TL;DR

- Morgan Stanley raises its price forecast for various types of memory in Q3 2026, while warning that the momentum of memory stocks may weaken in the short term.

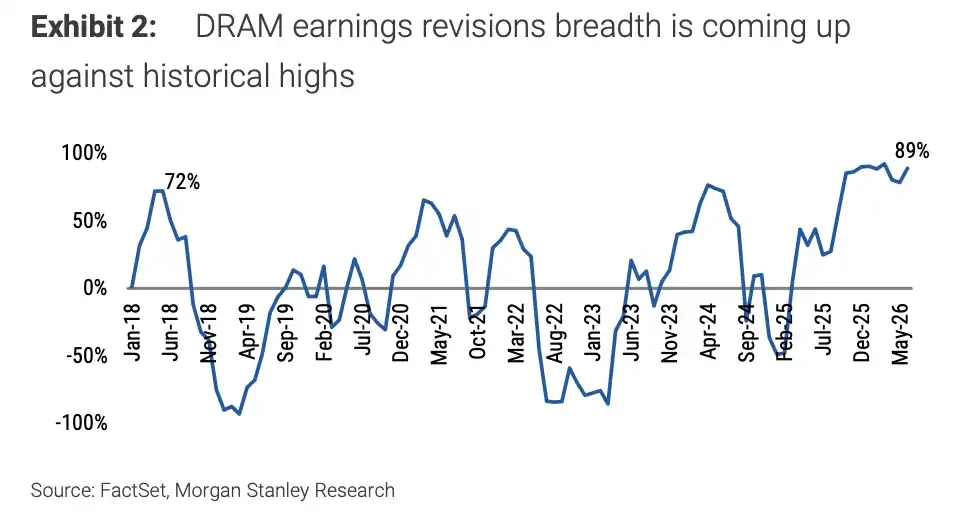

- Under this report's criteria, the price increase expectation for PC DRAM rises to 15-20%, with the breadth of DRAM earnings revision approaching 89%.

- Samsung and SK Hynix continue to be supported by AI demand, but financial report guidance, LTA, and capital expenditure statements will affect the continuation of the rally.

Morgan Stanley significantly raised its Q3 memory price forecasts in a research report on July 7, but at the same time warned that memory stocks might face short-term correction pressure.

This is not a shift to a bearish memory cycle. The report maintains an "attractive" stance on the South Korean technology sector, continuing to favor Samsung Electronics and SK Hynix, and forecasts that the earnings of related companies will grow by over 35-40% in 2027. The real warning is that memory prices, earnings expectations, and investor positioning have already reached high levels, and stock prices may not continue to rise at the same pace as in the past few months.

