We chatted with three Crypto VCs and found that LPs value exit routes and investment management systems, GPs are optimistic about real financial processes, and projects need to prove real demand.

Written by: KarenZ, Foresight News

If you only look at the leading funds, the Crypto VC market in the first half of 2026 is not cold.

According to statistics from Foresight News, among the new Crypto VC funds announced or launched in the first half of 2026, only a16z crypto and Haun Ventures have achieved sizes of $1 billion or more: the former launched a $2.2 billion Crypto Fund 5, while the latter completed the fundraising of a new fund of $1 billion.

For funds announced between $500 million and less than $1 billion, there is only Dragonfly's $650 million Fund IV. Further down are Variant's $222 million Variant 4 and ParaFi's $125 million new fund focused on stablecoins, tokenization, and institutional on-chain finance.

Almost every month, there is a Crypto VC secured with over $100 million in new ammunition. The market is not that cold.

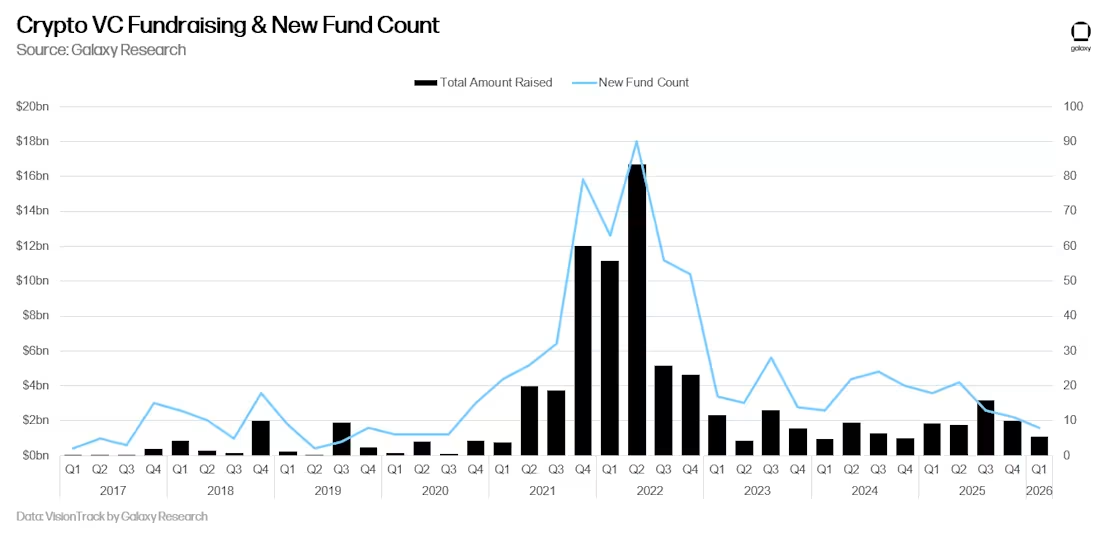

However, another set of data presents a cooler side. Galaxy Research report mentioned that only 8 new Crypto VC funds completed fundraising in Q1 2026, totaling about $1.1 billion, which is the lowest quarterly number of new funds since Q3 2020. Compared to Q1 2023, the number of new funds in Q1 2026 has decreased by about 43%, total fundraising has halved, average fund size has dropped by about 41%, and median size has decreased from $62.5 million to $55 million.

Source: Galaxy Research

This also makes the earlier big fundraising more meaningful: the market has not completely cooled down, but the heat is mainly concentrated in a few funds. The emergence of large funds amplifies the feeling of recovery, but the number of new funds, average size, and annualized fundraising rhythm all remind that the overall fundraising foundation of Crypto VC is already much thinner than in the previous round.

Combining public fundraising data and our interviews with IOSG Ventures founding partner Jocy Lin, HashKey Capital CEO Deng Chao, and Starbase founder Vivian, a clear signal is emerging:

The Crypto VC in 2026 is not a comprehensive recovery, but rather a narrower recovery. The fundraising window is still open, but the door has narrowed. Those who can squeeze in are usually GPs with long-term performance, exit cases, clear strategies, and cross-cycle capabilities; projects that can receive funding are increasingly concentrated in areas like stablecoins, RWA, institutional financial infrastructure, and Crypto x AI—directions that are easier to validate and closer to real financial infrastructures.

