TL;DR

- A semiconductor investor roundtable survey shows that funds prefer TXN, memory, and AMD, while being more cautious about equipment stocks and Intel.

- 70% of respondents believe TSMC's performance impacts the sector more than ASML, focusing on the revenue growth rate and capital expenditure for 2026.

- There is stronger optimism for TXN and memory, but there is still uncertainty regarding equipment stock orders, HBM rumors, and Intel’s foundry services.

A monthly roundtable survey for semiconductor investors reveals that the AI semiconductor market has not cooled, but funding preferences have noticeably shifted. TSMC, Texas Instruments (TXN), memory, and AMD are positioned more favorably, while semiconductor equipment stocks and Intel face more skepticism.

The timing of this survey is sensitive. TSMC's official calendar shows it will hold a performance meeting for the second quarter of 2026 on July 16. Texas Instruments announced it will hold its second-quarter earnings call on July 22 at 3:30 PM Eastern Time. AMD's official calendar indicates that the Advancing AI 2026 event is scheduled for July 22 to 23, with a flagship global AI event broadcast mentioned in April set for July 23.

Short-term investors are not just looking for a statement that "AI demand is strong," but rather whether several companies can translate AI demand into revenue growth, capital expenditure, gross margins, customers, and orders.

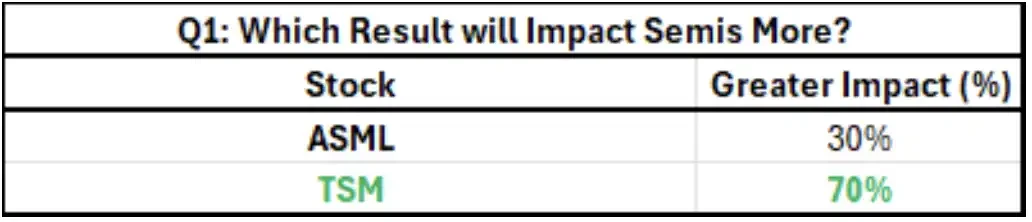

The most direct divergence in the survey was between TSMC and ASML. 70% of respondents believe TSMC’s performance has a greater impact on the overall semiconductor sector, while 30% chose ASML. This result indicates that buyers are currently more concerned about how much wafer foundry revenue and capital expenditure AI demand will ultimately translate into, rather than just the order volume for lithography machines.

Voting on influence: TSMC 70%, ASML 30%.

TSMC Becomes the First Stress Test for Semiconductors This Week

TSMC is positioned ahead of ASML because it connects two things: AI revenue growth and expectations for equipment stock orders.

The expectation among buyers in the survey is that TSMC may raise its 2026 sales growth guidance from more than 30% to over 35%, with some respondents even betting on nearly 40% year-on-year growth. The compound annual growth rate for AI sales over five years may also be revised upwards, with prior market discussions ranging in the mid-high 50% range.

These figures will directly affect investors' judgments on the sustainability of AI semiconductor demand. If TSMC confirms higher growth, the market is more likely to believe that demand for AI servers, advanced processes, and advanced packaging is continuing. If the company merely maintains its previous guidance, it may instead be viewed as "not strong enough" in the short term.

Even more sensitive is capital expenditure. TSMC previously provided a capital budget of $52 billion to $56 billion for 2026. The market now wants to hear whether the management will provide a clearer medium-term capital expenditure framework, but this is still a buyer expectation and not a confirmed arrangement.

Pressure on equipment stocks also stems from this. Over the past two weeks, equipment stocks have retreated, partly due to investor concerns that if TSMC does not signal sufficiently strong medium-term capital expenditure, the previously implied order expectations for equipment stocks may need to be revised down.

ASML's issue is not that there is no room for good news. After underperforming recently, valuation pressure has somewhat eased. However, the bar for buyers in the survey has already been set high, with expectations for 2026 EUV lithography machine shipments pushed above 100 units. For ASML, the performance press release itself may not be enough; orders, customers, and the pace for 2026 from the earnings call and subsequent communications will be more important.

TXN is Bet to Drive Analog Semiconductors

Within analog semiconductors, Texas Instruments is a clearer optimistic anchor.

