Tether and Circle remain ever-popular, concealing a hidden arbitrage strategy behind them.

Written by: Yuan Han Li, Partner at Blockchain Capital

Translated by: Luffy, Foresight News

Tether's current daily trading settlement scale exceeds that of most traditional payment networks. Its success to date is attributed to fulfilling a demand that all banks hesitate to touch: a type of on-chain, round-the-clock operating, and unregulated dollar stablecoin.

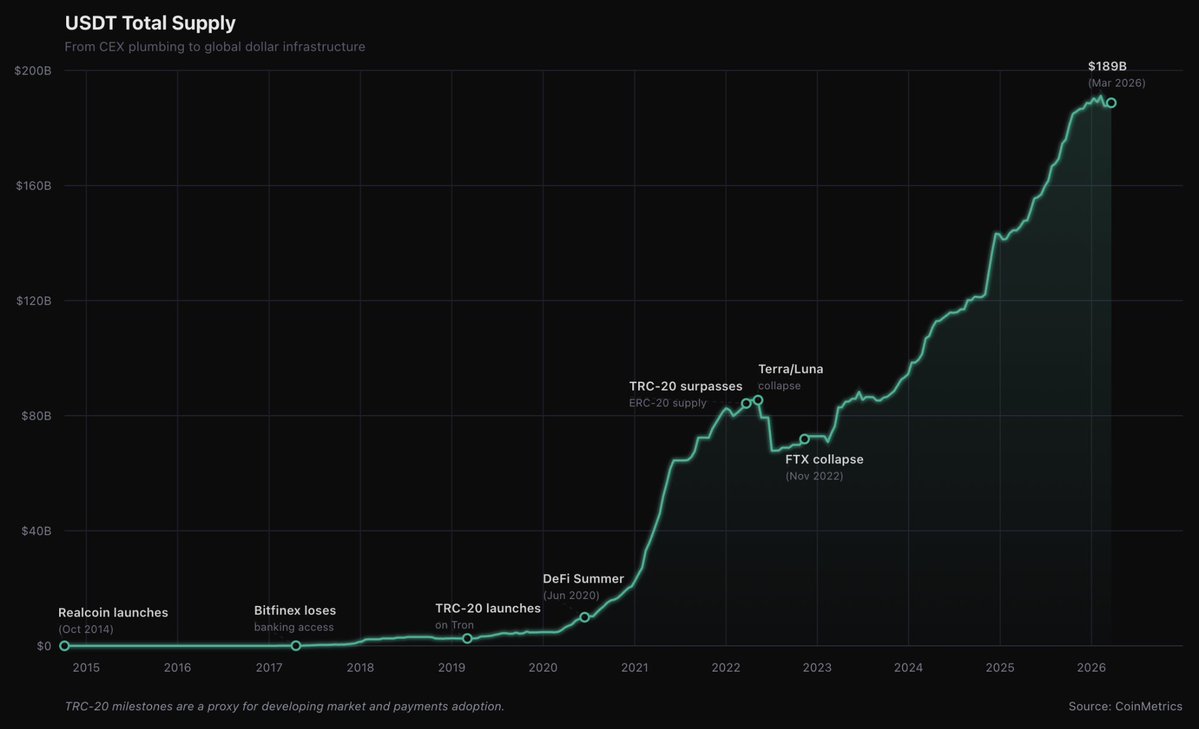

When Bitfinex launched USDT in 2014, its initial purpose was solely for transferring funds between major exchanges to bypass banking channels. This model achieved great success, allowing USDT to become the core trading pair for spot and perpetual contracts on all leading centralized exchanges, deeply embedded in exchange's underlying systems. That year, Binance attempted to develop its own stablecoin as a replacement but ultimately failed.

