Written by: Rita

Trend Guide

J.P. Morgan's Asia-Pacific Technology Sales Trading Brief on July 8 covers core topics such as Samsung Electronics, TSMC, Japanese semiconductor equipment, and passive components. Samsung's Q2 profit is strong but faces short-term pressure from leveraged ETF liquidations; TSMC's A14 process certification becomes a key catalyst for the device chain; MLCC might face shortages by 2027; and the substitution of ABF substrates for BT is becoming an industry trend. This brief comes from the sales trading department and is not an official research report, but it provides important reference value for understanding the global semiconductor cycle position and key variables.

Samsung Electronics: Strong Profits but Short-Term Pressure

Samsung Electronics' preliminary profit for Q2 2026 is 89.4 trillion won, a 1810% year-over-year increase, reaching a record high. However, investor models indicate that market expectations range from 95 to 100 trillion won, which suggests that the surface-level "outperformance" sentiment may be closer to "in line with expectations but not enough surprise."

Feedback from J.P. Morgan's sales trading department shows that the market is concerned about two short-term issues. First, Korean retail investors are clearing out leveraged ETF positions, with Samsung's 30-day volatility rising to 107 and Kioxia climbing to 127, limiting the ability of fund managers to re-leverage. Second, employee bonus provisions are around 15 trillion won, covering two quarters in the first half of 2026, with the market awaiting clear guidance after the full financial report disclosure on July 30.

However, J.P. Morgan remains optimistic about the memory cycle. NAND pricing may exceed market expectations (quarter-over-quarter growth of 20%), mainly driven by demand for enterprise-grade SSDs purchased for KV cache offload by hyperscale manufacturers. Memory manufacturers need to continue increasing capital expenditures to meet customer demand, with Tokyo Electron and Screen Holdings gaining shares from Samsung and Micron in the DRAM etching and cleaning equipment sectors.

TSMC: A14 Process Certification is a Key Catalyst

Ahead of TSMC's Q2 2026 financial report, investors are most concerned about the mass production certification timeline for the A14 process. J.P. Morgan expects this certification to be completed between late 2026 and early 2027, with Lasertec as a direct beneficiary.

In the device chain, Ebara's CMP tools have gained market share at TSMC, with investors expecting its first-quarter orders to potentially exceed expectations. Advantest and Disco are consensus choices among long-term investors, although Disco's valuation multiples are already high.

Regarding capital expenditures, investor models have factored in higher capital expenditure expectations for 2026/27, with the market expecting TSMC to provide positive guidance in its financial report to meet the backlog of customer orders.

