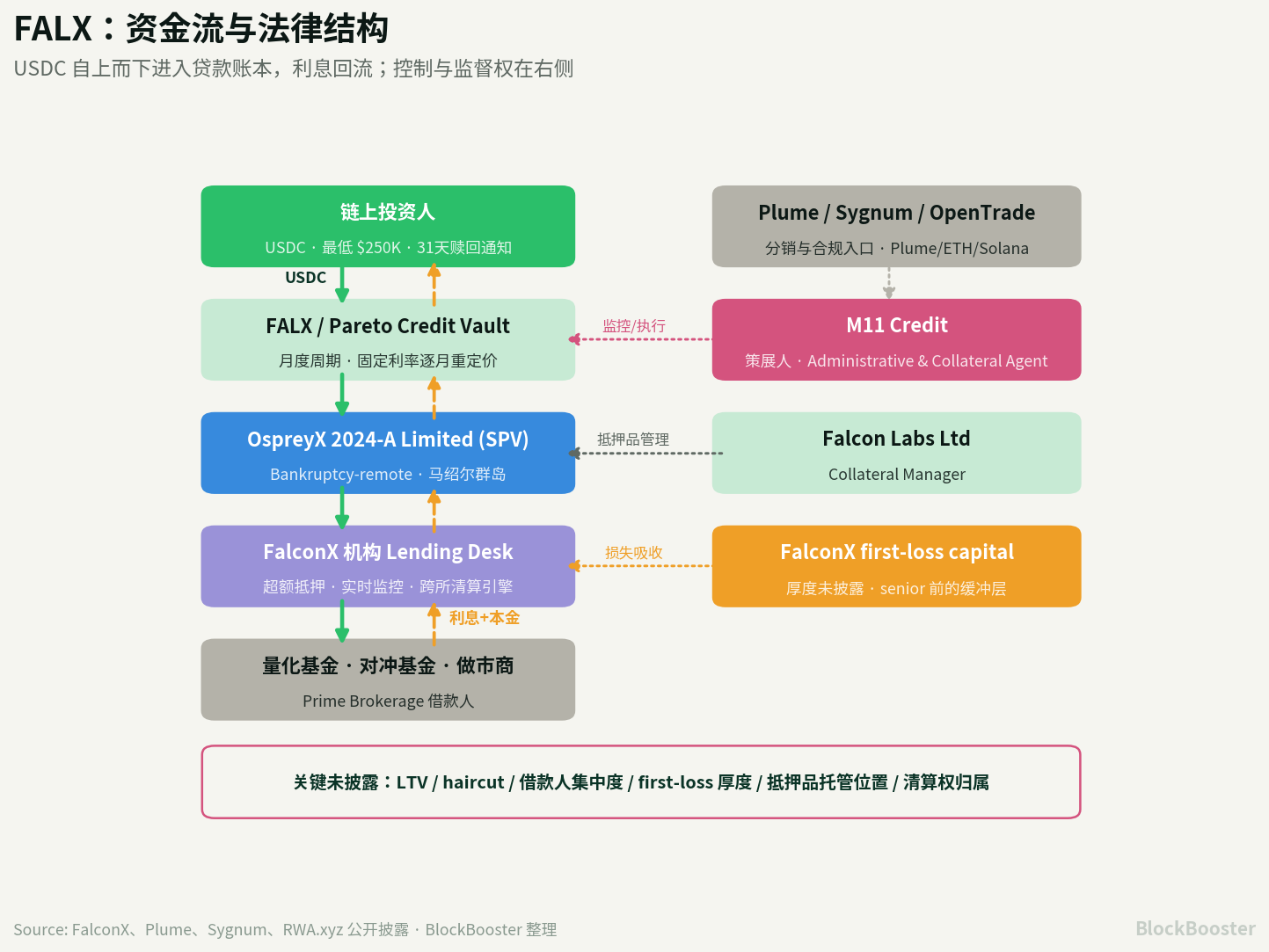

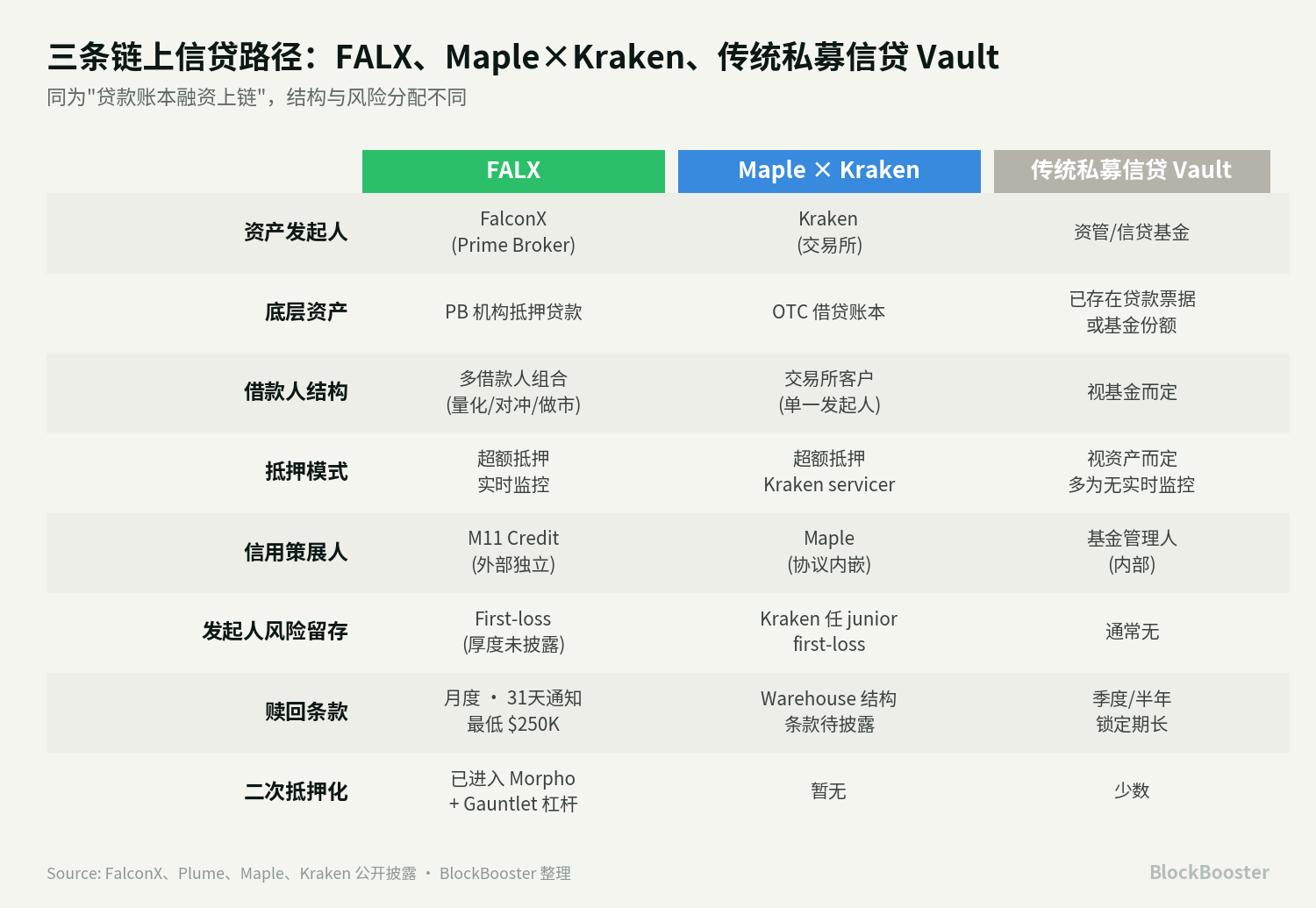

FALX is a capital formation mechanism that processes Prime Brokerage loan ledgers into on-chain fixed income assets.

Its core structure is:

- FalconX initiates collateralized loans

- → Loan exposure enters FalconX-managed SPV

- → Pareto provides on-chain Credit Vault

- → M11 Credit acts as credit curator, administrative agent, and collateral agent

- → On-chain entry distributions to investors through Plume / Ethereum / Solana, etc.

1. What exactly is FALX

FALX is more like an on-chain structured credit facility: investors deposit USDC into Pareto/FALX related Vaults, the funds enter a bankruptcy-isolated SPV related to FalconX, and then via FalconX's institutional credit system, over-collateralized loans are granted to institutional clients such as quantitative funds, hedge funds, market makers, and asset managers.