Subsequently, the emergence of Tron reshaped the landscape, with low transaction fees allowing USDT to become a widely accepted dollar asset for people in Latin America, Sub-Saharan Africa, and Southeast Asia. Originally designed for the flow of funds across exchanges, it unexpectedly gained another core user base—ordinary individuals in high-inflation countries urgently needing to preserve value in dollar assets. Tether built a financial infrastructure that ended up serving an entirely unexpected demographic. Today, it is one of the largest institutional holders of physical gold globally.

The technology itself is merely a secondary factor; the real key is the significant gap between market demand and the capabilities of traditional banking services. Leading companies in the crypto industry all capitalized on these types of supply-and-demand gaps, building positive growth momentum before traditional giants could fill the void.

This business model has a more precise definition: arbitrage. Here, it does not refer to traditional financial arbitrage but to the exploration of long-standing, significant gaps in supply and demand between different markets and regulatory systems that traditional giants find hard to immediately close. It relies on these gaps to establish a growth wheel; before the window closes, it converts short-term profits into sustainable long-term core barriers.

The complete arbitrage pathway consists of three steps: identifying supply and demand gaps, building a growth wheel, and completing business transformation. Most teams in the crypto space can accomplish the first two steps; the hardest part is the third step.

The first two steps require a deep dive into the crypto-native capital markets, understanding the flow of funds, and how various products attract liquidity; the third step necessitates mastering an entirely different system: compliance frameworks, institutional trust, consumer-grade product standards, and partnerships between banks and fintech. Founders that can navigate all three stages are "bilingual": they are proficient in both the crypto capital market and the rules of traditional finance and the mass market. Such individuals are extremely rare but can build enduring companies that withstand cycles.

