Recently, this machine has started making unusual noises.

Written by: Non-Small Number

In recent years, Strategy has been the most aggressive and controversial Bitcoin company in the capital markets. Its story is not complicated: continuous financing, continuous purchases of Bitcoin, turning the company's balance sheet into a massively oversized BTC position. As long as Bitcoin rises, this model works like an accelerating financial machine, with stock prices, financing capabilities, and market confidence reinforcing each other. But recently, this machine has started making unusual noises.

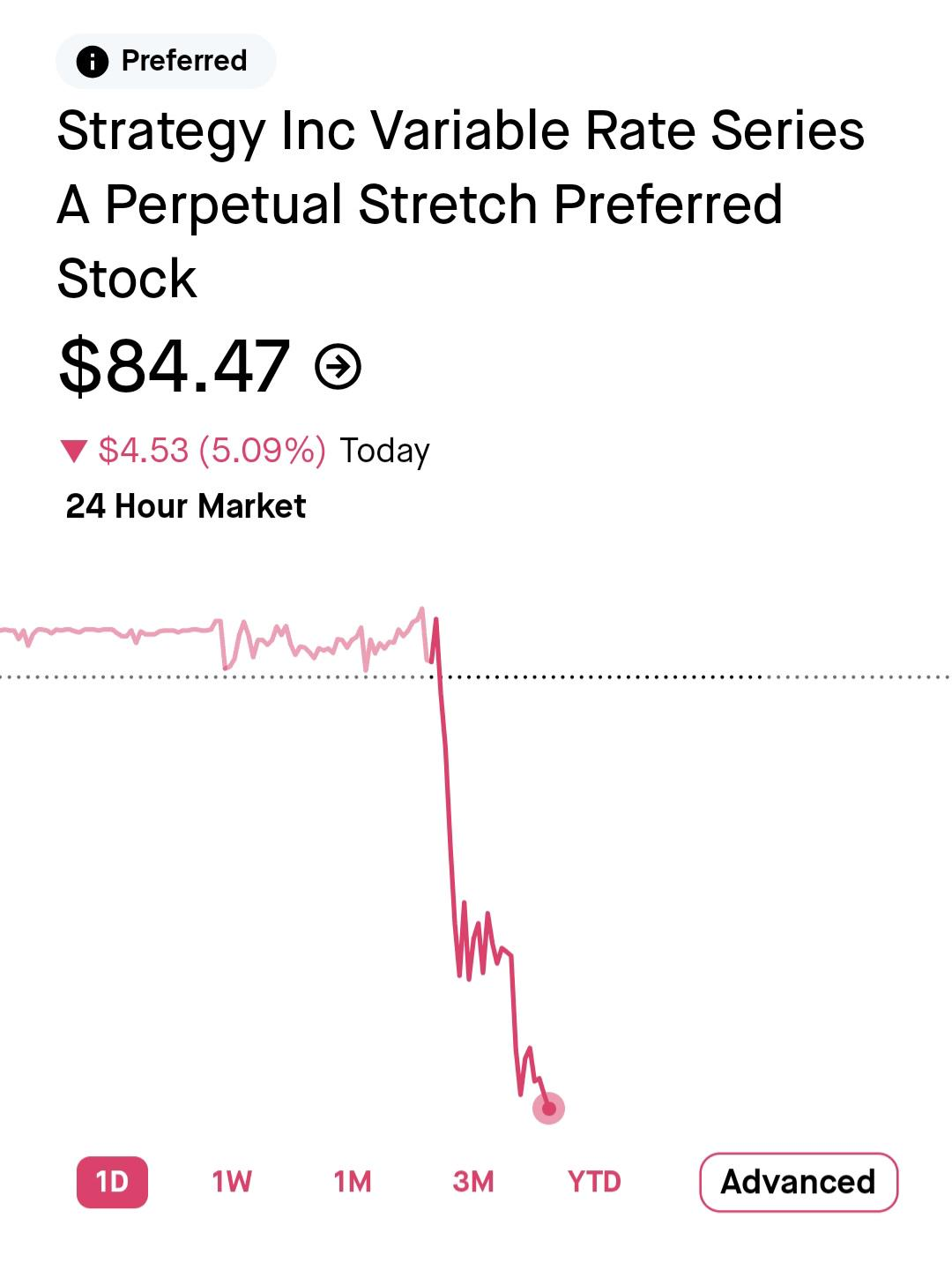

According to Decrypt, the flagship preferred stock STRC under Strategy has faced significant selling pressure, once dropping to a historic low of about $82.53 before rebounding to around $87. For a preferred stock designed to trade around a par value of $100, this price has clearly deviated from the target range. Even more notably, the drop in STRC was not an isolated event. The common stock MSTR of Strategy also weakened simultaneously, with a significant increase in the cumulative decline over the past month, even exceeding the downturn in Bitcoin prices during the same period.

