Original Author: Bao Yilong

Original Source: Wall Street Watch

Korean stocks experienced one of the most severe single-day declines of this century, triggering the seventh circuit breaker of the year, with Goldman Sachs traders publicly questioning: When will the sell-off finally stop?

On Monday, the Korea Composite Stock Price Index fell nearly 9% that day, marking the third-largest single-day drop since the Lehman crisis, closing below the critical support level of 6800 points, a cumulative retreat of 27% from the historical high established in early June.

The seventh circuit breaker of the year was triggered that day, making up over half of the 13 all-market trading suspensions since the circuit breaker mechanism was established in 2000.

This drop was primarily led by two companies crucial to the Korean market. Samsung Electronics plummeted 10.7%, while SK Hynix fell 15.4%, recording the largest drop in history, down 40% from the historic high just weeks earlier.

Goldman Sachs trader Heejae Lee admitted in a report that day:

To date, we have not heard a convincing explanation for the true fundamental catalysts behind this round of selling.

Leverage ETFs Forced Liquidation, Amplifying Declines

One of the key driving forces behind the extreme intraday volatility that day was the rapid deleveraging of recently listed single-stock leveraged ETFs.

The leveraged products related to semiconductors fell over 30% that day, forcibly undergoing large-scale re-hedging, which further accelerated the downward spiral. The 3x leveraged Korean ETF has now dropped 65% from its historical high on June 1.

Goldman estimates that forced liquidation of these products accounted for 62% of the total net selling by local institutions that day.

The regulatory body promptly responded. Lee Chan-jin, the head of the Financial Supervisory Service of Korea, met with the CEOs of 20 major asset management companies that day to express strong concerns about the systemic risk and "overheating" marketing of these products, calling for enhanced investor protection.

Reports indicate that the regulatory focus is expected to be on raising the entry threshold for these products rather than an outright ban.

Foreign and Institutional Investors Team Up to Exit, Retail Investors Exhausted

Goldman’s block trading desk observed that institutional block trading activity was relatively quiet that day, with momentum hedge funds selectively reducing their positions, while long-term institutions mostly remained on the sidelines.

In terms of funds, foreign and local institutions net sold a total of $1.13 billion and $1.5 billion, respectively, that day. Local institutions’ selling was highly concentrated on ETF liquidation, while foreign selling almost entirely came from quantitative trading, with a quantitative net outflow of $1.18 billion.

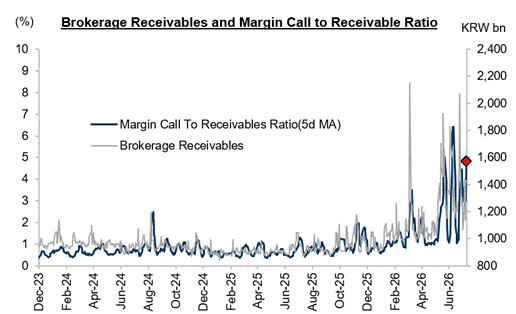

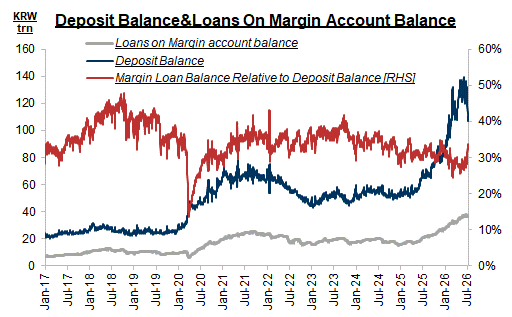

What is even more concerning is that retail funding, which has been the last support for Korean stocks, is rapidly reaching its limit. Goldman data shows that the margin call ratio for retail investors had risen to 5% as of last Friday, and considering Monday's decline, Monday's figure will be significantly higher.

