Author: Artemis and North Island Ventures (NIV)

Translation: Felix, PANews

Editor's note: Recently, the publicly traded company Robinhood (HOOD) has been buoyed by strong operational data and obtaining IPO underwriting qualifications, leading to a strong rebound in its stock price, which rose by 6.8% on June 11. In response, Artemis and North Island Ventures (NIV) wrote that with the Gold subscription, the growth of predictive markets, and asset inflows from upcoming mega IPOs such as SpaceX, Robinhood is likely to fully benefit from the largest intergenerational wealth transfer in history, and its current valuation is still underestimated. PANews has translated the original text, and the following is the content details.

Most investors view Robinhood (HOOD) as a retail brokerage that fluctuates with the Bitcoin trading cycle. This narrow view overlooks that Robinhood is becoming a financial super app for Generation Z and millennials, who are expected to be among the largest beneficiaries of the intergenerational wealth transfer in American history. Robinhood Gold is poised to become the "Amazon Prime" of retail finance, turning subscription revenue into a flywheel effect that makes Robinhood progressively higher quality, with more regular income and reduced cyclicality over time. Predictive markets represent an emerging asset class for retail investors, while Robinhood's monthly active users (MAU) are already more than 20 times that of second-largest native distribution competitors like Polymarket and Kalshi. Thanks to Robinhood’s strong product iteration speed and its solid position among Generation Z and millennials, its assets per user will continue to grow, making Robinhood a winner in retail finance.

We believe that Robinhood is misunderstood as an investment tool highly correlated with cryptocurrency, and investors overlook that Robinhood is evolving into a financial super app benefiting from intergenerational wealth transfer. Robinhood is poised to benefit from two major catalysts in 2026: predictive markets and large IPOs from companies like SpaceX and Anthropologie, OpenAI.

