Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

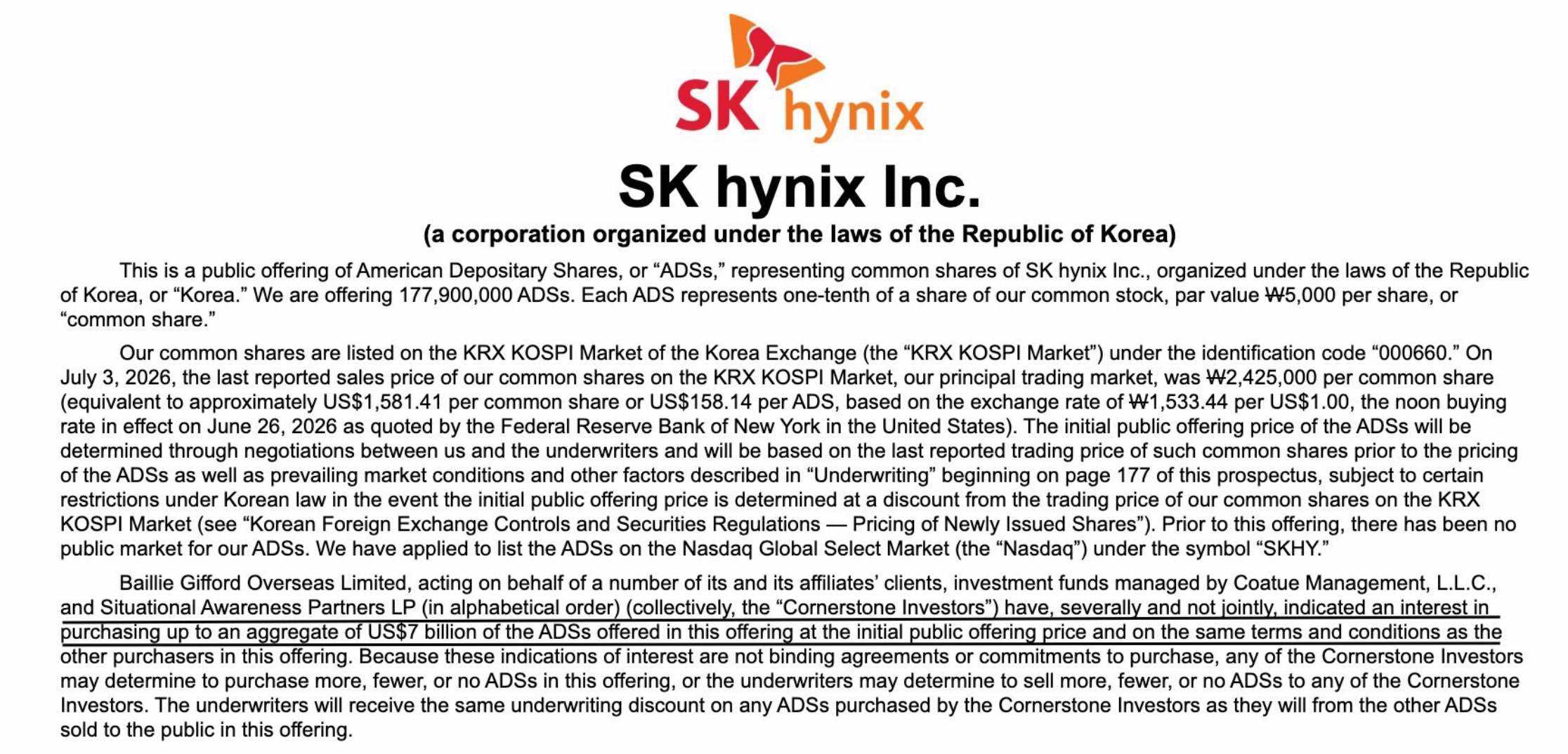

This morning, Bloomberg cited sources saying that the subscription multiple for the American Depositary Receipts (ADR) issued by South Korean semiconductor giant SK Hynix has exceeded seven times, likely becoming the largest foreign listing project in U.S. history.

Previously, at the end of June, SK Hynix had submitted its F-1 prospectus to the U.S. SEC, planning to issue 177.9 million ADRs to land on Nasdaq (each ADR corresponds to one-tenth of a common share), which based on the closing price of the Korean market on Wednesday of 2,076,000 Korean won (approximately $1,380), is expected to raise around $24.5 billion. The funds raised will be used entirely for the expansion of domestic production capacity in Korea, including the Yongin wafer fab, the Cheongju advanced packaging line, as well as investments in EUV and related equipment.

As SK goes to the U.S., the semiconductor sector is in a deep squat

While SK Hynix is set to go public in the U.S., the entire semiconductor sector is undergoing a sharp correction.

