TL;DR

- Goldman Sachs maintains a buy rating for Microsoft with a target price of $610, implying about 59% upside based on the stock price as of July 9.

- Azure growth remains the main focus of the earnings report, with Goldman Sachs expecting a growth rate of 40%-41% in the fourth quarter, higher than the company's previous guidance.

- Higher capital expenditures will amplify the controversy over return rates, with Copilot charges, Maia chips, and new capacity releases still awaiting realization.

Goldman Sachs maintained a buy rating for Microsoft ahead of the company's fourth-quarter earnings report on July 29, setting a 12-month target price of $610 and upgrading its long-term capital expenditure expectations. For investors, the focus of the earnings report is not whether Microsoft is an AI winner, but whether Azure can sustain high growth amidst continued increases in computing power, converting higher data center, chip, and power investments into revenue rather than dragging down free cash flow and profit margins.

The $610 Target Price Depends on Azure Exceeding Expectations

As of July 9 UTC, Microsoft’s stock price was approximately $383.34. Based on this price, the $610 target price corresponds to a potential upside of about 59.1%.

This calculation is based on several conditions: ongoing high growth in cloud demand, new data center capacity coming online as planned, no cannibalization between Microsoft’s internal AI R&D and external customer computing power allocation, and clearer revenue and profit contributions from AI products like Copilot.

Azure remains the primary focus of the earnings report.

Microsoft's FY26 Q3 official conference call revealed that Azure and other cloud services revenue grew by 40% year-over-year and 39% at constant currency. The company previously provided guidance for FY26 Q4 growth of 39%-40% at constant currency, noting that customer demand still exceeds available capacity.

Goldman Sachs reports that Azure's constant currency year-over-year growth in the fourth quarter is expected to reach 40%-41%, and guidance for the next quarter may also remain at 40%-41%. This forecast is slightly higher than the company's previous guidance, but market expectations are already high. If Microsoft merely meets high expectations for cloud growth, the stock price may not continue to support further AI investments.

Microsoft also needs to explain where the growth is coming from. It could be from new data center capacity being released, continued expansion of enterprise AI demand, or smoother allocation of computing power between internal applications and external customers.

In recent quarters, the constraint on Microsoft’s AI business has not been insufficient demand but tight supply. Azure must serve external customers like OpenAI while supporting Microsoft’s internal Copilot, MAI model development, and first-party applications. When computing power is tight, cloud growth is limited by delivery capability. If capacity is released too slowly, capital expenditure will first impact cash flow and depreciation pressures.