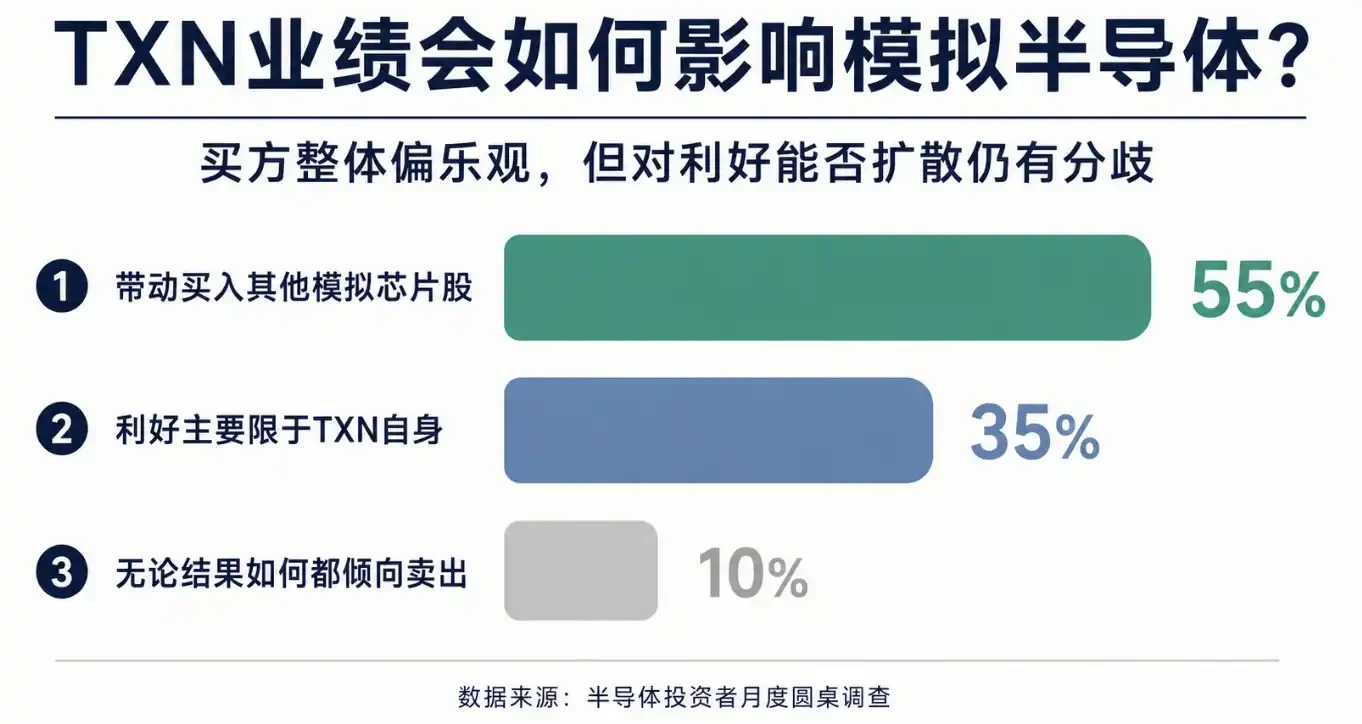

The survey shows that 55% of respondents believe that if Texas Instruments reports positively, it will drive buying of other analog semiconductor stocks. 35% think the good news will mainly be limited to Texas Instruments itself. Only 10% indicated they would sell regardless of the outcome.

Texas Instruments performance spillover expectations: 55% believe it will drive other analog stocks, 35% believe it's mainly limited to Texas Instruments, 10% tend to sell.

Investors are betting not on just a single quarter of better revenue, but on potential simultaneous improvements in demand, pricing, and gross margins for analog semiconductors.

The market expectation in the survey is that the consensus for Texas Instruments’ third-quarter sales quarter-on-quarter growth rate is about 7%, higher than the normal seasonality of 5%. Some buyers believe this figure may be revised up to 9% to 10%. On gross margins, the market consensus is about 60.25%, with Citi expecting 60.5%, and optimistic investors are still waiting for room for upside surprises.

Three main factors support this judgment: multiple rounds of price increases gradually entering financial statements, improved capacity utilization, and demand related to 800-volt technology entering a more favorable timing. For analog semiconductors, if revenue recovery is combined with gross margin improvement, the earnings elasticity will be more pronounced than simply rebounding shipments.

The boundaries are also clear. Whether good results from Texas Instruments can spill over to the entire analog semiconductor sector depends on whether the demand improvement is sufficiently broad, rather than just better pricing, capacity, or product structure for the company itself. Still, 35% of respondents believe that the good news may primarily belong to Texas Instruments, and the analog sector has not gained a consistent bullish outlook.

