TL;DR

- Taiwan Semiconductor Manufacturing Company will hold its Q2 earnings conference on July 16, with central focuses on AI/HPC demand, 2nm progress, and gross margin outlook.

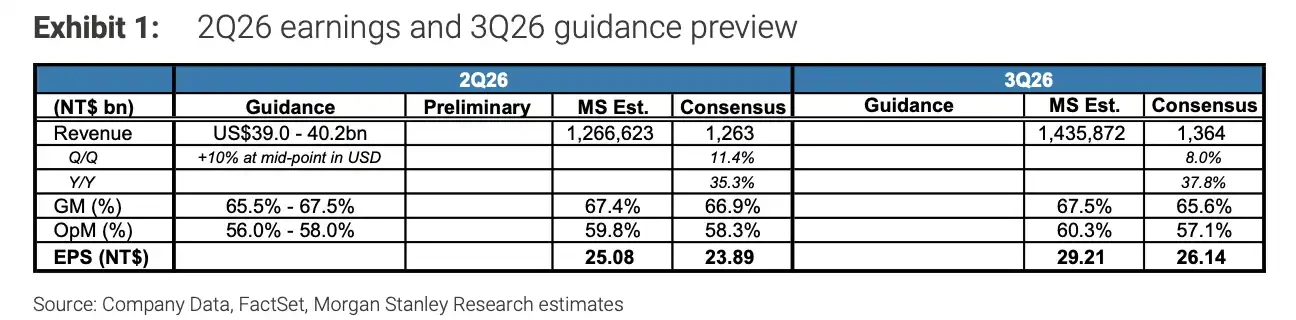

- The company's Q1 revenue was $35.9 billion, with a gross margin of 66.2%; the Q2 guidance is revenue between $39 billion and $40.2 billion, and a gross margin between 65.5% and 67.5%.

- HPC accounted for 61% of Q1 revenue, with advanced processes of 7nm and below making up 74% of wafer revenue, with high-performance computing and advanced nodes remaining the main growth lines.

- Taiwan Semiconductor expects dollar revenue growth exceeding 30% by 2026, with capital expenditure close to the high end of the range of $52 billion to $56 billion.

- AI orders remain strong, but the ramp-up of 2nm, increased depreciation, costs of overseas factories, and customer order rhythms will all impact whether high gross margins can be sustained.

Taiwan Semiconductor will hold its Q2 earnings conference at 14:00 Taiwan time on July 16, with a silent period from July 6 to 15.

The highlights of this earnings conference are not just about revenue growth. As the world's largest foundry, Taiwan Semiconductor connects with mobile chip clients like Apple and Qualcomm on one end, while catering to AI accelerators, self-developed cloud chips, and high-performance computing needs on the other. The Q2 financial report will directly verify three questions: whether AI orders continue to be strong, if the ramp-up of 2nm goes smoothly, and how long the gross margin close to 66% can be maintained.

Over the past year, AI demand has continuously boosted Taiwan Semiconductor's revenue, profit margins, and capital expenditure. The market is now more concerned about whether the high growth driven by AI/HPC can continue to translate into high margins.

Q2 Earnings Report: Focus on Whether Gross Margin Can Stay High

Taiwan Semiconductor has already delivered a strong performance in Q1. The company's revenue in the first quarter was $35.9 billion, with a gross margin of 66.2% and an operating profit margin of 58.1%. In New Taiwan dollar terms, the first quarter revenue was NT$1.134103 trillion, with a net profit of NT$572.48 billion and an EPS of NT$22.08; year-on-year revenue growth was 35.1%, and net profit growth was 58.3%.

The Q2 guidance still remains in the high range. Taiwan Semiconductor expects Q2 revenue to be between $39 billion and $40.2 billion, with a gross margin of 65.5% to 67.5%.

This means that on July 16, the market will be watching not just whether revenue falls within the guided range, but whether gross margins can hold above 65%. Currently, Taiwan Semiconductor's valuation and profit expectations are built on the assumptions of strong AI/HPC demand, tight advanced process supply, and high capacity utilization.

Monthly revenue has already released strong demand signals. Taiwan Semiconductor's revenue in May 2026 was NT$416.975 billion, a year-on-year increase of 30.1%; cumulative revenue from January to May was NT$1.961804 trillion, a year-on-year increase of 30.0%.

However, revenue growth does not equate to synchronized profit growth. Initial expansion of advanced processes will bring equipment investments, increased depreciation, and yield ramp-up costs. Ultimately, what determines market reaction will be the actual gross margin in Q2, as well as management's statements on profit margins for the second half of the year.

Morgan Stanley expects Taiwan Semiconductor's Q2 gross margin to reach 67.4%, at the high end of the company's guidance.

AI/HPC Remains Taiwan Semiconductor's Strongest Support

The strongest growth source for Taiwan Semiconductor is still AI and high-performance computing. Management stated during the Q1 conference call that AI-related demand is "extremely robust," and they have raised their revenue growth forecast for 2026 to over 30%.