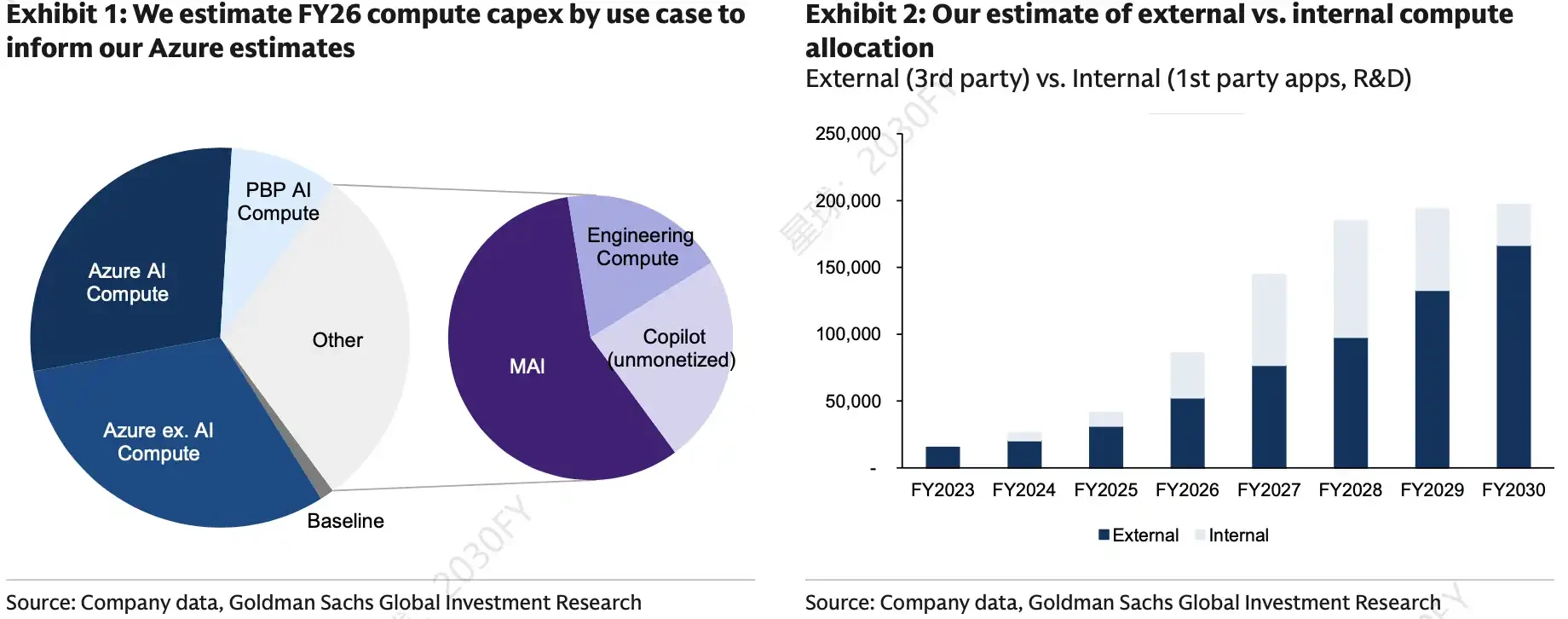

Microsoft FY26 computing capacity expenditures split by use and external/internal computing power allocation. AI computing, MAI, Copilot, etc., account for a significant proportion, and internal computing power investment tends to stabilize after a rise in the past 12 months, which is key to assessing whether Azure can support both customer demand and internal AI R&D.

Capital Expenditures Continue to Be Revised Upward, AI Computing Competition Shows No Signs of Cooling

Microsoft has signaled higher investments. FY26 Q3 capital expenditures were $31.9 billion, with the company guiding Q4 capital expenditures to exceed $40 billion, and expecting around $190 billion in capital expenditures for the 2026 calendar year, of which about $25 billion will come from higher component prices.

Goldman Sachs reports that Microsoft’s capital expenditure expectations for the fiscal years 2028-2030 have been revised up by about 10%. According to the report’s calculations, the adjusted annual capital expenditure assumptions are above the market consensus, reflecting a more aggressive judgment on Microsoft’s future computing power investments.

