In recent days, the market correction has made many of my brothers feel hesitant. Some even started to doubt whether this round of AI wave has already hit the "bubble burst" point. 🧐

But my answer is firm: this is by no means the end; instead, it is one of the best "golden pit" bottom-fishing opportunities of the year. Although last night, the issue of New York State banning the construction of data centers made me miss the best bottom-fishing time, I have already added half my position before the market opened today!

Next, I will discuss some underlying logic, combined with $ASML's Q2 financial report and TSMC's June performance report, providing double validation for the golden pit value of AI semiconductors!

1️⃣ASML and TSMC: Using indisputable data to shatter the "AI stalling theory"

To be honest, the results released by the two semiconductor giants in recent days are essentially slapping the bears in the face. As the upstream of the chip industry chain, their financial reports are the hardest anchors of this round of AI capital expenditure cycle.

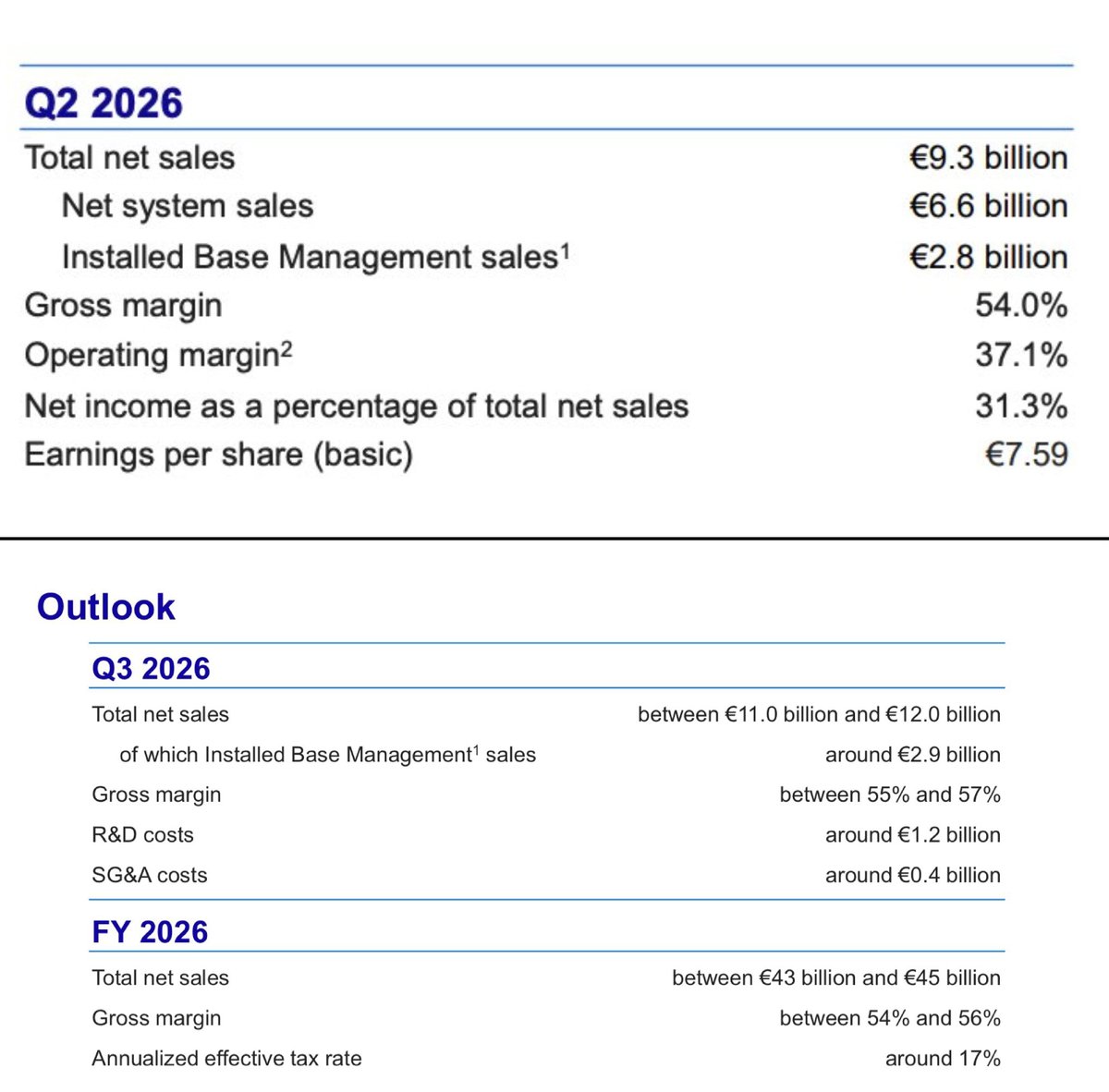

I have been focusing on ASML for more than a year or two, and honestly, this Q2 report ranks among the top three in terms of value over the past five years. The reason is not the expected revenue of 9.33 billion euros in Q2, which is all past. The real signal is that three forward-looking variables were simultaneously revised upwards, and the upward adjustment magnitude is somewhat exaggerated! 🤔

First, look at the significance of these data in the financial report:

2026 full-year guidance: Revenue from 36-40 billion euros → 43-45 billion euros. The lower limit has been raised directly above the original upper limit. This is the second upward revision this year, the first was in April from 34-39 billion → 36-40 billion. Two upward revisions within the same year, and the second one is much larger than the first, indicating that order visibility is accelerating rather than flattening.

Gross margin guidance: From 51-53% → 54-56%. In the business of EUV equipment, every 1% increase in gross margin represents an upward shift in product mix and enhanced bargaining power. A 3% increase equals ASML telling the market: customers not only want to buy but are scrambling to buy High-NA and upgrade packages.