From changes in LP questions to narrowing industry preferences, and then to reconfiguration of investment strategies and exit paths, Crypto VC is entering a stricter new cycle.

The Requirements from LPs Have Changed: AUM Is No Longer Enough; DPI Has Become Hard Currency

From 2021 to the first half of 2022, the primary market was like a high-speed operating financing machine. Funds were raising, projects were financing, ecological funds were subsidizing, exchanges and market makers were providing liquidity.

At that time, Crypto VCs had a kind of tacit consensus: as long as the industry beta continued to expand, early investments could always be caught by the next round of liquidity. But now, this default consensus has broken down.

IOSG Ventures founding partner Jocy Lin summarized this change as shifting from "narrative-driven" to "DPI-driven." He believes that "in the past narrative-driven cycles, the gap between top and mid-level funds was not fully widened; but in the current DPI-driven environment, funds that can achieve genuine exits and clarify exit paths will take more LP funds, while the remaining money will compete among a large number of mid-tier funds."

Deng Chao emphasizes, "The cyclicality of Crypto is strong, so funds cannot rely solely on a single exit path; they must have cross-cycle allocation capabilities. In terms of fund allocation, HashKey Capital places greater emphasis on portfolio structure: which are long-term infrastructures, which are cash flow projects, which are high volatility but high upside early projects, and which can enhance liquidity through secondary or liquidity strategies."

This is also why it is now difficult to judge the actual state of a Crypto VC by just looking at AUM.

Fortune magazine’s April report based on SEC filings reported a detail: during the market downturn in 2025, the asset management scales of leading institutions such as Paradigm, Pantera, a16z crypto, and Multicoin were all affected. The total AUM of a16z crypto's four funds fell nearly 40% to $9.5 billion between 2024 and 2025, partly because their first three funds began distributing capital to LPs.

It is worth mentioning that Fortune magazine quoted data from Newcomer reporting that a16z's first crypto fund achieved a net DPI (the ratio of capital allocated to paid-in capital) of 5.4. Pantera also allocated capital to LPs in 2025 due to five portfolio companies going public, including Circle and BitGo. Multicoin, on the other hand, was more affected by market cycles, with AUM halving to nearly $2.7 billion between 2024 and 2025. Haun Ventures, however, is one of the few leading institutions with AUM growth, exceeding 30% year-over-year to nearly $2.5 billion.

These details point toward a change: the narrative of scale in Crypto VC is now giving way to distribution capabilities. What LPs really want to see is whether GPs can turn paper-based returns into cash returns.

This dissatisfaction has also begun to appear in more public discussions. Akshat, co-founder of Maelstrom, a fund under Arthur Hayes, mentioned on Twitter in November 2025 that as an LP, he invested $100,000 in an early Token fund, and four years later there were only about $56,000 left (3% management fee + 30% revenue share); during the same period, Bitcoin doubled, and many seed-stage projects also saw returns of 20 to 75 times.

His conclusion is that many early Crypto funds have already surpassed the carrying capacity of truly high-quality project pools, and LPs need opportunities that are more suitable for large-scale allocation. Akshat also promoted the Maelstrom Equity Fund I product. This fund will focus on chain-off "shovel" businesses with positive cash flow, providing founders with cleaner cash exits through control acquisitions while developing these businesses into targets that could be acquired by new entrants such as Robinhood, Charles Schwab, X, and Wealthfront in the future.

For LPs, these types of products attempt to provide a path that does not directly bear Token volatility but can allocate cash flow assets in the Crypto industry on a nine-figure scale.

Beyond exit assessments, LPs are also increasingly questioning fund governance and risk control details.

Deng Chao told Foresight News that "LPs are no longer just asking about tracks and projects, but are more concerned about asset protection, compliance risks, exit capabilities, and real landing value. What institutional LPs ultimately pay for is a set of verifiable, executable, and sustainable investment and risk control processes."