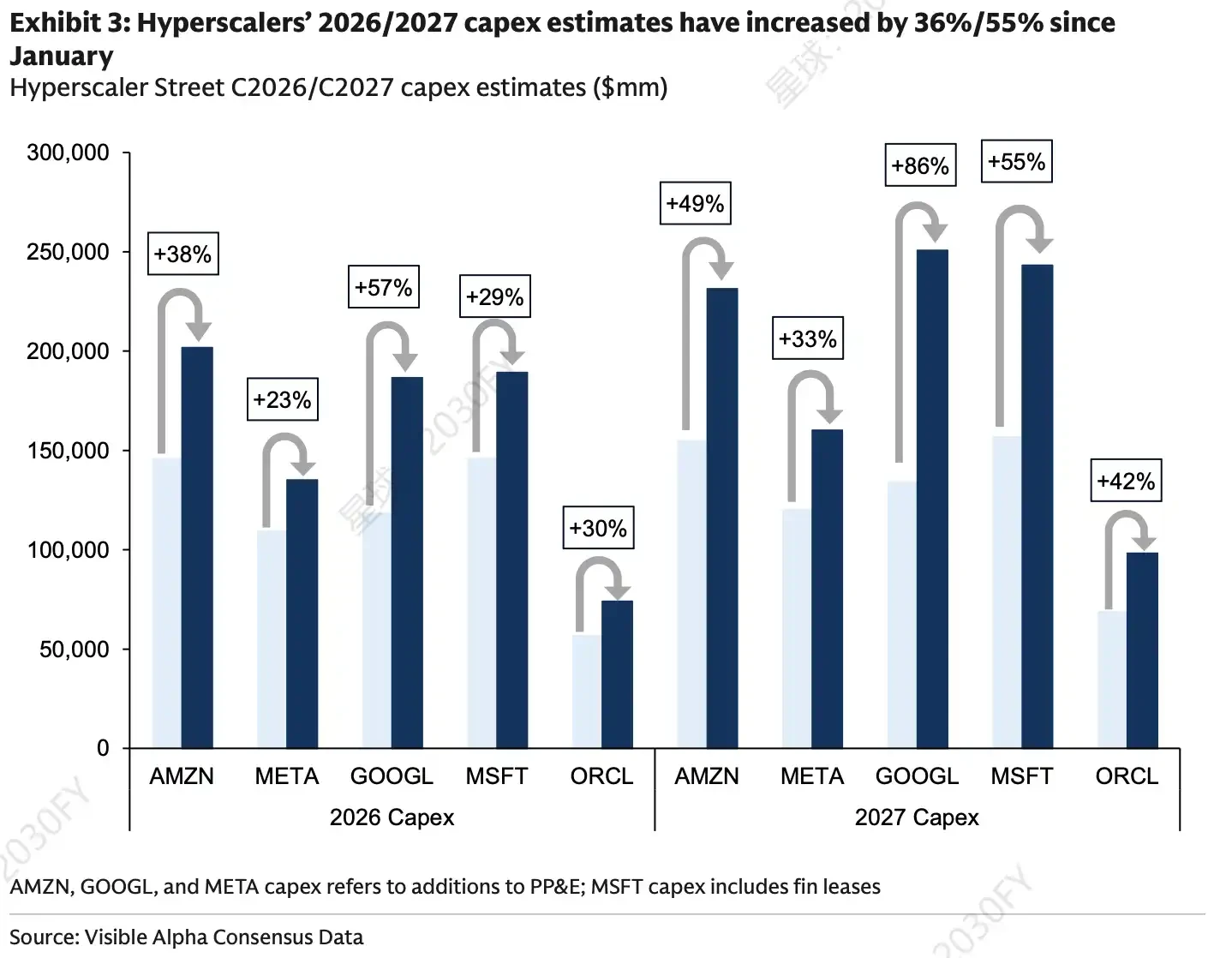

This is not just Microsoft’s choice. Guidance from chip manufacturers like NVIDIA, Broadcom, and AMD, as well as capital actions from cloud and internet giants like Google and Meta, all indicate that demand for AI computing power has not shown obvious signs of cooling. Hyperscale cloud providers are still preparing to expand their data centers, chip, and power resources in the coming years.

For Microsoft, high investment has two sides.

On one hand, Azure and AI product cycles remain a valuation support. Goldman Sachs reports that by mid-2030, Microsoft’s computing power capacity could expand to about 40GW. On the other hand, the higher the capital expenditures, the more investors will question whether the newly added computing power can translate into cloud revenue, AI subscriptions, and higher-margin businesses rather than just leading to heavier depreciation and cash flow pressure.

Goldman Sachs also expects Microsoft’s FY26 revenue to be $329.4 billion, with an EPS of $16.75, and FY27 revenue to be $387.1 billion, with an EPS of $19.32. The implicit premise of this set of forecasts is that AI investment can drive revenue while not continuously suppressing the profit release speed.

Hyperscale cloud providers’ capital expenditure expectations for 2026/2027. Since January, capital expenditure expectations for AMZN, META, GOOGL, MSFT, and ORCL have all been significantly revised upward, with MSFT's expected growth reaching 55% for 2027.