Q3 guidance: 11-12 billion euros, with a median of 11.5 billion, compared to Bloomberg's consensus estimate of 10.27 billion. This is not "slightly exceeding expectations," this is hitting the sell-side model in the face.

More crucially, one statement from CFO Roger Dassen: EUV capacity for 2027 is almost fully booked, with a significant number of orders already locked in for 2028. EUV takes more than a year from order to delivery, and CEO Fouquet directly revealed that the low NA EUV capacity for 2026 will be about 65 units, increasing by 30% in 2027, with further studies for another 30% increase in 2028; DUV immersion 130 units capacity in 2026, similarly increasing by 30% for two consecutive years. This trajectory is not about "responding to demand," it's about "not keeping up with demand,” as demand far exceeds expectations!

Additionally, Intel's $INTC Ultra 3 (Panther Lake) using High-NA EUV for mass production is another signal severely underestimated by the market. TSMC had previously publicly stated that High-NA costs are too high and adoption would be delayed, leading the market to question whether the $400 million machine could be commercialized. Intel directly ramped this machine up to mass production in Oregon, which equates to completing the valuation shift from "concept" to "production line" for High-NA. ASML’s most expensive product line is beginning to cycle positively.

Lastly, I want to add a point that may be overlooked: Musk's Terafab. ASML clearly acknowledges that in the 2027-2028 capacity planning, they have accounted for the demand from Musk's Terafab in Texas. In other words, even without considering such "black swan" incremental capacity as Terafab, ASML’s roadmap is already tightened. Once xAI/Tesla's self-developed chips are successful, it will represent another significant upward revaluation potential after 2029!

2️⃣ TSMC's June revenue: An independent evidence chain from the demand side

I never make judgments based on a single company. If ASML says demand is good, there must be client confirmations. TSMC’s combined revenue in June was 442.68 billion New Taiwan dollars, year-on-year +67.9%, exceeding the upper limit of broker predictions. The cumulative first-half revenue reached 2.4 trillion New Taiwan dollars, year-on-year +35.6%. From 415.2 billion in March, it climbed to 442.7 billion in June, with Q2 showing a single quarter reaching 1.2 trillion.

