Author: Curry, Trend Research

Trend Overview: On June 22, SK Hynix's market value surpassed Samsung for the first time in 26 years, triggering a trading halt in the Korean stock market, with panic selling in the semiconductor sector.

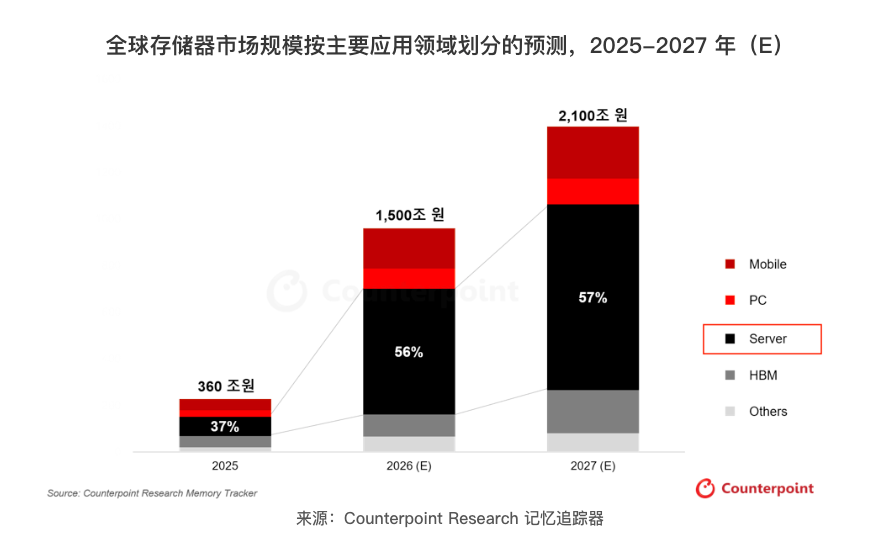

However, on the same day, research institutions released forecasts indicating that the global storage market will exceed $1.5 trillion in size by 2027, with the share of server storage rising to 57%, and the shortage situation expected to persist at least until the second half of next year.

Where exactly is the supercycle? When will the price turning point come? The capacity expansion plans of Samsung, SK Hynix, and Micron provide time clues, pointing to after the second half of 2027.

On June 23, the Korean stock market witnessed a textbook-like "from euphoria to panic."

The day before, SK Hynix's market value reached about $1.35 trillion during trading hours, surpassing Samsung Electronics for the first time in 26 years and closing up 5.6%. But just one trading day later, the KOSPI 200 futures plummeted 5%, triggering a trading halt, with both Samsung and SK Hynix encountering panic selling. According to TradingKey, the direct triggering factors included concerns over AI competitiveness due to changes in Google’s executive team, as well as forced liquidations resulting from regulatory scrutiny of the concentration of leveraged financial products in the semiconductor sector.

This extreme volatility coincided precisely with an optimistic industry forecast.

Data from Counterpoint Research's Memory Tracker released on June 23 shows that the global storage market (DRAM+NAND) will continue to expand in the first half of 2027, exceeding 210 trillion Korean Won (approximately $1.5 trillion), with the share of server storage rising from less than 50% in 2025 to 57%.

On one side, the market is experiencing severe fluctuations at high levels, while on the other, industry data indicates that shortages will persist. For investors focused on the storage sector, a moment of divergence has arrived.

Storage Chip Profit Margins Crush Nvidia, But Supply-Demand Gap is the True Pricing Anchor

To understand the current valuation of storage stocks, one must first look at how strong the fundamentals are.

SK Hynix's revenue for the first quarter of 2026 reached $52.58 billion (converted at current exchange rates), a year-on-year increase of 198%. Operating profit was $37.61 billion, a year-on-year increase of 405%, with an operating profit margin of 72%, surpassing Nvidia's 65% during the same period, setting a historical record in the semiconductor manufacturing industry.

According to CNBC, Counterpoint Research analyst MS Hwang commented that the first-quarter financial report indicates that demand for storage driven by AI inference far exceeded expectations, with companies competing to grab supply.

This exorbitant profit is rooted in structural undersupply.

Goldman Sachs estimated in an April report that the global DRAM supply-demand gap is expected to expand from 3.3% to 4.9%, the most severe in 15 years. Samsung, SK Hynix, and Micron control more than 95% of global DRAM capacity, but nearly all incremental supply is absorbed by AI.

According to TrendForce data, the DRAM contract price surged 90% quarter-on-quarter in the first quarter of 2026, and while the increase in the second quarter narrowed to 58% to 63%, NAND flash contract prices instead accelerated to a quarter-on-quarter increase of 70% to 75%.