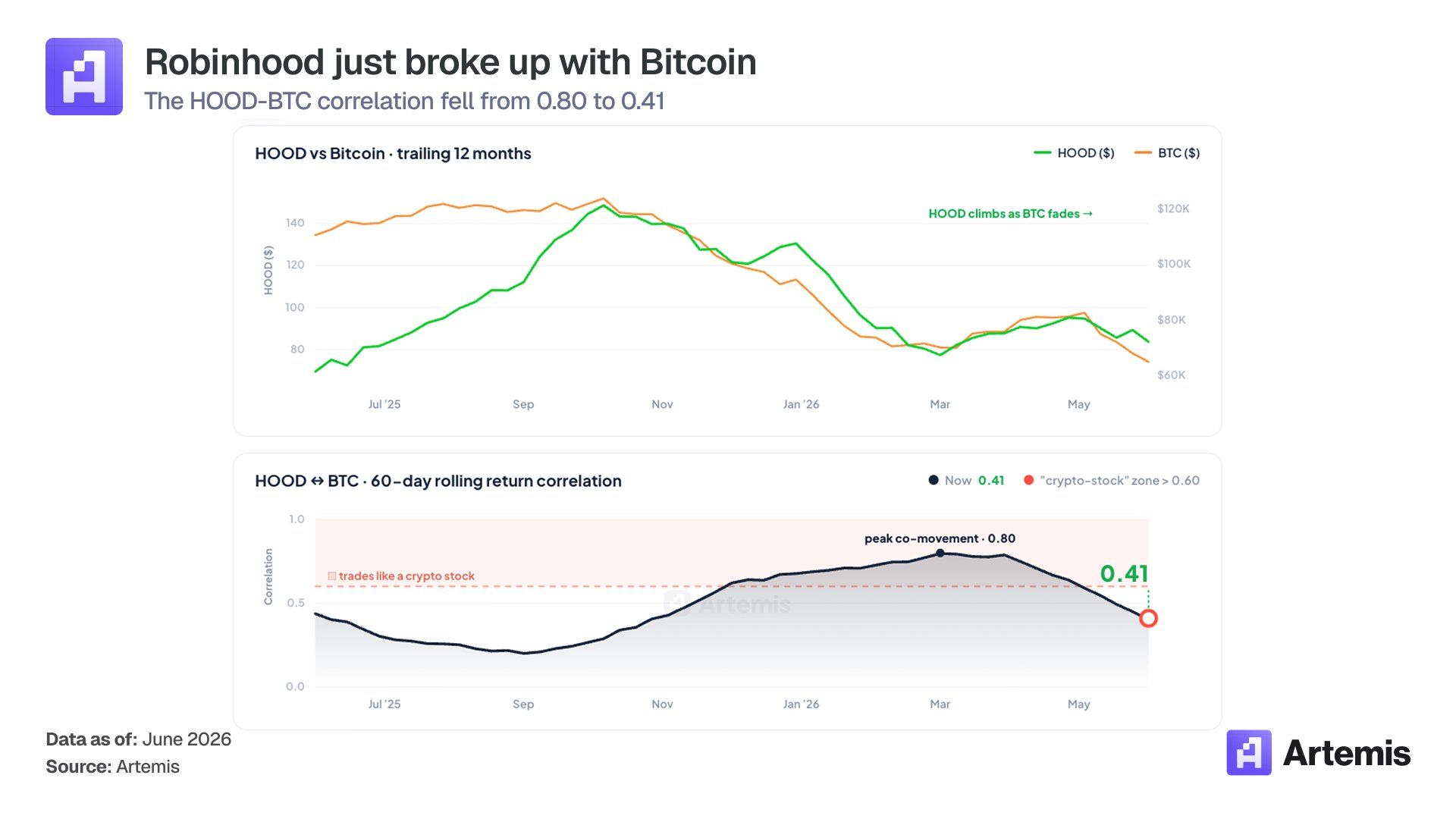

Most investors still classify Robinhood as a "retail brokerage" and view it as an asset highly correlated with Bitcoin. This article aims to clarify this misunderstanding: the correlation between Robinhood and Bitcoin is gradually decreasing, remaining above 0.70 for most of 2026 but has recently dropped to 0.41. The market pricing of the stock seems to tightly link it with options and cryptocurrency trading cycles. This view is inaccurate, and as the concept of super apps becomes more apparent, this pricing distortion will disappear.

1. Intergenerational Wealth Transfer and Super Apps

The median age of Robinhood users is 35 years old, a group expected to benefit from the wealth transfer from the baby boomer generation to Generation Z and millennials over the next two decades, which is anticipated to be one of the largest intergenerational wealth transfers in American history. While the average account balance for the baby boomer generation in traditional financial firms is more than 20 times that of the median balance of Robinhood users (approximately $12,000), Robinhood's relatively younger user base allows it to avoid the heavy historical liabilities of traditional financial firms.

As for why "now," the answer is super apps. Robinhood has developed a complete product matrix in the areas of investment, retirement, savings, consumption, and speculative products, capable of absorbing the funds that are about to flow in from the intergenerational wealth transfer.