In March 2025, FalconX announced its Structured Credit Facility, which packages FalconX-originated loans into structured products, allowing investors to access via the Pareto private credit Vault, and curated by M11 Credit. FalconX believes this connects the institutional credit asset formation process to on-chain capital.

On June 30, 2026, Plume announced the launch of the FALX Structured Credit Facility. According to disclosures from Plume, the Vault is supported by infrastructure provided by Pareto, curated by M11 Credit, with funds entering a FalconX-managed SPV, with underlying exposure coming from over-collateralized loans initiated by FalconX Prime Brokerage platform; this facility is also described as scalable to about $1B capacity.

Thus, FALX on Plume resembles a new entry and expansion of this existing structured credit facility from FalconX/Pareto/M11, rather than a completely new asset pool starting from scratch.

2. Capital flow and participants

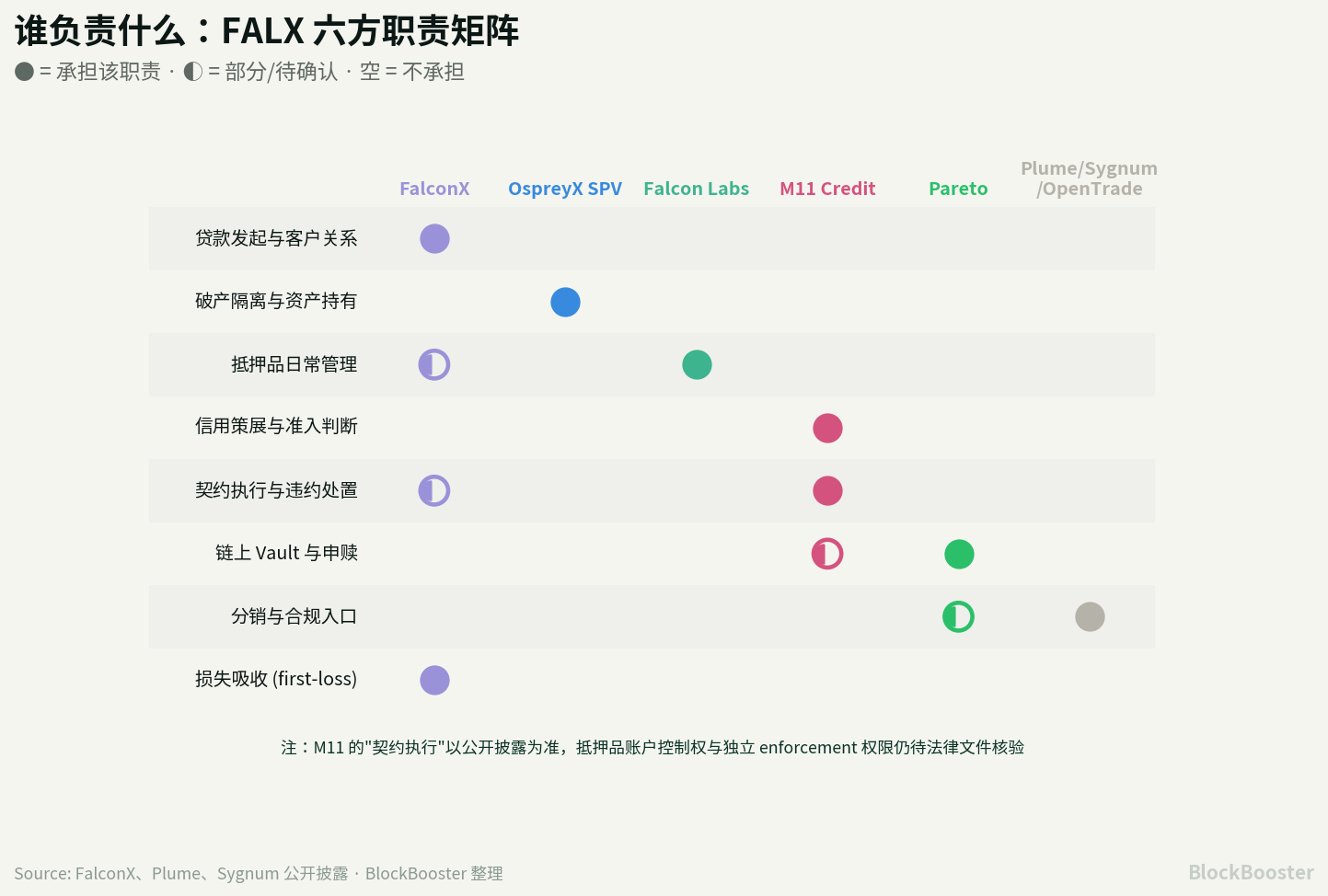

The six main participants are as follows:

