Written by: Rita

Trends Guide

On July 15, Jefferies provided key insights during a conference call with optical experts: the demand for optical modules is surging too quickly, and supply cannot keep pace. There is a 10% shortfall in 800G, a 30% shortfall in 1.6T, and by 2027, the entire market size is expected to triple compared to 2025.

Behind the shortages is the fact that American companies have a lock on upstream chips, while China has advantages in passive components and indium phosphide (InP) substrates. The optical module market is tripling, but where the money goes is distinctly different.

The optical module market is tripling, but 1.6T is still 30% short

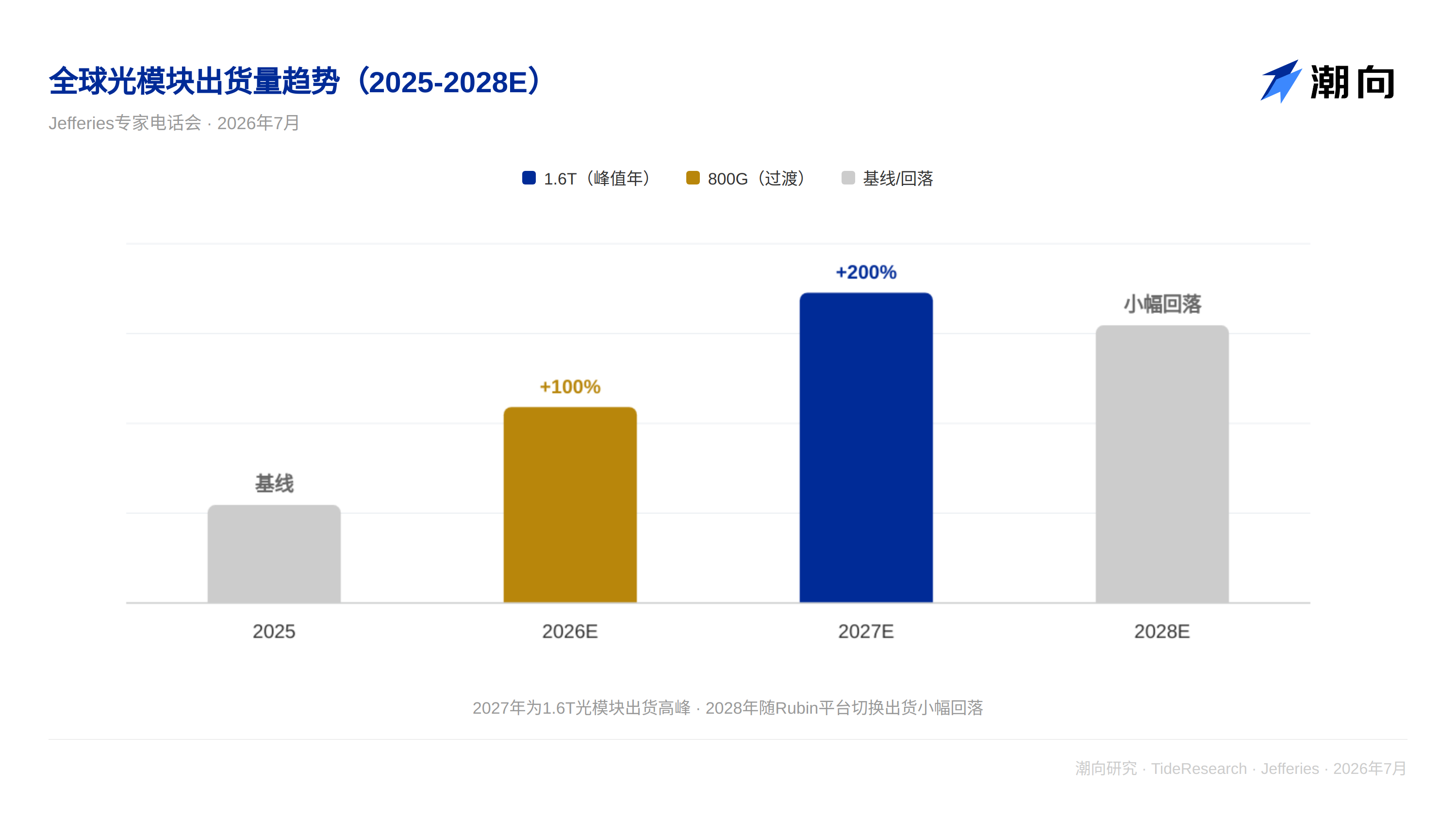

The demand side is clear. The shipment of 800G optical modules is expected to be about 40-42 million units in 2026, with demand exceeding 45 million units, resulting in a shortfall of about 10%. Shipments for 2027 are expected to reach 80 million units, with a slight decrease in 2028.

The shortfall for 1.6T is even larger. Shipments are expected to be around 18 million units in 2026, with demand around 26 million units, resulting in a 30% shortfall. Shipments are expected to reach 55 million units in 2027, with demand exceeding 75 million units, still facing a 30% shortfall.

Samples for 3.2T are expected to ship in the fourth quarter of 2026, and small-scale commercial use will have to wait until the fourth quarter of 2027. By 2028, shipments for 1.6T are expected to skyrocket to 100 million units, while 3.2T will begin with about 2.5 million units.

At this pace, the optical module market in 2027 will be three times that of 2025.

