Author: @agintender, @Johnnynkc, @alexzuo4_

Compiled by: Wu Says Blockchain

This article is for general informational reference only and does not constitute any form of legal opinion, investment advice, or other professional advice. Users should conduct independent reviews and confirmations with a qualified lawyer before taking any action based on this material.

1. Introduction

On June 30, 2025, the Monetary Authority of Singapore (MAS) officially implemented new regulations for Digital Token Service Providers (DTSP), marking the formal establishment of a regulatory framework for crypto assets that has been in development since it was proposed in 2022. The execution of these new regulations has caused some panic among community practitioners, as this move not only affects Web3 projects operating locally in Singapore but is also seen as a key event that could reshape the entire Asian crypto industry landscape. Many unlicensed institutions may be driven out of Singapore, while a few licensed institutions such as Coinbase, OKX, Matrixport, HashKey, and Amber will gain more benefits. Cities like Hong Kong, Dubai, Tokyo, Kuala Lumpur, and Bangkok are expected to accommodate these retreating individuals.

2. Policy Background: "Three-Year Preparation Period" Not Taken Seriously Enough

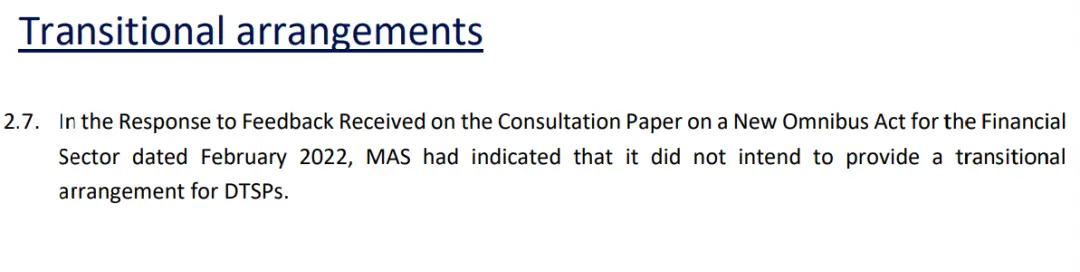

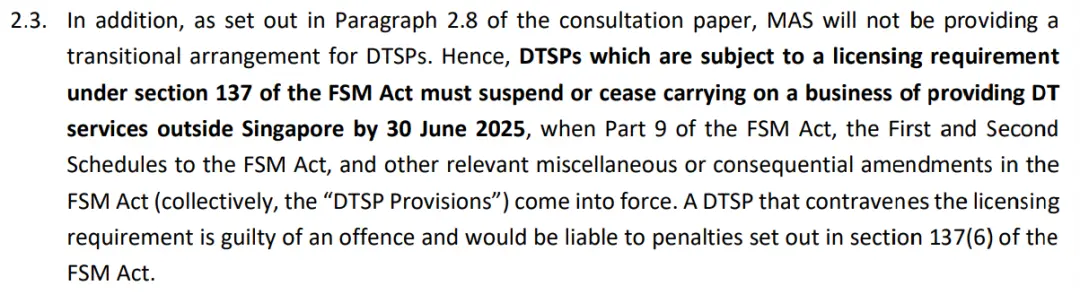

The regulatory changes in Singapore regarding the crypto industry did not happen overnight but were the result of several years of planning. Although the new regulations are widely viewed as "cliff-like regulation," in reality, MAS has been regulating digital payment tokens (DPT, i.e., cryptocurrencies) since 2020 through the Payment Services Act, requiring local businesses providing crypto exchange services to apply for licenses. Subsequently, MAS realized that there was still regulatory arbitrage: some crypto companies established bases in Singapore but only served overseas clients to evade local licensing requirements. To close this loophole and comply with the standards set by the Financial Action Task Force (FATF), Singapore passed the Financial Services and Markets Act (FSMA) in April 2022, which specifically introduced a licensing system for Digital Token Service Providers (DTSP) in Section 9. After the law was passed, MAS did not immediately enforce it strictly but allowed ample buffer time, planning to officially implement the new regulations in 2025. MAS had clearly stated in its guidelines that no transition period would be provided.