2. Predictive Markets as an Emerging Retail Asset Class

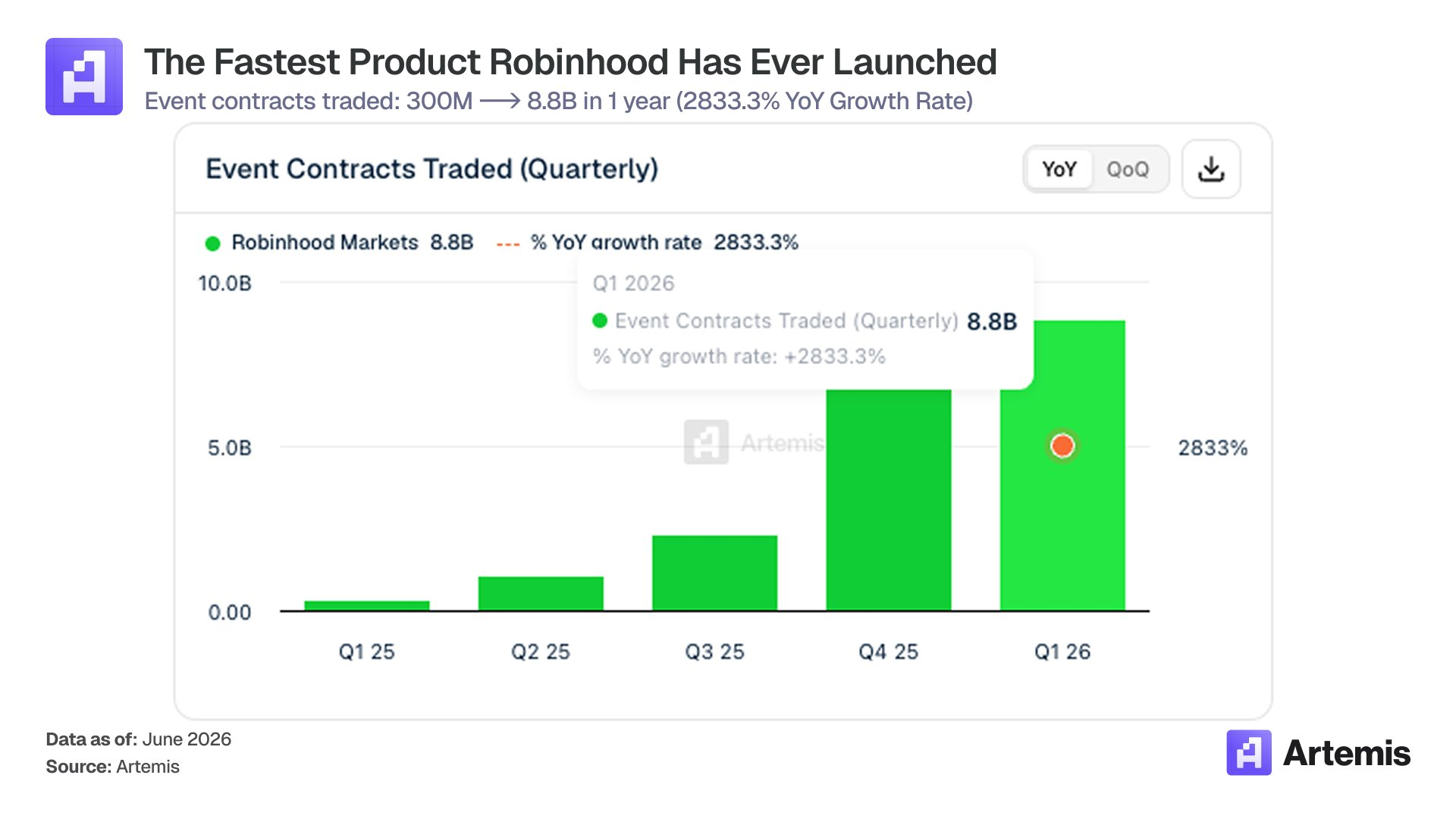

The trading volume of event contracts on Robinhood surged from $300 million in Q1 2025 to $8.8 billion in Q1 2026, exploding 30-fold over four quarters. Revenue from predictive markets during this period is expected to increase from approximately $3 million to about $104 million. This is one of the fastest-growing product lines in Robinhood's history, with major catalysts still to come: the World Cup, US midterm elections, an entire NFL season, and the launch of Rothera, Robinhood's vertically integrated exchange and clearinghouse regulated by the CFTC.

Currently, predictive market trading volume on Kalshi and Polymarket has already spiked, and this is likely to be reflected in Robinhood's Q2 and Q3 2026 financial reports.

These two favorable factors are still in their early stages and have not yet been reflected in the current expected price-to-earnings ratios.

3. Mega IPOs May Drive Retail Participation

SpaceX plans to conduct an IPO on June 12 and allocate a record 30% of shares to retail investors. Typically, the proportion of shares allocated to retail investors in an IPO is 5-10%. Anthropic and OpenAI may also go public in the coming months. These companies have unprecedented fundraising needs, and retail interest is very high. These IPOs may enhance user engagement on the Robinhood platform.

Why can HOOD benefit from the wealth transfer?