The growth curve of TSMC tells me several things:

Firstly, the N3 process has not weakened, but is accelerating. This is crucial at this moment in 2026, as according to the old semiconductor cycle rhythm, N3 should have already reached a demand plateau, but the orders from AI/HPC clients are pushing it further up.

Secondly, the preliminary volume release of N2 has arrived. In the institutional forecasts, ASP is up 10.7% month-on-month, and shipments are up 2.4%, indicating that the structure is driven by "more expensive advanced processes" instead of "more mature processes moving volume." This quantity-price structure is the most efficient for transmitting throughout the upstream equipment chain, EDA, and IP licensing.

Lastly, a gross margin of 67.6%. If realized, it would be a new historical high. TSMC's gross margin is the bottom line for global wafer foundry; if it rises to 67%, it elevates the entire pricing chain for advanced processes. ASML's upward revision to 54-56% is not coincidental; it's two sides of the same coin, mutually validating each other.

TSMC's financial report is due on the 16th, and I'm particularly interested in two things regarding the Q2 performance meeting: capital expenditure guidance and CoWoS/SoIC capacity planning. Institutions project capital expenditures of $57.2 billion / $76 billion / $88.6 billion for 2026-2028. If the Q2 performance meeting raises the 2026 full-year cap from $56 billion to $58 billion or even $60 billion, the valuation anchor for the equipment sector will need to shift upward. If they continue to indicate a tight situation for CoWoS and provide a more aggressive monthly capacity roadmap, that will directly benefit the entire ASIC chain of Nvidia, AMD, Broadcom, and Marvell.

3️⃣ In-depth logic on the demand side: This round is not an "AI chip cycle," but a "rebuilding of AI infrastructure"

I reviewed the SEMI mid-year forecast released on Tuesday, indicating that global semiconductor equipment sales will reach $229.5 billion by 2028, marking five consecutive years of growth. In 2025, it will be $165.9 billion, a year-on-year increase of +23.2%; wafer manufacturing equipment will see +23.1% to $143.9 billion in 2026, then an increase of +21.8% in 2027, and +14.1% in 2028 reaching $200 billion; test equipment will surge by 55.3% in 2025, followed by +31% in 2026; memory will increase by 39% to $13.9 billion in 2026, and reach $20.8 billion in 2028.

👆The data above may give people headaches. Let me break it down in simple terms: Capital expenditure driven by AI is expanding from "CPU/GPU" to the entire chain of "HBM+packaging+testing+power." This is not the short cycle of cryptocurrency ASICs seen in 2017-2018, nor the chip shortages during the pandemic in 2021. This round is a physical layer transformation of data centers from general computing to heterogeneous computing, where each GPU needs to be accompanied by HBM, HBM requires CoWoS packaging, CoWoS necessitates a large number of advanced test equipment, cabinets need liquid cooling, high-voltage DC power supplies, and 800G/1.6T optical modules. Every step in this chain is expanding production and raising prices.

From a financial perspective, the customer structure is also optimizing. Fouquet made a very important statement: clients are signing long-term agreements with their own clients. The significance of this statement is substantial; TSMC is locking down capacity with Nvidia, Apple, and AMD for three to five years; HBM manufacturers are locking multi-year agreements with AI cloud service providers. When the revenue visibility of the entire industry chain extends from six months to three years, the valuation multiples should expand, not contract. ASML's advanced foundry logic shows this year's revenue up +25% and memory up +75%; this figure for memory is the most explosive in this financial report, indicating that the re-investment in HBM3E/HBM4 capacity has fully launched.