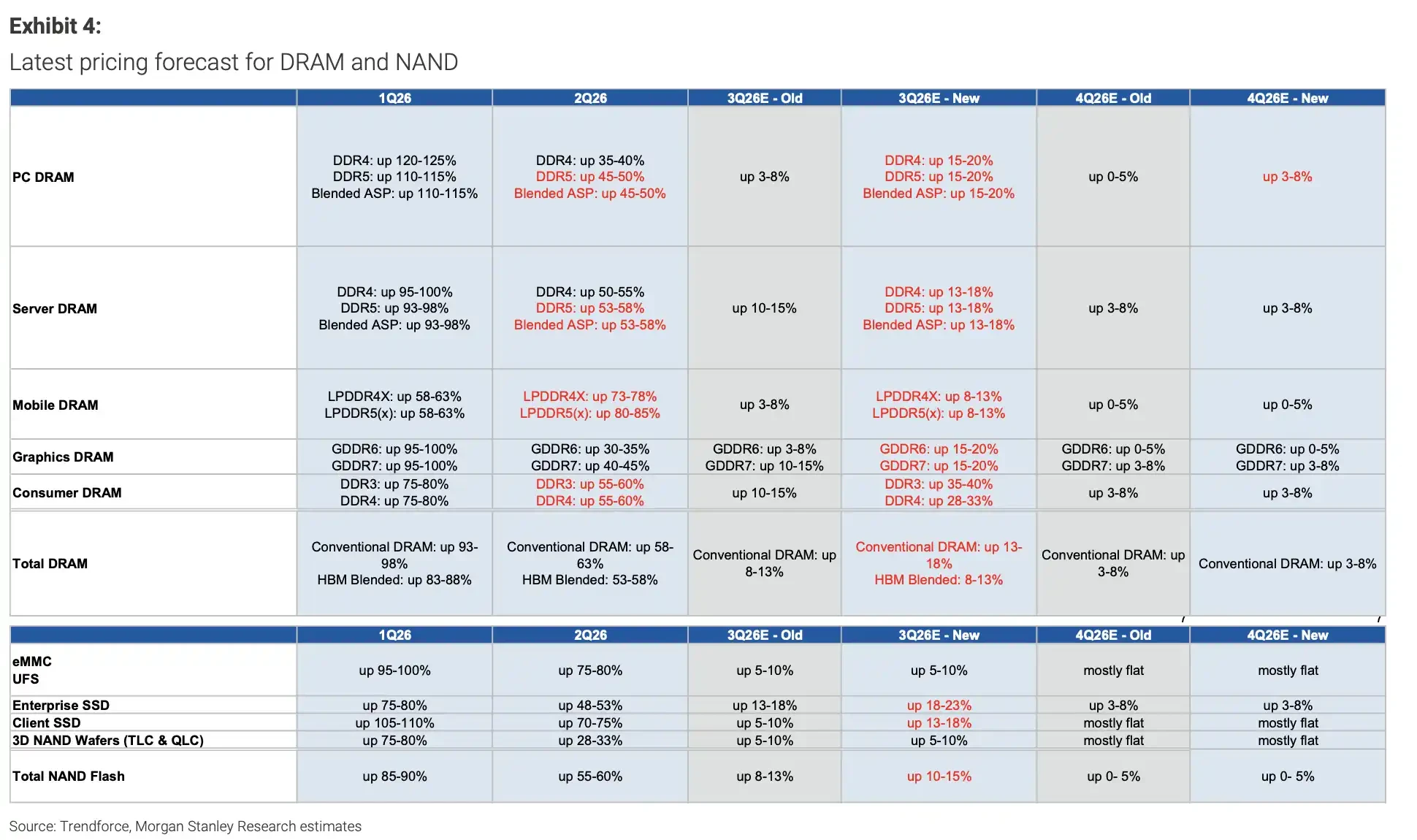

The most direct figures are the price forecasts. The report raised the sequential increase expectation for the blended ASP of PC DRAM in Q3 2026 from the previous 3-8% to 15-20%, server DRAM to 13-18%, GDDR6 and GDDR7 to 15-20%, and enterprise SSD to 18-23%.

Public price agencies also indicate a warming trend. A TrendForce article from July 3 stated that the DRAM market in Q3 2026 remains extremely tight, with contract prices expected to increase by 13%-18% sequentially, and NAND Flash contract prices expected to increase by 10%-15%. However, TrendForce also mentioned that while server DRAM remains in short supply, long-term supply agreements will slow the price increase.

Prices are still rising, but the trading difficulty for memory stocks is increasing. In Morgan Stanley's report criteria, the breadth of DRAM earnings revision has recently approached 89%, nearing historical highs. The memory market, driven by AI capital expenditures, HBM, and server demand over the past two years, has already reflected many positive outcomes in stock prices ahead of time.

The most substantial price hikes are expected in the third quarter, and concerns are also concentrated in this quarter

This round of price hikes covers a wide range. In addition to PC DRAM, the price expectations for server DRAM, graphic DRAM, general DRAM, and enterprise SSD in Q3 2026 have all been significantly raised. Among them, the 15-20% increase in PC DRAM and graphic DRAM is the most easily recognized price signal by the market. The 18-23% increase in enterprise SSD indicates that the price rise in storage is not only concentrated in AI server-related categories.

The problem also exists here. The faster the price expectations are raised, the more likely stock prices are to enter a "good news realization" phase.