Over the past two years, investments in AI infrastructure have been the core driving force behind the growth of the semiconductor sector. Benefiting from the continued capital expenditure expansions by tech giants like Microsoft, Google, Meta, and Amazon, the industry chain represented by GPUs, HBM storage, and advanced process equipment has seen explosive performance and driven stock prices to rise.

However, recently the market has begun to reassess the sustainability of this logic. First, it was reported that Meta plans to sell some idle computing power resources, which the market interpreted as a signal from tech giants to optimize AI infrastructure investments. Subsequently, the world’s largest planned data center project by Blackstone was also canceled, further reinforcing market concerns about the slowing growth of data center demand.

These events are not entirely equivalent to the end of the “AI investment cycle," but they triggered a re-pricing of a key question in the market — after hundreds of billions of dollars in capital investment, can tech giants maintain the current growth rate of AI capital expenditure?

As a result, the AI industry chain has faced significant pressure recently. From chips and storage to semiconductor equipment, the market trading logic has begun to shift from “unlimited demand growth” to “can future growth still be realized.” SK Hynix’s stock price has also seen a notable correction, falling from a high of 2,917,000 Korean won on June 25 to the closing price of 2,076,000 Korean won yesterday, with a maximum drawdown of nearly 30%.

Secondary markets are under pressure, but primary markets are extremely crazy

Interestingly, amid the ongoing adjustments in the secondary market, SK Hynix's U.S. listing has received far more funding support than expected.

As mentioned earlier, the subscription multiple for this ADR issuance has exceeded seven times, with strong enthusiasm from institutions. According to the information disclosed in SK Hynix’s roadshow materials, this subscription demand primarily comes from various types of institutions like global long-term funds, tech-themed funds, sovereign wealth funds, and Asian thematic investors, among which Baillie Gifford, Coatue Management, and Situational Awareness Partners have expressed a combined subscription intention of about $7 billion.

Notably, Situational Awareness is a fund controlled by the newly emerging “AI stock god” Leopold Aschenbrenner, which has been one of the most explosive funds in this AI cycle. For more details, refer to "SBF’s little brother turned $225 million into $5.5 billion in one year" and "A quick look at the latest layout of the 24-year-old “AI stock god”: 60% positioning to hedge semiconductor downturn.”

The enthusiasm from institutions suggests that, at least from a long-term funding perspective, the market has not completely dismissed the AI infrastructure investment cycle. In fact, the recent correction in the semiconductor sector is primarily a valuation and expectation adjustment rather than a reversal of the industry fundamentals. Investors are concerned about whether future capital expenditure growth will slow down, rather than whether core products like HBM and AI chips are losing demand.

Additionally, it is worth mentioning that there has been speculation circulating in the market regarding the timing of SK Hynix's listing: before landing on Nasdaq, the stock price underwent a notable adjustment, perhaps to perform better post-listing, benefiting the company, underwriters, institutions, and retail investors alike…

This logic may not be completely verifiable, but on a trading level, it could indeed strengthen the market's optimistic expectations for post-IPO performance — for the issuer, a lower valuation starting point is conducive to price performance after the listing; for subscribing institutions, it also means greater potential for price appreciation.

Thus, SK Hynix's U.S. listing is likely to become an important turning point in the semiconductor market sentiment in the short term.

The real reversal signal lies in the next answer sheet from tech giants

However, the excitement surrounding SK Hynix's U.S. IPO alone seems insufficient to fully answer whether the adjustment in the semiconductor sector has ended.

From an industrial cycle perspective, the current core dispute in the market is not whether AI demand still exists, but whether tech giants can continue to maintain the current scale of capital input. Over the past two years, companies like Microsoft, Google, Meta, and Amazon have been ramping up investments in AI infrastructure, pushing global data center investments into a phase of rapid expansion. According to the plans previously announced by major tech giants, AI-related capital expenditure is expected to remain high in the coming years.

However, simultaneously, as the scale of investment continues to grow, investors are becoming increasingly concerned about “when will these huge capital investments be able to translate into actual commercial returns?”

If AI application growth can match infrastructure investments, then the current adjustment in the semiconductor sector is more like a valuation digestion after a rise; but if tech giants begin to slow down data center construction and reduce GPU procurement pace, then the previously granted high growth expectations for the AI industry chain will face re-adjustment. Therefore, the financial reports of tech giants in the next few quarters will become crucial in judging the direction of the semiconductor market.

In other words, while SK Hynix's listing may serve as a catalyst for short-term sentiment in the semiconductor sector, what truly determines whether the AI cycle can continue are the clear answers from tech giants like Microsoft, Google, Meta, and Amazon regarding their future capital expenditure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。