Cold Start: Building a Growth Wheel on Crypto Native Benefits

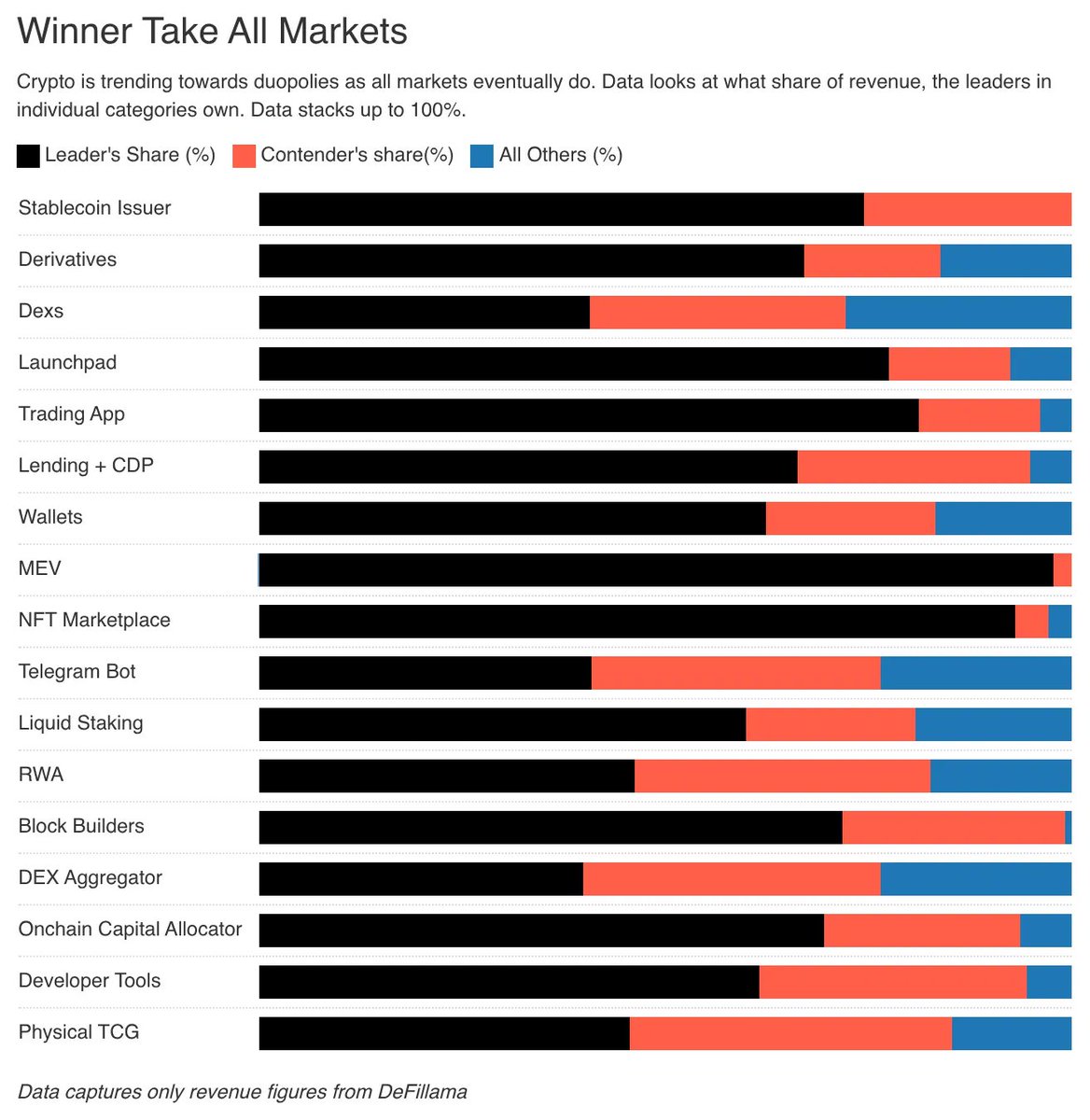

The first two steps of arbitrage—identifying gaps and building a growth wheel—center on a deep understanding of the crypto market; industry rules naturally dictate this. In the total crypto trading volume in North America from 2022 to 2023, 76.9% came from individual transactions of over one million dollars; on the Polymarket platform, a cumulative transaction amount of over 50,000 dollars ranks in the top 5% of global users. Crypto market users cannot be simply equated with ordinary consumers; at its core, this is a capital market: whales, market makers, and professional trading institutions regard various platforms as core financial infrastructure. Thus, the formation of a moat in the crypto industry occurs later and fades faster; true long-lasting barriers require years of accumulation, even if the underlying code can be copied, the barriers cannot be replicated.

Market share of leading companies in various sectors of the crypto industry, source: decentralised.co

In the early stages, projects will not possess any long-term barriers and will rely solely on community recognition and precise predictions of fund flows to get off the ground. The three core driving forces behind cold starts are often intertwined, each testing the founder's understanding of different dimensions of the crypto market.

Speculative Demand: The Most Mainstream Cold Start Method in the Industry

Industry discourse often swings to two extremes: either blindly praising speculation or taking a moral high ground to criticize it, with both perspectives being biased, the latter often having more negative impacts. Objectively speaking, speculation is the most stable cold start engine in the crypto industry’s history.

Tether's inception was entirely to serve speculative funds flowing through exchanges.

Circle seized the DeFi summer boom, where liquidity mining users needed a reliable stablecoin for exchanging various governance tokens. Although everyone at the time understood that most mining tokens would ultimately go to zero, the real demand for a compliant on-chain dollar stablecoin was unprecedented. Circle did not predict the DeFi craze; it merely launched a compliant, transparent product—slightly "conservative" in the crypto circle—just in time to meet market demand for trust.

