作者:MONK

编译:深潮TechFlow

交易代码是 $ETH。

华尔街正在经历一场加密货币的高光时刻。

传统金融(TradFi)正在耗尽增长叙事的资源。人工智能已经成为市场的热点,但大家对它的关注已经过度,而软件公司如今远没有2000年代和2010年代那么吸引人了。

深层次来看,那些为投资创新故事和大规模可服务市场(TAM)筹集资本的增长投资者们心知肚明,大多数人工智能相关公司的估值都处于荒谬的溢价水平,而其他所谓的“增长型”叙事已经不再容易找到。曾经备受推崇的FAANG股票也在逐渐转型为“品质优良、利润最大化、年增长率中等”的复合型资产。

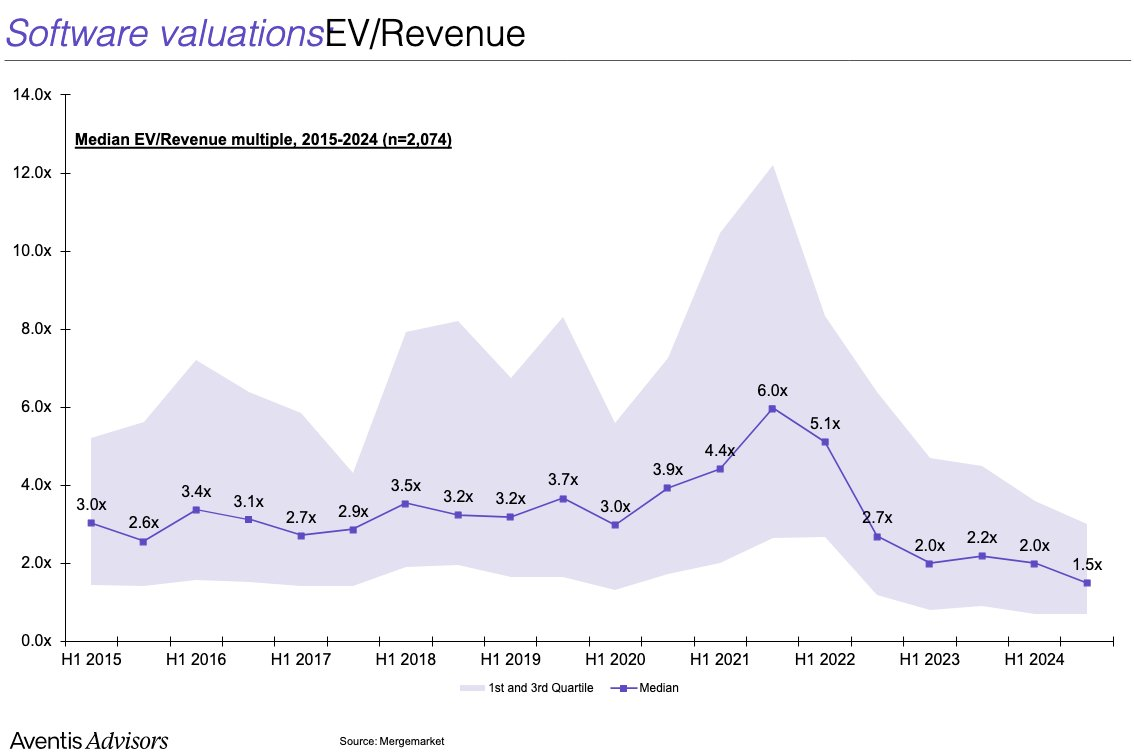

举个例子,软件公司的企业价值与收入(EV/Rev)倍数中位数已经下降到2.0倍以下。

这个时候,加密货币登场了。

比特币($BTC)突破历史高点,美国总统在新闻发布会上大力宣传我们的资产,还有一波监管利好风潮将加密货币资产类别自2021年以来首次推回聚光灯下。

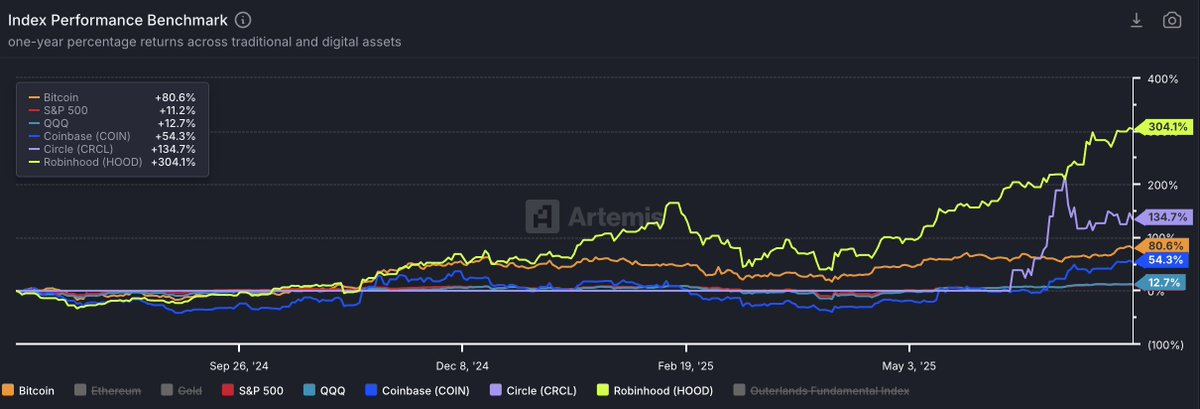

BTC、COIN、HOOD、CIRCLE vs. SPY 和 QQQ(来源:Artemis)

这一次,主角不再是NFT和狗狗币。这一次,是数字黄金、稳定币、“代币化”和支付改革的时代。Stripe和Robinhood正在声称加密货币将成为它们下一轮增长的核心重点;$COIN(Coinbase)成功加入标普500指数;Circle向世界展示,加密货币足够具备吸引力,让成长型股票可以再次忽略收益倍数。

但这一切如何与 $ETH 相关联呢?

对于我们这些加密原住民来说,智能合约平台的领域看起来非常分散。有Solana,有Hyperliquid,还有十几个新兴的高性能区块链和Rollups(链上扩容解决方案)。

