BTC is under pressure as the industry shrinks, and regulatory policies are catalyzing traditional finance to accelerate the integration of the crypto sector.

Written by: Oluwapelumi Adejumo

Translated by: Saoirse, Foresight News

Core Overview

- The price of Bitcoin continues to decline, leading to a wave of layoffs in the crypto industry, while the total amount of merger and acquisition transactions in the industry reached $9.37 billion in the first half of 2026.

- Major banks, payment networks, and asset management institutions are opting to directly acquire licenses, custody services, and payment channels, rather than building relevant systems from scratch.

- Market resources show significant differentiation: companies in distress, holding crypto asset management positions, see valuations plummet, while purely decentralized finance sectors receive little attention.

Bitcoin has been in a prolonged decline, forcing crypto firms to lay off workers en masse and push for automation, putting plans for aggressive expansion from the previous bull market on hold. However, at the same time, merger and acquisition activities in the industry are experiencing unprecedented prosperity.

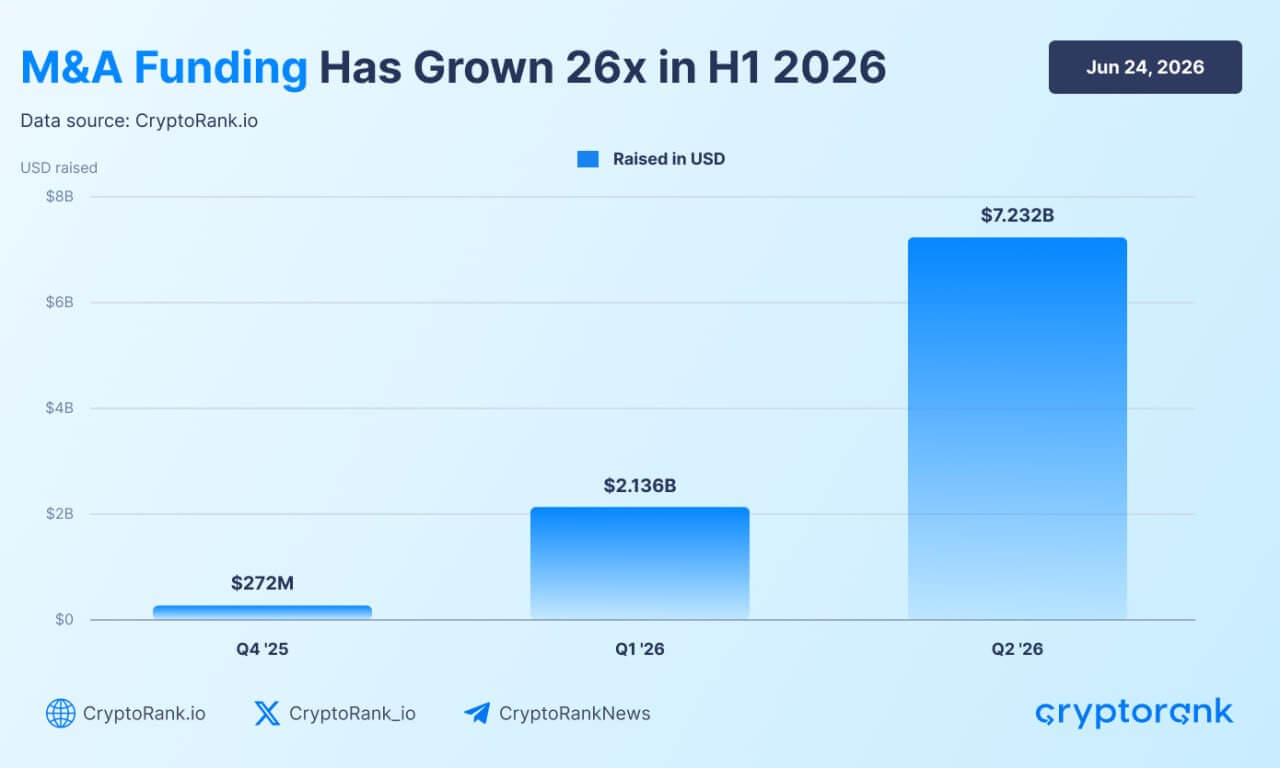

In the second quarter of 2026, the scale of crypto industry merger and acquisition transactions reached $7.23 billion, far surpassing the $2.14 billion in the first quarter. The cumulative investment over two quarters totaled $9.37 billion. Data from the crypto data platform CryptoRank shows that the scale of mergers in the first half of this year skyrocketed 26 times compared to the same period last year, indicating that even with a sluggish spot market, industry merger activity is drastically heating up.