The tightening LP standards will eventually be reflected in the fundraising data of Crypto VCs. The previously mentioned Galaxy Research data has already indicated that both the number of new funds and the total amount raised are shrinking, but a few leading GPs can still open a window.

Dragonfly is one of the typical examples of this cross-cycle fundraising capability. In February 2026, Dragonfly managing partner Haseeb Qureshi announced that Fund IV was completed with an over-raise of $650 million. Popular projects like Polymarket, Ethena, Rain, and Mesh became growth cases used by Dragonfly to persuade LPs.

Some GPs are also trying to respond to LP's new questions with the funds themselves. Jocy Lin mentioned that IOSG plans to launch new fund products this year, hoping to gain LP recognition through more distinctive product designs while continuously providing new investment cases to the market.

In other words, the competition among Crypto VCs is not just happening in project investments; it is also occurring in whether product structures can answer liquidity, DPI, and cross-cycle allocation requirements. A small number of GPs with brand, performance records, and exit cases can still secure funding, while more GPs are facing longer fundraising cycles and stricter LP questionnaires.

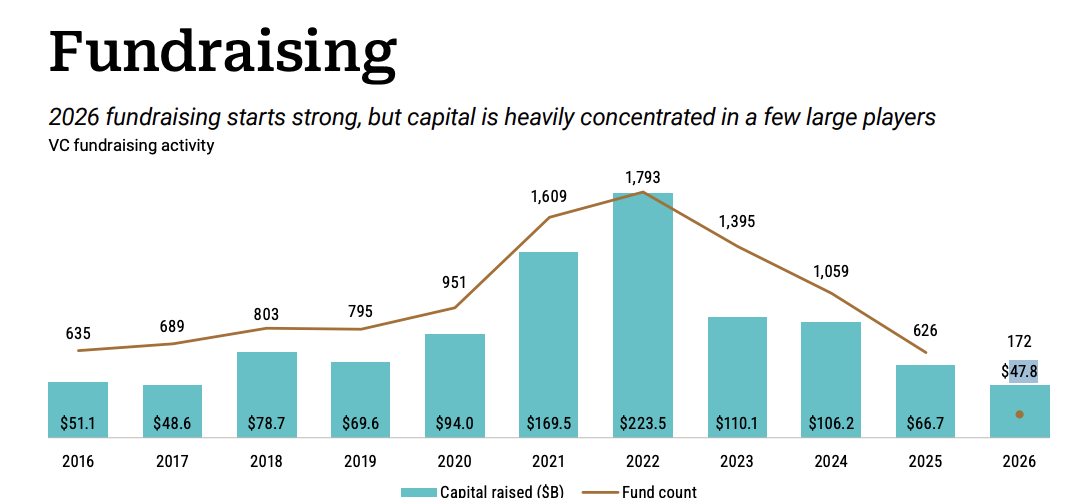

This is not a phenomenon unique to Crypto. The larger venture capital market is also concentrating on a small number of large managers. A capital market report for Q1 2026 jointly released by PitchBook and the National Venture Capital Association (NVCA) shows that U.S. VCs raised a total of $47.8 billion in Q1 2026.

This sounds quite strong, but capital is highly concentrated in a few large managers. Experienced managers took home 90.9% of the total raised amount, setting a new high for this dataset. At the same time, the median size of VC funds fell from $25 million in 2025 to $15.3 million in Q1 2026. Large funds appear to be larger, while small funds’ operational space is getting narrower.

Source: PitchBook and NVCA jointly released Q1 2026 capital market report

In the Asian market, this pressure is further amplified. Jocy Lin’s assessment of Asian Crypto VCs is sharper. He believes that U.S. funds have a more mature LP system and could still gain returns from investments in major cryptocurrencies like Bitcoin in the last round; Asian funds have a much thinner LP base and limited ammunition, so they must strike more certain opportunities with less money.

