Author: Liam 'Akiba' Wright

Translation: Deep Tide TechFlow

Deep Tide Introduction: BlackRock's IBIT contributed nearly 73% of the net outflow from the US spot Bitcoin ETF last week, redeeming $1.3 billion in just one week. When this largest gateway that once brought Wall Street buying interest to Bitcoin starts functioning in reverse, the bulls at the $60,000 mark no longer face retail selling pressure, but rather structural selling pressure from the ETF. The capital flow in the next few trading days will determine whether this is a liquidation or the beginning of continued bleeding.

BlackRock's iShares Bitcoin Trust (IBIT) is becoming the test that Bitcoin bulls least want to face. This ETF, which has helped Bitcoin establish a compliant inflow channel and turned "institutional demand" into a simple narrative, has now become a place where price-sensitive holders are concentrated.

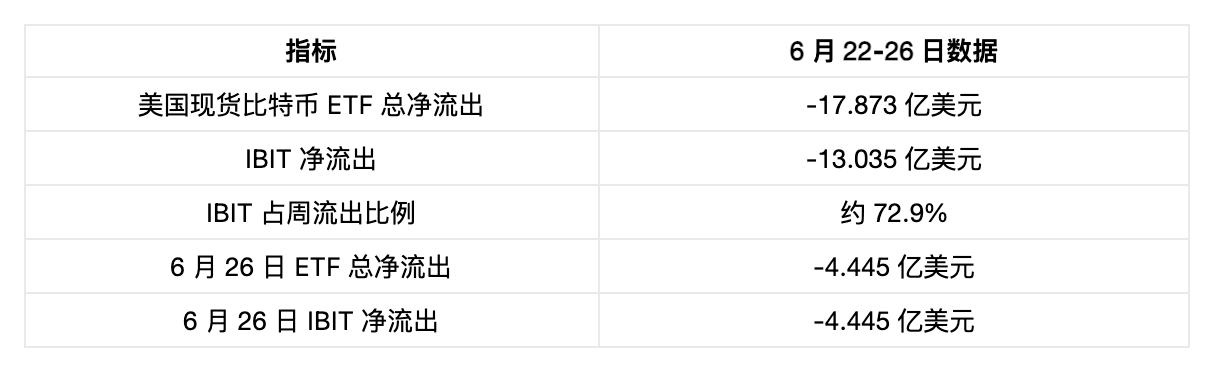

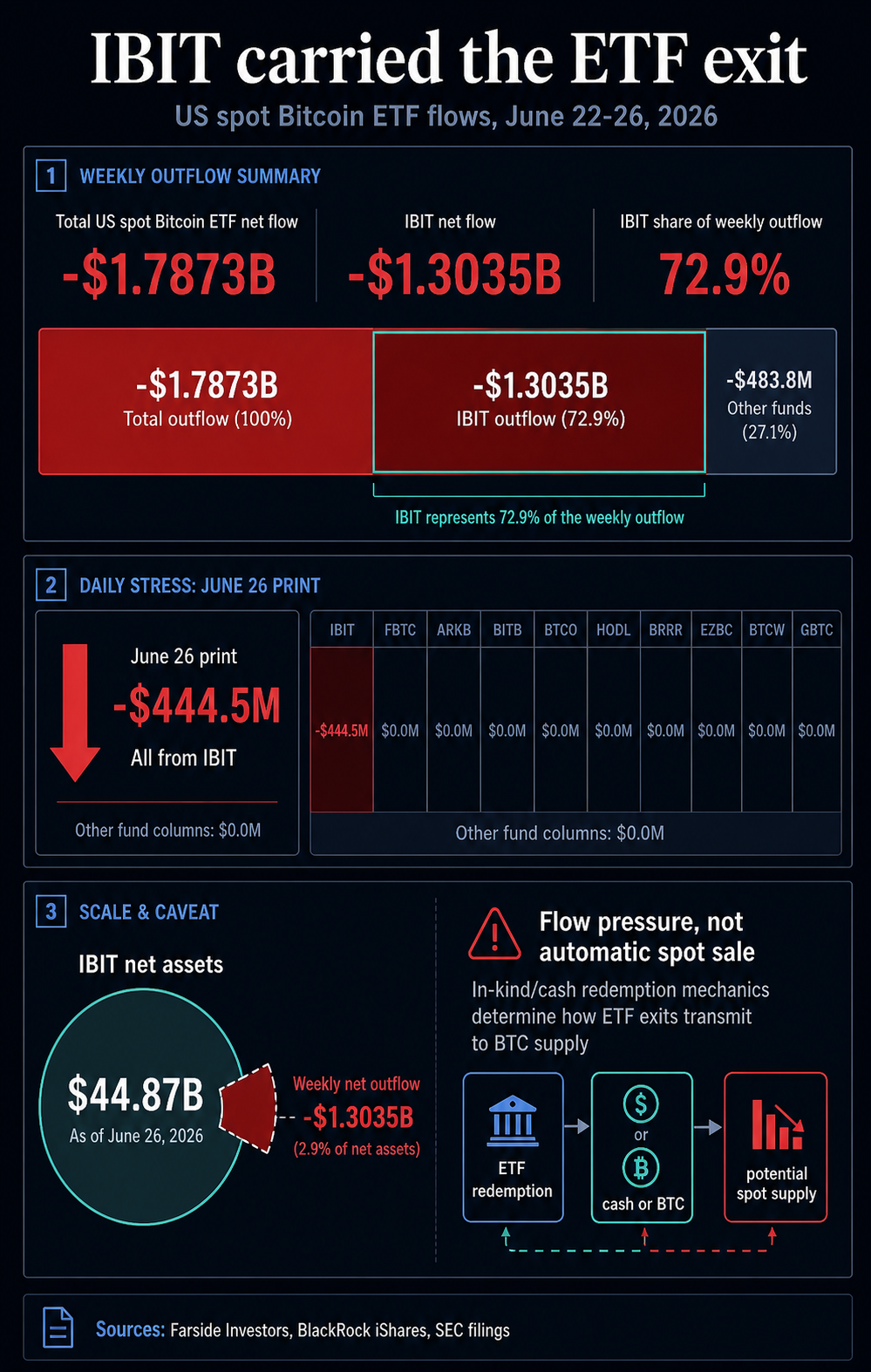

Farside Investors Bitcoin ETF flow data shows that from June 22 to 26, the US spot Bitcoin ETFs had a total net outflow of approximately $1.79 billion. Among them, IBIT accounted for about $1.3 billion, close to 73% of the total outflow for the week.

The data from the most recent trading day made the signals clearer: Farside's June 26 data table shows that the ETF aggregate had a net outflow of $444.5 million on that day, with all negative values coming from IBIT.

This concentration has changed the conditions under which Bitcoin rebounds are tested. The ETF aggregate can still be a demand channel, but the largest spot Bitcoin ETF must now also be viewed as a redemption channel.