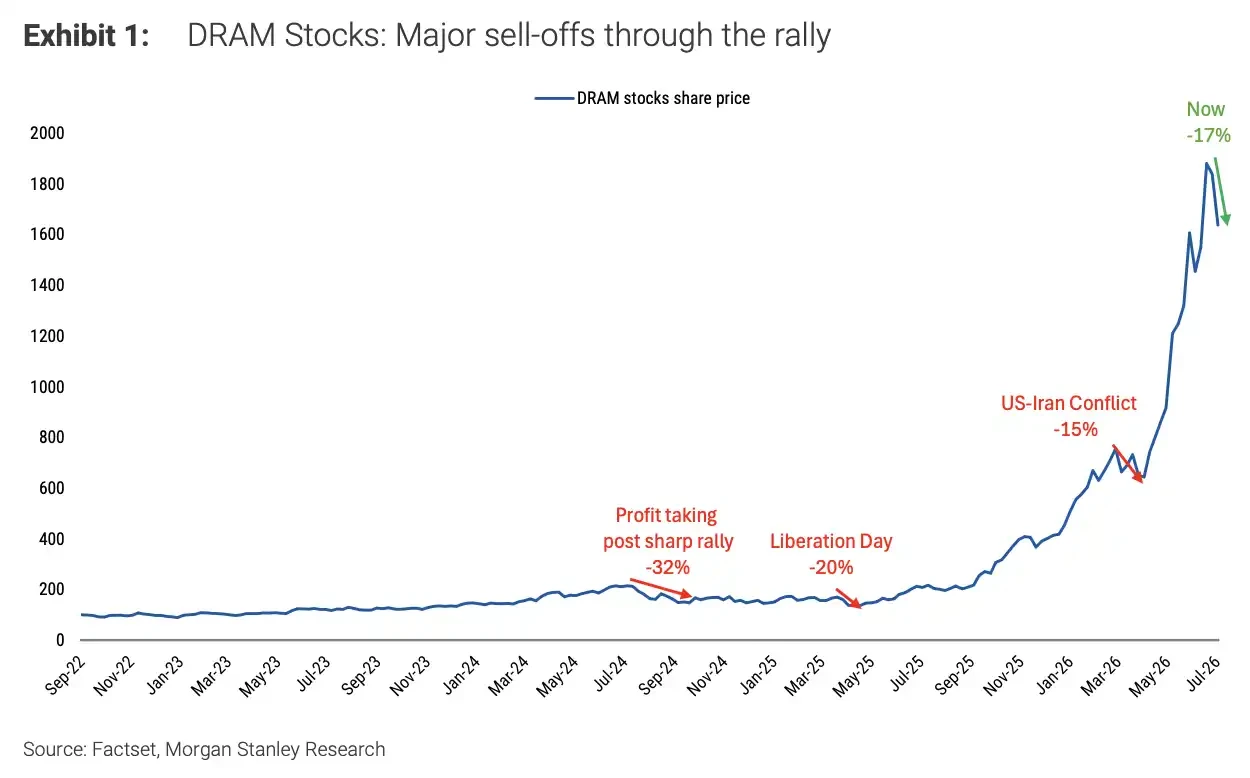

Memory stocks have not been without adjustments over the past two years. Statistics from Morgan Stanley show that since the generative AI wave began in November 2022, DRAM-related stocks have experienced three significant corrections, including profit realization, specific event impacts, and prolonged adjustments lasting several weeks. Each correction has not interrupted the long-term trend driven by AI capital expenditures, but they remind investors that even in a strong cycle, substantial phase declines can happen.

The three main corrections in DRAM stocks were approximately -25%, -25%, and -35%, but overall, they still rose from the 2022 low to a new high in 2026.

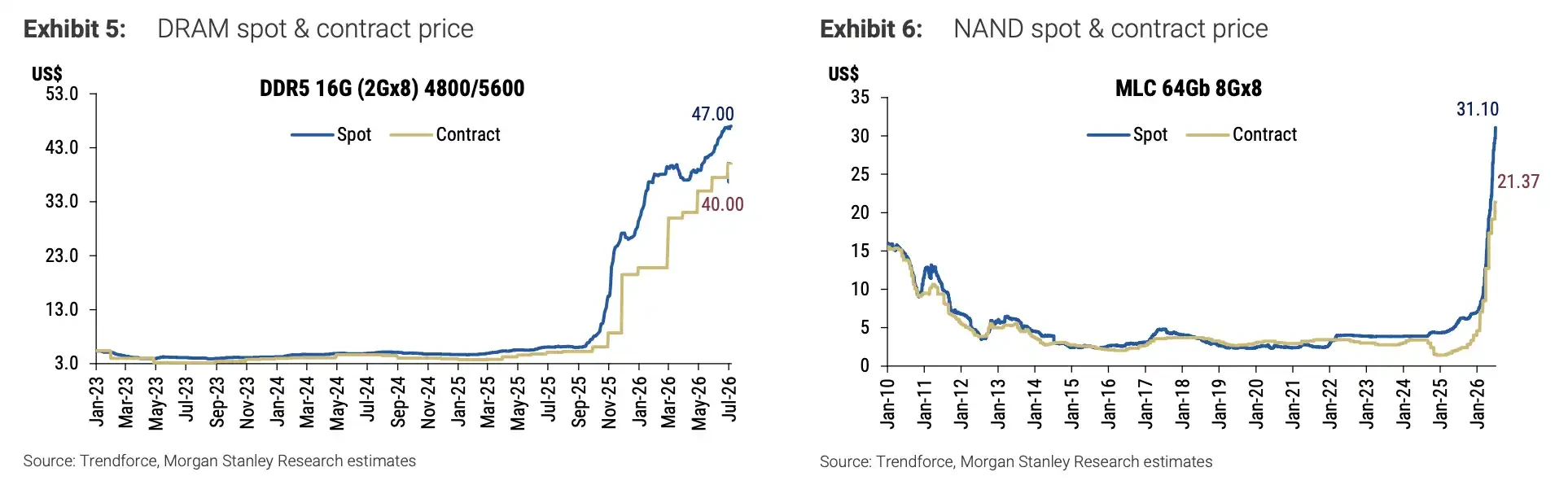

Spot prices are also supporting the price increase logic. The price tracking provided in the report shows that DRAM spot prices have surged rapidly since early 2025, and NAND spot prices have recently rebounded significantly from their lows; contract prices, though lagging, are also trending upward. This means that the short-term correction signal is not due to deteriorating prices, but rather because prices and expectations have risen too quickly.

