic stablecoins lacking backing by physical assets are explicitly excluded from regulation. Notably, this regulation has extraterritorial effect: regardless of where the issuer is located, as long as the issued Hong Kong dollar stablecoin reaches Hong Kong users, it must comply with Hong Kong's licensing regulations.

- Ensuring the "Stability" is Genuine

To issue stablecoins in Hong Kong, issuers must obtain a license from the HKMA. The core requirements revolve around "stability" and "trustworthiness":

1:1 Full Reserve: Must provide 100% reserve support with high-quality liquid assets.

Transparency and Trust: Reserves must undergo regular third-party audits and be disclosed to the public.

Robust Operations: Must establish reliable redemption mechanisms, strict AML/CFT measures, and plans to ensure network security and business continuity.

These high thresholds aim to ensure that stablecoins can be redeemed at any time, preventing "de-pegging" risks and thereby building market confidence.

- Cautious Start, Encouraging Innovation

The HKMA will adopt a very cautious attitude in the initial phase of licensing, expecting to issue only a small number of licenses and requiring applicants to demonstrate that their stablecoins have clear and genuine use cases.

Hong Kong has established a "sandbox" mechanism allowing interested institutions to test their business models and risk control capabilities in a controlled environment. This "cautious licensing + sandbox trial" strategy aims to ensure that the first batch of licensed institutions serves as benchmarks while providing valuable practical experience for regulation and the market, ultimately promoting the compliant application of stablecoins in payments, cross-border remittances, and other areas, consolidating Hong Kong's position in financial innovation. In the next chapter, we will continue to analyze how this mechanism operates.