4️⃣ CPI + Federal Reserve liquidity: The macro wind has shifted towards risk assets

I believe yesterday's CPI data is a watershed moment in this round of correction. Core inflation continues to unexpectedly decline, and the market's implied probability for Fed interest rate hikes in 2026 has plummeted. The signals from CME FedWatch are clear: the likelihood of another rate hike this year is very low, and there is even room for rate cuts by the end of the year. This is a triple boon for risk assets:

Real interest rates have peaked. Once the 10-year real yield confirms a downward channel, long-duration assets (growth stocks, AI infrastructure stocks) should experience valuation expansion.

Expectations for US dollar liquidity easing have strengthened. The combinations of RRP balances, reserves, and the Treasury's TGA point to positive net liquidity injections in the second half of the year.

Credit spreads are not widening. When high-yield bond spreads do not expand, it indicates that the market is not pricing in a recession. At this moment, declines in the equity market can only be characterized as "position adjustments," not "fundamental deterioration."

Overlapping these three factors onto the AI hardware sector: upward earnings revisions + declining risk-free rates + liquidity easing = a textbook scenario of a Davis double.

5️⃣ My conclusion: This wave of correction is an active deleveraging, not a trend ending

Let me be more straightforward. If you look at the structure during this recent market pullback, it becomes clear:

The deepest corrections have been for the Beta-high AI infrastructure leaders, not defensive sectors. This is a typical feature of "passive deleveraging," not "active risk-off." In the early stages of a real bear market, defensives typically drop more while growth falls less (because people have yet to realize the change). This time, it has flipped.

Volume has significantly increased during the correction, but it has not broken through critical support; it has basically made strong supports at the daily EMA 55 and 200 days. This indicates that the main forces are swapping holdings, offloading floating profit positions and second-quarter profit taking to prepare for the next round.

CDS spreads and VIX term structures have not shown signs of pressure. The futures curve for VIX is still in contango, indicating that the options market is not pricing systemic risk.

Analyst expectations for the semiconductor and optical module leaders continue to be revised upwards. Performance hasn't deteriorated, and valuations are contracting. This defines the best buying point.

After ASML's financial report came out, I have a clearer view of the time window: from mid to late July to early August is the golden window for increasing positions in this round of AI hardware correction. By the time Q3 earnings season (mid to late October) validates the performance again, valuations will return to normal positions, or even higher. Each week missed in this time window dilutes the odds.

📝 My position strategy

I usually avoid specifying individual stocks, but the allocation logic can be summarized in four points:

Upstream equipment ($ASML, $AMAT, $LRCX, $KLAC), with capacity for 2027-2028 almost locked down, the visibility of performance is the strongest, and the correction has brought valuations to a reasonable range. After this round of upward revisions, ASML's forward PE is still around 36 times, which isn't too expensive.

Foundry and IDM (TSMC, Intel's commercialization progress on High-NA is a catalyst), $TSM is the core foundation, with the July 16 earnings meeting being the most significant short-term catalyst.

HBM+packaging+testing, the fastest-growing sector in the SEMI data, has seen the most thorough correction this round, with valuations hit hard, thus the rebound force will also be the largest Alpha asset.

AI infrastructure support (optical modules, liquid cooling, power supplies), with the highest Beta, experienced a deep correction, but has the most valuation elasticity.

Lastly, I want to energize everyone: at the early stage of any technological revolution, the ones who profit the most are always those who build bridges, lay roads, and sell water and shovels. As long as the singularity of computing power expansion does not stagnate, AI hardware, as the unique infrastructure for running large models in the physical world, will not undergo any fundamental changes in its long-term upward trend.

Brothers, manage your positions well, actively wash away leverage, but never lose your core chips at the brink of dawn.

Tonight is the best time for us to "Buy the Dip" in batches, decisively, and with discipline. Load the bullets and wait for the flowers to bloom! 🧐

For trading US stocks, I choose #RWA US stock tokenization platform #MSX, let us invest together in the US stock market: http://msx.com/?code=Vu2v44

Early US stock investment fans and partners can DM me; after filling out the form, you can enter the US stock communication and discussion community for free (currently limited to 10 people per week, assistant review may take some time, thank you 🙏)!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。