The revenue structure also reinforces this judgment. In Q1 2026, HPC accounted for 61% of Taiwan Semiconductor's revenue, with advanced processes of 7nm and below making up 74% of wafer revenue. This cannot be directly equated with the proportion of AI revenue, but it sufficiently indicates that high-performance computing, advanced nodes, and high-end client demand have become the main lines of Taiwan Semiconductor's revenue structure.

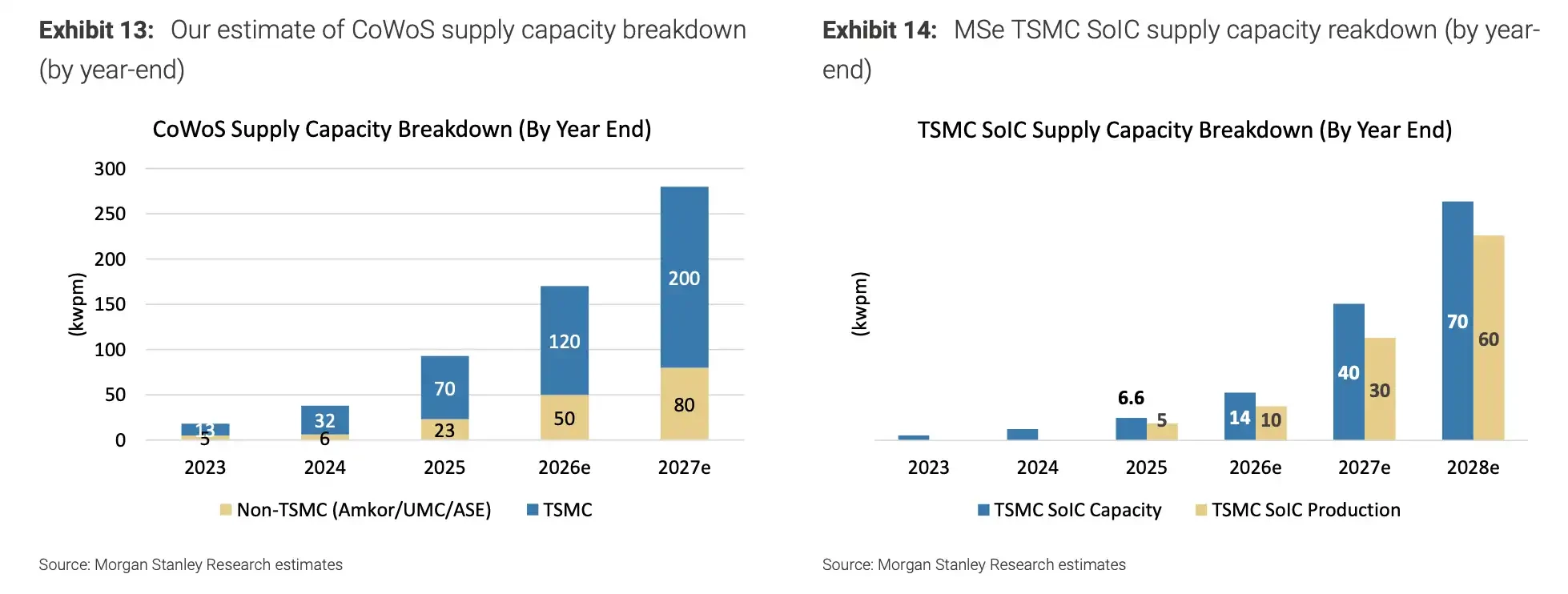

AI chip demand boosts advanced packaging capacity, with CoWoS and SoIC remaining Taiwan Semiconductor's expansion priorities.

The pull from AI chips for Taiwan Semiconductor comes not only from the quantity of orders but also from the individual chip value. AI accelerators and self-developed cloud chips typically have larger areas and higher manufacturing complexities, with stronger dependencies on advanced processes and advanced packaging. This drives up order values, making it easier to maintain tight high-end capacity.

As long as AI capital expenditure continues to expand, it will be easier for Taiwan Semiconductor to maintain capacity utilization and bargaining power. This is why the market views Taiwan Semiconductor as a critical performance verification point in the AI hardware chain.

However, Taiwan Semiconductor typically does not confirm specific client orders from Apple, Nvidia, Qualcomm, etc., one by one during financial reports. Investors can mainly judge true demand strength through revenue structure, capital expenditure, monthly revenue, and management's terminology. Therefore, statements concerning AI/HPC demand, customer inventories, and order rhythms for the second half of the year during the July conference call will be more crucial than single-quarter data.

Capital Expenditure Approaching Limits, Profit Margin Pressure Will Also Increase

Taiwan Semiconductor has directed its full-year capital expenditure for 2026 toward the high end of the range of $52 billion to $56 billion. This move indicates that management sees not short-term fluctuations in orders, but rather a long-term capacity gap driven by AI/HPC demand.