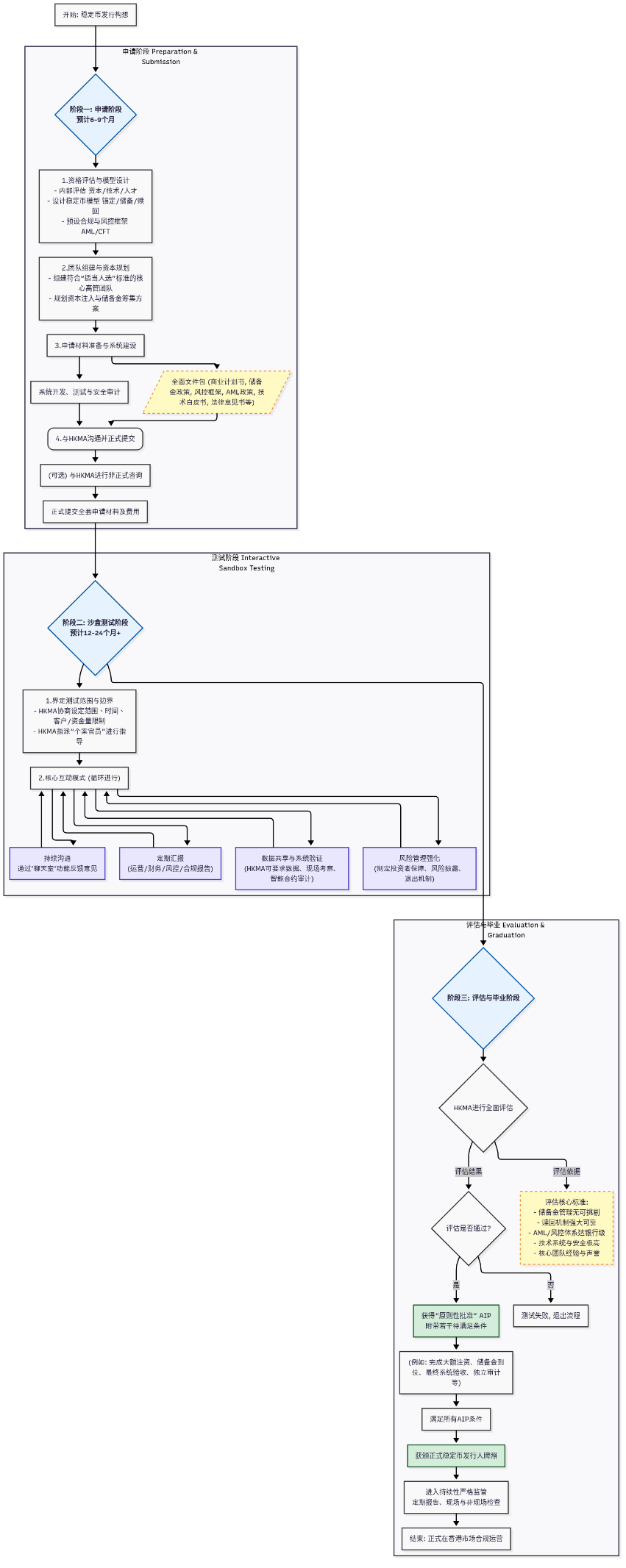

IV. A Comprehensive View of the Regulatory Sandbox Process from the Applicant's Perspective

Hong Kong's core strategy in the field of virtual asset regulation is its carefully designed "regulatory sandbox" mechanism, which is not only a regulatory tool but also a strategic platform for promoting the development of the fintech ecosystem, aiming to seek a balance between embracing fintech innovation and maintaining financial stability and protecting investors. Hong Kong's "regulatory sandbox" is essentially a "dialogue mechanism between regulation and innovation" and a "testing ground for risk isolation."

This process is not a simple licensing application but a long, rigorous, and deeply interactive "co-evolution" journey. It places high demands on applicants' capital, technology, compliance capabilities, and risk management levels.

To visualize this complex, multi-stage approval process, I have constructed the following "Regulatory Sandbox Comprehensive Process Map." This chart, based on a timeline, details every key step, interaction mode, and deliverable from the initial concept to the final licensing, aiming to provide potential applicants with a clear roadmap for action.

From the above chart, it can be seen that the design of the entire process reflects the rigor, interactivity, and transparency of Hong Kong's regulatory agencies.

Preparation is Key (Application Stage): The focus of this stage is on internal "fine-tuning." The HKMA expects applicants to have completed highly mature business model designs, technical system constructions, and compliance framework setups before formally submitting their applications. This effectively front-loads most of the preparatory work, ensuring that only well-prepared, high-quality participants enter the sandbox.

Deep Interaction (Testing Stage): The sandbox is far from a passive observation period; it is a "laboratory" where regulation and innovation collide deeply and evolve together. By appointing "case officers," establishing "chatroom" mechanisms, and requiring continuous data sharing and reporting, the HKMA gains deep insights into the actual operational risks of innovative businesses, while companies can timely adjust and optimize their plans under regulatory guidance, reducing the risk of non-compliance.

High Standards for Graduation (Evaluation Stage): The "graduation" threshold is extremely high, with evaluation criteria targeting the core of financial stability—reserves, redemption mechanisms, risk control systems, and technical security. The design from "Principle Approval (AIP)" to "Formal License" sets the final insurance for market entry, ensuring that all promised capital and systems are fully in place.