HBM (High Bandwidth Memory) is at the core of this round of price increases. This technology, which vertically stacks multiple layers of DRAM chips, is specially designed for AI accelerators, consuming about three times the wafer area of ordinary DDR5 to produce 1GB of HBM, but the price for a single stacked unit ranges from $300 to $500, with profit margins three to five times that of ordinary DRAM. SK Hynix currently holds about 57% to 62% of the global HBM market, being the primary supplier of Nvidia's AI accelerator.

Goldman Sachs estimates that SK Hynix has secured about two-thirds of Nvidia’s next-generation Rubin platform HBM4 orders. SK Group Chairman Choi Tae-won publicly stated in March that the global chip wafer shortage may last until 2030, with expansion of production capacity taking at least four to five years, expecting a gap of more than 20%.

Therefore, from a fundamental perspective, the shortage is expected to continue for another one to two years, and the two companies combined control about 70% of global DRAM capacity, meaning the supply-demand gap is unlikely to change in the short term.

Turning Point Timeline: New Capacity Concentrated After the Second Half of 2027

Counterpoint clearly states in the report: Once new production capacity becomes visible, the risk of a sharp price drop cannot be ruled out. The specific timeline is as follows:

Micron has raised its capital expenditure for fiscal year 2026 to $20 billion, with a new wafer fab in Idaho set to begin production in mid-2027, and a new HBM packaging plant in Singapore contributing capacity the same year. Samsung's P5 factory in Pyeongtaek is expected to be operational in 2028. SK Hynix's M15X facility is set to be operational in mid-2027, and the company has also announced an investment of 19 trillion Korean Won to build a new factory.

However, the pace of expansion is still far slower than the growth in demand.

Goldman Sachs estimates that the storage demand increase from US data centers in 2027 to 2028 will be about 9% to 12%, while domestic capacity expansion will only be about 2% to 4%. Meanwhile, the arrival of HBM4 will further exacerbate the supply-demand contradiction—each HBM4 stack requires 16 DRAM dies, up from 12, causing a 33% increase in DRAM consumption per AI accelerator chip.

TrendForce's direction of judgment is also consistent: HBM3E remains the main shipment, HBM4 has started to contribute to revenue, but delays in AI chip upgrades and inventory accumulation are slowing growth momentum. The real price adjustment window may occur between the second half of 2027 and 2028.

Before that, the absolute level of the supply-demand gap still supports high prices and high profit margins. After that, the concentration of new capacity release combined with possible slowdown in AI investment momentum begins to accumulate the risk of a sharp price drop.

Counterpoint emphasizes that the amount locked in long-term supply agreements (LTA), the customized HBM strategy, and the speed of transition to the next generation process will determine the competition for market share among suppliers. In other words, even if total growth slows, the competitive landscape among the three giants is still being reshaped fiercely.

What This Means for Holders and Observers?

The peak on June 22 and the trading halt on the 23rd encapsulate the core contradictions of the current storage sector:

While the fundamentals of the storage sector continue to accelerate, such as Hynix's first quarter profit margin of 72% and the largest supply-demand gap in 15 years, valuations have already priced in extremely optimistic expectations (SK Hynix has risen over 340% this year), and the concentration of leveraged products has magnified volatility in any direction.

Both Samsung and SK Hynix warned in their financial reports that the storage shortage is expected to continue at least until 2027.

Samsung's storage head Kim Jaejune stated that the demand fulfillment rate has dropped to a historical low, with customers scrambling to secure future supply. However, the market has begun to trade risk on the flip side: the Bank of Korea's inclination to raise interest rates due to the semiconductor supercycle has led Korean government bonds to perform poorly globally.

Currently available information indicates that 38 analysts have a consensus rating of "strong buy" for SK Hynix, with a 12-month target price averaging around 2.71 million Korean Won. Korean brokerage Hanwha Investment & Securities has just raised its target price from 1.63 million to 4.30 million Korean Won.

Thus, the overall judgment, based on publicly available analysis is:

- For holders: Counterpoint and TrendForce both point to the second half of 2027 as the earliest demand-supply turning point, with fundamental support remaining prior to this. However, the forced liquidation risk triggered by leveraged ETFs is an exogenous shock unrelated to fundamentals, making position management more important than directional judgment.

- For observers: The impact of storage shortages on consumer electronics has just begun, with pressure on profit margins for mobile and PC brands and a contraction of low-end product lines being certain events in the next two to three quarters. The short-selling logic along this transmission chain may be safer than chasing high storage stocks.

Note: This article is a compilation of information and viewpoints, with involved individual stocks, ratings, and target prices sourced from public disclosures and are timely, and do not constitute any investment advice. The market has risks, and decisions must be made independently.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。