In other words, from the formulation of the law to its effective date, Singapore has given the industry nearly three years to adjust. Therefore, the recent announcement of new regulations by MAS is not a "cliff-like" sudden attack but rather a regulatory path set years ago. However, when MAS reiterated the hard deadline of June 30 with no buffer period in its final regulatory response document released on May 30, 2025, it still shocked the Asian crypto community. Some practitioners had hoped for leniency in regulation, but it has been proven that MAS's enforcement attitude is very resolute, viewing the past few years as a window for practitioners to adjust themselves. Overall, the DTSP licensing system in Singapore has been long in the making, with public consultations (such as the consultation report in late 2024) leading to its establishment, rather than a sudden "one-size-fits-all" shift. The formal bill was released in 2022, and after multiple rounds of feedback, it was finally confirmed for implementation in 2025.

However, due to the insufficient attention of the Chinese community to policy dynamics, most practitioners only felt regulatory pressure on the eve of implementation, leading to panic interpretations and discussions of a "Web3 mass exodus."

3. Interpretation of Core Provisions

1. Definition of DTSP

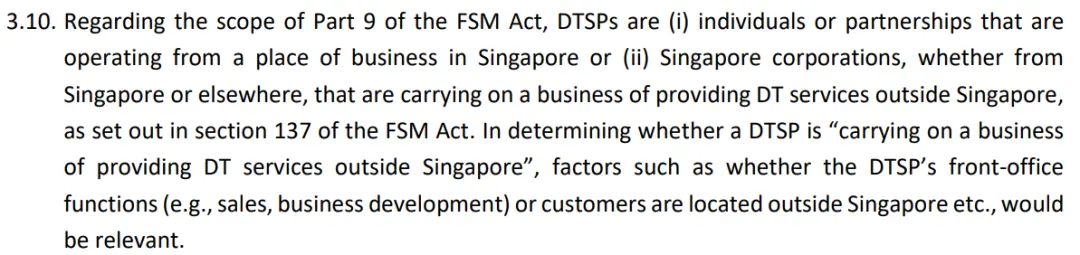

DTSP stands for Digital Token Service Provider. According to the definition in Section 137 of the FSM Act and the content of Document 3.10, DTSP includes two types of entities:

1) Individuals or businesses operating with a "place of business" in Singapore;

2) Singapore-registered companies providing digital token services to clients outside of Singapore, regardless of whether their actual operations are in Singapore or overseas.

2. Scope of Application: "In or From Singapore"

According to the above definition, whether an individual or a business, as long as the entity is engaged in digital token-related business in Singapore, or a company registered in Singapore provides crypto services to overseas clients, it falls under the regulatory scope of DTSP. It is worth noting that the source of clients is no longer important: regardless of whether the service targets locals or overseas clients, as long as the operating entity has a connection to Singapore, it must be licensed; otherwise, it is operating illegally. For example:

· The core development/operation team is located in Singapore;

· Servers or hosting systems are based in Singapore;

· Marketing activities are explicitly aimed at Singaporean clients;

· Receiving funds or assets from Singaporean users;

Thus, any service provided in Singapore or to Singaporean users that falls within the scope of DTSP requires a license.