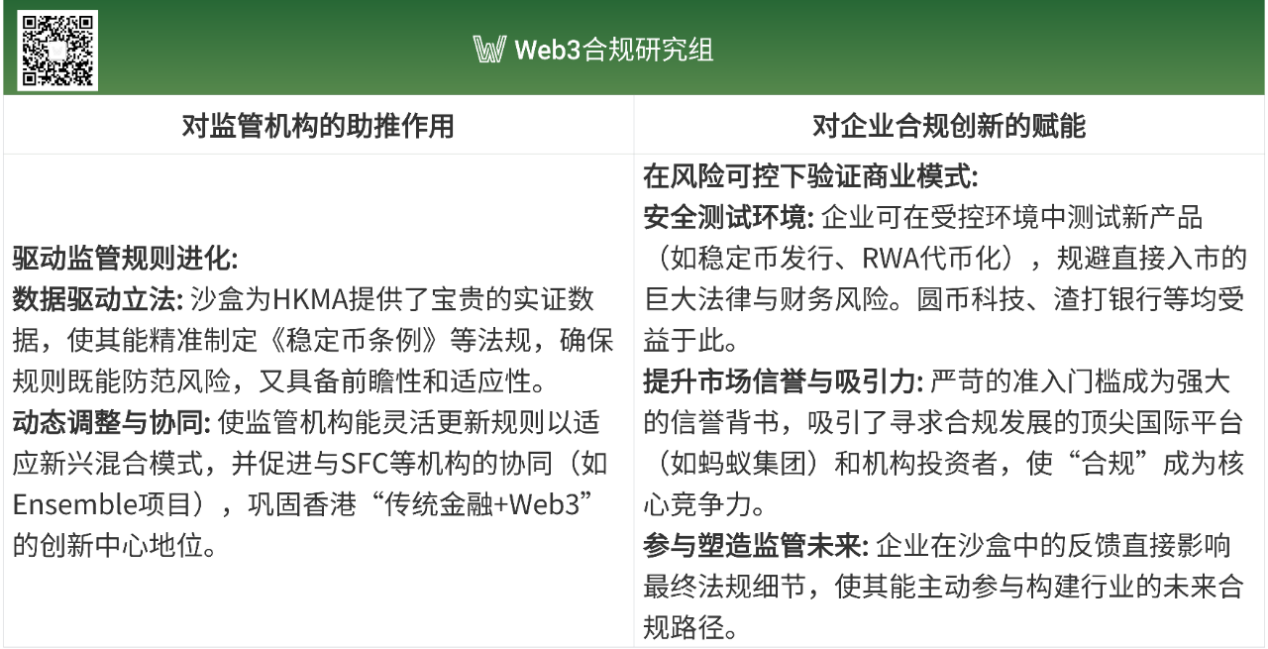

This rigorous process is not merely a regulatory hurdle; it constructs an ecosystem of mutual benefit between regulatory agencies and innovative enterprises. The actual effects produced are bidirectional, specifically reflected in the following two aspects:

In summary, Hong Kong's regulatory sandbox mechanism, particularly the pathway design for stablecoin issuers, is the most strategically visionary component of its digital asset regulatory framework. It transcends the traditional one-dimensional model of approval, creatively integrating the seemingly opposing concepts of "strict regulation" and "cutting-edge innovation."

Through this carefully designed process, Hong Kong not only sets globally leading compliance standards for the market but also establishes a dynamic, self-optimizing regulatory and industry interaction ecosystem. This not only safeguards its own financial stability but also announces to the world: Hong Kong has the capability and wisdom to navigate the future of digital finance and is committed to becoming the safest, most regulated, and most vibrant hub in the global virtual asset field. This "bidirectional empowerment" sandbox is the cornerstone of Hong Kong's construction of its global digital financial leadership. In the fifth part of the article, we will delve into the sandbox to analyze this dynamic interaction process.

V. Regulatory Sandbox—Typical Cases on the Path to Compliance

This chapter reveals the core considerations from a regulatory perspective by analyzing practical cases from Hong Kong's digital asset regulatory sandbox, attempting to grasp the "development pulse" of Hong Kong in embracing the Web3 innovation process.

(1) Stablecoin Regulatory Sandbox: Pragmatic First, Addressing Pain Points

In July 2023, the HKMA conducted consultations on legislative proposals for implementing a regulatory system for stablecoin issuers and announced the launch of a sandbox arrangement. In July 2024, the HKMA published the list of the first batch of participants entering the sandbox, including JD Coin Chain Technology (Hong Kong), Yuan Coin Technology, and a consortium formed by Standard Chartered Bank (Hong Kong), Ant Group, and Hong Kong Telecom. The first three all plan to issue stablecoins pegged to the Hong Kong dollar.

JD Coin Chain Technology (Hong Kong): According to JD Coin Chain CEO Liu Peng, its stablecoin project (JD-HKD) mainly focuses on cross-border payments, investment trading, and retail payments as three practical use cases. It aims to expand cross-border payment scenario users through direct customer acquisition and indirect customer acquisition (such as collaborating with compliant wholesalers), and to collaborate with global compliant exchanges to expand investment trading clients. In retail payments, it will first be implemented on JD Global Purchase's Hong Kong and Macau site, allowing users to use stablecoins to pay bills in JD's e-commerce business in the Hong Kong and Macau regions. In terms of specific strategies, JD will tailor stablecoin payment solutions for different industries while integrating data from overseas small and medium-sized enterprise orders and warehouses into the blockchain to improve payment and financing efficiency. Reports indicate that JD's JD Coin Chain has registered "JCOIN" and "JOYCOIN," and the market generally believes these two names will be used for its stablecoin.

