Original | Odaily Planet Daily (@OdailyChina)

Author|Golem (@web3_golem)

On June 12 local time in the U.S., Musk did not go to New York. Before SpaceX's stock (Nasdaq: SPCX) officially launched on Nasdaq, he chose to stay at the company's Texas headquarters, among a group of employees, and completed a remote bell ringing.

During this ceremony, Musk once again took SpaceX’s story to a broader audience. He stated that the company's goal is to send humanity to the moon, Mars, and even farther into interstellar space. After the bell ringing, Nasdaq’s live streaming channel played Elton John’s "Rocketman," adding a romantic note to the most high-profile IPO in the history of space commercialization.

However, the sentimental segment ended there, and the game of capital markets began. SpaceX's IPO was priced at $135, starting its first trading day at $150, briefly rising above $176 during the session, and ultimately closing at $160.95, with a temporary market capitalization fixed at $2.1 trillion.

Opened at $150, with a first-day market capitalization fixed at $2.1 trillion

The IPO of SpaceX has drawn global attention since it submitted its IPO declaration information to the U.S. SEC, with the company ultimately deciding to issue approximately 555.6 million Class A common shares at a fixed price of $135, corresponding to a company valuation of $1.77 trillion.

In terms of stock distribution, Musk personally holds about 42%, Valor Equity holds about 7.3%, Google holds about 5%, other early venture capital firms combined hold about 10% to 12%, and employees and former employees hold about 10% to 15%. The shares publicly issued in this IPO only account for 4.2%. Although Musk and the surrounding interest groups hold the majority of SpaceX shares, their holdings cannot be sold on the day after the listing; Musk and core investors like Valor Equity are subject to a lock-up period of 366 days, while ordinary IPO shareholders (institutions and employees) must also undergo a 180-day base lock-up, meaning they cannot sell until at least the end of 2026.

As a result, on the listing day of June 12, the initial circulating volume was only the approximately 555.6 million Class A common shares publicly issued in the IPO. SpaceX is considered a typical "low liquidity, high FDV" project; according to its valuation model, the initial circulating market value was around $75 billion, which was just about the amount SpaceX originally planned to raise.

Investors who frequently engage with cryptocurrency projects may not be unfamiliar with high control models. Therefore, during the subscription phase, market sentiment quickly fell into FOMO, with reports stating that SpaceX received more than four times oversubscription. Total subscription demand from institutional and retail investors exceeded $250 billion, with retail investors alone breaking the $100 billion mark, far exceeding the $75 billion issuance scale; of course, cryptocurrency players also participated in this feast, but unfortunately, most people “came back empty-handed.” (Related reading:SpaceX On-chain New Shares Dream Shattered: Trillion Dollar IPO Feast, I Only Got 4 Shares)

It is worth noting that SpaceX plans to allocate as much as 30% of its IPO shares to retail investors, significantly lowering the participation threshold for this tech feast. Typically, such large IPO projects only allocate 5% to 10% to retail investors. Although SpaceX ultimately allocated about 20%, it is still double the regular IPO allocation.

The reason for this is that SpaceX management believes retail investors will hold their stocks for the long term, similar to Tesla's core group of investors, which includes many retail investors. They fundamentally believe the retail public will pay for the dream Musk describes, but this time the retail investors are much more rational than they imagined. (Details below)

Before SPCX officially began trading on Nasdaq, pre-market quotes for SPCX on Hyperliquid fluctuated between $170 and $175, corresponding to a company valuation exceeding $2.2 trillion. Just before official opening, during Nasdaq's collective auction phase, the opening indicative price for SPCX was initially reported at $172, about 29% higher than the IPO price, aligning well with pre-market expectations. However, an hour later, SPCX's opening indicative price quickly dropped and ultimately opened at $150, only about 11% higher than the IPO price.

According to Gate’s U.S. stock market data, SPCX eventually rose to around $176 during the session, closing at $160.95, about 19% higher than the IPO price, but only about 7.3% higher compared to the opening price. The first-day market capitalization was fixed at $2.1 trillion. Overall, SpaceX's performance on its first day of trading can be considered successful, making Musk the world's first trillionaire. However, this result is not particularly impressive and did not fully meet market expectations.

