On the day of the world's largest IPO, crypto platforms staged a quota accident.

Written by: Sanqing, Foresight News

On June 12, SpaceX went public on Nasdaq at an IPO issue price of $135 per share, with the stock code SPCX, valuing the company at approximately $1.77 trillion, setting a record for the largest IPO in history. According to Nasdaq quotes, SPCX peaked at $176.52 on the same day, closing at $160.95, up 19.22% from the issue price, with a total trading volume of approximately 510 million shares.

However, what truly ignited the crypto community on that day was not the opening price but the refund announcements successively issued by major platforms, as almost all of them failed to acquire SpaceX shares.

Seven platforms, seven responses

Kraken: The core initiator of this new listing event. Through its parent company's xStocks platform, it opened subscriptions to users in over 110 countries, focusing on the concept of "the first continuous 24/7 trading of an IPO worldwide," attracting over $1 billion in subscription demand a week before the listing. On the day of the listing, a single account was allocated a maximum of only 4.2786 shares, with a total cost of approximately $606.5.

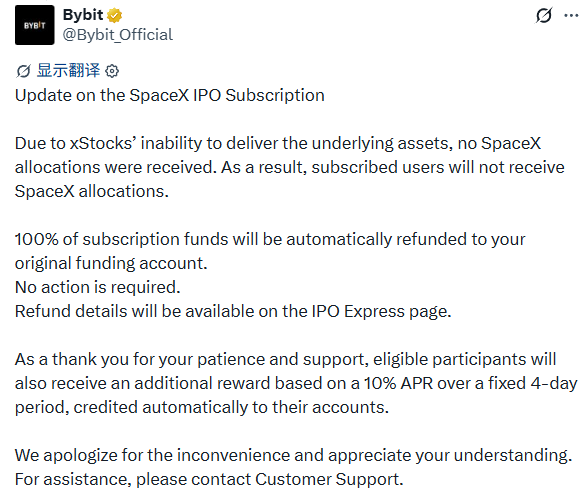

Bybit: The official announcement was straightforward, stating, "Due to xStocks' inability to deliver the underlying assets, it failed to obtain any SpaceX IPO quota." All subscription funds were refunded 100%, and 4-day compensation returns were provided at a 10% annual interest rate.

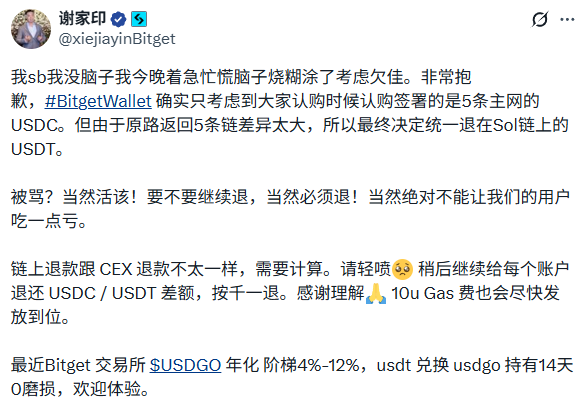

Bitget Wallet: Also experienced quota failure, issued full refunds, and provided a 10 USDT GetGas subsidy. However, the refund process itself sparked secondary disputes: users subscribed using USDC, but refunds were uniformly credited in USDT on the Solana chain, leading to strong dissatisfaction over price differences. Bitget's Chinese head, Xie Jiayin, publicly apologized on X, admitting poor handling and promising to compensate for the discrepancies and gas fees.

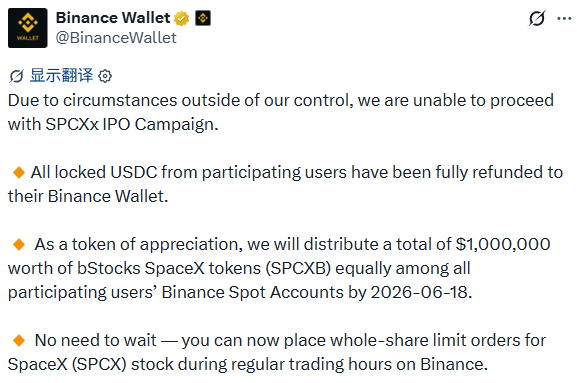

Binance Wallet: Announced the cancellation of the SPCX IPO event, issuing full refunds. The compensation plan involved distributing 1 million SPCXB (which is SpaceX's share in Binance's own bStocks product) equally among participating users. This also inadvertently completed a product promotion of bStocks.