Yuan Coin Technology: Founded by former HKMA president Norman Chan, Yuan Coin Technology is set to launch the HKD stablecoin HKDR, primarily targeting three major business scenarios: cross-border trade, virtual asset trading, and RWA. Leveraging its parent company's obtained Stored Value Facility (SVF) license, as well as the foundational and channel advantages accumulated by shareholders and partners such as HashKey Exchange, Cobo digital asset custodian, and LianLian Pay in the fields of web3, custody, payment, and trading, Yuan Coin Technology is expected to establish a full-chain web3 ecosystem payment, achieving a seamless connection between web2 and web3.

Standard Chartered Bank, Ant Group, and Hong Kong Telecom Consortium: Ant Group, as a practitioner in the native web3 field, is responsible for developing native web3 application scenarios. Standard Chartered Bank, as the issuer of Hong Kong dollars, drives bank customer resources, while Hong Kong Telecom has the electronic payment program Tap&Go, focusing on retail customer outreach. The three parties jointly apply to maximize the promotion, large-scale circulation, and application of stablecoins, achieving full coverage of traditional bank customers, traditional payment customers, and web3 users. Application scenarios include virtual asset trading in web3 games, cross-border trade, and financial settlement in traditional finance.

It is noteworthy that on July 23, HKMA President Eddie Yue reiterated that dozens of institutions interested in applying for stablecoin licenses have contacted them, many of which lack actual application scenarios, feasible specific plans, and implementation strategies, let alone awareness and capability for risk control. Some institutions that can provide application scenarios lack the technology and experience to issue stablecoins and manage financial risks. It is suggested that they do not need to become issuers but rather collaborate with issuers to provide application scenarios. Overall, the HKMA will only approve a few stablecoin licenses, which may disappoint many applicants.

In my opinion, from the current stablecoin issuers entering the sandbox, the HKMA's considerations for stablecoin issuers include the following three points: First, focus on whether the issuer has real application scenarios, especially in the fields of cross-border trade, e-commerce, and finance, and whether they can leverage the technological advantages of stablecoins to improve payment efficiency and other financial conveniences in transactions. Second, whether they have financial risk management awareness and capability, ensuring the establishment of appropriate investor protection measures. Third, control the overall number of licenses to avoid financial risks and waste of competitive resources due to the lack of the necessary prerequisites of the first two points.

(2) Ensemble Sandbox: Innovating Financial Market Infrastructure to Promote Tokenization Applications

In March 2024, the HKMA announced the launch of the Ensemble project to promote interbank tokenized deposit settlement using wholesale Central Bank Digital Currency (wCBDC) and facilitate tokenized asset trading using tokenized currencies. In May of the same year, a working group for the Ensemble project was established to collaboratively develop standards and proposals with the industry to promote interoperability between wCBDC, tokenized currencies, and tokenized assets. In August, the HKMA announced the first phase progress of the Ensemble project and introduced four major tokenization use cases, including fixed income and investment funds, liquidity management, green and sustainable finance, and trade and supply chain financing.

HKMA CEO Julia Leung stated, “The Ensemble project is a key infrastructure construction project that will drive the scaling of the tokenized ecosystem in the new stage of development and is at the core of Hong Kong's innovative financial infrastructure.” Tokenizing central bank currency and bank deposits at the wholesale level will inject strong momentum into the overall tokenization project. Tokenized currencies and deposits are prerequisites for fully unleashing tokenization potential.

Over the past year, the Ensemble project has announced numerous use cases, and this chapter will focus on key examples.