Higher capital expenditure helps Taiwan Semiconductor secure future orders but will also bring higher costs. Advanced process production lines require significant investments, and the depreciation of equipment and facilities will gradually reflect in the profit and loss statement. Building factories overseas in the United States, Japan, Germany, etc., can help spread geopolitical risks but will also introduce higher operational costs, management complexities, and supply chain costs.

Thus, capital expenditure nearing its limit is a double-edged sword. When demand is strong, it represents Taiwan Semiconductor's continued expansion of its leading edge; when demand slows, it will more quickly translate to pressure on gross margins.

This is also the reason the market repeatedly questions gross margins. Taiwan Semiconductor currently does not lack demand; the genuine divergence lies in whether these orders can continue to be realized at high profits.

2nm Ramp-Up Will Determine Next Phase of Profit Elasticity

Aside from Q2 performance, 2nm is an even more critical variable for Taiwan Semiconductor in the coming years. Management previously stated that the N2 process will enter high-volume production in the fourth quarter of 2025, with phased ramp-ups in Hsinchu and Kaohsiung, driven by demand from smartphones and HPC/AI.

For clients, 2nm determines the performance boundaries of the next-generation flagship smartphone chips, AI accelerators, and high-performance computing chips. For Taiwan Semiconductor, 2nm determines the pricing, capacity allocation, and gross margin levels of advanced processes for the next few years.

The market is currently concerned not about whether 2nm enters volume production, but about how quickly supply can be ramped up post-mass production, whether the yield can improve as planned, and whether initial customer demand can cover the hefty capital investments.

If the ramp-up of 2nm goes smoothly, Taiwan Semiconductor can continue to dominate the supply of advanced processes during the peak of AI demand, thereby maintaining the bargaining power of high-end capacity. However, if yield, equipment delivery, or cost pressures exceed expectations, even if revenue continues to grow, gross margins may still be dragged down.

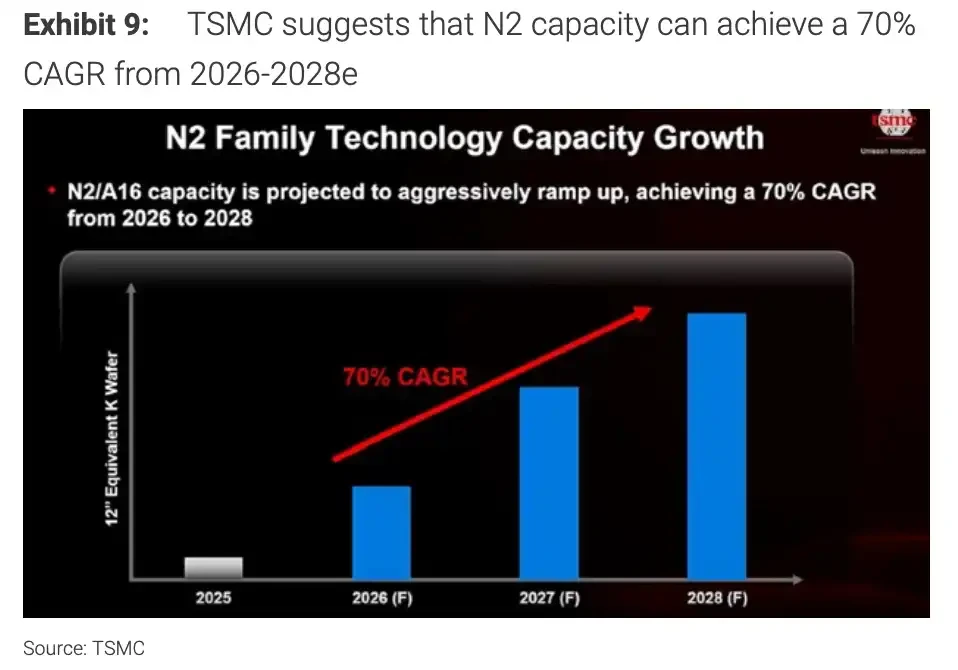

Taiwan Semiconductor expects the N2/A16 capacity to ramp up rapidly from 2026 to 2028, with a CAGR of about 70%.

What to Pay Attention to on July 16

In the earnings conference on July 16, the focus is not just whether Taiwan Semiconductor can meet the Q2 guidance.

The more critical aspect is how management will describe demand for AI/HPC in the second half, advanced packaging capacity, the ramp-up progress for 2nm, capital expenditure arrangements, and the outlook for gross margins.

If Taiwan Semiconductor continues to maintain a strong demand assessment while keeping gross margins within the guided range of 65.5% to 67.5%, market confidence in the AI hardware chain will continue to be supported. If management signals a more cautious outlook regarding customer orders, inventory, or cost pressures, investors will reevaluate how long the high growth in the AI supply chain can persist.

The current strength of Taiwan Semiconductor comes from AI/HPC demand, tight advanced process supply, and high capital expenditure for expansion. The risks are also on the same chain: demand, price, yield, depreciation, and overseas execution; as long as one link does not meet expectations, the gross margin close to 66% will be tested first.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。