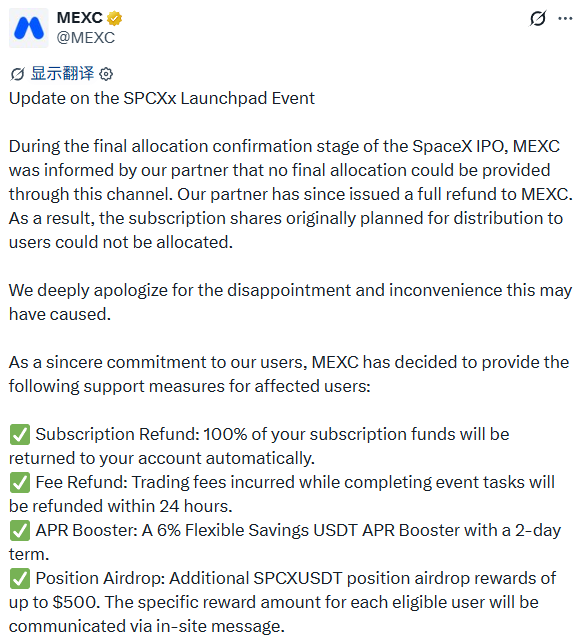

MEXC: Received notification from partners stating that they could ultimately provide no quotas, issuing full refunds and offering the following compensation: a return of event task fees within 24 hours, a 6% APR interest coupon for 2 days in USDT savings, and an airdrop voucher for SPCX USDT contract positions valued up to 500 USDT.

OKX: Did not participate in this xStocks SPCX IPO cooperation and was humorously referred to by netizens as having "won by lying down."

Gate: Successfully completed the distribution this time due to the differences in infrastructure. On June 3, Gate partnered with Alpaca, a licensed self-clearing broker in the U.S., which has formal brokerage status and can directly participate in the IPO quota distribution process. Gate entered the underwriter's distribution chain through Alpaca, rather than through an additional intermediary layer like xStocks. Ultimately, it achieved a proportional distribution of 5% to 12% of the allotted shares, and the SPCX real shares of allocated users were directly credited to their Gate stock accounts.

Why the quotas were announced after the opening

Kraken employee Nata tweeted at 3:00 PM mentioning "distribution delays," but it wasn't until 10:00 PM, some time after the bidding began, that Nata further publicly explained the full scope of the quota issue: the Kraken xStocks platform failed to obtain the expected Pre-IPO quota from SpaceX's underwriters, resulting in only partial fulfillment of user orders.

Nata explained that IPO quotas are entirely determined by the issuer's underwriters, unrelated to Kraken or xStocks, and that global demand for this issuance was exceptionally high. All unfulfilled orders will be fully refunded to user accounts without any fees. However, he later deleted that tweet.

To clarify the distribution chain of U.S. stock IPO quotas, SpaceX adopted a fixed issuance price model, locking in a price of $135 per share before the roadshow, with the subscription window closing on June 11. After that, main underwriters such as Goldman Sachs and Morgan Stanley led the quota distribution: core institutional investors (hedge funds, mutual funds, pensions) were prioritized, followed by registered brokers with direct agreements with underwriters, and finally retail channels.

Underwriters do not directly settle stocks with non-registered entities; each allocation must correspond to a trading party registered with FINRA or the SEC.

It is worth noting that reports indicated that SpaceX's total retail quota was compressed from the planned approximately 30% to just over 20%, with even users of traditional retail brokers like Fidelity and Robinhood proportionally cut back.

xStocks itself does not have U.S. registered broker qualifications, meaning it cannot directly appear on the underwriter's quota list in its own name; it must interface through a licensed intermediary. It’s unknown how many quotas this intermediary obtained in this IPO and how much it decided to allocate to xStocks.

There is a saying circulating online: xStocks saw SPCX's surge at the opening and withheld stocks; had the opening been below the issue price, it would have distributed in full to users. This conspiracy theory logic is indeed very appealing.

However, a more plausible explanation may be: in the face of the largest IPO in history, xStocks, as the upstream distributor shared by Kraken, Bybit, Binance Wallet, Bitget Wallet, and MEXC, received an extremely limited quota from the intermediary brokerage layer. After xStocks's overall significant quota cut, Kraken, as a platform directly under its parent company Payward, received only a small portion of quotas, while the remaining platforms through xStocks received none.

One entrance does not equal a real share

Some users opened short positions in the SPCX contract market to hedge, planning to close them after acquiring the spot market to lock in the price difference. As a result, the spot market fell through, but the short positions skyrocketed with SPCX from $135 all the way to above $160, resulting in sustained floating losses. They incurred service charges from the new listing and also losses on hedging, missing out on both ends.

This incident exposed not only the execution problems of a particular platform but also the fragility of the "platform raising funds to compete for quotas" model. The multi-layered agency gathering method is essentially no different from traditional entrusted investment; the longer the chain, the weaker its ability to cash out under extreme pressure. The failure of xStocks visually presented this hidden risk.

On the same day, Gate achieved real proportional distribution (5%-12%) through Alpaca (a U.S. licensed self-clearing broker), while xStocks's multi-layer agency model significantly cut orders or resulted in zero quotas across platforms. It can be seen that the dividing line has never been about "whether there are tokens" but whether the supply chain can really fulfill its commitments under extreme conditions.

This incident provided a vivid lesson for all users participating in crypto new listings and offered a clear reference standard for choosing platforms in the future: direct connections to licensed brokers' compliance qualifications, transparent and traceable sources and priority distributions of quotas, as well as a clear distinction between "real ownership" and "price exposure."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。