3. Broad Definition of "Place of Business"

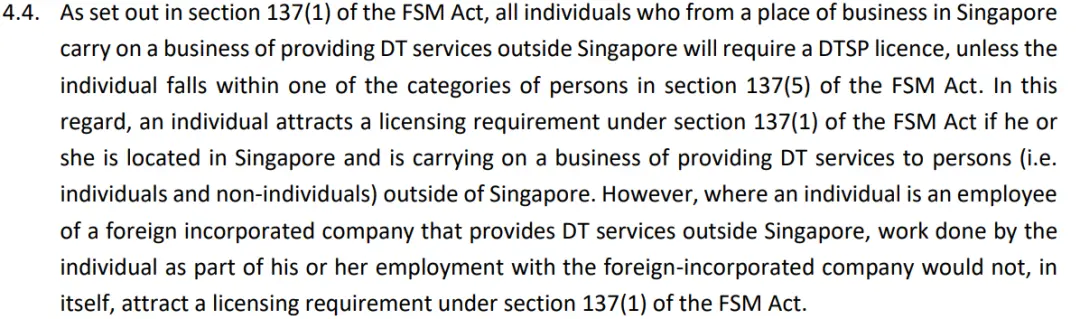

MAS has a very lenient definition of "place of business," almost equating it to any location where business is conducted. The official statement clarifies that a "place of business" can be any location used for conducting business, even including temporary or mobile locations like street stalls. As long as a person is within Singapore, whether in a company office, shared workspace, or on their own sofa at home, if they are engaged in digital token-related business (and without a license), they are considered to have a place of business in Singapore and are operating illegally. This interpretation dispels the delusions of some individuals—many practitioners previously believed that working remotely from home for overseas projects did not count as a "place of business," but MAS clearly does not accept this evasion. However, MAS does provide some flexibility: if the individual is a formal employee of an overseas company working remotely from home, then the responsibility primarily lies with the employer, and the company must be licensed, while the individual does not need to apply separately. The key to this provision lies in how "employee" status is defined: does the founder of a startup count as an employee? What about a consultant with equity? These gray areas are currently unclear and may require further clarification from MAS through FAQs or other means in the future. Regardless, the regulatory intent is clear—preventing behaviors that exploit the "being in Singapore, serving overseas" narrative, as even working from home cannot be an excuse to evade regulation.

4. Scope of Covered Digital Token Services

Simply put, anything related to "trading" is not allowed. Under the DTSP licensing regulation, the scope of "digital token services" is extremely broad, almost encompassing all aspects of crypto business. According to the FSMA annex, there are as many as ten categories of relevant activities, mainly including:

1) Token issuance or arranging the issuance of digital tokens (Issuance or Arranging Issuance)

Any involvement in creating or issuing digital tokens for others, including IDOs, Launchpads, Token Generation Events (TGEs), etc. Any service involving the provision or sale of digital tokens falls under regulation. This not only refers to projects directly issuing tokens to the public (similar to ICOs) but also includes inducing or prompting others to buy/sell tokens. In simple terms, whether as an issuer or intermediary, as long as one is promoting tokens or raising funds, a license is required.

2) Digital token custody services (Custody Services)

Holding or controlling clients' digital tokens, including cold wallet and hot wallet services. Whether providing custody vaults, custody wallets, or executing token-related instructions on behalf of clients (e.g., helping clients operate their token accounts, executing transactions), as long as the service provider has control over the tokens or their control tools, it falls under regulated activities. This means that providing clients with secure access to their assets through interfaces or systems is also subject to regulation.

3) Brokerage, matching, and trading arrangement services (Brokerage / Matching / Exchange Services)

Operating centralized or decentralized order books, trading matching services (including OTC, DEX Aggregator).

This covers platforms for buying, selling, and exchanging digital tokens, as well as brokerage services that facilitate token trading for others, such as providing trading platform interfaces (UI/UX) to assist buyers and sellers in completing transactions.

4) Transfer or payment services (Transfer Services)

Any service that assists clients in transferring tokens from one wallet or account to another (i.e., acting as an intermediary in transactions or cross-chain bridge transfers also requires licensing). This includes payment gateways, bridging protocols, and "client transfer" functions provided by wallets.

5) Validation and governance services (Validation / Governance Participation)

Participating in node validation on behalf of clients (e.g., staking in the client's name), running validator nodes, or participating in on-chain governance voting. This also involves activities related to receiving rewards or compensation from staking or governance.

6) Technology enabling custody services (Technology Enabling Custody)

Providing the infrastructure or technical support necessary for custody services (e.g., MPC wallet service providers, key custody, custody API developers). Although not directly controlling assets, technology that plays a key role in asset control is also included.

The above scope shows that the DTSP license almost covers all services in the digital token lifecycle, from issuance, trading, and transfer to custody and operation, all of which cannot evade regulation.

4. What Businesses Do Not Require a License?

- Pure technical consulting (Pure Advisory / Consultancy)

For example: project design, token economic model consulting, legal structure advice, product design guidance, etc. As long as you do not participate in the actual custody of assets, issuance, or execution of transactions, you will not be considered a DTSP.

- Marketing and publicity services (Marketing / Publicity Services)

Including community management, advertising, brand design, etc. Even if you help a Web3 project promote its market in Singapore, as long as you do not involve asset circulation, transaction matching, or token management, you generally will not be subject to regulation; however, if you directly arrange token sales/distributions or transfers on behalf of clients, it may trigger regulatory obligations.