- Green and Sustainable Finance

Ant Group is an important participant in the fields of green and sustainable finance, trade, and supply chain finance, having implemented multiple use cases. In addition to the three use cases in collaboration with Ant Group, the "Chong Meihao" electric vehicle charging station tokenization case by China Resources Longyuan was also selected for the Hong Kong Ensemble project, with a business model similar to that of Longxin Technology. This section will elaborate on the three use cases in collaboration with Ant Group.

- Charging Pile Industry RWA (in collaboration with Longxin Technology): Longxin Technology is a leading energy technology company in China, having developed multiple energy digital products and new energy internet platforms. For example, a life payment platform in collaboration with Alipay and other portals, providing online services for over 450 million meter users for utilities such as water, electricity, and heating; the Xinyang Photovoltaic Cloud Platform, which connects various power stations through distributed photovoltaic platform operations, aggregating green electricity transactions; its new energy aggregation charging platform—Xindian Road, which constructs an AI smart hub for charging, linking new energy vehicle demand with over 2 million charging devices. Thus, Longxin is not a traditional new energy enterprise transformed by digital technology but a digital technology solution provider with a core competitive advantage in the industry, focusing on technology and services for business information systems in the utility sector.

The first charging pile industry RWA has a financing amount of 100 million RMB. Longxin Group will use part of the charging piles operated on the Xindian Road platform as supporting assets, issuing "charging pile" digital assets on the blockchain based on credible data, with each digital asset representing a portion of the revenue rights corresponding to the charging pile. The Ant Chain inside product module provides data on-chain technology support. Local and small charging stations connected to Xindian Road face similar financing challenges as small and medium-sized enterprises, such as low credit ratings and difficulties in bank financing, but they also have advantages in familiar local resources, market expansion, and flexible operating models. By uploading operational data of the equipment to the blockchain, this project is expected to provide construction and operational support for thousands of small and medium-sized energy companies, such as energy storage and charging operators, to revitalize quality existing assets.

Photovoltaic Industry RWA (in collaboration with GCL-Poly Energy): Ant Group further partnered with GCL-Poly Energy to successfully complete RWA based on photovoltaic physical assets, involving amounts exceeding 200 million RMB. GCL-Poly Energy's "Xinyangguang" brand, based on household photovoltaic business, conducts an integrated business system including product R&D, market sales, engineering construction, and operational maintenance for household photovoltaic systems. GCL-Poly Energy will use approximately 82MW of "Xinyangguang" household photovoltaic systems located in Hubei and Hunan provinces as RWA supporting assets, packaging and storing the value, operation, revenue, and other data of the household photovoltaic projects on the blockchain through the combination of blockchain technology and IoT technology, forming digital tokens.

Two-Wheeled Battery Swap Business RWA (in collaboration with Xunying Group): Approximately 4,000 battery swap cabinets and 16,000 lithium batteries operated by Anhui Xunying New Energy Group will be designated assets, issued to the private placement market, raising 20 million RMB. By combining IoT and blockchain technology, the value, operation, revenue, and other data of the battery swap project are stored on the blockchain, forming digital tokens to revitalize existing assets, accelerate capital recovery, and enhance the liquidity and tradability of battery swap assets.

From the three new energy RWA cases in collaboration with Ant Group, some commonalities can be observed:

First, compared to operational assets like agricultural products, real estate, and restaurant operations that require human intervention, the assets in the new energy charging and swapping industry have the inherent advantage of being connected to power sources and networks, allowing them to operate autonomously and upload data without personnel intervention, eliminating scenarios where "hiring a cleaner for 100,000 a month to wipe the equipment" as operational costs could harm investors' rights.

Second, compared to direct financing where large companies serve as financing entities and indirect financing where they serve as credit entities, RWA financing provides a new solution for financing small and medium-sized enterprises (or a collective of small and medium-sized enterprises or operators) in project form (the aforementioned cases involve large-scale (millions) revenue rights of small and medium-sized new energy operational terminal devices), supporting the development of the domestic new energy industry with overseas funds.

Third, Ant Group provides multiple technologies to safeguard investor rights. For example, IoT technology ensures real-time connection of assets, instant tracking of equipment operation dynamics, AI enhances operational efficiency, and asset data is uploaded to the blockchain, ensuring data authenticity and reliability, ultimately synchronizing detailed data such as the charging device ID, charging device status, charging amount, charging fees, and charging time with multiple parties, making asset and revenue situations transparent and visible.

