How should the account for Plasma U Card be calculated? Is it worth locking XPL?

Written by: KarenZ, Foresight News

After the U Card rolled out to AI subscriptions, Plasma found a new entry point for locking assets.

On June 12, Plasma launched three types of U Cards, which will be open to all users this week.

On the surface, this is a membership system for stablecoin consumption cards. But what users see are basic cashback and AI benefits, airport cashback, and Visa consumption scenarios. The project team is focused on longer-term consumption frequency, holding tokens, and locking assets.

How the three types of cards are divided: Lite attracts new users, Core targets AI users, Platinum locks in big holders

Before discussing the benefits, it is necessary to clarify the product boundaries of Plasma One. According to the official website, the global account service for Plasma One is provided by Bridge, and the Plasma One card is primarily issued by Visa member Rain under Visa authorization, applicable in countries and merchants accepting Visa cards. In other words, Bridge is more focused on account services, while Rain focuses on card issuance and Visa payment channels. Ultimately, users experience a stablecoin consumption card connected to the Visa network.

Lite is the entry point with the lowest threshold. The official site indicates that the Lite card costs 0 dollars, offers a basic cashback of 2%, and provides 1 free virtual card. It is suitable for users who only want to try a stablecoin card and do not temporarily wish to buy XPL or lock assets.

Core targets everyday AI users. It provides a 3% basic cashback, a 5% AI consumption cashback, a ChatGPT Go subscription, and up to 2 free virtual cards. The way to obtain Core is either by paying 120 dollars annually or by locking 10,000 XPL for 12 months. It is important to note that the Core page specifies that the 5% AI cashback applies to a maximum of 500 dollars of AI consumption per month. Here, the 500 dollars refers to the maximum consumption limit, not the cashback limit.

Platinum is more like a high-consumption card. The official page states that it is designed specifically for major XPL holders, and the way to obtain it is by locking 100,000 XPL for 12 months without needing to pay any extra fees. Benefits include a 4% basic cashback, a 10% AI consumption cashback, Claude Pro and ChatGPT Plus subscriptions, up to 600 dollars/year in flight cashback, VIP lounge access, Visa concierge services, car rental insurance, travel insurance, baggage delay and loss coverage, global eSIM, and more.

The Platinum product page also highlights cashback and benefits with a total value exceeding 10,000 dollars per year, including a basic cashback of 7,500 dollars, an AI credit of 1,400 dollars, and an airline credit of 600 dollars, but these are closer to marketing assumptions and do not guarantee that users can unconditionally receive the full amounts.

Is it worth it: Lite can be tried, Core looks at AI consumption, Platinum considers asset volatility tolerance

First, let’s look at Lite. Its advantage is simplicity: a 0-dollar card fee, a 2% basic cashback, and no asset locking. The drawbacks are clear: no additional category bonuses, no AI subscriptions, and no travel benefits. For most ordinary users, Lite is the most suitable option to dip their toes in because it does not push you directly into XPL price fluctuations.

The key issue with Core is whether the 120-dollar annual fee or 10,000 XPL locked can be covered by real transactions. Based on the value of 0.088 dollars/XPL calculated on June 15, locking 10,000 XPL roughly equates to 880 dollars.

If you do not lock XPL, you need 120 dollars to register for the Core card. Comparing ordinary consumption between Lite and Core, Core provides a 3% basic cashback, while Lite offers 2%, resulting in a difference of 1 percentage point. To cover the 120-dollar annual fee with this 1 percentage point, around 12,000 dollars of annual qualifying consumption is needed.

If we focus mainly on AI consumption, Core’s benefits should be calculated separately: the official website states that Core provides a 5% AI cashback, applicable to a monthly maximum of 500 dollars of AI consumption; Lite clearly does not provide AI cashback. Therefore, based on the AI-specific cashback calculation, covering the 120-dollar annual fee requires 2,400 dollars of annual qualifying AI consumption, which is about 200 dollars per month. If AI consumption is filled up to the 500 dollars limit each month, Core can earn about 25 dollars in AI cashback monthly, totaling about 300 dollars for the year. Additionally, with the ChatGPT Go subscription benefits, Core is more suitable for users who already have ongoing AI tool expenses.

However, if users choose to lock 10,000 XPL instead of paying the annual fee, this calculation cannot be based solely on cashback. The real cost of the locked version of Core comes from XPL price fluctuations and the 12 months of liquidity occupation, which should not be simply viewed as getting a card for free.