The path for mid-tier and small funds has shifted from "keeping up with all the hot spots" to "proving they have unique capabilities." Vivian, founder of Starbase, has a more direct judgment. She believes that "pure Crypto VCs have basically vanished, and funds will continue to concentrate at the top. Mid-tier institutions will find it difficult to survive using the previous round's pure financial investment approach if they cannot find vertical niches or move towards incubator and accelerator models."

Track Preferences Have Changed: New Money Is Bet on Crypto Embedded in Finance

As LP questions change, the fundraising narratives of GPs will also shift.

What is really interesting in this round is not the keywords in fundraising materials shifting from L1, NFT, DAO, SocialFi, and chain games to stablecoins, RWA, prediction markets, and AI; but rather that Crypto VCs are beginning to acknowledge that the growth most understandable to LPs is happening at the interfaces of the financial system.

From the narratives of new funds launched by a16z crypto, ParaFi, Haun Ventures, and Dragonfly, terms like stablecoins, tokenization, prediction markets, institutional DeFi, and agentic finance keep recurring.

They may sound different, but the commonalities are clear: they all attempt to integrate Crypto into financial processes, information pricing, or machine economies.

These directions can be broken down into four more core lines: Crypto x AI, stablecoins and payments, RWA and on-chain capital markets, and prediction markets.

The first line is Crypto x AI.

AI agents are a new variable.

Several VCs are putting AI agents into their focus tracks, but they are not simply concerned with the "AI + Crypto" concept.

Within IOSG's framework, the weight and assessment methods for Crypto x AI are more specific. Jocy Lin told Foresight News that IOSG will allocate 30% of its capital to Crypto and AI intersection fields, particularly in decentralized data services, DePIN, data collection, and B2B scenarios. His judgment is that AI demand is strong, but if Crypto x AI projects want to find business scenarios, they should start with B2B because revenue is easier to realize.

This means that IOSG's focus is not just on labeling projects with an AI tag. What it really wants to validate is whether the AI era will generate new credible data, machine payments, decentralized computing power, automated collaboration, and verifiable execution demands.

Haun Ventures lists the agentic economy as one of the three major focus areas of Fund II, believing that AI agents will complete more tasks on behalf of humans in the future: they will pay, transact, subscribe to software, and purchase services, while also automatically collaborating across different applications and creating entirely new paradigms of coordination, trust, and value exchange.

a16z crypto also mentions that software agents will represent user decisions, actions, and trades, while acquiring computing power, data, and services in the process. What blockchain can provide for AI agents are wallet identities, on-chain credentials, stablecoin settlements, smart contract constraints, and verifiable execution logs.

New themes of Dragonfly and ParaFi's funds also involve the agentic economy and payments, indicating that more Crypto VCs are looking for new financial execution levels in the AI era: who will provide identities, wallets, payments, transactions, data calls, and automatic settlements for agents.

It is noteworthy that Jocy Lin stated that social, gaming, NFTs, and other tracks have undergone large-scale disproof, but he did not completely exclude them. His judgment is that if these directions can be altered by AI in terms of production methods, IP play, or distribution logic, new opportunities may still arise. Furthermore, IOSG will be more cautious in investing in new public chains because the major public chain landscape is already relatively stable, and investments in new public chains are significant and developer migration costs are high, hence IOSG has basically stopped investing in new public chain projects.

The second line is stablecoins and payments.

The allure of stablecoins comes not only from the circulating scale already formed by USDT and USDC but also from their beginning to enter scenarios like cross-border payments, enterprise settlement, treasury management, and merchant collection. This means that stablecoins are starting to establish a commercial path for financial infrastructure.

a16z crypto, in its announcement of the $2.2 billion Fund 5, regards stablecoins as one of the clearest use cases in this cycle, believing that their usage continues to grow during downturns and is being utilized for savings, cross-border transfers, and payments.

McKinsey and Artemis estimate in their analysis that by December 2025, stripping out activities mainly driven by transactions, internal rebalancing, and automatic contract cycles, the actual payment scale of stablecoins will be about $390 billion, increasing more than double compared to 2024.