5. Severity Analysis: Why MAS Has Shifted from Leniency to Strictness

Web3 is not outside the law; businesses involving transactions and fund flows are subject to regulation everywhere. The only difference is that Singapore's policies are somewhat more "forward-looking." The severity of the new regulations lies in their uncompromising enforcement and stringent entry standards. This is driven by both external events and reflects MAS's consistent regulatory philosophy:

- Singapore's "Everything Requires a License" Legal Culture

Singapore implements meticulous licensing management for any business activity: street vendors must complete regular training and obtain a vendor license; even coffee shops need to apply for a public performance license to play background music; if a hotel wants to operate a swimming pool, it must obtain additional permits. Singapore's "crypto-friendly" stance does not mean a lack of regulation for the industry—similarly, the crypto industry must also "obtain a license before operating and undergo regular reviews," essentially a "registration system" rather than a "laissez-faire" friendliness. In Singapore, everything requires regulation.

- Investor and Fund Security as a "National Policy" Foundation

The Singapore government acts as a parental figure, placing great emphasis on the welfare of its citizens, especially in fund management. For example, to prevent retirees from running out of money in their old age, the Singapore government even restricts the withdrawal of retirement savings (CPF) until the age of 55. At the same time, MAS emphasizes the protection of investor rights, highlighting AML/KYC, capital, and insurance requirements in crypto licensing to ensure accountability and compensation in case of incidents. It ensures that responsible parties can be identified promptly, and there are corresponding deposits and insurance.

- The "Fujian Gang" 3 Billion SGD Money Laundering Case Triggering Regulatory Red Lines

The tightening of regulations by MAS is primarily due to the need to prevent cross-border financial crimes and money laundering. Digital token services often operate across borders via the internet, characterized by strong anonymity and rapid fund flows, making them more susceptible to misuse by criminals for money laundering or financing terrorism. Singapore has experienced some lessons in recent years, the most significant being the "Fujian Gang" cross-border money laundering case exposed in 2023. This case involved ten foreign nationals from Fujian, China, who laundered money through companies and bank accounts established in Singapore, with the amount involved reaching 3 billion SGD, making it the largest money laundering case in Singapore's history. The severity of this incident even influenced public sentiment during the recent Singapore elections.

MAS is not afraid of fraudulent platforms damaging Singapore's reputation; the Singapore government has rich experience and means to respond to such incidents. Through Singapore's IAL list (https://mas.gov.sg/investor-alert-list), it is evident that what the Singapore government truly fears is the diplomatic crises caused by the inflow or outflow of illicit funds and its position as a financial reservoir in the Asia region.

- "Strict Entry and Management" of Licenses Originates from the "Disenchantment" of Review Practices