Growth of cryptocurrency mergers and acquisitions (Source: Cryptorank)

This wave of mergers occurs against the backdrop of Bitcoin prices falling to nearly two-year lows, with several leading industry companies continuing to cut back on their workforce. The stark contrast between these two phenomena clearly illustrates the shift in capital flow during a bear market: companies are no longer aggressively hiring and blindly expanding, while traditional financial institutions and leading crypto firms with ample funds are instead acquiring payment systems, regulatory licenses, and custody facilities that would take years to build independently.

This results in a unique situation: the bear market severely impacts many crypto firms, but institutional capital's demand for blockchain-related technology has not disappeared.

Traditional Finance's Massive Acquisition of Crypto Infrastructure

Traditional financial institutions are the core driving force behind the current wave of crypto acquisitions. They prefer to directly acquire a complete suite of mature digital asset infrastructure rather than building compliance systems and technological frameworks from scratch.

Banks, payment service providers, and fintech companies are increasingly targeting startups that already have custody solutions, payment channels, and compliance qualifications. The gradual stabilization of global regulatory policies is the core driving force behind this wave of acquisitions: the EU's MiCA establishes uniform licensing standards, while related legislation for stablecoins in the United States continues to advance, allowing large enterprises to confidently make long-term plans in the crypto sector.

Professionals in the legal and consulting sectors state that the improvement of policies is a key catalyst for this round of mergers and acquisitions. Architect Partners' Q1 crypto merger financing report points out that the banking and securities industries have fully embraced blockchain technology and are reshaping it as the underlying foundation for traditional financial markets.

Mastercard's $1.8 billion acquisition of the stablecoin firm BVNK is a typical case. This acquisition allows the payment giant to directly obtain stablecoin payment technology and global compliance licenses, eliminating years of independent research and development cycles.

Other Wall Street giants are also taking targeted investments to seize early opportunities: Intercontinental Exchange is investing in the prediction market platform Polymarket, Fortress Securities is investing in the brokerage service provider Alpaca, and Standard Chartered's venture capital fund is investing in the market maker Keyrock.

Asset management institutions are similarly capturing the demand of institutional clients through full acquisitions. Franklin Templeton, with a managed scale of $17 trillion, recently established a dedicated digital asset department, Franklin Crypto. This department integrates its investment research team and previously operated crypto active management products under CoinFund by acquiring 250 Digital, directly providing crypto asset management services to Franklin Templeton's global clients.

Overall, private capital is highly favoring companies that can bridge blockchain and traditional financial systems. Q1 financing data shows that funds are primarily directed towards practical applications of stablecoins, such as foreign exchange trading, corporate payroll distribution, and cross-border settlements, rather than toward speculatively inclined native crypto projects.

In the current market environment, compliance qualifications have become a core competitive barrier for companies. Enterprises with brokerage operating qualifications, federal bank charters, and registered investment advisor qualifications (such as Alpaca, Anchorage, Superstate) are favored by buyers, as acquirers can directly obtain legal operating qualifications.

While traditional finance is making large-scale acquisitions with considerable funds, various underlying public chains have also become proactive acquirers. In the past, first-layer and second-layer public chains relied on external developers to build applications on-chain; now, user competition in the public chain sector is heating up, and major public chains are starting to directly acquire application products aimed at ordinary users.

Polygon's recent acquisitions of Coinme and Sequence wallets are a reflection of this shift. By acquiring payment gateways and wallet infrastructure, this public chain is establishing a complete end-to-end user ecosystem, locking in on-chain transaction flow, proving that relying solely on underlying technology is insufficient to maintain market share.

The Crypto Industry's Layoffs Continue to Intensify, AI and Compliance Reshape Talent Demand