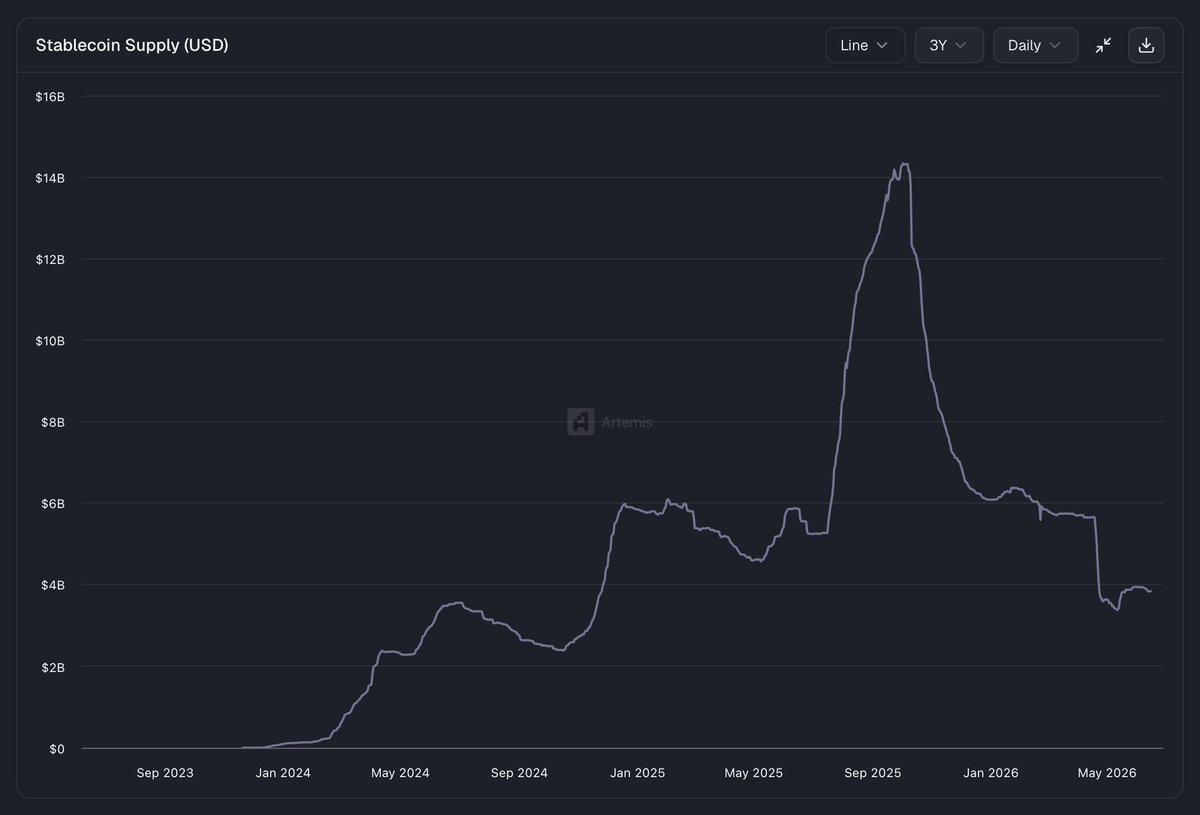

Ethena opened up another user base, aiming for yield. The synthetic dollar USDe generated profits through basis arbitrage from spot and perpetual contracts, with a maximum locked amount reaching 14.5 billion dollars, ranking as the third largest stablecoin globally, and generating over 480 million dollars in fees. This cold start was entirely based on crypto native financial engineering, expanding at an unprecedented pace in DeFi history.

However, not all projects rely on speculation to start.

Essential Demand Drive: The Failure of Traditional Financial Channels Fuels the Popularity of Crypto Products

When existing financial systems are costly and reject large groups, essential demand can directly drive product popularity: high-inflation economies, expensive cross-border remittance routes, ordinary people unable to open dollar savings accounts, etc. When people's pain points are strong enough, there is no need to educate the market, only a usable transfer and saving avenue is needed. RedotPay is a typical case: this crypto payment card company was established in mid-2023 and by the end of 2025, annual revenue exceeded 150 million dollars, with products supporting users in holding and spending stablecoins through a digital banking interface.

This type of model cannot be conceived in offices in New York or London; it must be rooted in local insights. The same product may be merely a novelty for Manhattan residents, but for ordinary people without easy access to dollars or usable bank cards, it is a matter of survival—this is the arbitrage space of supply and demand.