If this shell, which once helped Bitcoin gain recognition from brokerage account investors, becomes the main exit route, then spot buyers outside the ETF must absorb these exposures when ETF holders reduce their positions.

IBIT Dominated the ETF Capital Exodus

Farside's data constitutes a market structure signal because the pressure is concentrated on the most prominent Bitcoin ETF in the market.

Caption: IBIT accounts for 72.9% of the total weekly outflow from US spot Bitcoin ETFs ($1.3035 billion / $1.7873 billion), data source Farside Investors

IBIT is not just a code among the ETF aggregate. It is one of the clearest channels for Bitcoin to achieve compliant access through existing brokerage accounts, and its scale makes its capital flow carry more market weight than smaller fund redemptions.

When this product contributes most of the capital outflow within a week, the signal is no longer just about "the ETF market cooling down." This is a stress test for the strongest access channel Bitcoin has gained since the spot ETF was launched.

When capital outflow occurs, Bitcoin itself is already under pressure. CryptoSlate market data shows that BTC traded around $60,000 on June 28, with negative returns over both the 7-day and 30-day periods.

Previous reports from CryptoSlate have tracked the backdrop of the collective surrender of ETFs, as well as Bitcoin's struggles in the $58,000 to $60,000 range. Now the new pressure that adds on is that IBIT itself has become a marginal capital flow that needs to be monitored.

Narrative Flip: The Same Channel, Bidirectional Operation

The early spot ETF story is simple: the compliant channel has broadened the buyer group, ETF demand has reduced available supply, and Bitcoin has gained a holding path that institutional and brokerage account investors are more familiar with.