The spot price of DDR5 16Gb has risen to around $47, while the spot price of MLC 64Gb NAND recently rose to $31.10.

Earnings revisions are nearing highs; memory stocks need to digest expectations

For stocks, what matters more than the price itself is how much upward revision potential remains.

The breadth of DRAM earnings revision recently reached about 89%, which is near historical highs. This indicator can be understood as an increasing number of analysts raising their earnings forecasts. Once most people have raised their earnings expectations, it becomes more challenging to continue to exceed expectations.

The breadth of DRAM earnings revision rose to about 89% after 2025, nearing historical peak ranges.

This is also one of the reasons why short-term momentum may weaken. Memory stocks are not without fundamental support; rather, the confluence of rising prices, upward earnings revisions, crowded capital positions, and AI chain sentiment has stacked together. If financial report guidance is not strong enough, capital expenditure statements are not sufficiently aggressive, or if major cloud vendors’ stock prices come under pressure, the memory sector is more likely to amplify volatility.

Morgan Stanley still prefers DRAM and traditional memory with clearer capital flows and more obvious supply bottlenecks, believing they are more attractive than NAND, while being relatively less optimistic about memory module manufacturers. This ranking indicates that the market is not simply betting on "all storage prices going up," but rather looking at whether price increases can indeed translate into profits.

The price increase expectation for Q3 2026 PC DRAM was raised from 3-8% to 15-20%, and the enterprise SSD was raised to 18-23%, with price predictions for multiple DRAM types also raised.

Samsung has given guidance; SK Hynix will have to wait until the end of the month

The financial reports of the two leading memory companies in South Korea will serve as a window for the market to validate the price increase logic.

Samsung Electronics released its Q2 2026 performance guidance on July 7. The company expects sales of approximately 171 trillion won and operating profit of approximately 89.4 trillion won, with the operating profit range from 89.3 trillion to 89.5 trillion won. For Samsung, the market is not only looking at quarterly profits but is more concerned about the recovery strength of the memory business, progress of AI-related products, and whether the traditional storage price increase can continue to improve profitability.

The timing of SK Hynix's financial report still needs to be awaited. The public market calendar shows that the company is expected to release its next financial report on July 29. Given that SK Hynix has a more prominent position in HBM and AI server memory, the market will be more sensitive to its Q3 commodity memory prices, long-term supply agreements (LTA), and capital expenditure statements.

If management confirms that the commodity memory remains strong in Q3, that LTA commitments have increased, and that capital expenditures only show mild upward adjustments, the short-term correction may resemble a healthy adjustment. However, if the guidance is not strong enough or capital expenditure is interpreted as supply increasing too quickly, the market may reassess how long memory price increases can continue.

LTA itself is not without risk signals. Historically, long-term agreements do not necessarily lead to stock price increases; some agreements have been renegotiated or have turned into constraints where customers are forced to take delivery when demand changes. The market will not only look at "how many have been signed" but will also consider price, duration, customer quality, and execution flexibility.

AI demand is still there, but the market is starting to question whether there is an oversupply

The long-term bullish logic still comes from AI, especially AI agents that can execute tasks, call tools, and engage in continuous interaction. Morgan Stanley in its report expects that by 2027, the earnings of related companies will still likely grow by over 35-40%, which is why it does not equate short-term correction risks with the end of the cycle.

However, the controversy over AI demand is changing. Previously, the market was more focused on the continuous expansion of model training and inference scales, which drove up computing power and memory demand. Now, some investors are beginning to worry that after Q3, cloud vendors may emphasize token savings, inference efficiency, open-source low-cost models, and the impact of chip inflation on profit margins.

There is an even more sensitive question: whether the largest AI spenders truly have available computing power for sale, which implies that previous construction may be experiencing phase oversupply. This assertion has not yet formed a conclusive outcome, but it is enough to make the market more cautious before the financial reports of major cloud vendors.

The divergence in this round of memory market trends lies not in whether AI demand will immediately disappear, but whether price increases, upward earnings revisions, and customer capital expenditures can continue to reinforce each other. If the Q2 AI supply chain financial reports remain friendly, but Q3 guidance begins to weaken, memory stocks may first undergo a round of valuation and positioning adjustments.

The memory cycle is still under the backdrop of AI capital expenditures, but short-term trading has shifted from "how much prices have risen" to "how long these price increases can be trusted by the market." The upcoming performance communications from Samsung and SK Hynix, capital expenditure statements from cloud vendors, and LTA execution conditions will determine whether this correction is merely a pause in the bull market or the true beginning of a deceleration in the rally's speed.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。