Compared to the global payment market, this scale still appears small, but the growth speed and application scenarios are already sufficiently clear.

The acquisitions by traditional fintech companies for such infrastructures are further validating this direction. Stripe acquired Bridge for $1.1 billion, Mastercard announced a maximum acquisition of BVNK for up to $1.8 billion, and Payward, the parent company of Kraken, agreed to acquire the Hong Kong stablecoin payment company Reap for up to $600 million.

These acquisitions indicate that stablecoin payments, settlement capabilities, and merchant networks are no longer just internal opportunities for Crypto-native companies but are also becoming infrastructures that traditional fintech companies are willing to buy with real money.

This change is also reflected in the ranking of tracks by interviewed VCs. Jocy Lin noted that IOSG Ventures is focusing on stablecoin payments, clearing and settlement, and on-chain credit—tracks with clear interfaces to traditional finance. Deng Chao indicated that HashKey Capital’s current three main lines are trading and financial market infrastructure, stablecoin payments and clearing networks, and RWA and on-chain capital market infrastructure. Vivian also lists consumer-grade stablecoins and payment applications as one of Starbase’s current most willing betting directions.

The third line is RWA and on-chain capital markets.

RWA has regained attention in this round, not because "moving assets on-chain" itself is new, but because it is beginning to approach the segments that traditional finance truly cares about: asset issuance, distribution, collateralization, trading, and settlement.

Citi's report, "Tokenization 2030," released in June 2026, predicts that the scale of tokenized assets globally could reach $55 trillion under the baseline scenario by 2030, and $80 trillion under a bull market scenario.

Actions by traditional financial institutions are also making this logic more tangible. Major market infrastructure providers, including DTCC, the New York Stock Exchange, and Nasdaq, have begun integrating tokenization into their core platforms.

For VCs, such projects are much easier to validate than many consumer narratives from the previous round. What the underlying assets are, who is responsible for issuing and custodying them, who will buy them, how cash flow is generated, how compliance identities are obtained, and how secondary liquidity is formed all directly impact whether a project can be established.

HashKey Capital and IOSG are both looking at these directions within the framework of financial industry innovation.

Deng Chao stated, "What attracts us in this direction is the combination of regulatory windows, institutional demand, and exit imagination. The key of RWA is not just putting assets on-chain, but whether it can enhance the accessibility, liquidity, transparency, and efficiency of the assets after being put on-chain."

Jocy Lin also mentioned that IOSG values on-chain credit (like Morpho), RWA, and other directions that have clear interfaces with traditional finance.

Haun Ventures’ expression of this direction is closer to "new assets and markets." They noted that "stablecoins are just the starting point, tokenization is expanding to currencies, securities, derivatives, and other real-world assets. Once issued in a tokenized way, these assets will become borderless, always online, and programmable financial primitives."

The fourth line is prediction markets.

For Crypto VCs, the allure of prediction markets comes not only from trading volume but also from their potential to develop into a new type of information market infrastructure.

From the perspective of Haun Ventures, prediction markets can naturally extend from tokenization logic. Haun Ventures believes that tokenization can create new market forms, as it can form a global liquidity pool without relying on separately constructed trading and settlement infrastructures in various regions. Prediction markets are a typical example. Although today's prediction markets mainly focus on sports and politics, in the future, they may give rise to event risk hedging, insurance, and commercial outcome markets, where the results of these markets can directly trigger conditional programmable cash flows.

a16z crypto researcher Scott Kominers is an economist who has long studied markets and incentive mechanisms. In an article published in June, he stated that "prediction markets can directly provide probability estimates, which is in itself a kind of 'superpower.' Its investment implications go beyond simply 'betting on event outcomes' to integrating dispersed information, incentive mechanisms, event validation, contract settlements, and transparent auditing into the same market structure."

However, the rapid influx of funds can also raise entering costs. Jocy Lin suggests that the prediction market track has already shown signs of capital concentration, and projects like Polymarket may face issues of overvaluation.

These directions share a common thread: they are easier to integrate into real financial processes or information pricing.

