Is RWA in the US stock market really the savior of the cryptocurrency industry? I don't think so!

This tweet only represents my personal opinion and may not be correct. Discussion is welcome; feel free to criticize.

I expressed my views when RWA in the US stock market first appeared. Whether it is on-chain US stocks or exchange US stocks, they are essentially "pseudo-demand", with an actual ceiling that is very limited. The only true demand comes from derivatives trading of US stocks, such as contracts and options.

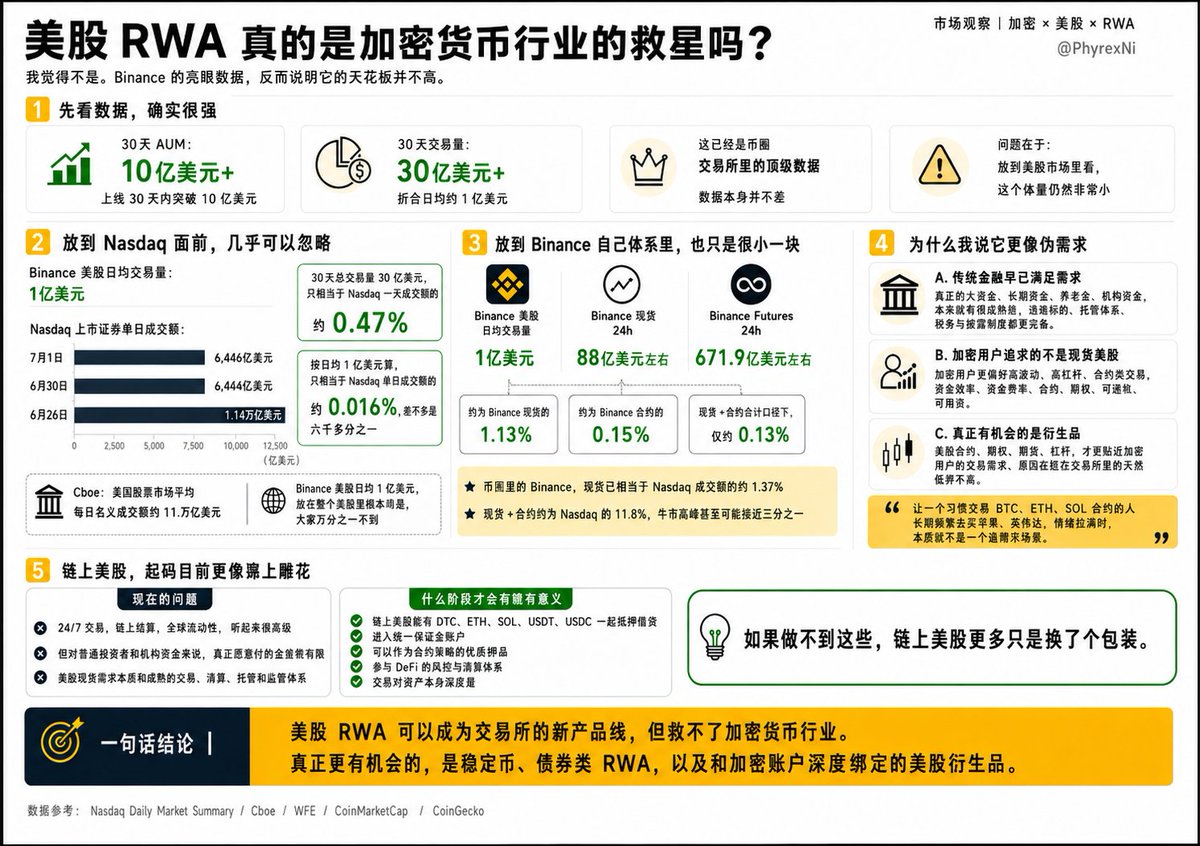

Today, I saw a chart shared by a friend on X, which reinforced my viewpoint. It is said that Binance's US stocks reached an AUM of 1 billion USD in just 30 days, and a trading volume of 3 billion USD is indeed impressive. I completely agree with this.

It is precisely because I agree that I still view RWA in US stocks as pseudo-demand. First, let’s look at the trading volume. 3 billion USD over 30 days averages about 100 million USD per day.

In comparison, the Nasdaq official Daily Market Summary shows that the single-day transaction amount for securities listed on Nasdaq across all trading venues was 644.6 billion USD on July 1, 2026, and 646.4 billion USD on June 30. It even reached 1.14 trillion USD on June 26.