According to the Korea Financial Supervisory Service, as of July 13, over 1.2 million leveraged retail accounts in the Korean market had received margin call notices, with approximately 320,000 to 360,000 accounts already forcibly liquidated by brokers, with the principal wiped out, and some accounts even showing negative balances.

Additionally, as of July 9, the balance of retail brokerage margin deposits had dropped to 107.1 trillion won, a decline of about 30 trillion won from 132.47 trillion won on June 29, marking the lowest level since February 2020.

Goldman points out that once retail investors' willingness to "buy high and sell low" is completely exhausted, the real bottom for the KOSPI may yet to come.

Fundamental Divergence: Institutions Bullish, Funds Voting with Their Feet

Monday's sharp decline sharply contrasted with the feedback collected by Goldman during its roadshow in Singapore last week.

At that time, the mainstream view among institutional investors was that the recent adjustment had significantly improved the risk-return ratio, and they leaned towards re-establishing exposure to memory chips. However, the market responded with a starkly different outcome of a 9% drop in a single day.

The bullish camp is supported by structural factors of equipment capacity shortages, expecting industry capacity expansion to be delayed until the second half of 2028.

A minority of bears expressed concerns about downward average selling prices (ASP) in the fourth quarter of 2026 and that the HBM4 cycle may have peaked.

Korea Investment & Securities previously released a report predicting that SK Hynix's operating profit would reach 60.4 trillion won, a year-on-year increase of 556%, but 8% lower than the market consensus of about 65 trillion won, citing that the high proportion of HBM revenue led to ASP increases falling below the market average level.

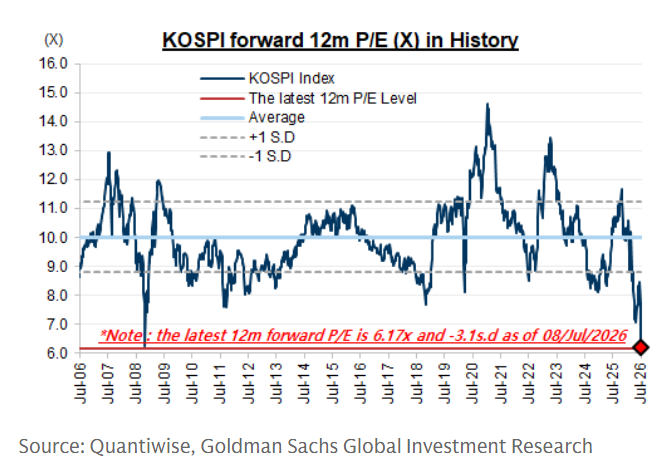

It is worth noting that although the Korea Composite Stock Index has significantly corrected, forward earnings per share expectations continue to be downgraded, largely due to overly optimistic earnings forecasts for memory stocks previously.

Technical Levels at a Critical Juncture, Goldman Remains Cautiously Optimistic

In light of the above analysis, Goldman characterizes this round of KOSPI decline as a "liquidity-driven position clean-up."

From a technical perspective, the KOSPI closed just at the 6800-point support level, which is the 52-week Fibonacci retracement level. If that support fails, the next support level will be at 6500 points, indicating a potential further drop of 4.5%.

Lee cited historical data showing that the maximum decline of the KOSPI over the past five years was about 30%, noting that the current -25% drop is "already quite close."

Goldman recommends that investors use the current extreme volatility to selectively buy high-conviction memory chips and tech stocks at deep discounts.

However, Goldman also acknowledges that the market still faces multiple headwinds in the short term.

First is the seasonal trend. The Korea Composite Stock Index has historically shown weak performance in the third quarter. If the first half shows a considerable rise, the third quarter naturally becomes a window for institutions to lock in profits, rebalance portfolios, and rotate into defensive sectors.

Secondly, there is the issue of financing costs. The financing loans available in the Korean banking sector to retail investors are nearing their limits, and although swap financing costs have slightly declined from their peak, they remain high, with prime brokers actively reducing inventory and risk exposure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。