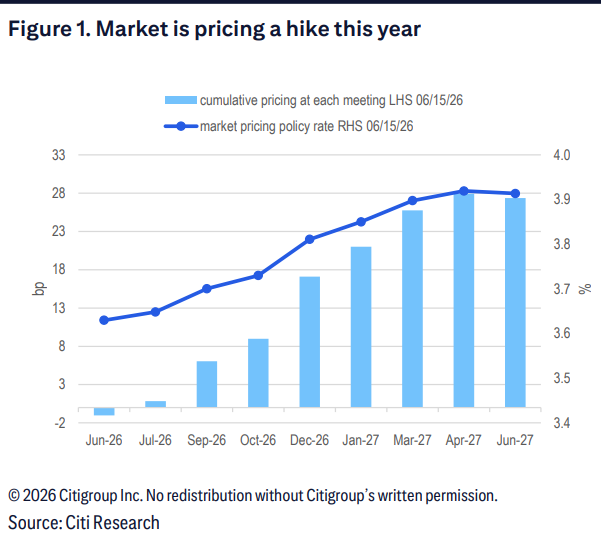

The probability of a dovish signal being released by Wash at this week's FOMC meeting is tilted upwards, and the two-year U.S. Treasury yield still has significant room for downward movement, with a rate cut potentially imminent.

Written by: Zhao Ying

Source: Wall Street Insights

Two major catalysts for declining inflation are simultaneously developing, providing sufficient basis for Federal Reserve Chairman Wash to shift towards a dovish stance at this week's Federal Open Market Committee (FOMC) meeting.

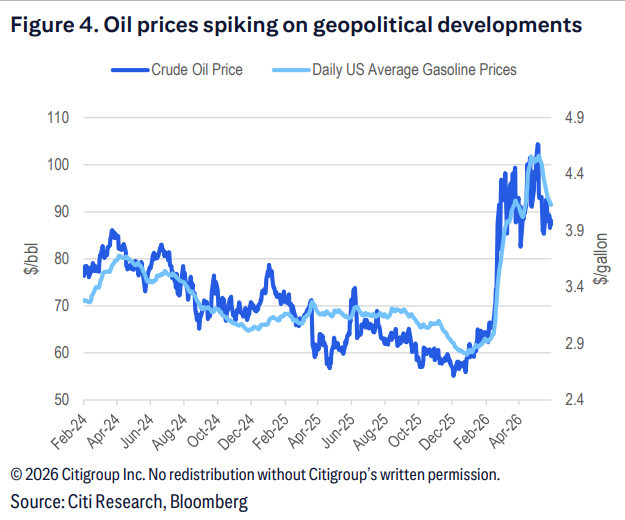

According to the Wind Trading Desk, Citigroup Research released a report on June 15 stating that the planned reopening of the Strait of Hormuz will drive oil prices down, eliminating upward risks of energy prices on inflation; at the same time, last week's core CPI data was notably weak, recording only a 0.21% month-on-month increase.

The combination of these two developments further weakens the rationale for the Federal Reserve to maintain a hawkish stance, and the path for rate cuts has once again come to the forefront.

For the market, this judgment has direct pricing implications. The two-year U.S. Treasury yield has decreased by about 13 basis points compared to a week ago, but it is still over 60 basis points higher than in February. The market currently still has room to compress expectations for rate hikes, and there is also further room to enhance expectations for rate cuts.

Energy price pressure eases, inflation upward risks diminish

The expectation of reopening the Strait of Hormuz is one of the core drivers of this dovish logic. Once the strait is reopened, the increase in crude oil supply will lead to lower oil prices and other energy prices.

Gasoline prices have fallen for a month straight, with the national average dropping from about $4.50 per gallon to $4.00, and Citigroup expects this trend to continue alongside further declines in other energy commodities. This trend is expected to yield several months of negative overall inflation readings in the coming months and will prompt Federal Reserve officials to shift the characterization of energy prices from "inflation risks" to "neutral or even deflationary factors."

Core CPI cools, inflation indicators become more divergent

At the core inflation level, while the May core PCE is expected to remain strong, the core CPI has shown clear signs of cooling, with a month-on-month increase of only 0.21%.

The core PCE has increasingly become an "outlier" among various inflation indicators—truncated mean PCE and core CPI both are closer to target levels, and the downward trend is clearer. This divergence is becoming more widely recognized by the market and Federal Reserve officials, providing data support for a dovish stance.

FOMC hawkish adjustments have been fully priced in, dovish statements have upward room

The report estimates that this week's FOMC statement will remove the wording of "accommodative bias," and the median of the dot plot will also show maintaining the rate unchanged this year. However, the aforementioned hawkish adjustments have been fully expected by the market and do not constitute new information.

The real variable lies in Wash's wording orientation. In light of the latest developments regarding the reopening of the Strait of Hormuz and the cooling trend in core inflation, the risk of Wash releasing dovish signals at this meeting is tilted upwards. If his wording is milder than expected, the market's repricing on the rate cut path may accelerate.

U.S. Treasury yields still have downward space, market pricing has room for adjustment

From the perspective of market pricing, the report argues that the current implied probability of rate hikes in interest rate futures remains high. Although the two-year U.S. Treasury yield has decreased by about 13 basis points compared to a week ago, it is still over 60 basis points higher than February levels, indicating that the market has not fully absorbed the impact of easing inflation risks.

As the inflation upward risks that previously supported hawkish expectations gradually dissipate, the market is expected to further compress rate hike pricing while simultaneously enhancing rate cut pricing, and U.S. Treasury yields still have downward space.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。