RedotPay's core advantage lies in the team fully grasping two systems: the crypto on-chain channels and the emerging market offline distribution channels. User retention is higher as they are not chasing short-term gains, but rather addressing long-term, inescapable financial pain points.

Subsidy Incentives: Token Rewards, Airdrops to Attract Customers

Subsidies can bolster early trading volumes before natural demand takes shape; the activity generated solely by subsidies may seem like real market demand until the subsidies cease. However, well-designed, quantifiable incentive mechanisms can accelerate the exploration of genuine demand rather than merely creating false prosperity.

Hyperliquid is a recent benchmark in subsidy operations. Large-scale points campaigns and airdrops attracted a massive number of traders, but the underlying product itself possesses industry-leading prowess—fast transaction response times, ample liquidity, and a trading experience comparable to centralized exchanges. Subsidies are merely a stepping stone; robust products retain users. After the incentive activities concluded, the platform's trading volume did not shrink but continued to rise.

All three driving forces above will first attract crypto native participants. Even for essential demand products in emerging markets, funds will still pass through exchanges, wallets, on-chain protocols, and other crypto intermediaries before reaching ordinary end users. Nearly all successfully growing crypto companies in the early stages rely on an understanding of the operational logic of the crypto capital market; without understanding this system, a cold start would be akin to a blind person trying to figure out an elephant.

But relying solely on an understanding of the crypto market is not enough to complete the business transformation.

Mature Transformation: From the Crypto Circle to the Masses

Successfully executing a cold start is inherently difficult; most companies falter at this stage, failing to break out of the crypto-native traffic and achieve normalized profits aimed at the mass market. All companies mentioned in this article once faced the same ultimate question: when core users are no longer just crypto professional traders, does the product still hold value?

A large number of teams successfully navigated the cold start phase but ultimately still faced failure.

The business mindset suited to cold starts, such as rapid iteration, deep community engagement, and fast launches, becomes a burden during the transformation phase. New user groups expect standardized customer service, minimal interaction interfaces, and compliance systems as foundational configurations; growth channels shift from token airdrops and community marketing to banks, fintech, and merchant collaborations; revenue quality becomes more important than trading volume; and the overall operation of the company requires stable and predictable processes, which are completely unnecessary in the early phase.

Circle is a model of successful transformation. Before the full rollout of a stablecoin federal regulatory framework, it invested heavily years in advance to build a compliance system and deeply engage with institutional financial discourse, at a time when the entire crypto industry was still focused inward. When the "GENIUS Act" rolled out in July 2025, establishing the first federal stablecoin regulatory framework in the U.S., Circle’s early layout was no longer conservative but rather highly forward-looking. The company went public on the New York Stock Exchange, achieving annual revenues of 2.7 billion dollars, with USDC's circulation amount reaching 75 billion dollars. Speculative funds still exist but are no longer the entirety of the business.

Ethena, however, is at an uncertain stage of transformation. By the end of 2025, basis yields have shrunk, and the platform's locked assets dropped almost by half. Its cold start was entirely reliant on a single mechanism: spot and perpetual contract basis trading, with the core task of the transformation being to escape a sole source of income. Ethena is simultaneously launching multiple business lines: offering compliant packaged products for institutional yield, issuing USDtb stablecoin based on the BlackRock BUIDL fund, building the perpetual contract exchange HyENA based on Hyperliquid, and opening stablecoin as a service for other ecosystems to issue tokens. The asset reserve structure has been significantly adjusted, with perpetual contract collateral falling from 93% of USDe reserves to less than 5% by mid-2026. Whether these new businesses can substantially carry the previous growth engine remains to be seen, but the direction of transformation is very clear: Ethena is learning the rules of traditional finance while the time window is continuously narrowing.