我们知道以太坊的领先地位已经真正受到挑战,它正面临存在性的威胁。我们也知道它尚未解决价值捕获的问题。

但我非常怀疑华尔街是否了解这些。事实上,我甚至可以大胆地说,大多数华尔街的投资者对Solana几乎一无所知。如果我们诚实一点,XRP、Litecoin、Chainlink、Cardano和Dogecoin可能比$SOL在外部市场的认知度更高。毕竟,这些人已经对整个加密资产类别冷漠了好几年。

华尔街知道的是,$ETH 是“林迪效应”(指长期存在的事物更可能继续存在)的代表,它经过了实战检验,并且多年来一直是 $BTC 的主要“beta 投资选择”。华尔街看到的是,$ETH 是唯一另一种拥有流动性ETF的加密资产。华尔街热衷的是即将到来的催化剂与经典的相对价值投资。

那些穿西装的投资者或许对加密货币了解不多,但他们知道 Coinbase、Kraken 以及现在的 Robinhood 都决定“基于以太坊进行构建”。通过最少的尽职调查,他们可以发现以太坊链上拥有最大的稳定币池。他们会开始计算“登月数学”,很快意识到,虽然 $BTC 已经达到历史新高,但 $ETH 仍比2021年的高点低了30%以上。

你可能认为相对表现不佳看起来很悲观,但这些人有不同的投资方式。他们更愿意买入价格较低但目标明确的资产,而不是追高那些让他们质疑自己是否“已经错过机会”的资产。

我认为他们已经来了。投资授权不是问题,任何基金都可以通过适当的激励推动加密货币敞口。尽管加密推特(CT)已经宣称一年多不会再碰 $ETH,但该交易代码过去一个月表现持续优异。

截至今年,$SOLETH 下跌了近9%。以太坊的市场主导地位在5月份触底,此后创下自2023年中以来最长的上涨趋势。

如果整个加密推特(CT)都将 $ETH 标记为“被诅咒的币种”,那它为何还能表现优异?