In June 2026, FalconX disclosed that the Vault loaned to OspreyX 2024-A Limited, which is designed as bankruptcy-remote, aimed at isolating investor capital from FalconX's company balance sheet; Falcon Labs Ltd serves as Collateral Manager, M11 Credit functions as Administrative and Collateral Agent, and FalconX provides first-loss capital contribution.

3. Who pays the return

The returns of FALX are the financing costs paid by Prime Brokerage borrowers in order to achieve capital efficiency.

FalconX's financing business covers scenarios such as margin loans, flexible settlement, OTC lending, DMA credit, prime brokerage financing, structured products, and yield generation.

This product list indicates that the underlying cash flow of FALX comes from the comprehensive financing needs of institutions making capital adjustments across multiple trading venues, various collateral, and multiple settlement cycles.

Therefore, the returns of FALX come from four types of premiums:

- U.S. dollar benchmark interest rate;

- Digital asset collateral volatility premium;

- Instant liquidity and cross-exchange scheduling premium;

- Prime Brokerage service premium.

This also explains why FALX cannot simply be compared to the Aave USDC supply rate. Aave is on-chain over-collateralized, algorithmic interest rates, and public pools; FALX is an institutional Prime Brokerage loan portfolio, taking on risks from FalconX, SPV, M11, collateral execution, and underlying client portfolio.