DSP and 200G EML are controlled by the United States

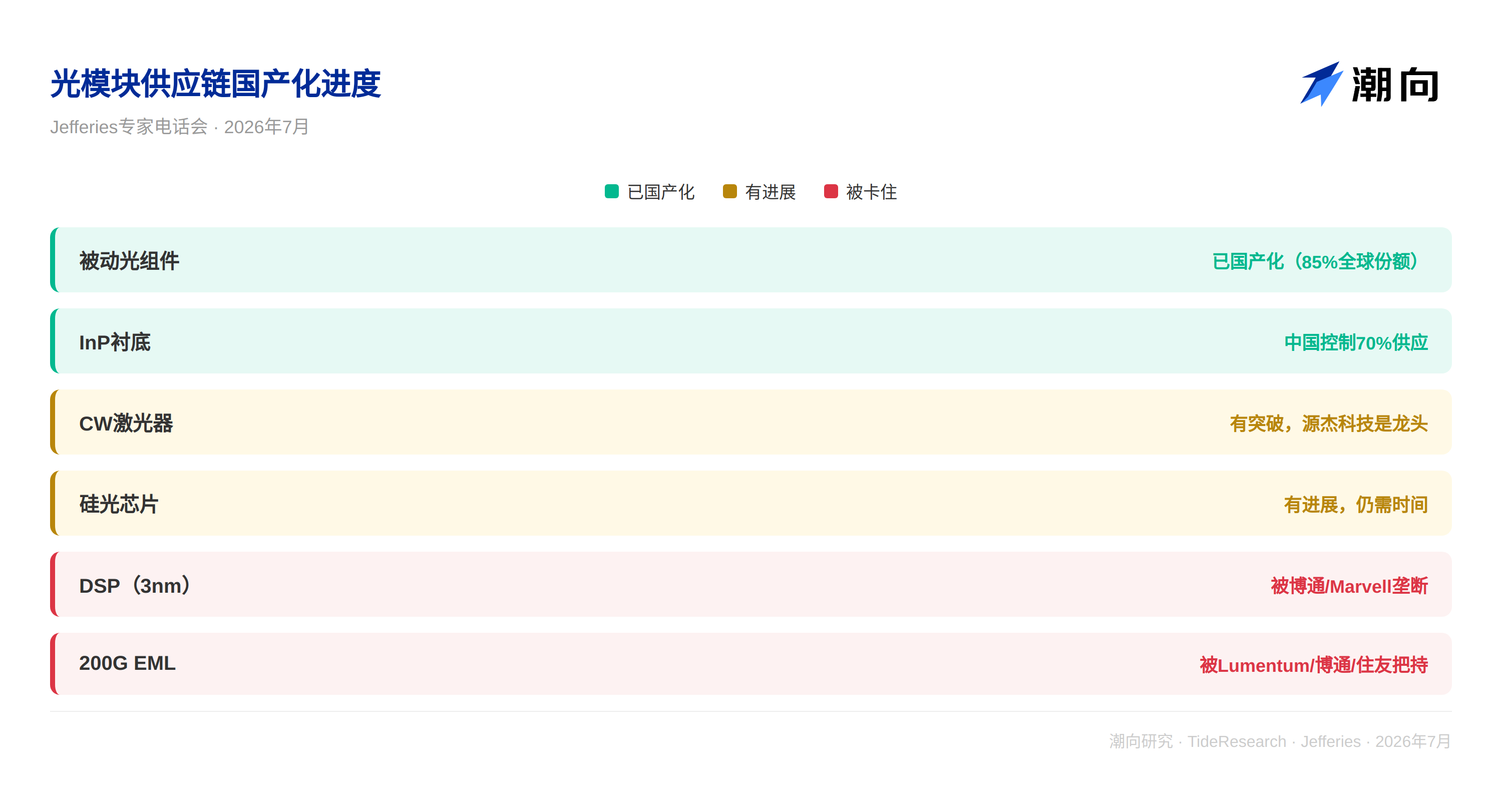

The upstream bottleneck for optical modules lies in DSP and 200G EML.

The 3nm DSP chips used for 1.6T are monopolized by Broadcom and Marvell. The 200G EML is controlled by Lumentum, Broadcom, and Sumitomo Electric. China currently lacks a mature 200G EML supplier, with Desay Battery expected to start mass production in the second half of 2026.

The progress of localization in China varies. For passive optical components (isolators, filters, lenses, AWG), China accounts for 85% of the global market. In terms of CW lasers, SourceLight Technology is a leader, along with four other companies in development. Progress has been made in electric chips and silicon photonic chips, but more time is needed.

In the optical module assembly sector, Zhongji Xuchuang, Neward, Optical Communication Technology, and Tianfu Communication are the main players.

The winning hand in the material route: InP is irreplaceable

The era of 800G belongs to EML. By the time we reach 1.6T, silicon photonic solutions are expected to capture over 60% of the market share—15% lower power consumption, and lower costs (only needing 2-4 CW lasers compared to 8 for EML), and higher integration. However, when we move to 3.2T, EML will once again dominate because silicon photonics cannot achieve the required frequency.

More critically, no matter which technical route is taken, we cannot avoid indium phosphide (InP). EML requires InP substrates, and the CW lasers needed for silicon photonic solutions and CPO solutions also rely on InP. China controls 70% of the global InP supply, with Yunnan Ge Industry as the core player.

Thin film lithium niobate may become a new modulation material in the 3.2T era, but it is only responsible for the modulation function; the light source will still rely on InP-based CW lasers. Therefore, InP is irreplaceable in optical interconnect solutions for data centers.

Trend Perspective

The demand for optical modules is certain, but the upstream supply landscape determines profit distribution. American companies hold the key with DSP and high-end EML, while Chinese companies control InP substrates and passive components. The flow of three times the money for optical modules depends on understanding who controls the irreplaceable segments.

For investors, the two most important directions to watch are: first, the InP supply chain (with 70% of global supply in China), and second, the progress of breakthroughs in 200G EML in China (mass production by Desay Battery in the second half of the year is a critical milestone).

Disclaimer

This article is a整理和解读 of the third-party brokerage research report (Jefferies, July 16, 2026) by Trend Research. The ratings, target prices, profit forecasts, and related judgments quoted in the text are the views of the brokerage analysts and only represent their institution's position, not the views of Trend Research and do not constitute any investment advice.

The market carries risks, and decisions should be made independently. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。