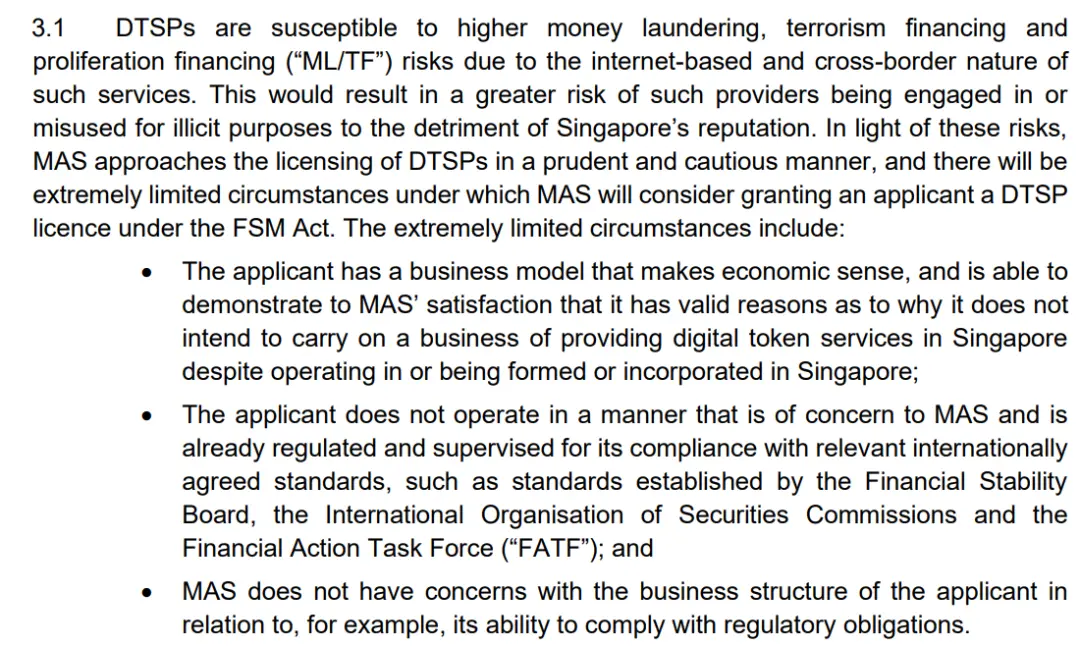

MAS's firmness is also reflected in its stringent entry standards. According to the guidelines, MAS states that it "will only consider issuing DTSP licenses in very rare cases" and has set forth nearly harsh approval conditions:

1) Applicants must demonstrate that their business model is economically viable and provide sufficient reasons for operating in Singapore without serving the local market (in other words, MAS must be convinced why they only conduct overseas business).

2) Applicants must assure MAS that their operational methods will not raise regulatory concerns and that they have obtained regulatory licenses or are subject to regulation in all foreign jurisdictions where they provide services, complying with international regulatory standards (such as those set by the Financial Stability Board, IOSCO, and FATF). This means that companies must be legally compliant in every country where their clients are located, which is nearly an impossible task for many startups.

3) MAS also emphasizes that the applicant's organizational structure and compliance capabilities must not cause regulatory unease, such as having sound corporate governance and sufficient manpower and financial resources to fulfill regulatory obligations.

As a result, after applications opened in 2021, over 500 institutions rushed to obtain licenses at peak times, but most had mediocre qualifications, with an approval rate of less than 10%. By the end of 2024, only 13 had obtained the main DPT license, and the total number of license holders increased from 16 to 29, coupled with MAS's tight regulatory staffing, leading to even stricter approvals.

- Web3 Has Not Brought "Depository" Economic Benefits to Singapore

The crypto industry has surged into Singapore; however, many projects have low registered capital, renting luxurious offices without paying local taxes. Funds do not remain in local banks but continuously consume and push up housing prices, salaries, and vehicle ownership costs, leading to a deterioration in social evaluation. Local voters are not convinced, and the government naturally has no intention of "working hard for little reward."

6. Industry Impact Assessment: Who Will Be Affected, Will Web3 Experience a "Mass Exodus"?

- Affected Groups:

Individual practitioners: such as independent developers, crypto project consultants, market makers, miners, KOLs (content creators), community operators, project founders, business development personnel, etc. In the past, these individuals did not need a license to work in Web3 in Singapore, but under the new regulations, everyone may have a sword hanging over their heads. For example, independent developers writing smart contracts for overseas blockchain projects, consultants providing token issuance solutions, and KOLs writing token analyses—all these activities theoretically fall under "providing digital token services."

Unlicensed institutions: such as crypto exchanges (whether centralized CEX or decentralized DEX) that have not yet obtained PSA licenses, DeFi project teams, NFT trading platforms, crypto wallet providers, cross-border payment networks, and various blockchain startups. These institutions, if they have personnel or company registrations in Singapore but no licenses, will face the risk of business interruption first. Especially for some startups that have previously established roots in Singapore and focused on overseas markets, if they do not meet the application conditions, it is equivalent to being sentenced to "death row," as they will not be able to continue operating in Singapore. According to the new regulations, they must cease related operations by June 30 at the latest; otherwise, they will be operating illegally.

- Exempt Groups:

Institutions that are already licensed or exempt under PSA/SFA/FAA do not need to apply for the DTSP license under FSMA but must fulfill the additional obligations of FSMA.

Typical examples:

Custodians: If already licensed/exempt under PSA, they are exempt from obtaining a DTSP license even when dealing with overseas clients. However, they must fulfill additional regulatory obligations under FSMA regarding technology, auditing, and AML/CFT.