The projects currently favored by Crypto VCs can no longer primarily rely on grand narratives and future Token liquidity to support valuations; they need to engage with real trading demands, institutional distribution networks, financial ledgers, or new automated processes in the AI era.

Investment Strategies Have Changed: Looking at Primary, Secondary, and Exit All at Once

As LP requirements tighten and VCs focus more on tracks closer to real financial processes, the strategies of Crypto VCs have started to shift from "investing" to "how to catch and exit."

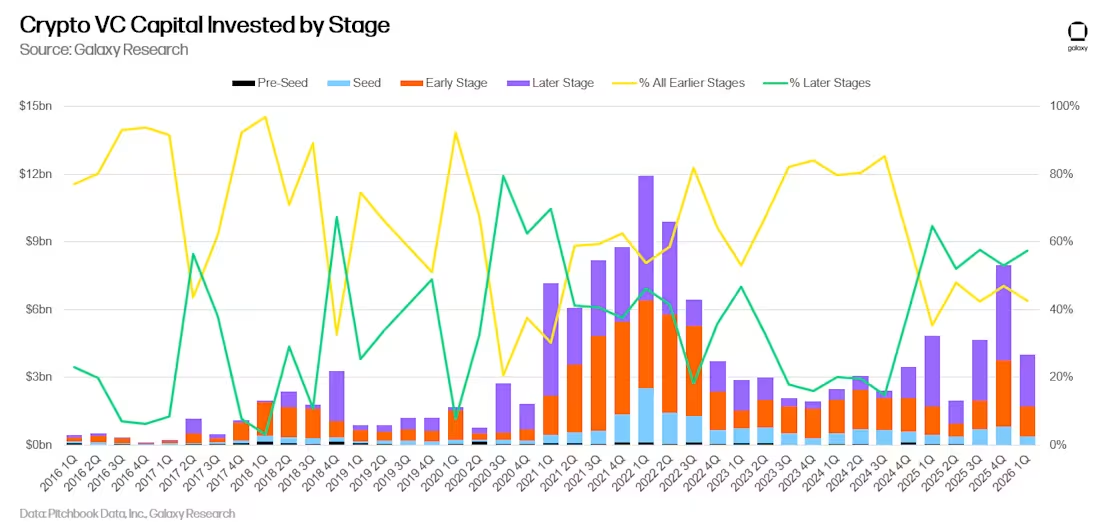

The distribution of investment stages has provided a signal. Galaxy Research noted in the Q1 2026 report that 57% of capital in the first quarter flowed to later-stage projects, while younger companies secured about 43%; in terms of the number of investment transactions, Pre-Seed rounds dropped to 19%, with later-stage transactions accounting for about a quarter.

Source: Galaxy Research

This does not mean early investments are unimportant. Variant still emphasizes investing in the earliest rounds, Haun Ventures will also layout early and late stages simultaneously, and a16z crypto highlights whether projects can enter real user scenarios like finance and payments.

The real change is that early judgments must be placed alongside product validation, revenue validation, compliance paths, and exit paths on the same table.

This change also reflects a more micro market feel. On June 15, Jademont, founder and CEO of Waterdrip Capital, mentioned on X that some teams only wish to secure $36,000 when raising funds, claiming it is the actual cost after rigorous accounting. Jademont believes that the industry's more practical approach may be a signal of hitting rock bottom.

In specific allocations, some VCs have already started to manage primary, secondary, and off-market opportunities within the same portfolio.

Multicoin Capital has built a heavy position in the privacy coin ZEC since February of this year.

IOSG's portfolio adjustments also reflect this shift in strategy. Jocy Lin stated that "IOSG maintains an annual total investment quantity of about 15 projects, with 30% as lead investments. Due to market conditions, the number of quality projects in the primary market has decreased, resulting in a slowdown in disclosed investment frequency, but the overall activity has been maintained through Post-TGE and OTC transactions. IOSG adjusts its investment ratio to: 50% primary market, 30% Post-TGE, and 20% OTC, to capture severely undervalued secondary market opportunities." Jocy Lin revealed that he personally comes across 3-5 offline projects every week, maintaining a high-intensity project screening rhythm throughout the year.