Memory Buying is More Concentrated, but HBM Rumors Remain Disruptive

Memory is another direction where optimistic sentiment is concentrated.

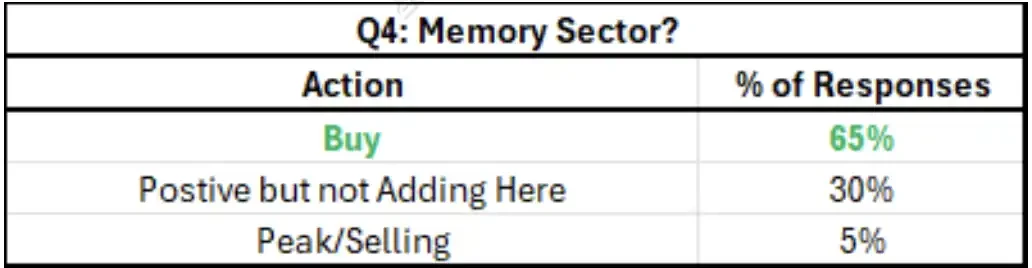

The survey shows that 65% of respondents choose to buy into the memory sector, 30% have a positive attitude but are not adding positions, and 5% believe it has peaked. This distribution shows that memory has become relatively crowded within semiconductors but is still viewed favorably by buyers.

Memory investment attitudes: 65% buy, 30% positive but not adding positions, 5% believe it has peaked.

Optimistic expectations stem from potential demand extending into the first half of 2027. Long-term agreements are also changing investors' perspectives on memory companies. If customers secure supply through long-term agreements, memory manufacturers will have better visibility on demand, capital expenditure, and free cash flow, making it easier to consider shareholder returns in valuations.

The survey also mentioned that some memory companies might repurchase over 20% of their shares. This figure is significant for cyclical stocks, as memory has often been discounted by the market on the premise of "peak cycle will reverse." If cash flow is more stable and repurchase is more defined, valuation logic may no longer treat them solely as traditional cyclical stocks.

However, memory also has controversies. Respondents slightly prefer NAND and DRAM and remain skeptical about the "de-specification" rumors regarding HBM. One view is that this may just be a strategy in negotiations between customers and suppliers, and does not necessarily indicate a real deterioration in demand. Another risk is that if high-end HBM specifications or pricing do not meet expectations, optimistic sentiment regarding memory could be impacted.

AMD More Easily Tells the 2026 Story, Intel Still Needs to Prove Foundry

AMD's AI event from July 22 to 23 is another focus within the semiconductor funding divergence.

The survey shows that 50% of respondents expect the event's outcome to be bullish and are prepared to trade long. 40% believe the outcome will be positive but more neutral. 10% worry about selling out of disappointment.

The market hopes AMD will provide several types of information: the total addressable market for CPUs and GPUs expands, progress with new customers, improvement in average selling prices, rebound in Xilinx high-margin business, and TSMC’s foundry support for 2027. To put it more directly, investors want to confirm that AMD is not just a second-tier target for "AI replacement trades," but can form clearer revenue and profit clues in 2026 and 2027.

This also explains the change in attitude towards Intel in the survey. Buyers prefer AMD and are becoming cautious about Intel. The reason is not that Intel has no opportunities at all, but that the difficulty of the stories each company can tell is different: AMD's profitability model for 2026 is easier to construct, while for Intel’s stock price to significantly rise, the market needs more confidence in its path to successful foundry services.

Intel’s issue still lies in execution. To gain customer trust in foundry services, it needs to prove itself in process, yield, delivery, and economics simultaneously. As long as this path is unclear, it is not surprising that funds continue to shift towards AMD.

The backdrop of this round of semiconductor divergence is clear: AI demand remains strong, but funds are no longer buying all semiconductor assets indiscriminately. TSMC needs to prove growth and capital expenditure can still support the equipment chain, Texas Instruments needs to prove price increases and utilization can drive analog stocks, memory needs to prove long-term agreements and HBM demand are not just short-term sentiments, and AMD needs to translate AI opportunities into customers, pricing, and profitability models.

The areas most prone to issues in the short term still involve expectations that have already been heightened. If TSMC does not provide sufficiently clear signals on medium-term capital expenditure, equipment stocks may continue to feel pressure. If HBM de-specification rumors are confirmed to be more than just negotiation noise, optimistic sentiment regarding memory may cool. If Intel fails to increase market confidence in the success of its foundry services, the trend of buyers leaning towards AMD will likely continue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。