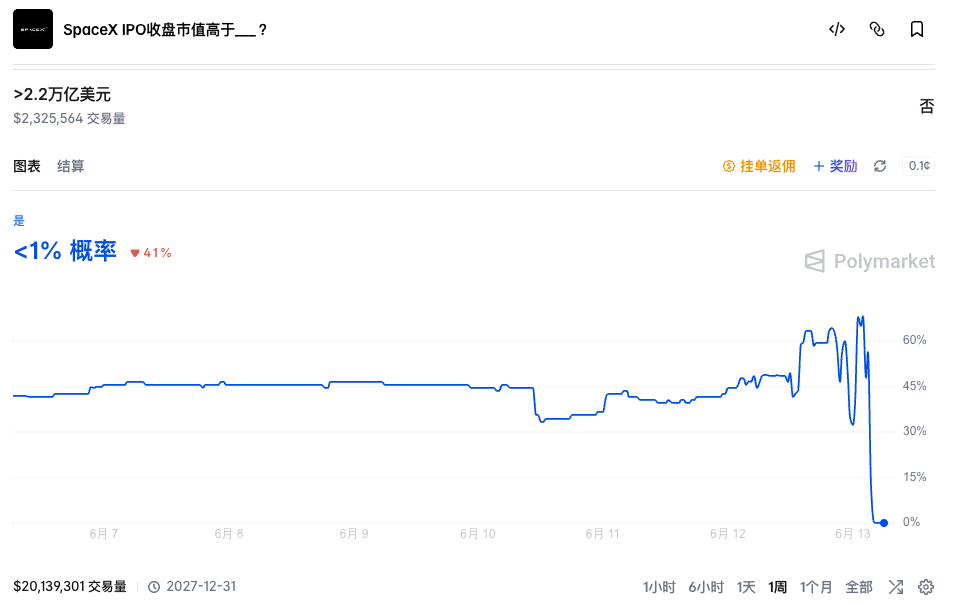

In the advance pricing of SpaceX, not only did some pre-IPO platforms misfire, but the predictive market was also rather inaccurate. In the hours leading up to SpaceX's IPO, the market generally believed its market capitalization could reach over $2.2 trillion, with the probability on Polymarket that "SpaceX IPO's closing market capitalization exceeds $2.2 trillion" at above 65%, briefly rising to 70%.

However, as SPCX opened "relatively low," that event probability began to fluctuate dramatically, ultimately settling at a closing market capitalization near $2.1 trillion, and the event was settled as a no.

Retail investors influence volatility, not price increase

The reason for this phenomenon is simple: even though the market is still willing to believe SpaceX's narrative and the "Musk premium," SpaceX is still too expensive; no matter how strong a belief, it can be sold if there’s a good price.

SpaceX is the first super giant in human history to directly land on the capital market with a "trillion-dollar" valuation; on its first day of trading, its market capitalization surpassed tech giants like Meta and Samsung, becoming the ninth largest company globally by market capitalization. However, even the most fervent retail investors know that SpaceX’s current revenue cannot support its massive valuation. SpaceX has yet to achieve profitability, with a projected net loss of $4.9 billion for the full year of 2025 and a net loss of about $4.28 billion for Q1 2026.

Starlink is currently SpaceX's only profitable business. According to the prospectus, the Starlink business is expected to generate $11.387 billion in revenue for the entire year of 2025, accounting for 61% of SpaceX's total revenue, with an operating profit of $4.423 billion. Its global user base has exceeded 10.3 million, with more than 9,600 satellites in orbit, and it achieved revenue of $3.257 billion in Q1 2026, with an operating profit of $1.188 billion. But this "cash cow" business is merely an auxiliary to SpaceX.

Aerospace launches are SpaceX's flagship offering. By the time the prospectus was disclosed, the Falcon series rockets had cumulatively launched over 650 times, with a success rate of 99%. Its rocket booster recovery technology has formed significant cost advantages and technical leadership in the industry. However, SpaceX's largest external customer for launch services is the U.S. government, and it is still operating at a loss, with a projected operational loss of $657 million for the entire year of 2025, representing a loss rate of 16.1%, and the operational loss for Q1 2026 soaring to $662 million, amounting to a loss rate of 107%.

The substantial losses stem from SpaceX increasing investments related to the Starship program, but based on current technological limitations and usage scenarios, Starship is still far from achieving true commercial mass production.

In addition to these two businesses, SpaceX’s somewhat speculative space computing sector is also part of its valuation system. Compared with the mature businesses of Starlink and aerospace launches, Musk's claims in the space computing segment do seem somewhat exaggerated.