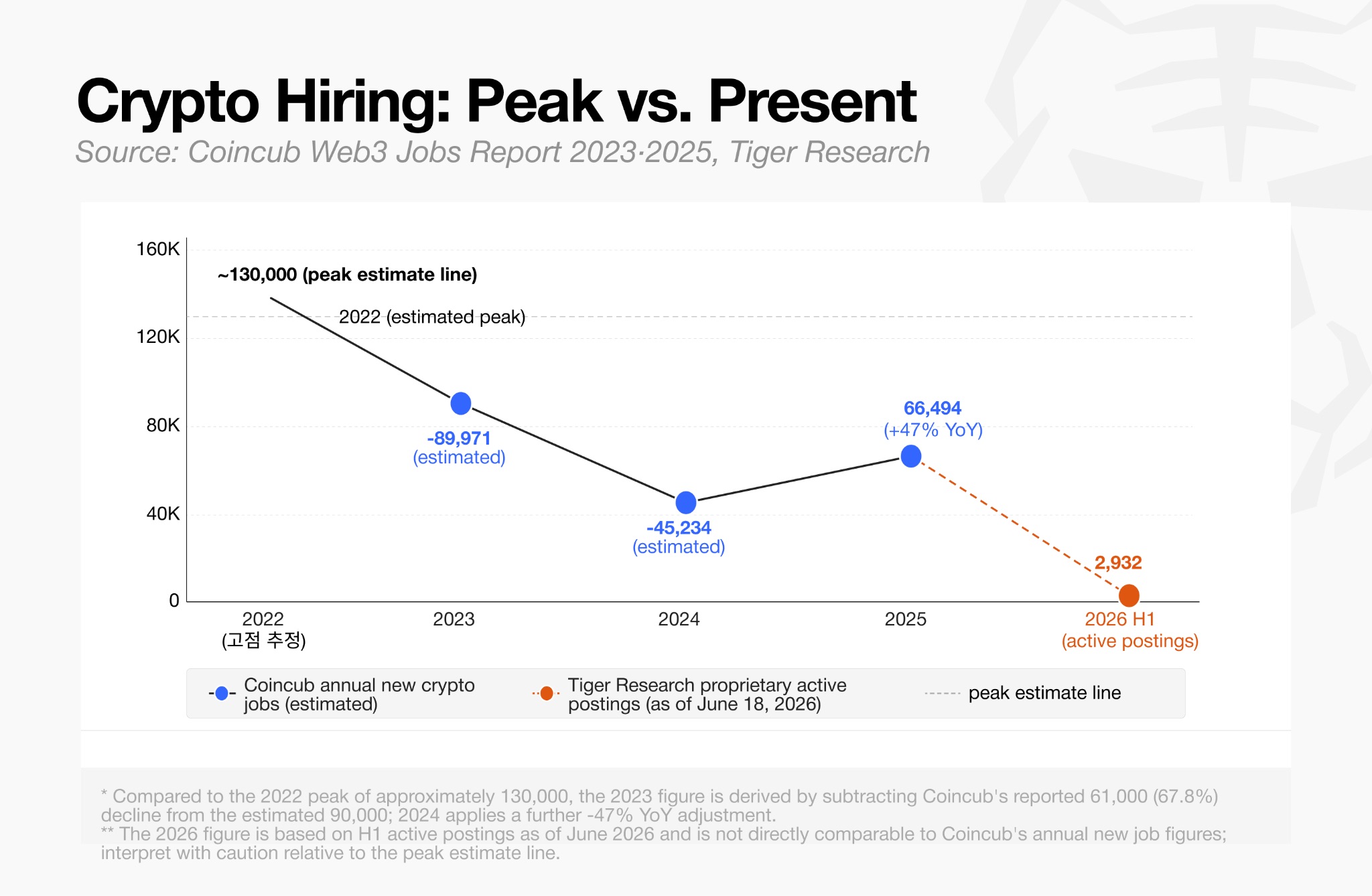

The bustling wave of corporate mergers contrasts starkly with the shrinking job market in the digital asset industry. Tiger Research's statistics for June 2026 reveal that the global crypto industry currently has only 2,932 valid job openings.

Decline in cryptocurrency job openings (Source: Tiger Research)

This number stands in stark contrast to the hiring boom during the bull market from 2021 to early 2022, when major trading platforms, decentralized finance protocols, and NFT platforms were all expanding their workforce. The layoffs started with the market downturn in 2022 and further intensified after the FTX collapse, with the total number of crypto positions in North America and Europe shrinking by about 40%, and have yet to recover to previous levels.

In the first half of 2026, corporate downsizing remains ongoing. Gemini, Coinbase, Kraken, Algorand, Crypto.com, and most recently the Ethereum Foundation have all initiated a new round of layoffs.

Corporate executives indicate that layoffs are primarily due to low token prices and macroeconomic pressures, while the efficiency improvements brought by AI are also an important factor. Coinbase has even directly defined the organizational restructuring as a shift to an "AI-native operational model."