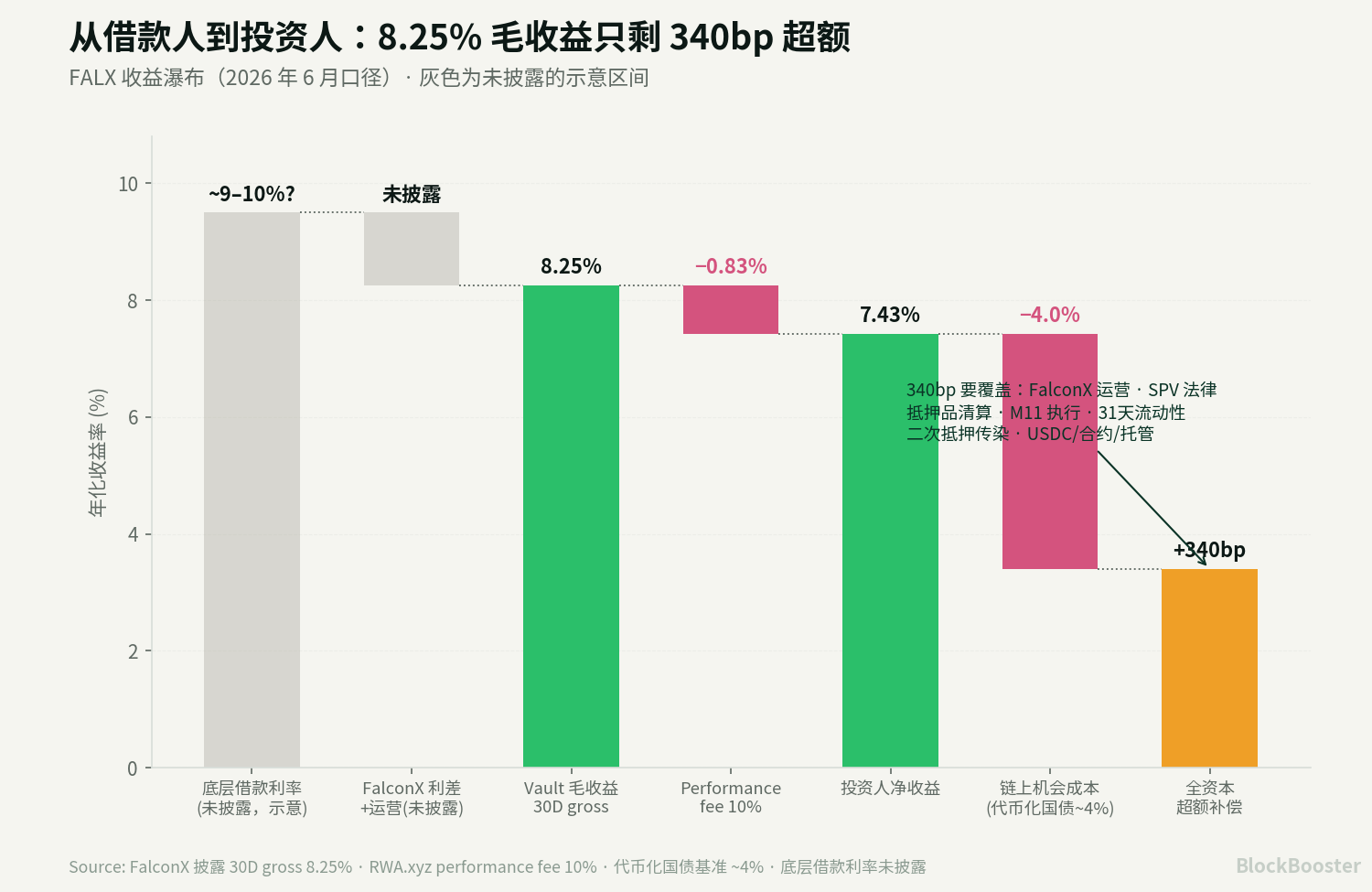

4. Return calculation

FalconX discloses:

- Benchmark yield = FalconX disclosed 30D gross yield 8.25%

- Less 10% performance fee

- Investor approximate net yield ≈ 7.4%

The next step is to calculate excess return. For on-chain USDC investors, the most relevant opportunity cost is the obtainable low credit risk yield on-chain, such as tokenized treasury bonds, BUIDL-type money market products or Aave USDC. FalconX itself compared Aave USDC at 3.26% in the article. Considering that tokenized treasury bonds are approximately around 4%, this paper uses 4% as the opportunity cost for on-chain funds.

Thus:

- FALX net yield approximately 7.4%

- − On-chain USDC low-risk opportunity cost approximately 4.0%

- = Excess compensation approximately 3.4%

This 340bp needs to cover:

- FalconX operational risks;

- SPV legal risks;

- Collateral liquidation risks;

- M11 execution risks;

- Liquidity discount caused by 31-day redemption notice;

- Contagion risks from DeFi secondary collateralization;

- USDC, contract, cross-chain, and custody risks.

