Author: Claude, Deep Tide TechFlow

Deep Tide Overview: If you hold assets related to memory, AI hardware, or the semiconductor supply chain, Samsung Electronics' second-quarter forecast on July 7 is worth watching closely. The market collectively expects its operating profit for the quarter to be around 85.5 trillion won (approximately 55.9 billion USD), exploding approximately 18 times year-on-year, surpassing Apple and NVIDIA during the same period, setting a global record for the highest quarterly operating profit in the history of tech companies. DRAM and NAND contract prices jumped 40% to 65% in a single quarter, and Samsung is also asking for another 20% increase in DRAM for the third quarter. This round of price increases driven by AI memory shortages is pushing the pricing power of memory manufacturers to heights not seen in a decade.

Samsung Electronics will disclose its second-quarter performance forecast for 2026 on July 7, and this forecast is likely to set a new record.

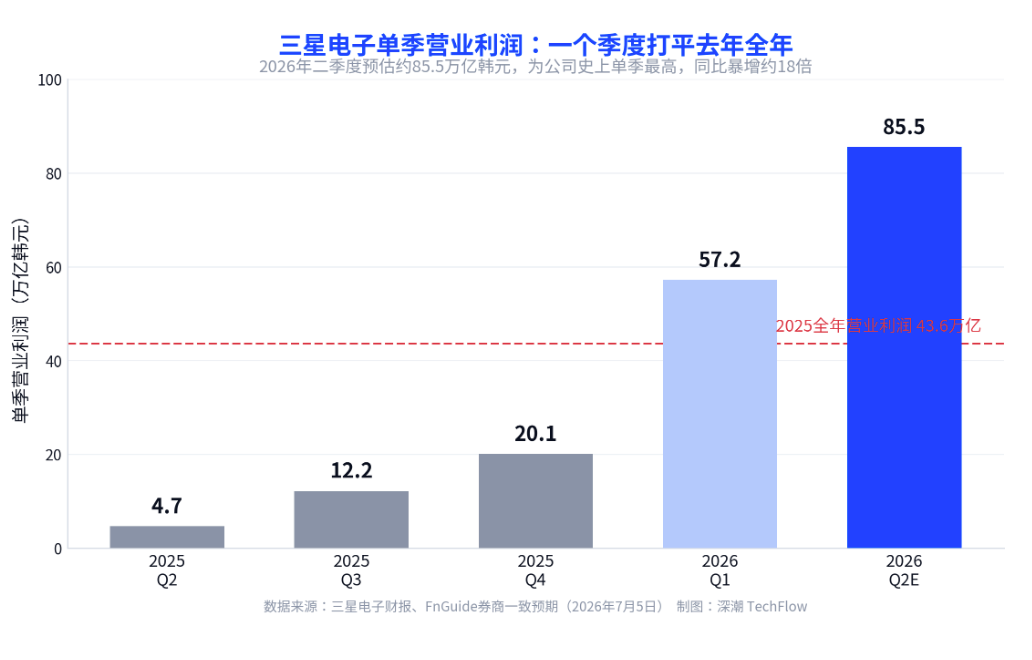

According to brokerage consensus expectations compiled by financial data provider FnGuide, Samsung's second-quarter revenue is expected to be approximately 169.4 trillion won (approximately 110.7 billion USD), with operating profit estimated at around 85.5 trillion won (approximately 55.9 billion USD). This profit represents an increase of about 18 times compared to 4.7 trillion won in the same period last year and an approximate 49.5% increase from 57.2 trillion won in the previous quarter, marking the highest quarterly operating profit since the company's establishment, surpassing Apple and NVIDIA revenue during the same period.

Looking at the year as a whole, Samsung's earnings figures for this year are even more astounding. Multiple brokerages predict that the full-year operating profit for 2026 will exceed 100 trillion won, more than double the 43.6 trillion won for 2025. Meanwhile, the 57.2 trillion won in profit for the first quarter had already exceeded the total profit for last year. For investors focused on the semiconductor cycle, the slope of this upward trend is unprecedented in the past two memory super cycles.

One quarter matches last year's entire year, profit almost entirely from chips

Samsung's profit structure has undergone fundamental changes in this cycle.

In the first quarter, 57.2 trillion won in operating profit came largely from the DS department responsible for chip business, contributing 53.7 trillion won, accounting for about 94%, and growing nearly 48 times year-on-year. The operating profit margin for the chip business exceeded 70%, which is higher than the margins of NVIDIA and TSMC during the same period. In contrast, the profits from the mobile phone and home appliance businesses shrank by nearly 40% year-on-year, almost negligible.