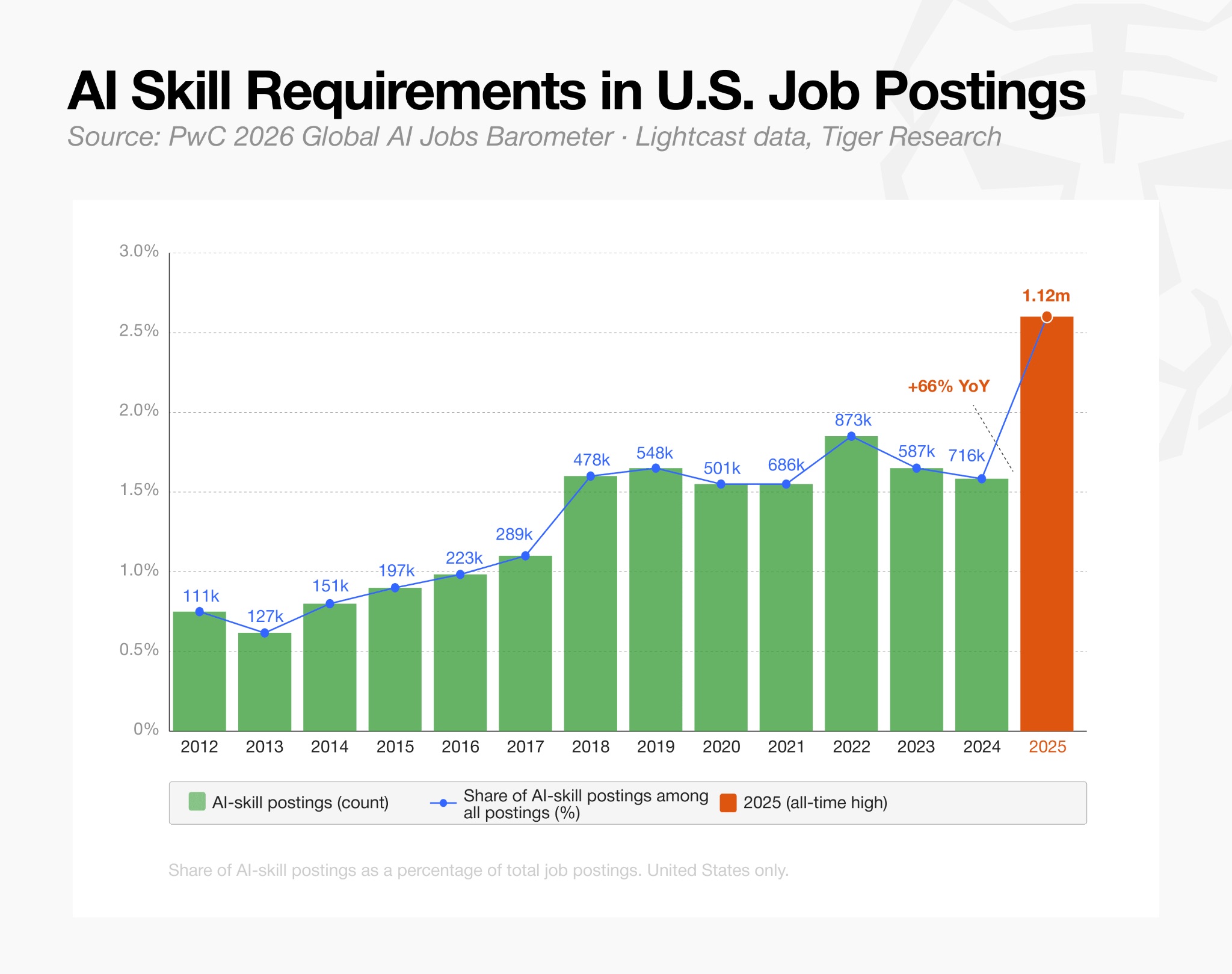

Changes in talent demand are vividly reflected in recruitment information: the proportion of crypto positions requiring AI-related skills has doubled in a year, soaring from 23% in early 2025 to 53% in March 2026.

AI skill requirements for cryptocurrency positions (Source: Tiger Research)

Although overall hiring has cooled, the talent structure in the industry has fundamentally changed: companies are not freezing hiring outright, but are instead concentrating their hiring efforts on technical and compliance roles.

Tiger Research data shows that technical development positions account for 34% of all hiring needs, while legal and compliance roles account for 10%. Compliance positions in centralized exchanges make up 16% of total hiring, which is more than twice the number of market and business development roles.