The failure of the "monolingual model" (note: monolingual refers to a focus solely on the crypto field, ignoring traditional finance; bilingual means proficient in both) is foreseeable, with many teams falling into pitfalls:

- 1. Mistaking the false trading volume generated by subsidies as market-product fit;

- 2. Founders unable to simplify product logic to adapt to the general public;

- 3. Compliance work indefinitely postponed, ultimately leading to regulatory summons;

- 4. Continuous loss of user groups, yet the company's hiring, assessment, and product roadmap remain unchanged.

There is also a more insidious monolingual mindset: founders completely skip the cold start phase of crypto, directly launching crypto products for the masses, and then wonder why no one uses them. The cold start is the ignition phase of the engine; it cannot be omitted; however, once the engine is successfully ignited, if the company continues to optimize solely for the ignition mechanism, it will also stagnate. Both types of teams fall into the category of "monolinguals," just with different spheres of expertise.

Not all tracks present arbitrage opportunities. People continuously propose tokenization products for Manhattan commercial real estate, yet fail to materialize in every cycle: they can attract neither crypto funds nor traditional investors. Such projects lack a supply and demand gap; there’s simply no real demand in either of the markets.

The spike in risks during the transformation phase is fundamentally due to changes in the arbitrage opportunities themselves. During the cold start phase, you leveraged the gaps between crypto demand and unmet markets; in the transformation phase, you need to uncover another layer of gaps: the foundational infrastructure and user trust you’ve accumulated and the access gap to mainstream market channels. As these gaps shift, only bilingual founders proficient in both systems can stand on the side of new opportunities.

Leaders Who Understand Both Cryptocurrency and Traditional Finance

In the 1790s, Mayer Amschel Rothschild dispatched his five sons to five core cities: London, Paris, Vienna, Naples, and Frankfurt. Each learned the local language and financial customs and communicated information using coded messages that outsiders couldn't decipher, with their exclusive network of messengers transmitting messages faster than any official channels. At the time, European banks were flush with capital, but only the Rothschild family could simultaneously perceive market conditions in various countries, seizing opportunities by thoroughly understanding each cross-border supply-and-demand gap.

This logic also applies to the crypto industry, with bilingual founders falling into three categories.

The first type is natural bilinguals with hands-on experience in crypto capital markets and backgrounds that have long engaged with institutional and mass market rules. Circle has been this type since its founding and has been a sought-after asset by capital.

The second type is acquired bilinguals. They delve deeply into the crypto space, with their products naturally adapted to cross-market demands, learning traditional finance rules as a means of expansion rather than completely overturning their own approach. RedotPay is a typical representative: it bridges crypto payment channels with emerging market offline distributions; the team understood the needs at both ends of the gap from the beginning; while they need to continually learn and adjust, they don't have to completely change their positioning.

The third type is founders who refuse to transform, sticking to a singular sphere.

Sometimes, it is those who achieved great success at the start of their entrepreneurial journey that believe market rules are eternally unchanged and that there's no need to learn a second system. When the window closes, companies are still optimizing early-stage businesses that have long been completed, missing transformation opportunities.

At times, the opposite scenario occurs: founders excel in traditional finance but lack instinct in cryptocurrency. Everything appears perfect, yet during the launch phase, no one is interested because the founders never learned how to communicate with the market—essential for navigating the first stage.

Discerning which category a founder belongs to is not reliant on fixed frameworks, but more on market intuition shaped by industry cycles, akin to the market judgment honed by generations of the Rothschild family, deepening their recognition of business models in each cycle.

All founders must confront the same core question, which is the essence of arbitrage logic: which supply-and-demand gap are you exploiting? How does your growth wheel continue to compound? What is the complete path to mature transformation?

As the crypto industry matures, arbitrage opportunities will not disappear; they will only become more elusive, demanding greater operational capabilities, making it hard to detect without mastering both systems.

This bidirectional understanding that spans both crypto and traditional finance is the hardest core barrier to replicate and sustain in the long term.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。