Platinum has a higher threshold. 100,000 XPL is about 8,800 dollars and requires a 12-month lock. It is suitable for three types of people: users who are already heavily invested in XPL, those with high AI and travel expenditures, and large holders who can accept a year of asset locking and price fluctuations.

The AI benefits of Platinum are also more substantial: in addition to the 10% AI consumption cashback, it includes subscriptions for Claude Pro and ChatGPT Plus. For users who are already long-term users of Claude Pro and ChatGPT Plus, these two subscriptions can be seen as real cost offsets. However, for those who just temporarily lock their assets to get the card, they are more like additional perks and do not offset the price volatility risks brought by locking 100,000 XPL for a year.

Relying solely on the 4% basic cashback to achieve the 7,500 dollars in value displayed on the page necessitates about 187,500 dollars in qualifying consumption; the maximum 600 dollars in flight cashback, calculated at 10%, also corresponds to about 6,000 dollars in qualifying airline ticket consumption. For ordinary users to buy 100,000 XPL temporarily for benefits, the risk-reward ratio does not look favorable.

Moreover, there is another layer of risk from terms. Plasma One cashback is initially calculated in dollars and then converted to XPL based on the XPL/USD price at the time of issuance. Rewards might go through a pending period, and issues such as transaction refunds, chargebacks, unusual consumption, or arbitrage-style card usage could trigger confiscation or recovery. The terms also state that Plasma can adjust reward rates, monthly caps, qualifications, exclude transactions, distribution cycles, and referral reward structures. It is best to factor in these variables before estimating benefits based on full cash flow valuations.

What impact will it have on XPL?

The most direct impact of the Plasma U Card on XPL is that it has added a membership attribute to the token. Previously, the narrative surrounding XPL primarily came from the Plasma chain itself and zero-fee USDT transfers. Now, Core and Platinum bind XPL to consumption benefits, prompting users to hold XPL for AI subscriptions, cashback, travel perks, and card levels.

Plasma documentation indicates that the initial supply of XPL is 10 billion tokens, of which 10% is for public sale, 40% for ecology and growth, 25% for the team, and 25% for investors; within the ecology and growth portion, 800 million tokens will unlock on September 25, 2025, when the mainnet beta goes live, while the remaining 3.2 billion tokens will be released linearly over 3 years.

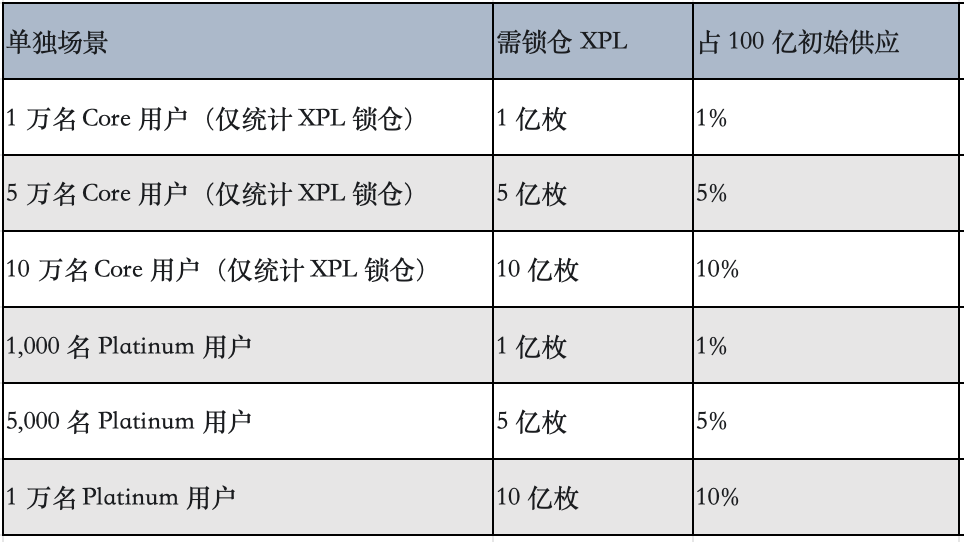

Let’s look at the locking effects through a few scenarios:

The meaning of this table is straightforward: Core needs scale, while Platinum requires big holders. With just 1,000 Platinum users, it can lock 100 million XPL; with just 10,000 Platinum users, it can lock 1 billion XPL, accounting for 10% of the total initial supply.