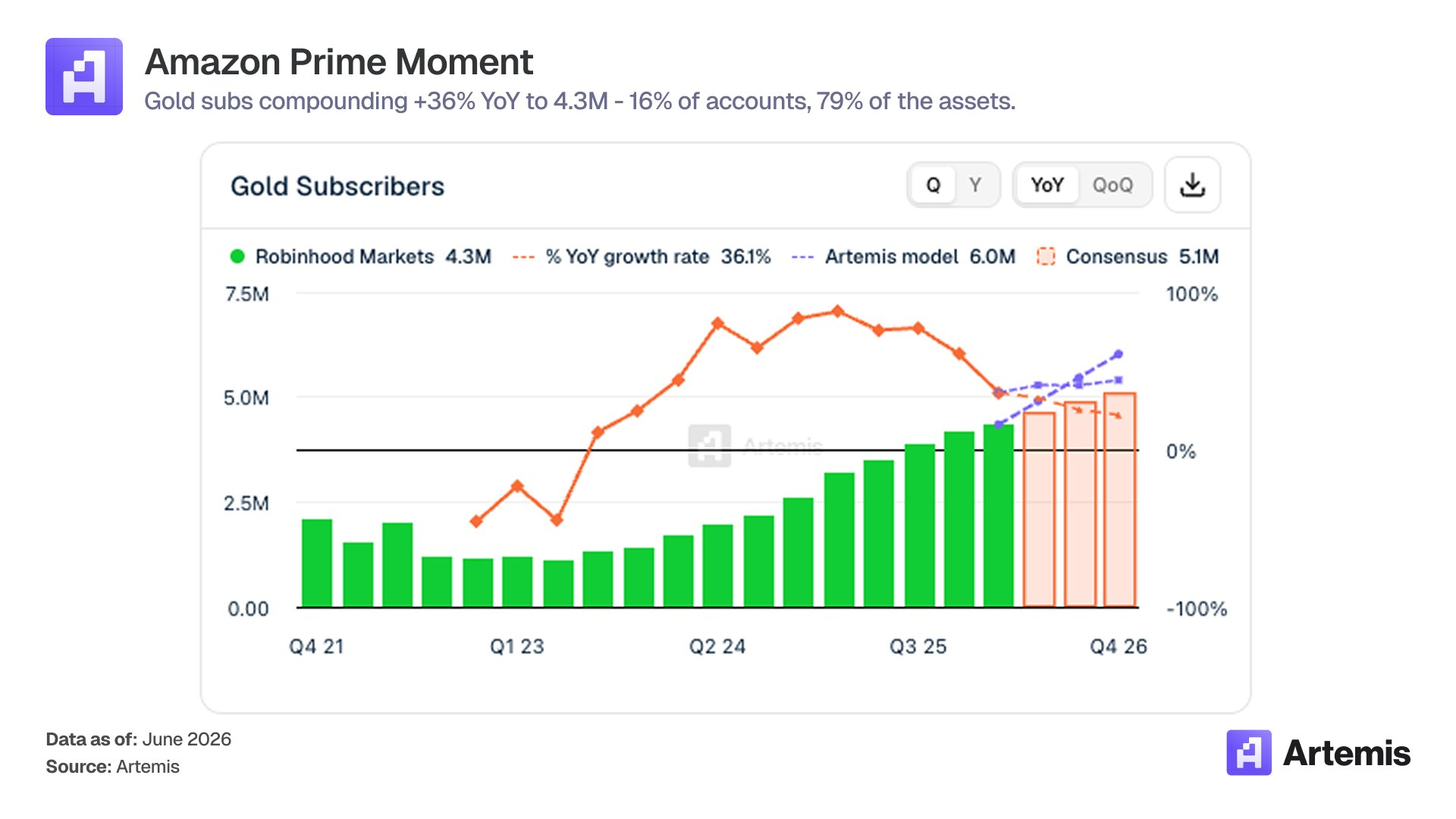

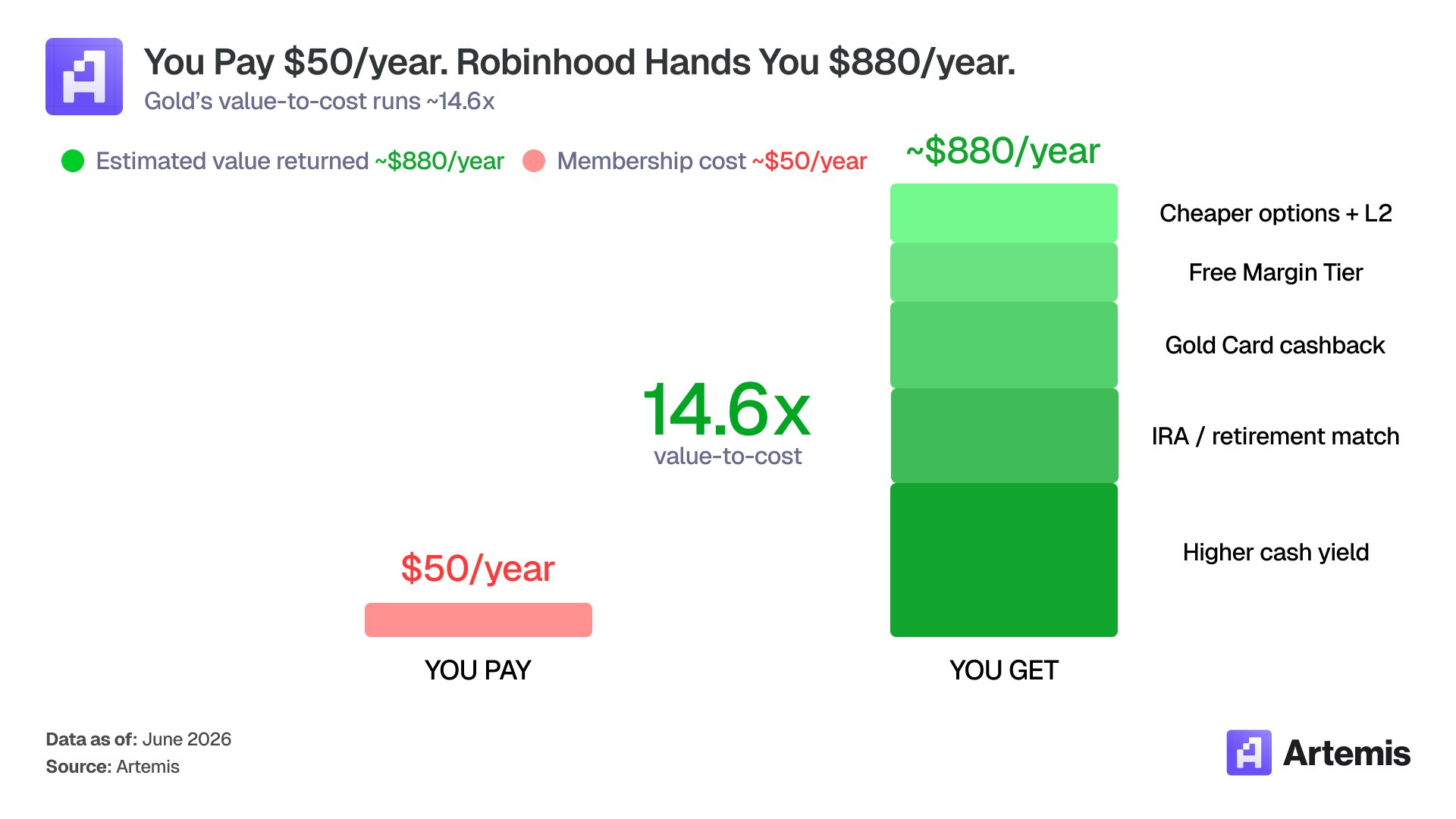

The number of Gold members on the Robinhood platform has increased from 1.14 million at the end of 2022 to 4.34 million in Q1 2026, growing 3.8 times in just three years. This product charges $5 per month (or $50 per year). It is estimated that members can generate approximately $880 in total value per year (including higher cash gains, IRA matching, free margin, lower options fees, Robinhood Gold card, Morningstar research, second-tier data, and Robinhood strategies).

Importantly, the user structure. Gold members account for about 16% of funded accounts but represent approximately 79% of platform assets. They are the main contributors to asset appreciation. Robinhood's continuously expanding product portfolio enables it to better convert a larger share of the existing 27 million funded accounts into Gold members. As the penetration rate of Gold membership increases, all value indicators: ARPU (average revenue per user), net deposits, user retention rate, and gross margin will rise.