Based on the above cases, new ideas and inspirations are provided for potential underlying assets of future RWA products. Existing assets with four major characteristics—networked management, local operation, connection to power sources and networks, and direct revenue generation—have significant potential to become RWA-supported assets. For example, locally shared rental equipment (self-service rental children's cars and scooters in shopping malls), smart unmanned retail machines, revenue rights from rental equipment in the industrial sector, smart parking revenue rights, and edge computing node computing power service rental revenue rights, etc.

- Trade and Supply Chain Financing

International trade involves numerous documents, with a single transoceanic shipment potentially requiring 50 pages of documents and 30 related parties. The bill of lading, as an important property right certificate, carries the function of ensuring the delivery of goods to the final recipient named on the bill. However, currently, bills of lading still primarily circulate through traditional paper methods, with the usage rate of electronic bills of lading (eBL) below 4% in 2024. In 2018, COSCO Shipping initiated the establishment of a global shipping business network platform (GBSN), and in 2021, GBSN was registered in Hong Kong, launching the first "paperless release" product in July of the same year. In June 2022, the first blockchain electronic bill of lading based on the GSBN platform—IQAX eBL—was approved by the International Group of P&I Clubs.

Electronic Bill of Lading (eBL): Ant Group assisted the HKMA in building a tokenized asset platform within the sandbox to facilitate Delivery versus Payment (DvP) transactions between traditional assets and tokenized deposits, allowing electronic bills of lading (eBL) issued by the Global Shipping Business Network (GSBN) to be traded in tokenized form on the platform. HSBC, Hang Seng Bank, and Bank of China (Hong Kong) have facilitated the use of tokenized deposits to settle the transfer of electronic bills of lading. This solution significantly enhances the efficiency of trade processes, improves the security of data and transactions, and opens new avenues for addressing trade financing gaps.

- Fixed Income and Investment Funds

Fixed income and investment funds focus on the tokenization of bonds and funds. In the bond market, Hong Kong has explored the tokenization of green bonds through EvergreenHub:

In February 2023, the Hong Kong SAR government announced the successful issuance of 800 million HKD in tokenized green bonds under the green bond program, making it one of the first tokenized green bonds issued by a government globally. The primary issuance of this bond used a private blockchain network, settling securities tokens representing the actual rights of the bonds and cash tokens representing the HKMA's HKD-denominated bonds through a T+1 DvP method. The settlement was provided by the HKMA's Central Moneymarkets Unit (CMU), with Goldman Sachs' tokenization platform GS DAPTM responsible for the delivery. Subsequent bond processes (including coupon payments, secondary market trading settlements, and redemption at maturity) will also be conducted digitally on the private blockchain network.

In February 2024, the Hong Kong SAR government announced again the successful issuance of digital green bonds valued at approximately 6 billion HKD, denominated in HKD, RMB, USD, and EUR, under the Hong Kong government's green bond program. The settlement and delivery system used for this batch of digital green bonds is the CMU and HSBC Orion digital asset platform, making it one of the first multi-currency digital bonds globally.

The settlement process for traditional bond issuance or fund trading generally takes 2-5 working days, while tokenized bonds and funds support 24/7 timely payments and settlements, significantly reducing the required time, simplifying the trading process, eliminating settlement delays, and lowering associated risks.

In August 2024, at the launch ceremony of the Ensemble sandbox, HKMA Vice President Li Dazhi stated that the bond issuance being validated in the sandbox aims to verify the end-to-end trading process, which is technically different from previous tokenized bonds. The development of tokenized finance is not achieved overnight and requires validation across different technical aspects. It can be inferred that the initial issuance tests focus on the issuance and settlement phases on the blockchain network and digital asset platform, while later stages will validate the circulation of bonds among a broader range of different entities, thereby verifying the technology for 24/7 trading of tokenized green bonds.