SpaceX’s plan, simply put, is to send GPUs into low Earth orbit, utilizing solar power to provide cloud computing power for global AI computing clusters. Musk stated in SpaceX's prospectus that the goal is to deploy 100GW of AI computing capacity in orbit each year. Currently, the global AI industry demands about 15-25GW of electrical power annually, meaning the planned orbital computing system could theoretically support a nearly fivefold expansion of the current global AI industry scale.

In case readers are unaware of what 100GW entails: the current capacity of the Three Gorges Dam is about 22.5GW, meaning that Musk's proposed space computing center would be equivalent to 4.4 fully operational Three Gorges Dams.

Moreover, SpaceX clearly mentioned in its prospectus that future (primarily AI-related) business has the potential to tap into a market worth $28.5 trillion. To put this into perspective, China's nominal GDP in 2025 is estimated to be about $19.4 trillion. This figure proposed by SpaceX is equivalent to 1.47 times China's nominal GDP in 2025.

Reading through this information, one might wonder whether this is an IPO prospectus or a sci-fi short story, and even the most FOMO-driven investors might need to cool down after seeing these figures. The research agency CFRA rated SpaceX with a "Sell" rating following its IPO, setting a target price of $115.

In addition to the actual business not matching the valuation, the high proportion of retail investors in the IPO may also be a reason for SPCX’s price being suppressed. Musk allocated 20-30% of SpaceX's IPO shares to retail investors. The higher the proportion of retail holdings, the larger the inherent volatility. Retail investors can buy in without regard for cost due to FOMO sentiments and may also sell emotionally and thoughtlessly due to minor fluctuations. Thus, retail investors primarily influence volatility rather than the final price increase.

Important upcoming gambling time points

Of course, whether you are holding a short position or have already cashed out, the following three time points are particularly important for investors interested in SpaceX.

Approximately 15 trading days after the IPO (expected around July 6 - July 7)

This is the most important time point because SpaceX is expected to enter the Nasdaq 100 Index 15 trading days after its listing. In March, Nasdaq specifically modified its rules; originally, newly listed companies had to wait three months to qualify for inclusion in the index, but now they can be quickly included after listing for 15 trading days as long as they meet the conditions, and the requirement for at least 10% float has been removed. These new rules appear to be tailor-made for SpaceX and subsequent AI tech giants.

If SpaceX successfully enters the index, it means that over $10 billion globally will be passively invested in SpaceX's stock, becoming a significant support for its share price. So, knowing that there is a high probability SpaceX will be included in the Nasdaq in July when top-tier funds will buy this stock, would you, as an investor, choose to buy in advance now and then sell at a high price to them later?

However, on the other hand, some U.S. pension funds and long-term insurance funds have already expressed opposition. In May 2026, three of the largest public pension fund management organizations in the U.S. (managing over $1 trillion in assets) jointly sent a letter to Musk, expressing concerns about the risks of passive funds that may result from rapid inclusion in the index after the IPO. In the same month, Randi Weingarten, president of the American Federation of Teachers (representing about 1.8 million teachers, healthcare professionals, and public sector workers), directly wrote to the SEC calling for a special review of the SpaceX IPO.

SpaceX Q2 earnings report release (early to mid-August)

The second important time point is the release of SpaceX's Q2 earnings report for 2026 in August, which will be SpaceX's first performance report since its IPO. If the business shows no progress compared to now (and realistically, such substantial progress is unlikely), then its stock price may face further pressure. Additionally, the prospectus stipulates that two days after the company releases its Q2 2026 earnings report, eligible internal shareholders (employees, former employees, certain early investors) may sell a portion of their locked shares, allowed to sell up to 20% of the locked shares. If the stock price rises by 30% compared to the IPO issuance price and 5 out of 10 trading days meet this standard, an additional 10% may be unlocked.

This means that in August, the market will not only welcome the revenue report volatility brought by SpaceX but also face substantial stock unlocks for the first time since the listing, presenting significant challenges.

Will we suffocate for Musk's dream? At least from the first day's performance, the market chose to believe the story, but it has not completely lost its rationality. What will determine the fate of SpaceX going forward is its actual performance.

Recommended reading:

SpaceX On-chain New Shares Dream Shattered: Trillion Dollar IPO Feast, I Only Got 4 Shares

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。