This ratio may be more suitable as a single institutional case, but it reflects a broader shift: Crypto VCs are transitioning from merely investing in primary projects to simultaneously managing primary, secondary, Post-TGE, and OTC opportunities.

Many Post-TGE projects already have cash flow and user growth, but their token values have not been fully priced by the market, and these opportunities were often overlooked in the last round of hot money cycles. For investment teams, assessing a project cannot simply be based on financing rounds; they must also consider its repricing opportunities in the secondary market, off-market liquidity, and token value capture.

HashKey Capital's changes emphasize the discipline of the investment framework itself and cross-cycle allocation capabilities. In the past year, their biggest optimization has been to make the investment framework more disciplined, systematic, and verifiable. The team remains active but is more disciplined in terms of investment frequency compared to previous years, preferring to invest in teams that have proven capable of doing business, as these projects tend to be more resilient during downturns.

This round of fundraising employs a multi-strategy structure that will combine primary markets, public markets, OTC, PIPE, convertible bonds, and some more liquid cross-investment opportunities.

Starbase has adjusted its strategy to focus on fewer, higher-quality projects with depth of operation. Vivian mentioned that Starbase will incubate no more than three key projects per cycle, no longer pursuing widespread investment but rather concentrating resources to support key teams in vertical tracks like RWA, AI Agents, consumer-grade stablecoins, and payment applications.

AI is also changing the workflow of VCs themselves. Jocy Lin observed that AI is leading the global capital markets to exhibit certain "Crypto-like" characteristics: information distribution is faster, ordinary investors' judgments and trading decisions are more easily amplified by AI, and capital can more easily concentrate towards a few of the most certain targets. For VCs, interpersonal judgment and trust are still hard to replace, but data observation, statistics, back-testing, and cross-timezone collaboration processes have started to be rewritten by AI Bots.

The change in strategy will also impact the due diligence level.

Crypto VCs have not stopped taking risks; they have merely made their risk budgets more disciplined.

This discipline is first reflected in changes in due diligence questions. HashKey Capital's due diligence has shifted from narrative coverage to hypothesis validation: the era of looking at every new narrative has passed; projects now need to answer who the customers are, who pays, why there is a real need now, if there is genuine retention and natural demand, how value will ultimately be captured, and whether the team has long-term execution and capital management capabilities.

At the project level, the granularity of verification will become finer.

Jocy Lin of IOSG broke down these due diligence changes further. Income is no longer only looked at in aggregate; it should be broken down into revenue structure: how much do hardware sales, node sales, subscription fees, protocol fees, and recurring revenues each account for, and is the ARR sustainable. Consumer projects also cannot just report attractive user numbers; retention rates, conversion rates, payment behaviors, and retention of such granular data are starting to enter the basic checklist of VCs.

In other words, the due diligence language of Crypto VCs is turning towards unit economics, cost structures, gross margins, and long-term value capture.

Jocy Lin’s reminders sound more like risk memoranda for entrepreneurs. He believes that the key indicators for projects that can survive this round have already shifted from TVL or MAU to cash flow. He also emphasized that tokens are actually a form of liability; if they can be avoided, they should be; if they can be issued later, they should do so.

According to internal observations from IOSG, the median comprehensive listing costs that projects bear on leading exchanges during the cycle from 2024 to 2026 amount to about $8 million, which includes structured costs like margins. This figure may not apply to all projects, but it reveals a problem obscured by the previous bull market: issuing tokens does not equate to exiting; often, it merely cashes out future liquidity pressure in advance. The valuation at which projects raise funds today determines what metrics they must achieve over the next three years to catch the next round. If they cannot catch it, they should not fundraise.

As project selection and due diligence standards change, the post-investment value of VCs also needs to be reevaluated.

In the past, funds that could help projects with financing, ecological BD, and exchange relationships were already considered valuable. Now, invested projects need more such as regulatory communication, institutional client referrals, and expansion into Asian markets. Deng Chao mentioned that HashKey Capital will place greater emphasis on connecting institutional clients, expanding into Asian markets, compliance resources, trading and liquidity resources, ecological cooperation, follow-on financing, and brand building in their post-investment approach.