More crucially, it compares with the unlocking rhythm. In the ecology and growth distribution, the remaining 3.2 billion tokens will be released within 3 years (fully unlocking by September 25, 2028), equating to about 88.89 million tokens per month. To absorb one month's ecological release, about 8,889 Core users locking XPL, or 889 Platinum users, would be needed.

The allocation for the team and investors totals 5 billion tokens, with a one-year cliff unlocking one-third on September 25, 2026, approximately 1.667 billion tokens; to fully hedge this amount using cards, around 166,667 Core users locking XPL, or 16,667 Platinum users, would be necessary. This number is already significant, indicating that the Plasma One card levels can improve the circulation structure but find it difficult to digest large releases in the future alone.

Another variable is inflation. Plasma plans to launch validator rewards after external validators and delegated staking go live, starting with an annual inflation of 5%, decreasing by 0.5 percentage points each year until stabilizing at a long-term baseline of 3%; at the same time, it will offset new issuance through a base fee burning mechanism similar to EIP-1559.

Based on the 10 billion initial supply, 5% annual inflation corresponds to 500 million XPL, and to cover this in one year requires locking in 50,000 Core users or 5,000 Platinum users.

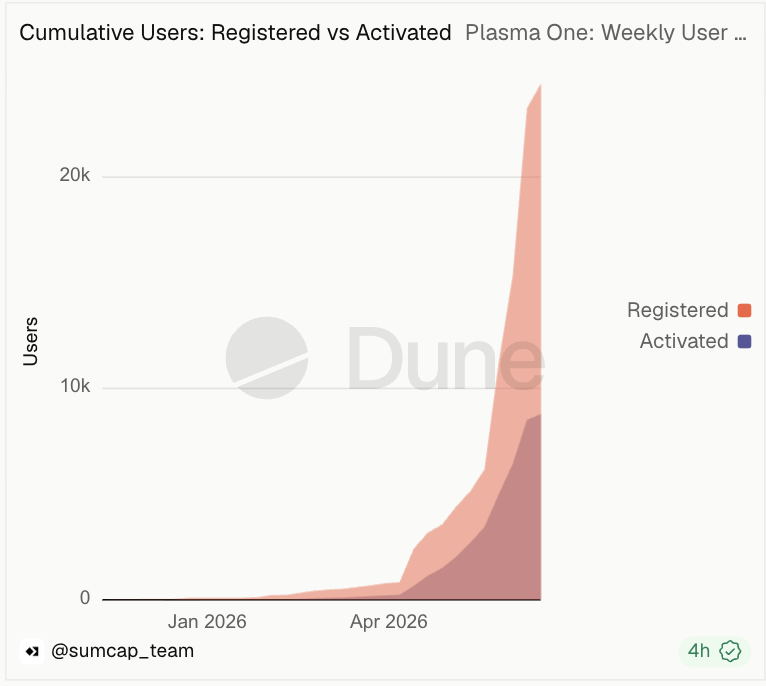

According to a Dune dashboard created by Sumcap, Plasma One currently has 24,000 cardholders, having activated 8,884 cards.

The positive effect of this action on the token is clear: it gives XPL a non-speculative holding reason, reduces some circulation, and expands XPL's reach.

The negative effect is also clear: cashback is issued in XPL, and if users treat it as a cash equivalent, they may sell it directly upon receipt. Of course, this part will be gradually digested.

One more point is that the official has not currently disclosed the specific source of the rewards for XPL, which determines whether it will ultimately be net buying, net distribution, or a mix of both.

The true experiment of Plasma

The counterintuitive aspect of Plasma is this: the smoother the zero-fee USDT transfers, the less ordinary users need to actively hold XPL to pay Gas. Membership locking provides XPL with an additional demand curve. It takes users from exchanges, airdrops, and staking pages to more everyday scenarios: swiping Visa cards, receiving cashback, subscribing to AI tools, and more.

This is good for the project itself. Stablecoin public chains are easily measured by TVL and subsidies by the market; Plasma One provides a consumption finance entry point, establishing a link between XPL and real payment frequency. However, this path is more difficult to tread. Users won't swipe cards daily due to public chain narratives; they will stay for rates, exchange, risk control, customer service, regional coverage, and reward fulfillment.

For XPL, Plasma One Tiers is a useful experiment for locking assets and distribution but cannot substitute for real transaction volumes, stablecoin liquidity, and subsequent unlocking management.

It is more like a door that presents on-chain assets to everyday consumption. The door is open; now we must see how many people truly come in and out from here every day.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。