This suggests that market concerns may not be just about "Bitcoin dropping." The real question is: Can Strategy continue to maintain this financing cycle that relies on capital markets, preferred stock dividends, and Bitcoin reserves in the long term?

1. Why did STRC become the market focus?

STRC, short for Stretch Preferred Stock, is a type of variable-rate perpetual preferred stock launched by Strategy. Simply put, it is neither common stock nor ordinary bonds, but a kind of financing tool that lies between the two. Investors buy STRC not primarily expecting the company's stock price to rise significantly, but rather to obtain stable, high cash dividends.

Its design target is to trade around a par value of $100. Theoretically, STRC should remain as stable as possible around $100. If the price stays below $100 for a long time, the company can increase the dividend rate to enhance attractiveness and encourage the market to buy back in. In the past few months, STRC's annualized dividend yield has remained around 11.5%. In traditional markets, this is already a relatively high yield.

But herein lies the problem. When a company issues high-yield preferred stock, what the market really focuses on is not "how much is promised," but "whether there is the ability to pay in the long term." Especially for a company like Strategy that has core assets highly tied to Bitcoin, investors will naturally question: If Bitcoin prices continue to fluctuate, where will the company's cash flow come from? What will cover the preferred stock dividends? Will there be a need to continue issuing stock, issuing bonds, or even selling Bitcoin?

STRC dropping below $90 essentially means the market is reflecting these questions directly into the price. It is not merely a short-term fluctuation, but investors are reassessing Strategy's capital structure, dividend capabilities, and financing model.

2. The decline of STRC is not a coincidence, but a mechanism at work

On the surface, the decline of STRC is related to the ex-dividend date. The so-called ex-dividend date refers to the day from which investors buying STRC will no longer be entitled to the upcoming dividend payment. Therefore, it is normal for the preferred stock price to see a certain pullback after the ex-dividend date. However, this time, the market's reaction has been noticeably more intense.

The reason is that STRC has not returned to the vicinity of the $100 par value for a long time, indicating that investors are not satisfied with the current dividend level. In other words, the market is demanding a higher actual yield at a lower price. When the dividend yield of a preferred stock falls below the risk compensation required by the market, its price will naturally move down until the yield becomes attractive again.

Benchmark-StoneX analyst Mark Palmer's view is quite direct: this is not a product malfunction, but rather the structure is functioning as intended. When the actual dividend yield of STRC is below the market-required yield, the price will naturally decline; if the company raises the dividend rate, it theoretically will push the price back towards par value. This is also the key mechanism for products like STRC: falling prices lead to rising yields; if prices fall too much, the company has the motivation to increase dividends in an attempt to stabilize prices.

However, increasing the dividend rate does not come without costs. The higher the dividend, the more cash the company has to pay each year. For Strategy, this will further amplify the market's concerns regarding its cash reserves and financing capabilities. In other words, the mechanism of STRC can indeed help the price return to par value, but the premise is that the market believes Strategy has the capacity to bear higher cash payment obligations.

3. What is truly being repriced, is Strategy's cash pressure

In the past, Strategy was able to continuously buy Bitcoin due to its strong capital market financing ability. During the Bitcoin bull market, this model worked very smoothly: the market believed in it and was willing to buy its stocks and preferred stocks; the company secured funding and continued to buy BTC; the rising BTC further increased the company's asset value, enhancing its financing capabilities.

However, when the market starts to have doubts, the cycle can reverse. CoinShares' research director James Butterfill believes that the continued weakness of STRC is not entirely driven by Bitcoin prices; more importantly, the market is uncertain about how Strategy will manage its growing fixed payment obligations. This statement is crucial. While rising Bitcoin prices will increase Strategy's asset value, the increase in BTC assets doesn't mean the company has more cash immediately available for dividend payments.

