Author: Rita

Tide Guideline

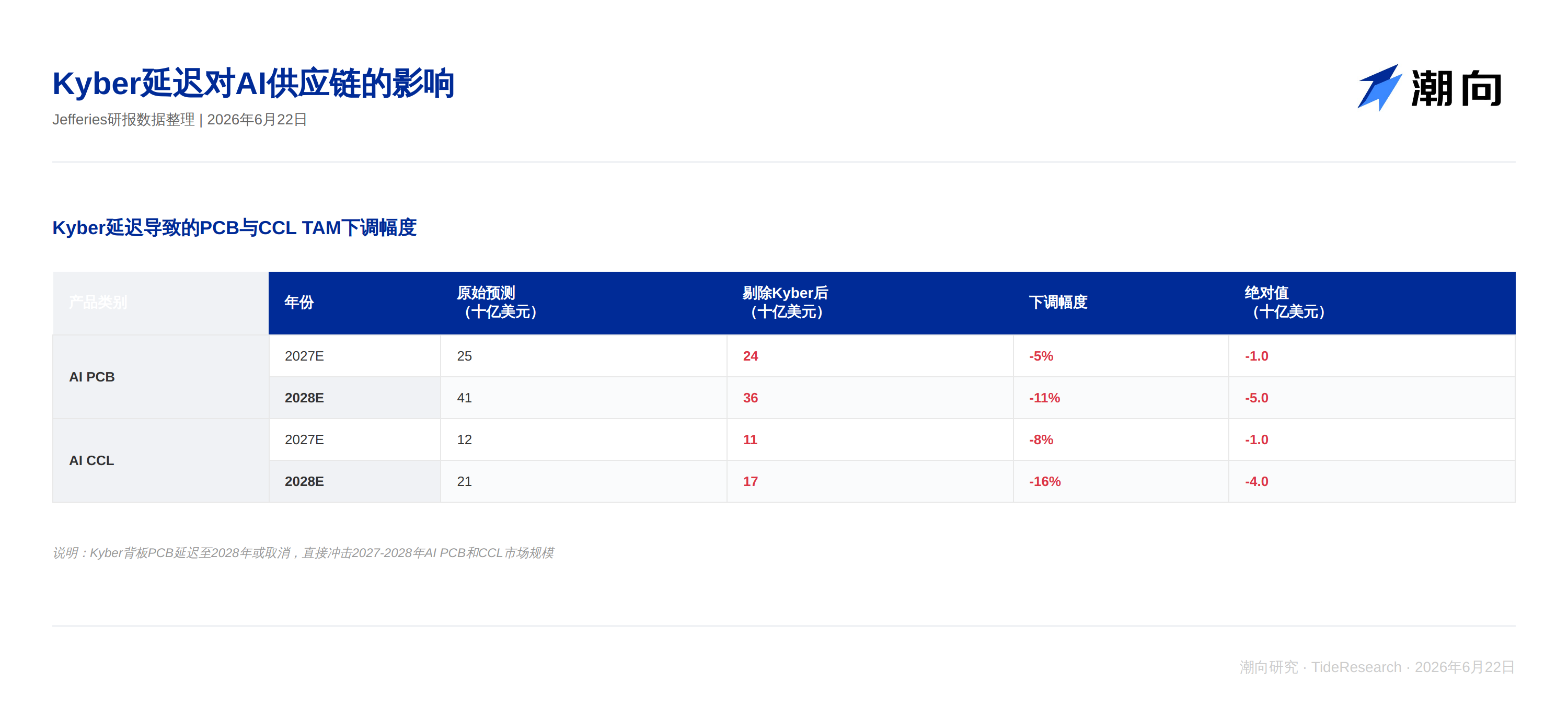

Jefferies released a research report on NVIDIA on June 22, maintaining a buy rating and raising the target price to $300 (an upward increase of 42% from the current $210.69). The core viewpoint is surprising: while optimistic about NVIDIA, they poured cold water on the AI server PCB supply chain. The backplane PCB product Kyber is highly likely delayed until 2028 or completely canceled, leading to a downward revision of the global AI PCB market size by 5% and 11% for 2027/2028 respectively, with CCL (copper-clad laminate) revised down by 8% and 16%. This adjustment may seem like bad news, but it is reshaping the winner's list in the AI server supply chain.

What Does the Kyber Delay Mean

Jefferies believes the Kyber delay is fundamentally certain. The Rubin Ultra was originally planned to feature the orthogonal backplane PCB (Kyber structure), but due to technical bottlenecks in internal rack connectivity, it will still use the Oberon architecture in 2027. Kyber is delayed until at least 2028, with the worst-case scenario being complete cancellation. This change directly impacts the iteration timeline of PCBs.

However, a delay does not mean regression. Switchboards and mid-backplanes continue to migrate to high-end materials, with M9/10 level CCL and PTFE processes becoming industry standards. CoWoP (chip-level interconnect technology) is expected to penetrate by 2027 at the earliest. The trend of increasing unit value remains unchanged, with just an extended time window.