Copilot Must Charge, Maia Must Reduce GPU Dependency

Whether Microsoft’s AI investment can work effectively ultimately relies on two key drivers: the commercialization of Copilot, and the maturity of self-developed and alternative chip supplies.

The logic behind Copilot is relatively clear. An increase in usage over the long term benefits software revenue growth and has the potential to improve profit structure. However, the short-term issue is that usage itself does not equate to revenue realization.

Microsoft disclosed in FY26 Q3 that M365 Copilot paid seats have exceeded 20 million. GitHub Copilot is also shifting toward more usage and value pricing. The company has also introduced fair usage clauses for high-usage scenarios, attempting to more closely bind higher reasoning costs and the payment mechanism.

The market is not only looking at the continued increase in seat numbers but also user engagement, renewal willingness, and actual payment expansion on the enterprise side. If the Copilot user experience and commercialization pace cannot improve in sync, the payoff from high-margin AI software will be delayed.

Chips and the supply chain are another line of focus. Microsoft’s self-developed AI chip Maia is still in catch-up mode, with maturity lagging behind some peers. Improvements to Maia 300, production progress from AMD as a secondary source, and memory procurement costs will all affect Microsoft’s ability to reduce reliance on external GPU supply chains.

The company has previously mentioned that new supplies need to be balanced between Azure, first-party applications, R&D, and server replacements. If new supply releases smoothly, Microsoft can provide more computing power to external Azure customers while continuing to invest in internal AI R&D. If the release is uneven, Azure growth, internal model training, and Copilot inference demand will still squeeze each other.

Xbox Restructuring is Just a Valuation Edge

Apart from the AI main line, Goldman Sachs also estimated the value of Microsoft’s gaming business at about $30 billion using the SOTP method.

On July 6, Microsoft announced a restructuring of its Xbox business. Multiple media reports indicated that Microsoft laid off about 4,800 employees, with approximately 1,600 from Xbox immediately terminated and about 3,200 more in FY27. Four studios—Compulsion, Double Fine, Ninja Theory, and Undead Labs—are leaving the Xbox management system, and the company reportedly streamlined part of its management.

This part feels more like a structural adjustment rather than a core trading theme in the earnings report. Microsoft’s gaming business still holds value, and the restructuring also shows the company is cleaning up inefficient assets and shrinking some non-core investments, but it is unlikely to short-term replace the returns from Azure, Copilot, and AI capital expenditures, becoming a primary factor in explaining stock price direction.

According to Goldman Sachs' SOTP valuation report, Intelligent Cloud remains the largest contributor to Microsoft’s enterprise value. The M365 business and consumer segment has an implied enterprise value of about $492 billion, corresponding to about 4 times EV/sales or 6 times GAAP EBIT for 2027, incorporating certain assumptions about demediated risks.

Whether the $610 Can Be Realized Depends on Three Things

This earnings report outlook remains optimistic: Microsoft is in a favorable position for AI computing power, Copilot, and orchestration layers, with the opportunity to continue benefiting from the AI product cycle. However, the realization of the $610 target price depends on whether the earnings report and conference call can provide more verifiable progress.

Azure needs to continue delivering high growth and explain whether new capacity coming online can support external customer demand. If growth only meets the already high market expectations, higher capital expenditures may instead become a point of contention.

Maia 300 and AMD’s secondary source need to provide clearer progress. Supply chain tightness, rising memory costs, and insufficient chip maturity will all impact the unit economics of Microsoft’s AI investments.

Copilot must prove its actual charging capability. Over 20 million paid seats is just a starting point; expansion of enterprise-side payments, usage-based billing, and user feedback will determine whether it can transition from an AI entry point to a profit source.

The point of interest in Microsoft's earnings report is not whether AI investments will continue, but whether higher investments can be converted into faster Azure growth, AI software revenue, and sustainable profit margins. If these pieces of evidence remain insufficient, the controversy over capital expenditure returns will continue to weigh on the stock price.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。