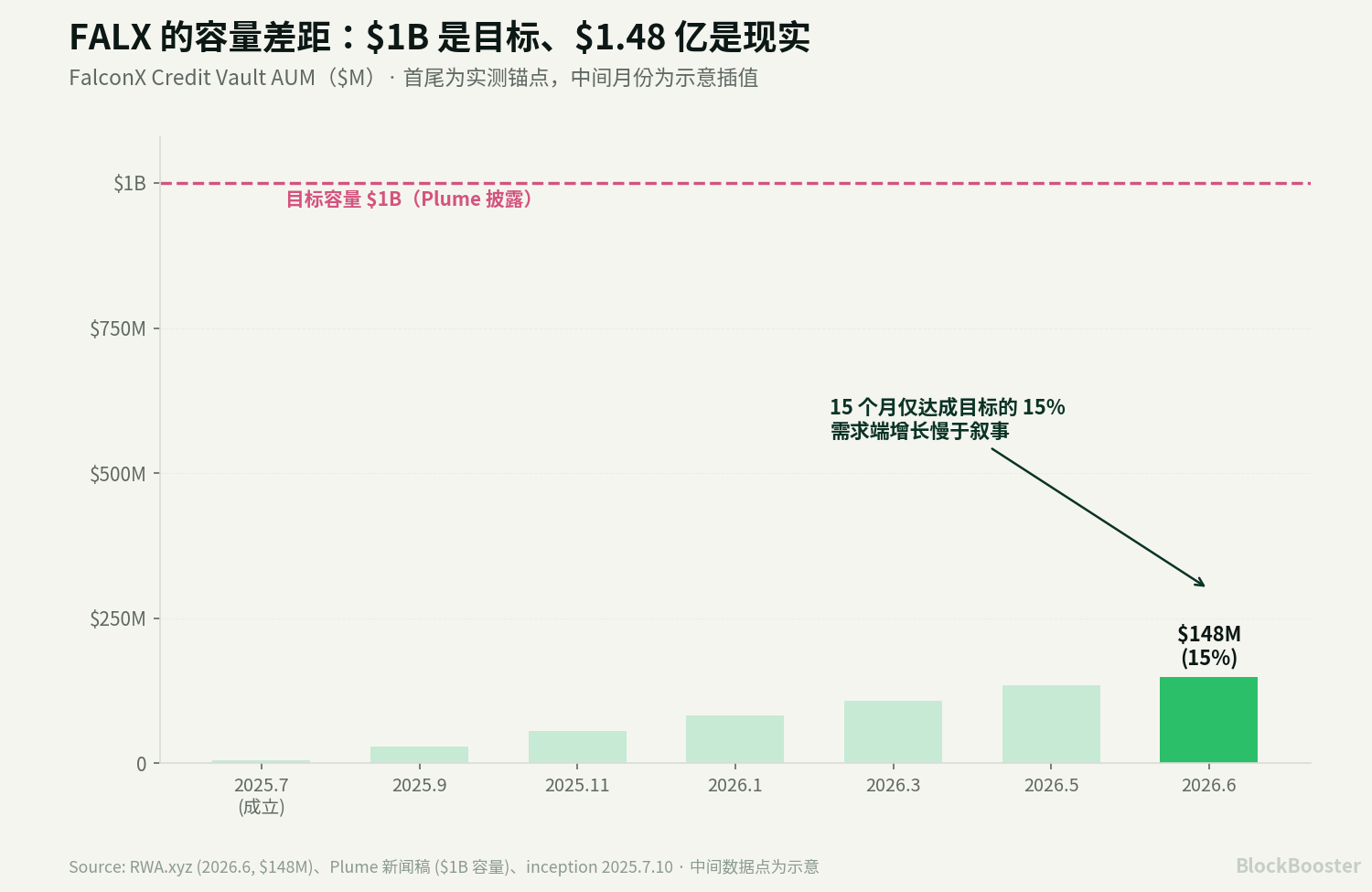

5. FALX capacity reality

Plume disclosed that the current capacity of FALX is scalable to about $1 billion.

FalconX disclosed in March 2025 that its 2024 loan originations reached $2.5 billion, indicating that FalconX has the capability to initiate loans.

However, RWA.xyz's current page shows that the total assets of the FalconX Credit Vault are about $148 million.

There is an important signal here: In March 2025, SCF announced that by June 2026, the Vault AUM would be approximately $148 million, only reaching about 15% of the $1 billion target capacity. This suggests that demand for on-chain funds for this type of product is not easy to grow.

Capacity can be broken down into five layers:

- Legal and contractual capacity: How much can the SPV and Vault theoretically support;

- Loan origination capacity: What is the total institutional loan demand for FalconX;

- Qualified loan capacity: How many loans meet LTV, collateral, borrower concentration, and covenant standards;

- Target yield capacity: How much borrowers are willing to borrow at a net yield of 7%-8% for investors;

- Investor demand capacity: Whether on-chain funds are willing to accept a minimum investment of 250,000 USDC, a 31-day redemption notice, and complex credit risks.

6. The role of M11

6.1 The positive value of M11 in FALX

FalconX discloses that M11 is the Vault Curator, responsible for reporting, epoch cycles, subscription and redemption requests, credit assessments, loan covenants execution, and real-time risk monitoring.

Plume discloses that M11 Credit also acts as a curator.

Sygnum explicitly discloses that M11 Credit is the Administrative and Collateral Agent.

This indicates that M11 is not an ordinary distributor. It takes on the most critical intermediary layer in credit products: representing investors in assessing whether assets can enter the pool, and supervising the initiator and borrower throughout the loan cycle.

6.2 Review of M11's blemishes

M11 must be viewed alongside its failure case on Maple in 2022. In December 2022, Orthogonal Trading defaulted on approximately $36 million on Maple, of which $31 million came from the USDC pool managed by M11, and another approximately $5 million came from the wETH pool managed by M11; this resulted in about an 80% hit to the remaining investors in the M11 USDC pool.