This indicates that companies prioritize retaining personnel related to licensing, risk control, and core infrastructure operations while significantly reducing spending on marketing and community operations.

The remaining few job openings are highly concentrated within leading firms rather than dispersed among startups. Centralized exchanges offer nearly one-third of industry positions. Jobs in the stablecoin and payment sector are also considerable, but resources are highly concentrated: Tether and Ripple alone account for 80% of the hiring demand in that sector.

Overall data reflect that industry firms are generally carrying out targeted organizational adjustments and adopting defensive operating strategies, with no signs of an industry-wide recovery in employment.

Difficult Crypto Firms Become Acquisition Targets

The acquisition of data agency Messari by Blockworks perfectly illustrates the simultaneous occurrence of massive layoffs and industry consolidation. Crypto analytics service provider Blockworks acquired Messari for approximately $10 million, whereas Messari had a valuation of up to $300 million after a round of funding in 2022, which has now plummeted significantly. Before this sale, Messari had already completed three rounds of layoffs since 2023.

The valuation crash reflects the harsh reality facing crypto startups that rely on venture capital, advertising, and subscription income for survival. Continuous cash flow strain and sluggish revenue growth are forcing many small and medium-sized firms to actively seek mergers and acquisitions, allowing well-funded buyers to acquire professional talent, exclusive data, and traffic channels at low prices.

Industry analysts predict that funding pressures will soon spread to the crypto asset treasury sector. In 2025, several publicly listed crypto treasury companies had stock prices exceeding the total value of their held crypto assets, successfully completing multiple rounds of financing. However, with token prices continuing to decline and corporate stock prices weakening, many of these companies now have market values lower than the real value of the crypto assets they hold, making it difficult to continue to accumulate crypto assets through stock issuance.

The Galaxy Digital research team states that industry mergers are a feasible way out for such companies. High-quality treasury firms, represented by Michael Saylor's Strategy company, can acquire peers at low prices, consolidate balance sheets, and also acquire profitable operating businesses to reduce companies' reliance on the single dependency on token price increases.

Meanwhile, as the relevant legal framework gradually improves, decentralized autonomous organizations (DAOs) are also expected to join the wave of mergers and acquisitions. Wyoming, USA, has introduced a legal framework for decentralized nonprofit collectives (DUNA), granting DAOs the legal capacity to hold off-chain assets and intellectual property. Clear governance and ownership rules allow protocol treasuries to acquire supporting software projects or professional development teams.

However, compared to the current market dominated by compliance-focused traditional corporate mergers, acquisitions by decentralized projects are still in a highly experimental stage.

Market Capital Has Not Dried Up, But Investment Standards Have Become Extremely Strict

Although the scale of crypto mergers and acquisitions approached $10 billion in the first half of 2026, the choices for capital investment have become increasingly selective.

The prediction market sector is the only area not subject to strict selection constraints, with various event trading platforms continuously receiving large financing to aggressively compete for mainstream market share. There are reports that the federally regulated trading platform Kalshi is negotiating a round of financing, with a post-funding valuation reaching $40 billion, almost double its previous valuation of $22 billion; Polymarket has also received massive funding support, and the two platforms continue to compete for the leading position in the prediction market.

Apart from the prediction sector, the industry investment logic has narrowed significantly. Funds are almost entirely directed towards companies that can bridge traditional finance and digital assets.

Tokenization service providers and institutional trading platforms find it easier to secure large financing, as these companies rely on providing compliance services to banks, brokerages, and asset management institutions for stable fees, with business models not influenced by fluctuations in the retail crypto market. Superstate recently completed $82.5 million in funding to expand its blockchain securities issuance business; Alpaca has also taken a leading position in the tokenization of US stocks and ETF settlement sectors.

Financing trends indicate that investors are no longer focusing on conceptual tokenization pilot projects, but are instead betting on mature financial products that are already in place and regulated.

It is worth noting that purely decentralized finance protocols and new underlying public chains without actual implemented applications have completely missed out on large financing this quarter.

The logic of capital investment selection aligns closely with the overall trend of mergers and acquisitions: market liquidity has not vanished, but funds are flowing only to startups that possess compliance licenses, institutional channels, and real traditional financial implementation scenarios.

This round of bear market has effectively completed the survival of the fittest in the industry: companies with weak business models and lacking compliance qualifications must either merge or downsize; meanwhile, companies building compliant financial infrastructure are simultaneously reaping the dual benefits of acquisitions and financings.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。