The change in exit paths is the final link in the strategy change.

In the past, Crypto VCs could assume tokens were the core exit channels. Now, exit paths are becoming more complex: IPOs, strategic acquisitions, secondary market exits, and Post-TGE liquidity management all begin to be prioritized in VC investment judgments.

The earlier mentioned acquisition chain of stablecoin payment infrastructure is a signal: when Crypto projects can integrate into real financial processes such as payments, custody, trading, brokerage, and clearing and settlement, their exit targets are no longer just exchanges and the secondary market but also include payment companies, exchanges, banks, brokers, custodians, or fintech platforms.

This has direct significance for VCs: if a project can be understood, integrated, and priced by traditional financial or fintech buyers, it becomes easier to form an exit story that LPs can understand. Tokens are still important, but they are no longer the only answer.

Why Is This Happening?

This round of changes is not due to VCs suddenly becoming conservative; it is being simultaneously squeezed by four forces.

First, the trauma from 2022 to 2023 lingers.

FTX, Terra, Three Arrows Capital, and a series of bankruptcy events shattered LPs' trust in Crypto. Many projects, after raising high valuations in the last round, had neither revenue nor real users, ultimately resorting to issuing tokens to create paper exits for early investors.

LPs are now questioning liquidity, custody, counterparty risks, and compliance disclosure, which is a reflection of cycle memory.

Second, AI has captured global venture capital's attention.

According to Crunchbase statistics, in Q1 2026, about 6,000 startups worldwide received approximately $300 billion in venture capital, an increase of more than 150% quarter-over-quarter, of which AI companies obtained about $242 billion, accounting for about 80%.

This indicates that competing with Crypto for LP attention is not just other Web3 narratives, but also a broader range of AI and later-stage tech assets.

As AI absorbs capital at such an exaggerated pace, Crypto VCs can no longer claim "the next generation of the internet" to seize LP imagination. They must prove their irreplaceable position in the AI era, such as in machine payments, agentic identities, verifiable data, decentralized computing power, compliant settlements, and on-chain financial execution layers.

Third, institutional clients are starting to genuinely go on-chain.

Stablecoin payments, tokenized U.S. Treasury bonds, on-chain clearing and settlement, RWA perpetual contracts, prediction markets, and institutional trading infrastructures are transitioning Crypto from retail speculation to more complex financial scenarios. Institutions will not migrate processes for a pretty narrative; they will only do so for cost, efficiency, regulatory feasibility, and new revenue migration processes. This naturally shifts the judgment standards of Crypto VCs closer to those of traditional finance.

Fourth, the U.S. policy environment has improved significantly.

Since 2025, U.S. regulatory signals have shifted from enforcement to rule shaping. The SEC has provided a clearer explanation for the application of securities laws to digital assets, and discussions on the boundaries between the SEC and CFTC have started becoming more concrete; in May 2026, the U.S. Senate Banking Committee advanced the CLARITY Act.

Regulatory uncertainties have not disappeared, but policy signals have shifted from mere enforcement to rule shaping. For VCs, this will enhance the investability of projects related to compliance payments, stablecoins, custody, RWA, and market structures.

These forces together push Crypto VCs toward a tougher evaluation system. LPs want to see DPI and risk control, GPs need to explain the liquidity and exit paths in their portfolios, and entrepreneurs must demonstrate that their projects are not just waiting for the next round of market mood.

In the previous cycle, Crypto VCs often priced for a future that had not yet fully formed. By 2026, the market is requiring entrepreneurs to lay more on the table: income structures, customer lists, compliance paths, token value capture, and exit solutions must withstand scrutiny.

This does not mean that Crypto no longer needs imagination—in fact, stablecoins, RWA, prediction markets, and AI agents still require new market imagination.

The change lies in the fact that imagination must be connected with verifiable demand, cash flow, compliance paths, and value capture mechanisms.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。