This means that Binance's total trading volume over these 30 days is equivalent to only about 0.47% of the daily transaction amount for securities listed on Nasdaq. If we calculate based on the average of 100 million USD per day, it represents only about 0.016% of the daily transaction amount of Nasdaq-listed securities, which is roughly more than one six-thousandth.

Please note, I am not saying that Binance's data is poor; this is already top-tier data for cryptocurrency exchanges. What I want to say is that the real trading volume of US stocks is immense, far beyond what the cryptocurrency crowd and these volumes can compare to.

Now looking at the entire US stock market. According to Cboe's 2025 review of the US stock market, the average daily nominal transaction amount in the US stock market has reached 1.1 trillion USD. With Binance's average of 100 million USD per day, it represents less than one ten-thousandth of the entire US stock market.

The same goes for AUM. You cannot directly compare it with Nasdaq because Nasdaq is an exchange, not a brokerage account custody platform. If we look for a reference, according to WFE data, the total market capitalization of Nasdaq-US-listed companies was about 30.61 trillion USD in December 2024, while Binance's 1 billion USD AUM is merely about 0.003% of that scale.

Of course, many friends say this is just the beginning, and there is a long way to go. The data might see significant improvements in the future, and I agree with this point. However, let’s look at another set of data, which is Binance's data as a cryptocurrency exchange.

According to publicly available data, @binance's spot 24-hour trading volume on CoinMarketCap and CoinGecko is currently around 8.8 billion USD, and Binance Futures' 24-hour trading volume on CoinGecko is approximately 67.19 billion USD.

This means that Binance's average daily trading volume of 100 million USD for US stocks only accounts for about 1.13% of Binance's daily spot trading volume and about 0.15% of Binance's contract daily trading volume. When looking at spot and contracts together, it only amounts to about 0.13%.

This also has to be mentioned in the context of the current cryptocurrency bear market, where trading volumes for both spot and futures have significantly decreased compared to the bull market. Meanwhile, the US stock market is still in spring. Even so, how strong is Binance in the cryptocurrency space currently? Binance's spot trading volume is roughly 1.37% of the transaction amount for Nasdaq-listed stocks, and for spot plus contracts, it is about 11.8%.

The performance comparative in the bear market cryptocurrency exchanges is more than one-eleventh of Nasdaq's transaction volume, which is already a remarkably strong figure. If it were a bull market, this comparative value could reach one-third.

Therefore, from my perspective, the real demand for spot US stocks has long been satisfied within the traditional financial system. True large funds, long-term funds, pensions, and institutional funds already have mature channels, clearer legal rights, more complete custody systems, and more stable tax and compliance paths.

What do cryptocurrency users like? They like high volatility, high leverage, round-the-clock trading, capital efficiency, funding rates, contracts, options, the ability to collateralize, the ability to borrow, and the ability to quickly switch risk exposure.

Spot US stocks are precisely very difficult to meet these needs. Asking a user who is used to trading BTC, ETH, and SOL contracts to buy Apple, Nvidia, or Tesla spot stocks may create a novelty in the short term but is unlikely to become a long-term high-frequency trading hub.

Therefore, I have always believed that the truly promising part of RWA in US stocks lies in US stock derivatives.

The contracts, options, futures, and leverage of US stocks are what investors favor more now, allowing you to choose 20 times leverage on Micron or 20 times leverage on altcoins; most people would likely choose the former. If the volatility is not enough, leverage compensates!

So, the actual business of US stock spot in exchanges is not one with a very high ceiling; even in the long term, the contribution it can provide is very limited. This kind of demand is also "pseudo-demand"!

As for on-chain US stock spots, in my view, they currently resemble ornamental designs on excrement. It sounds sophisticated, with concepts like 24/7 trading, on-chain settlement, and global liquidity, but when it really comes down to user needs, the problems it can solve are very limited.

US stock spots already have the world's most mature trading, clearing, custody, and regulatory systems. Enveloping NVDA, TSLA, AAPL in a layer of on-chain assets will not suddenly make ordinary investors perceive it as more valuable, nor will institutional funds abandon their original brokerages, custodians, and compliance paths because it has gone on-chain.

Unless one day on-chain US stocks can truly become native assets within the cryptocurrency system, able to be collateralized and lent together with BTC, ETH, SOL, USDT, USDC, enter unified margin accounts, serve as collateral for contracts and options, participate in DeFi risk control and clearing systems, and even allow users to manage US stocks, cryptocurrencies, stablecoins, and bond assets with a set of margin, then it might have some significance.

Otherwise, what is the significance of on-chain US stock spots? I really don't see much.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。