The latest data retains this history while revealing that the same entry can operate in reverse when ETF holders decide to exit.

The scale of IBIT is not only the reason why this week's outflow is important, but it also provides a proportional reference. BlackRock's iShares official product page shows that as of June 26, IBIT's net assets were $44.87 billion, with a benchmark price near $59,813.

A weekly outflow of $1.3 billion is enough to dominate the ETF aggregate, but relative to the total fund assets, it is still a small proportion. IBIT remains an important compliant Bitcoin package product. The market's question is what this scale means on the margins.

When IBIT attracts capital, its scale reinforces the "institutional demand" narrative. When IBIT bleeds, its scale makes this outflow hard to ignore for other parts of the market.

Smaller funds can continue to bleed without changing the entire ETF narrative; IBIT cannot. Its redemption indicates that ETF holdings around Bitcoin's support levels may be becoming more price-sensitive.

This distinction is crucial at the $60,000 mark. The optimistic interpretation is: the largest redemptions have been digested by the system, and a return of Bitcoin to the $59,000 to $62,000 range would mean the market has absorbed selling pressure.

The cautious interpretation is: the next round of rebounds must not only recover from the liquidation shock but also withstand new ETF selling pressure.

This is the "selling pressure wall" version of the IBIT story. It does not require BlackRock to be bearish on Bitcoin, nor does it require IBIT holders to exit all at once. It is a market structure judgment: the largest access product can become the place where price-sensitive holdings manifest first.

Precise Definition of ETF Mechanism

ETF capital flow data is a pressure signal, and does not equate to direct records of on-chain sell-offs.

In July 2025, the SEC approved the physical creation and redemption mechanism for crypto ETPs. IBIT's filing documents also indicate that the redemption mechanism can involve cash proceeds from the sale of Bitcoin or physical Bitcoin, depending on the path used.

Therefore, ETF outflows should be viewed as conduits of risk rather than direct evidence that every dollar redeemed automatically converts into a dollar sold in the spot market.

Risks still exist. A large, liquid ETF can turn the risk-reducing operations of investors into a recurring source of pressure on the Bitcoin supply side (or supply expectation side), especially when redemptions are settled in cash or when Bitcoin redeemed is subsequently sold.

The market does not need perfect mechanistic certainty; the signals already carry weight. If IBIT continues to produce large net outflow days, buyers must ask: when ETF holders exit, who is absorbing these exposures?

If Bitcoin cannot recapture $60,000 during this period, the old "institutional demand" narrative will weaken. If capital flows stabilize rapidly, the same set of data looking back may simply reflect a clearing of crowded trades.

The real test is whether ETF holdings have matured into a bidirectional source of price pressure. Spot ETFs provide investors with a more convenient holding path, and more convenient holdings also mean more convenient exits.

IBIT's outflows last week placed this exchange condition on a fragile position in the Bitcoin chart.

Two Scenarios

If IBIT's outflows slow, Bitcoin holds the $50,000 high range, and reclaims the $59,000 to $62,000 range, this week can be interpreted as a possible capitulation-style clearing or capital flow reset.

In this version, ETF holders who wanted to exit have already left, the market has absorbed the conduit risks, and the largest compliant product remains a net positive for Bitcoin over a longer timeframe.

If IBIT continues to dominate redemptions, and Bitcoin is unable to re-establish its position above $60,000, the interpretation changes. The ETF aggregate will define the conditions for the next round of recovery testing: non-ETF spot buyers must independently support the market without the help of this shell, which once provided the simplest bullish narrative.

The capital exodus led by IBIT leaves Bitcoin with a live test rather than a conclusion. A week's worth of capital flow data cannot determine investor motivations, and the redemption mechanism does not allow for simple "one dollar out = one dollar sold in the spot market" type inferences.

But the data does indicate: at the moment when Bitcoin most needs demand from outside the ETF system, the most prominent Bitcoin ETF in the market can become a major source of outflow pressure.

For Bitcoin, the unusual weight of the next few trading days is significant. If IBIT's bleeding slows, it will be seen as a depletion of selling pressure. Another round of large redemptions, and the narrative of the "selling pressure wall" will be harder to ignore.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。