答案是:它正在吸引新的买家。

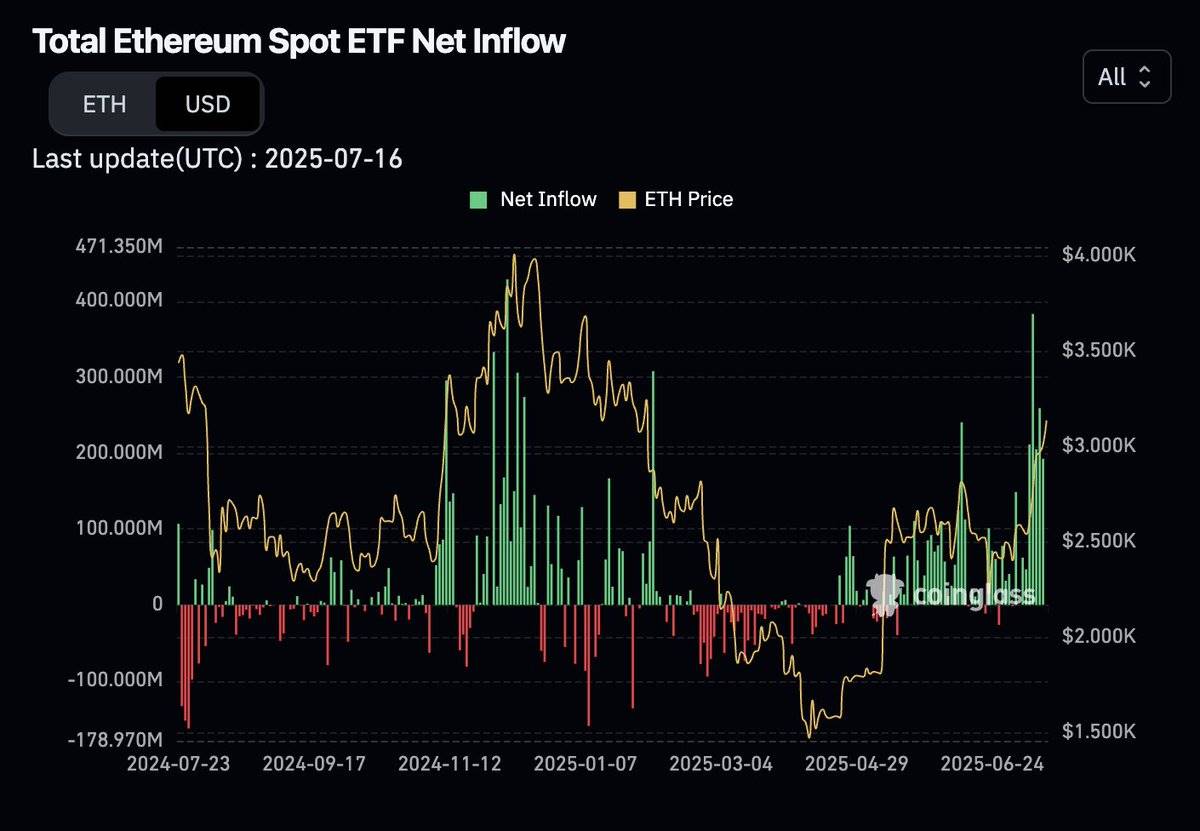

自今年3月以来,现货ETF资金流入一直呈现单向增长趋势。

来源:Coinglass

类似于 $ETH 的微策略克隆基金(Microstrategy Clones)正在大举加仓,为市场加入了早期的结构性杠杆。

或许,一些加密货币原住民意识到自己对 $ETH 的敞口不足,开始重新调整仓位,可能从过去两年间表现突出的 $BTC 和 $SOL 中退出,转而布局以太坊。

我并不是说以太坊已经解决了它存在的问题。我认为现阶段可能发生的事情是,$ETH 作为资产开始与以太坊网络本身脱钩。

外部买家正在推动 $ETH 资产的范式转变,挑战我们对它“只会下跌”的固有认知。空头最终会被迫平仓。而后,加密货币原住资本将开始追逐涨势,直到市场对 $ETH 的某种全面投机狂热出现,并以一次壮观的顶部结束。

如果这一切真的发生,那么历史新高(ATH)也不会太遥远。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。