M11's own disclosures also acknowledge that Orthogonal severely misreported its financial situation after the FTX collapse, only revealing on December 3 that its losses far exceeded previous claims and could not repay. M11 states that Orthogonal had continuously asserted both verbally and in writing that its exposure to FTX was limited, which severely impacted M11's ability to manage credit risks.

This case exposed four problems:

- Over-reliance on borrower self-reported data: If borrowers intentionally conceal, curators may not be able to discover in time;

- Concentration out of control: By December 2022, approximately 80% of loans in one USDC pool managed by M11 were concentrated in Orthogonal, whereas that proportion was about 14% at the end of August;

- Insufficient pool cover protection and valuation issues: Pool covers for the three pools managed by M11 were essentially exhausted, covering only a small portion of bad debts; meanwhile, the native Maple token MPL plummeted during the risk event. The underlying lesson is that if first-loss/insurance is primarily valued in related governance tokens, when a risk event occurs, the insured and insuring assets may depreciate simultaneously;

6.3 Essential differences between FALX and Maple 2022

The issues of Maple/M11 in 2022 essentially stemmed from unsecured/low-collateral institutional credit loans. They relied on borrowers disclosing balance sheets, exchange exposure, and financial statuses. Once a borrower lies, on-chain transparency cannot automatically discover off-chain asset black holes.

FALX has a different structure. It is Prime Brokerage over-collateralized loans; FalconX discloses its use of real-time collateral monitoring, automated margin calls, cross-exchange clearing engines, and first-loss capital contributions.

7. Loss waterfall: Who loses money first at least discloses three layers of protection:

FALX

- The underlying loans are typically over-collateralized;

- FalconX provides first-loss capital contribution;

- M11 acts as Administrative and Collateral Agent, providing independent supervision.

The ideal loss waterfall should be:

- Excess portion of collateral

- → Borrower adds margin

- → Collateral liquidation

- → FalconX first-loss/equity tranche

- → Other junior protections

- → Senior investors' principal loss.

However, public information does not disclose the specific thickness of each layer.

8. Redemption runs and secondary collateralization risks

The basic terms of FALX are monthly cycles and a 31-day redemption notice. RWA.xyz shows that the FalconX Credit Vault has a 31-day notice period for redemptions and discloses that, apart from a 10% performance fee, there are no other management, subscription, redemption, or entrance/exit fees.

This presents an ALM issue: Investors have a 31-day notice, and the underlying loans are also on a monthly rolling basis, but if in one month, 50% of investors redeem, does the SPV require FalconX to compress the loan ledger in advance, or to queue for redemption, set gates, or let the secondary market take on the risk? Public information has not sufficiently answered this question.

More importantly, FALX has entered the DeFi secondary collateralization layer. The FalconX Credit Vault Token has become one of the important RWA collaterals on Morpho; Gauntlet also launched the FalconX Levered RWA Strategy, using the FalconX CV token as collateral to borrow USDC and subsequently buy more CV tokens.

This will create a new transmission chain:

- FALX token used for Morpho collateral

- → Under market pressure, FALX token discounts or NAV adjustments

- → Morpho health factors decline

- → Liquidator sells or discounts FALX tokens

- → Secondary prices continue to decline

- → More holders redeem

- → SPV needs to release cash

- → FalconX loan ledger forced to contract or suspend redemptions.

The secondary collateralization of FALX enhances capital efficiency but also connects the initially relatively closed private credit risks to the DeFi clearing system. It transforms from a "credit product" to "composable collateral," accelerating the speed of risk transmission.

9. Conclusion

The true innovation of FALX is combining FalconX's Prime Brokerage loan ledger, SPV legal structure, M11's external credit curation, Pareto's on-chain Vault, and distribution channels such as Plume/Sygnum/OpenTrade into a comprehensive on-chain capital formation mechanism.

It proves that on-chain credit does not necessarily need to first solve the most challenging issue of "fully on-chain native credit scoring."

A more pragmatic path is: first find professional initiators with real cash flows and loan demands; then use SPV, first-loss, over-collateralization, external curators, and transparency of on-chain fund flows to process this batch of loans into investable assets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。