Therefore, the biggest winners from this delay are not on the manufacturing end, but upstream. Upstream material supply like fiberglass and CCL is already tight, with strong pricing power and cost transfer capabilities. PCB manufacturers face more direct pressure from shrinking orders. Copper cable manufacturers benefit from the extended lifecycle of Oberon, with reduced risks of being replaced by PCB.

Why Focus on Specifications Instead of Just TAM

On the surface, the delay of Kyber resulted in a significant downward revision of the AI PCB and CCL market size. But looking closely, this adjustment reflects a reordering of the rhythm of specification upgrades rather than a disappearance of demand.

From data, the original expectation for the global AI PCB market in 2027 was $25 billion, which drops to $24 billion after excluding Kyber, a decrease of 5%. This isn't "shrinking," it's "misalignment." The order volume for Kyber will not disappear; it will just shift from 2027 to 2028. During this shifting process, the order volume left for 2027 will be used for Oberon upgrades, thus raising the specification standards.

This means that the value of a single PCB does not change linearly. Low-end products are revised down, while high-end products are revised up, and there remains space for restructuring overall value under mixed structures. Those profiting will be the players positioned on high-end specifications and upstream material segments, whereas manufacturers that fully rely on low-end capacity expansions will passively bear pressure.

Supply Chain Differentiation: Who Gets Eliminated and Who is in the Inner Circle

The most direct impact of the Kyber delay is the acceleration of the PCB industry's elimination race. Mid-tier manufacturers face the greatest pressure. High-end players have technological depth and customer stickiness, allowing them to follow NVIDIA's rhythm to iterate specifications; low-end capacities have cost advantages and can quickly meet basic demand. However, manufacturers stuck in the middle, unable to handle high-end complexity or compete on cost, will be squeezed out.

Upstream material providers are ushering in structural opportunities. Fiberglass suppliers and CCL manufacturers face demand from the entire industry. The cancellation of Kyber will not reduce the demand for fiberglass and CCL; it will only change the structure. The tight supply situation will not ease in the short term, with pricing power in the hands of material suppliers.

Copper cable manufacturers gain "probation" from the Kyber delay. Before Kyber's launch, copper cables faced the risk of being gradually replaced by high-speed PCB interconnects. The extended lifecycle of the Oberon architecture still provides utility for copper cables.

Why NVIDIA is Still Worth $300

Although Jefferies revised down the TAM expectations for PCB and CCL, they are not pessimistic about NVIDIA's prospects. The Kyber delay does not affect NVIDIA's core GPU competitiveness, nor does it change the growth trajectory of AI server shipments.

Kyber was intended to optimize rack efficiency further in 2028 and beyond. Its delay means NVIDIA loses an innovation story for 2027, but it does not imply a decline in chip sales for 2027. Specification upgrades (M9/10, CoWoP) are still proceeding as planned, and the unit value of AI servers continues to rise.

From a financial perspective, CY28E NVIDIA's expected earnings per share are $14.14, which translates to a target price of $300 based on a 21 times price-to-earnings ratio. This valuation level considers the certainty of long-term AI demand rather than the rhythm of a specific generation of products.

What Are Analysts Betting On

Jefferies' final judgment points towards: upstream materials > NVIDIA > copper cable > downstream PCB.

They are bullish on the "high value-added end" and "supply bottleneck end" of the AI industry chain. GPU chips, as the core computing resource, have the highest value and most steadfast demand. Upstream materials are bottlenecks, with scarcity determining premium pricing. Copper cables gain a breathing opportunity from the delay. PCB manufacturing is the most affected because they are neither bottlenecks nor core competitiveness, just executors.

The delay in this PCB specification upgrade is not bad news, but rather a process of reordering. After the reordering, the inner circle players and companies with the right positioning will have higher profit margins, while those waiting in line will be pushed out of the queue.

Disclaimer

This article is a compilation and interpretation of third-party broker research reports by Tide Research. The ratings, target prices, profit forecasts, and related judgments quoted in the text are the views of the analysts at that brokerage and only represent the stance of their respective institutions, not the views of Tide Research, nor does it constitute any investment advice.

Please note three points while reading: 1. The target price is the analyst's expectation for the next approximately 12 months; it is a prediction rather than a commitment and will be adjusted repeatedly with performance and market conditions. 2. Sell-side research reports tend to be overly bullish, and some covered companies may have investment banking relationships with the brokerage. 3. The value of research reports lies in the mainline logic and its underlying assumptions, rather than in a single target price. Focus on logic, don’t just look at the price.

Markets are risky, and decisions must be independent. This article should not be used as the basis for buying or selling any securities.

Data sources: Jefferies Research Report (Jacky He et al., June 22, 2026) · Prismark · NVIDIA Public Financial Reports

Tide Research · TideResearch · June 2026

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。