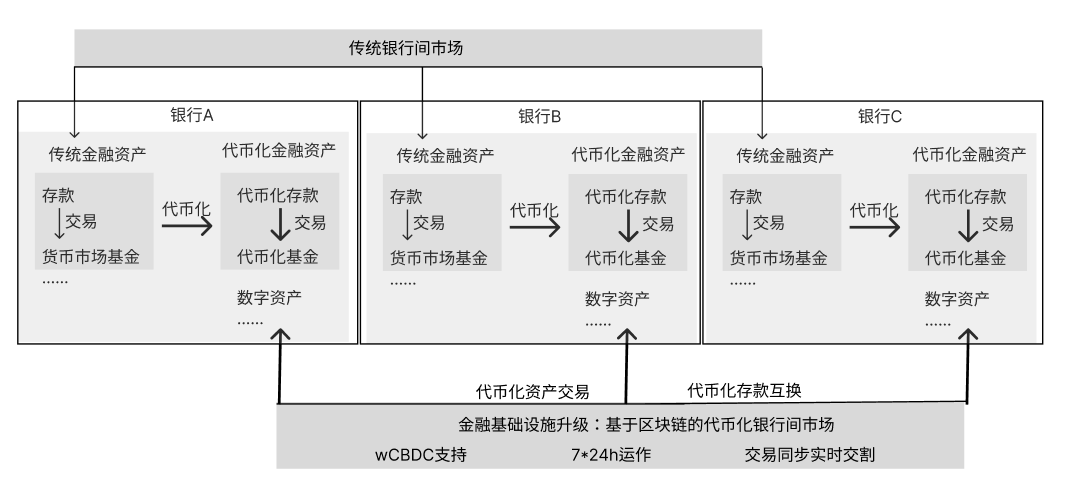

Regarding money market funds, HSBC and Bank of China (Hong Kong) are among the first participants in this theme. According to disclosures from both banks, the feasibility of tokenizing deposits and financial assets, trading between tokenized deposits and tokenized assets, and transferring tokenized deposits to different financial institutions' blockchains has been achieved.

This use case effectively illustrates how Ensemble facilitates the tokenization conversion and trading of traditional financial assets between banks, aligning with the goal of building new financial market infrastructure. The diagram below shows the specific process, where the thick arrows indicate the new technologies and trading channels tested in the sandbox.

Figure: Ensemble sandbox supports the tokenization of financial assets and the construction of new infrastructure

- Liquidity Management

Liquidity management focuses on repurchase agreements and treasury management use cases, promoting banks to build corporate treasury management solutions based on tokenized deposits for clients. In May 2025, HSBC's tokenized deposit infrastructure was put into use, launching Hong Kong's first blockchain settlement service provided by a bank. Ant International is the first corporate client to adopt this solution, with its subsidiary's deposits in HSBC accounts being tokenized. Through its internal fund management platform Whale, it issued instructions for tokenized deposit transfer transactions to HSBC, successfully completing instant internal fund allocation. By leveraging the programmable and instant settlement characteristics of tokenized deposits, the tokenized fund management solution is expected to enhance more transparent, efficient, and convenient corporate payment and fund management solutions.

VI. Future Outlook

The digital asset regulatory framework established in Hong Kong, along with its pioneering sandbox use case practices, clearly presents a specific path for innovation to achieve robust development within a compliant framework. As stated in the "Hong Kong Digital Asset Development Policy Declaration 2.0," Hong Kong is continuously building a "trustworthy and innovation-focused digital asset ecosystem" and will continue to strengthen its leading position in the global digital asset field, promoting Hong Kong as a global innovation center.

With the official implementation of the "Stablecoin Ordinance" on August 1, it also provides a more solid institutional foundation and broad development space for Hong Kong to promote stablecoin application scenarios, expand the variety of tokenized products, and enhance the liquidity and popularity of stablecoins and tokenized financial products.

Looking ahead, leveraging the deep foundation of a traditional international financial center, the first-mover advantage of a systematic regulatory framework in the digital asset field, and its natural hub position connecting the mainland and global digital asset markets, Hong Kong is expected to rise as a key node in the global digital asset landscape and a core hub for the tokenization of real-world assets, building an irreplicable unique competitive advantage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。