Preferred stock dividends are a cash obligation and cannot be directly paid from the "book value of Bitcoin." As long as the company commits to paying distributions to STRC holders, real cash must be produced. This is also what concerns the market the most: if cash reserves decrease and financing windows narrow, will the company be forced to sell some BTC?

One of the most controversial recent events was Strategy's sale of 32 Bitcoins, cashing out about $2.5 million. In terms of scale, this sale is not significant. For a publicly traded company holding hundreds of thousands of BTC, 32 Bitcoins are almost just a drop in the bucket. But what the market cares about is not the amount, but the signal.

In the past, Strategy’s core narrative has always been “buy and never sell.” It consistently financed through capital markets and then continued to increase its BTC holdings. This steadfast one-way behavior has been a crucial source of market faith. Now, even a small-scale sale prompts investors to rethink: Is it really possible for Strategy's Bitcoin reserves to become a source of funds for paying dividends and debt costs in the future?

Once the market forms this expectation, Strategy's valuation logic becomes more complex. It is no longer just a "leveraged Bitcoin proxy asset," but a financial engineering company that needs to constantly balance its BTC holdings, cash dividends, financing costs, and market confidence. This is why the volatility of STRC is worth paying attention to. It is not only an issue of preferred stock prices but also a measure of market trust in Strategy's overall capital structure.

4. "32 years of coverage capability" does not equal 32 years of cash

In response to the criticism, Strategy stated on social media that based on its BTC reserves, the company has about 32 years of debt coverage capability. This statement sounds strong. It roughly uses the market value of the Bitcoin held by the company to compare with the annual dividends and interest expenses. If calculated based on the current market value, it can indeed yield a seemingly high coverage multiple.

However, investors need to understand that this is not cash coverage, but asset coverage. Bitcoin is a highly liquid asset, but it does not equate to frictionless cash. Large-scale sales of BTC may bring price impacts and also affect market sentiment. More importantly, once Strategy is perceived by the market to be relying on selling coins to maintain dividends, its original narrative of "continuously accumulating coins" will be weakened.

This is also part of the reason some market participants are raising concerns: the seemingly huge BTC reserves on the books do not mean they can be fully realized at market price when it comes to actual financing or liquidation. Asset values and disposable cash are always separated by a layer of market liquidity and investor confidence. Especially during times of increased market volatility, investors will pay more attention to "can it be liquidated," "will liquidation affect price," and "does the narrative still hold after liquidation."

Currently, directly interpreting the drop in STRC as the "crisis outbreak" of Strategy might be premature. The company still possesses a large Bitcoin reserve, and its asset side has not collapsed. STRC itself also has a stabilizing mechanism; if prices continue to be below par value, the company can attract buyers by increasing the dividend rate. From this perspective, the current situation appears more like a capital structure stress test following Strategy's rapid expansion.

In the past, the market focused on how much BTC it had purchased, but now the market is beginning to focus on how it will pay dividends, how it manages cash, and how it maintains financing ability without damaging the narrative. This is a shift in narrative. For ordinary investors, several signals are worth watching: whether STRC continues to fall below $90, whether Strategy raises the STRC dividend rate, whether the company continues to sell BTC, and whether MSTR common stock continues to underperform BTC.

5. Can Bitcoin's rise solve everything?

Strategy's story is essentially an experiment about faith, leverage, and cash flow. When Bitcoin rises, all problems tend to be obscured. Asset values increase, financing becomes easier, and the market is willing to believe the company can continue to expand. But when price volatility occurs, preferred stock prices decline, and cash obligations are magnified, investors return to the most fundamental questions: How much does the company need to pay each year? Where does the money come from? If smooth financing cannot continue, will it need to tap into BTC reserves?

STRC dropping to a new low does not necessarily mean the failure of Strategy's model. But it reminds the market: even the world's largest publicly traded Bitcoin holder cannot only tell the story of the asset side. As long as there are fixed dividend and interest obligations, the realities of cash flow, financing costs, and investor confidence must be faced.

Bitcoin can be a trump card on the balance sheet. But in the capital markets, whether the trump card can continue to play ultimately depends on whether the market is willing to continue believing in this game. For Strategy, the real test is not how much BTC fluctuates on a given day but whether it can maintain market confidence in its long-term model when financing costs rise, preferred stock prices are under pressure, and cash payment pressures become apparent.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。