FSMA Additional Compliance Checklist:

1) Technology Risk Management (TRM): Architecture, backups, penetration testing, and third-party services must comply with industry best practices.

2) Annual Independent Audit Report: Must cover both financial and system control dimensions and be submitted within the specified timeframe.

3) Higher AML/CFT Requirements: Stricter KYC, transaction monitoring, and suspicious reporting obligations.

4) Major Security Incidents Must Be Reported Within 1 Hour: Data breaches, loss of private keys, continuous downtime, etc., must be reported to MAS immediately.

5) Prohibition of High-Cash Transactions: Cash payments of SGD 20,000 or more are completely banned.

The formal implementation of the DTSP licensing system in Singapore marks the end of the era of regulatory arbitrage and the beginning of a new phase. Amid the global trend of tightening regulations, major jurisdictions are gradually filling the regulatory gaps for crypto activities, with Singapore being one of the more aggressive examples. The previously exploited model of "establishing in Singapore and providing services overseas" is now uniformly regulated, undoubtedly sending a clear signal to the industry: the future development of Web3 must be based on legality and compliance, attempting to consolidate the regulatory powers scattered under PSA/SFA/FAA, eliminating "gray areas," and shifting the regulatory focus from "whether licensed" to "whether compliant." Regulation of stablecoins is also being upgraded simultaneously.

1) Single Currency Stablecoins (SCS): Implementing an independent framework.

2) Other Stablecoins: Continue to be treated as DPT, still falling under PSA; if serving as underlying assets for derivatives, they may fall under SFA regulation.

The gray areas that exist outside of regulation will become increasingly scarce. Compliant operations will become the mainstream, and the era of exploiting differences in various jurisdictions is coming to an end. If from 2018 to 2021, Asian crypto entrepreneurs were keen on finding regulatory havens, after 2025, those that can stand firm will mostly be enterprises willing to embrace regulation and possessing compliance capabilities. Major financial centers in the region are also competing to launch clear regulatory frameworks; rather than saying companies are "fleeing" from certain places, it is more accurate to say they are seeking regulatory environments that best fit their business.

7. Two Self-Check Questions for Practitioners

1) Am I already licensed or exempt under the PSA/SFA system?

2) Am I providing any DT services to overseas clients?

If the answer to Question 1 is "Yes," no new license is needed, but compliance upgrades should be initiated immediately.

If the answer to Question 1 is "No," then a license must be obtained or operations must cease by June 30.

MAS's regulatory screws will only tighten—do not wait until the last day to act. Licensed institutions should view "compliance upgrades" as a normalized process; unlicensed teams lacking a full set of compliance resources should decide as soon as possible whether to apply, merge, or withdraw. This strong measure of not providing a transition period and requiring violators to cease operations immediately is also sending a signal to the market: Singapore will not be a safe haven for uncontrolled crypto businesses. Even if it was seen as "crypto-friendly" in the past few years, it will no longer allow loopholes. MAS's actions indicate that Singapore's crypto regulatory environment has tightened significantly, and many local companies will either incur high costs to obtain licenses or will have to restructure their businesses and exit overseas markets. The government would rather bear the short-term cost of losing some businesses than allow Singapore's international reputation and financial security to be eroded.

8. Indirect Benefits to Surrounding Regions

Singapore's actions may indirectly benefit other regions, prompting a new division and migration of the Asian crypto landscape. As another crypto hub in Asia, Hong Kong has been vigorously promoting the legalization of virtual assets and the establishment of regulatory frameworks in recent years. Coinciding with Singapore's tightening, Hong Kong is actively accommodating the crypto businesses that are being squeezed out. Hong Kong Legislative Council member and National Committee member Wu Jiezhuang tweeted that Singapore recently released the "Guidelines on Licensing for Digital Token Service Providers," which introduces new policies for companies, institutions, and personnel engaged in virtual assets. Since Hong Kong issued its virtual asset declaration in 2022, it has welcomed the industry to develop in the region. According to unofficial statistics, over a thousand Web3 companies have established operations in Hong Kong. Companies engaged in related industries in Singapore are encouraged to relocate their headquarters and teams to Hong Kong, with the government willing to provide policy and landing assistance, aiming to make Hong Kong a leading crypto hub in Asia.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。