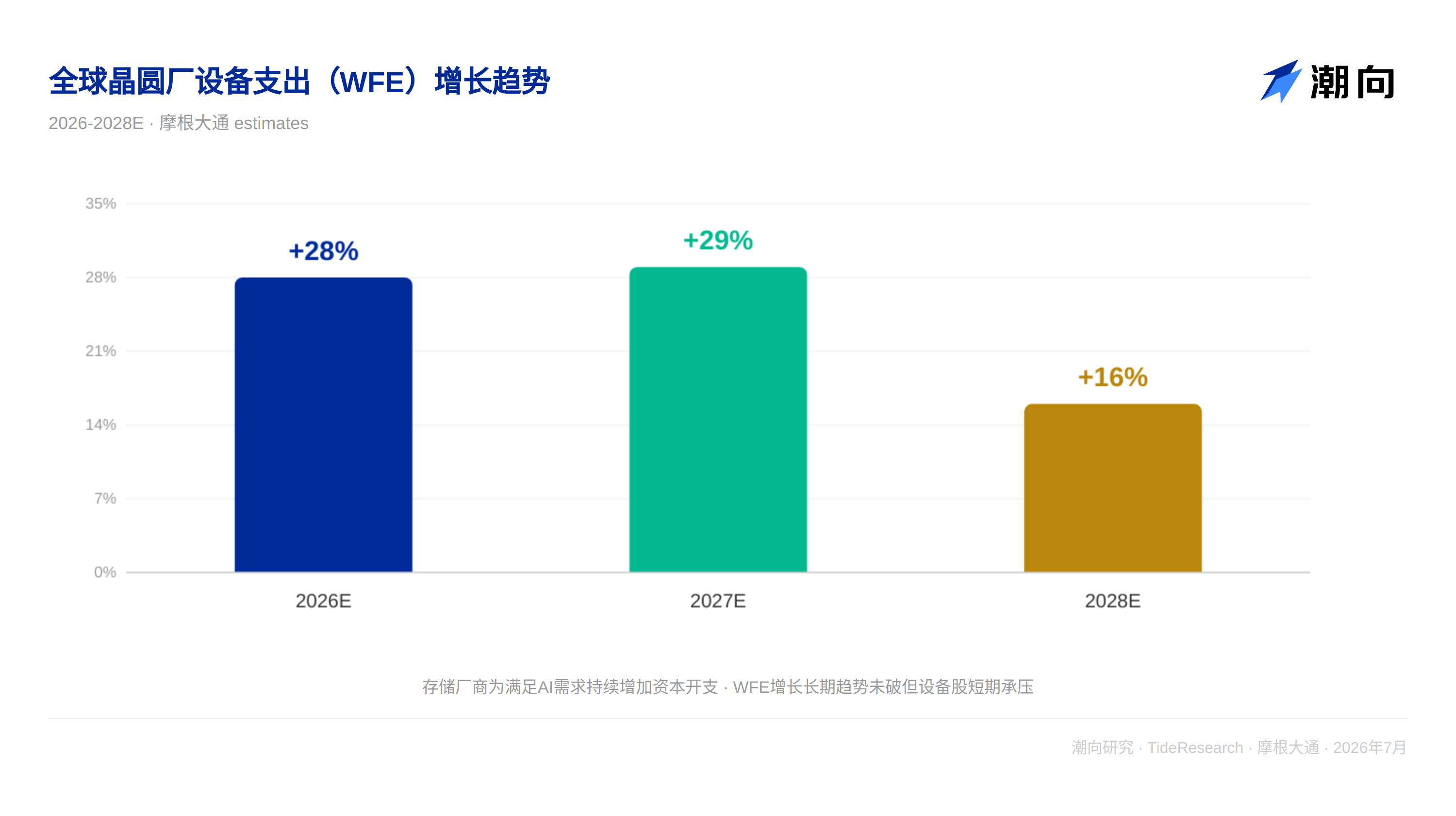

Japanese Semiconductor Equipment: Storage Cycle Position Determines Stock Price Direction

The J.P. Morgan team expects global wafer fab equipment (WFE) spending to grow 28%, 29%, and 16% in 2026-2028, respectively. Investors agree that memory manufacturers need to increase capital expenditures to meet AI demands, but semiconductor equipment stocks often perform poorly under expectations of peak memory prices.

Tokyo Electron (TEL) is a focus, with the market expecting its gross margin to reach 50% within two years. Advantest's further profit upside is driven by CPU and CPO (Co-Packaged Optics) testing demand. Nittobo benefits from the adoption of M9 and T-glass in multilayer ceramic substrates, with potential market space expanding.

MLCC: 2027 Likely to Enter a Shortage Cycle

J.P. Morgan's passive components team expects that MLCC may face shortages in 2027, with prices starting to rise during negotiations in October to December when customers realize the shortages.

Murata Manufacturing is expected to report an operating profit of 86.5 billion yen in the first quarter, but due to yen depreciation and strong market conditions, it may reach 90 billion yen or higher. Sunlord Electronics is expected to report an operating profit of 5 billion yen in the first quarter, but there is uncertainty regarding when the strike at the Korean MLCC plant will end. TDK is expected to report an operating profit of 67.4 billion yen, with anything exceeding 70 billion yen being a positive surprise.

Rohm's discrete semiconductor products are also seen as tightening in supply and demand.

Substrates: BT Exiting ABF Becomes a Trend

Supply chain checks show that several Asian substrate suppliers are planning to convert BT substrate capacity to ABF substrates. Both revenue and profit margins for ABF substrates are significantly higher than for BT, and the conversion will result in net positive benefits.

Xinquan Electronics plans to cease half of its BT substrate production by 2028 and may eventually exit completely. This trend presents clear incremental demand for ABF substrate equipment suppliers and material vendors.

Trend Perspective

The most valuable point of this sales trading brief is not what it says, but that it captures what the market is currently thinking. Samsung faces short-term pressure, but the cycle direction hasn’t changed; TSMC's A14 certification is the next step for the device chain; and the potential shortage of MLCC may materialize in 2027. These are the marginal variables that the market is pricing in.

However, there is one judgment worth pursuing separately: If NAND pricing indeed exceeds expectations with a quarter-over-quarter increase of +20%, is Samsung's short-term volatility a buying window magnified by sentiment? The liquidation of leveraged ETFs is a trading structural issue, not a fundamental one. The direction of the memory cycle remains unchanged, while the market is being forced to reduce positions due to rising volatility, presenting a reflexive opportunity.

For investors, the real value of this brief lies in breaking down the global semiconductor cycle into three layers: the upstream equipment (WFE growth), the midstream manufacturing (TSMC A14), and the downstream terminal demand (MLCC shortages). The device chain looks at domestic substitution, the manufacturing chain focuses on breakthroughs in advanced processes, and the terminal examines the spillover of passive components. The driving factors of the three-layer logic are different, but the time windows are synchronously narrowing.

Disclaimer

This article is a compilation and interpretation of the third-party broker sales trading brief (J.P. Morgan, July 8, 2026) by Trend Research. The ratings, target prices, earnings forecasts, and related judgments quoted in the text represent the views of the analysts of that brokerage, reflecting their institutional position, and do not represent the views of Trend Research, nor do they constitute any investment advice.

The market carries risks, and decisions should be made independently. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。