The driving force comes from the shortage and price increase of AI memory. Major tech companies are continually expanding their AI data centers, drawing a significant amount of memory from consumer markets such as mobile phones, PCs, and gaming consoles, thus squeezing supplies to the limit. Samsung's memory business head, Kim Jae-jun, stated in the first quarter earnings call that the company's demand fulfillment rate has dropped to an all-time low, with clients worried about supply shortages even placing orders in advance to secure production capacity for 2027. Consequently, prices surged, with contract DRAM prices rising approximately 50% quarter-on-quarter.

For holders, one point to note is that this round of price increases is a double-edged sword for Samsung. Samsung is the biggest beneficiary of upstream price hikes but also one of the biggest victims of rising costs downstream. The same price increase is recorded as profit in the chip division’s accounts but as losses in the mobile division’s accounts. The Samsung mobile business has issued an internal alert that the department may experience its first annual loss since its establishment in 2026, with the cost of core components accounting for over 40% of the overall product cost.

Behind the expectation of 85 trillion, there is a bonus variable

The consensus expectation of 85.5 trillion won is not the upper limit, as the differences among brokerages mainly focus on employee bonus provisions.

Last month, Samsung's labor and management reached an agreement to establish a special performance bonus for the semiconductor (DS) department, based on 10.5% of the department's operating profit, with the estimated provision for the first half ranging between 19 trillion and 25 trillion won. This provision directly depresses the recorded profits. Korea Investment & Securities has adjusted its operating profit estimate from 95.85 trillion won to 86.05 trillion won, while Shinhan Investment has cut its estimate from 89.86 trillion won to 82.1 trillion won.

Sohn Kyung-tae, an analyst at Shinhan Investment, pointed out that excluding the impact of bonus provisions, Samsung's actual profitability is likely to exceed the 100 trillion won threshold. In other words, the actual earnings capacity for the second quarter is higher than the 85 trillion won figure on the books, with some profits shifted to employees due to the bonus provision. For investors tracking Samsung's fundamentals, it is important to distinguish between recorded profits and operating profits after removing provisions when reviewing the forecast on July 7, as there could be a difference of tens of trillions of won.

Price increases continue, Samsung asks for another 20% increase in DRAM for the third quarter

The momentum for memory price increases has not yet peaked, which determines Samsung's profit elasticity for the next two quarters.

Contract prices for DRAM and NAND flash memory soared 40% to 65% quarter-on-quarter, and Samsung is already asking for another 20% increase in DRAM contracts for the third quarter. Consumer electronics manufacturers are resisting this round of price increases, but supply remains tight, leaving the initiative still in the hands of memory manufacturers like Samsung. Micron Technology in the U.S. has already validated the industry's profit strength, reporting an operating profit of 33.32 billion USD (approximately 51 trillion won) for the fiscal quarter ending in May, an increase of about 15.4 times year-on-year.

This round of shortages is judged by Samsung to last until 2027 or even longer. As production capacity increasingly shifts towards AI infrastructure projects, consumer electronics may be the segment most affected. For those looking to position themselves within the semiconductor supply chain, the fact that the price increase cycle has not yet ended is currently a major support. However, it is also essential to recognize that prices are at historic highs, and once investment in AI data centers slows down, the risk of price retraction from these high levels is also significant.

The divergence between stock prices and profits, what is the market worried about

Profits reach record highs, while stock prices are falling; this divergence is the most critical signal that needs to be understood currently.

Despite the second-quarter profit expectations far exceeding those of Apple and NVIDIA, Samsung's stock price has trended in the opposite direction over the past week. As of last Friday, it closed at 309,500 won, down 4.18% within the week and about 17.36% from the 52-week high of 374,500 won set on June 19. At the beginning of July, the weakening of semiconductor indicators in the U.S. triggered a global sell-off, with the Korean composite index falling nearly 8% in one day, causing Samsung and SK Hynix to be dragged into a deep correction.

There are two catalysts supporting a rebound in stock prices. One is reports that AI company Anthropic is in negotiations with Samsung to customize hardware, adding a new narrative to Samsung's chip manufacturing capabilities beyond memory. The second is that the momentum for price increases in the memory market is still ongoing. The current hesitation in the market comes more from concerns about the cycle reaching its peak; investors are waiting to see whether this record-breaking performance can dispel fears of a peak and become a turning point for emotion restoration. The U.S. Depositary Receipts (ADR) of SK Hynix will be listed on NASDAQ on July 10, with an issuance scale of about 45.5 trillion won, which is another key event this week that may affect sentiment across the entire sector.

For readers holding semiconductor assets, the events on July 7 and 10 are worth watching closely. If Samsung's actual performance confirms that profitability is still on the rise and if the guidance for the third quarter is not weak, the current stock price correction is more likely a mid-cycle adjustment rather than a peak signal. Conversely, if the performance materializes and favorable news is exhausted with stock prices continuing to weaken, caution is warranted that the market may have begun pricing the peak of this memory super cycle.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。