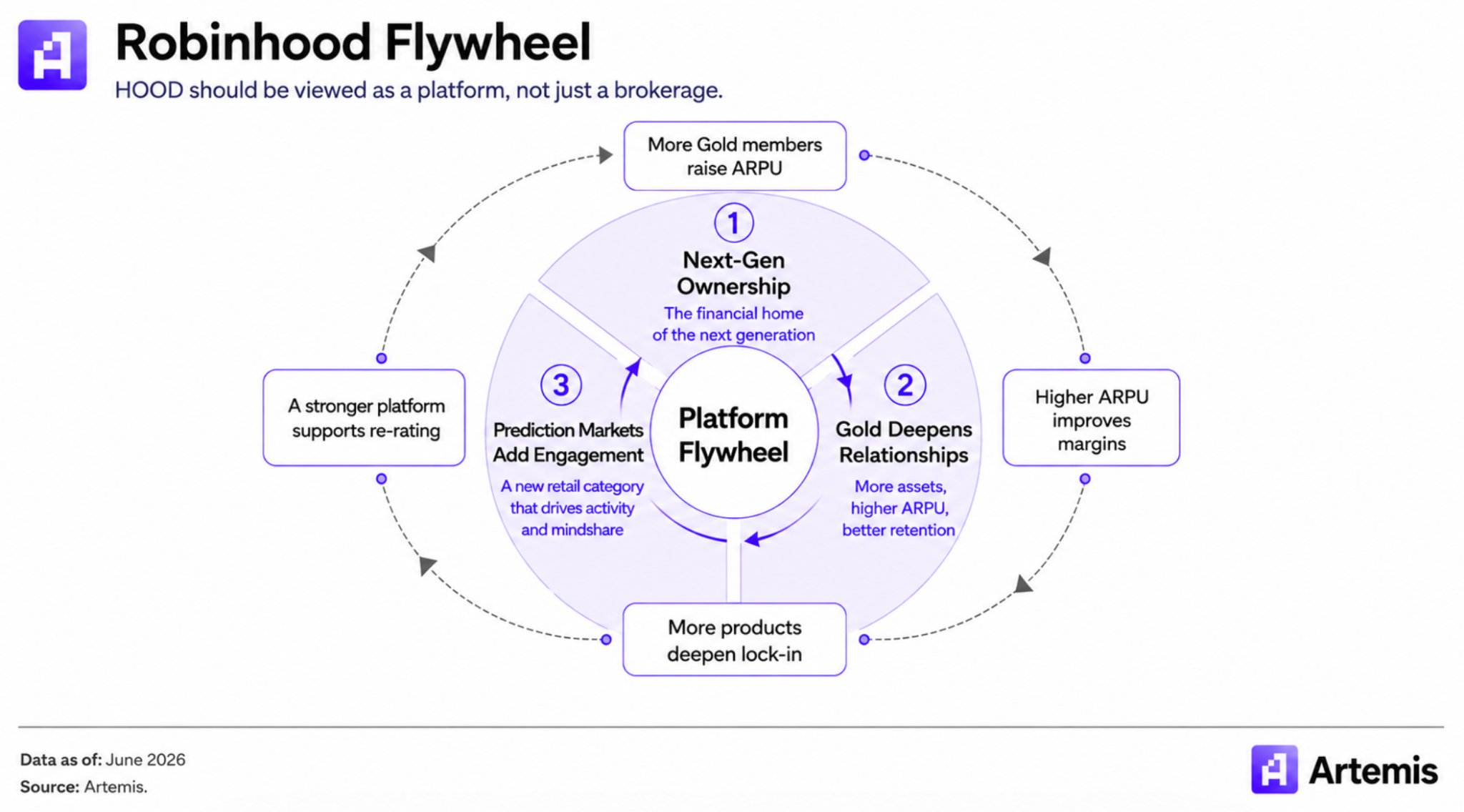

We believe that Prime transformed Amazon from a retailer into a consumer habit. The Prime subscription model increases user engagement, ultimately boosting spending on Amazon and creating stickier, higher-value customers. We believe Gold can have a similar effect for Robinhood, potentially making Robinhood the preferred financial platform for the next generation.

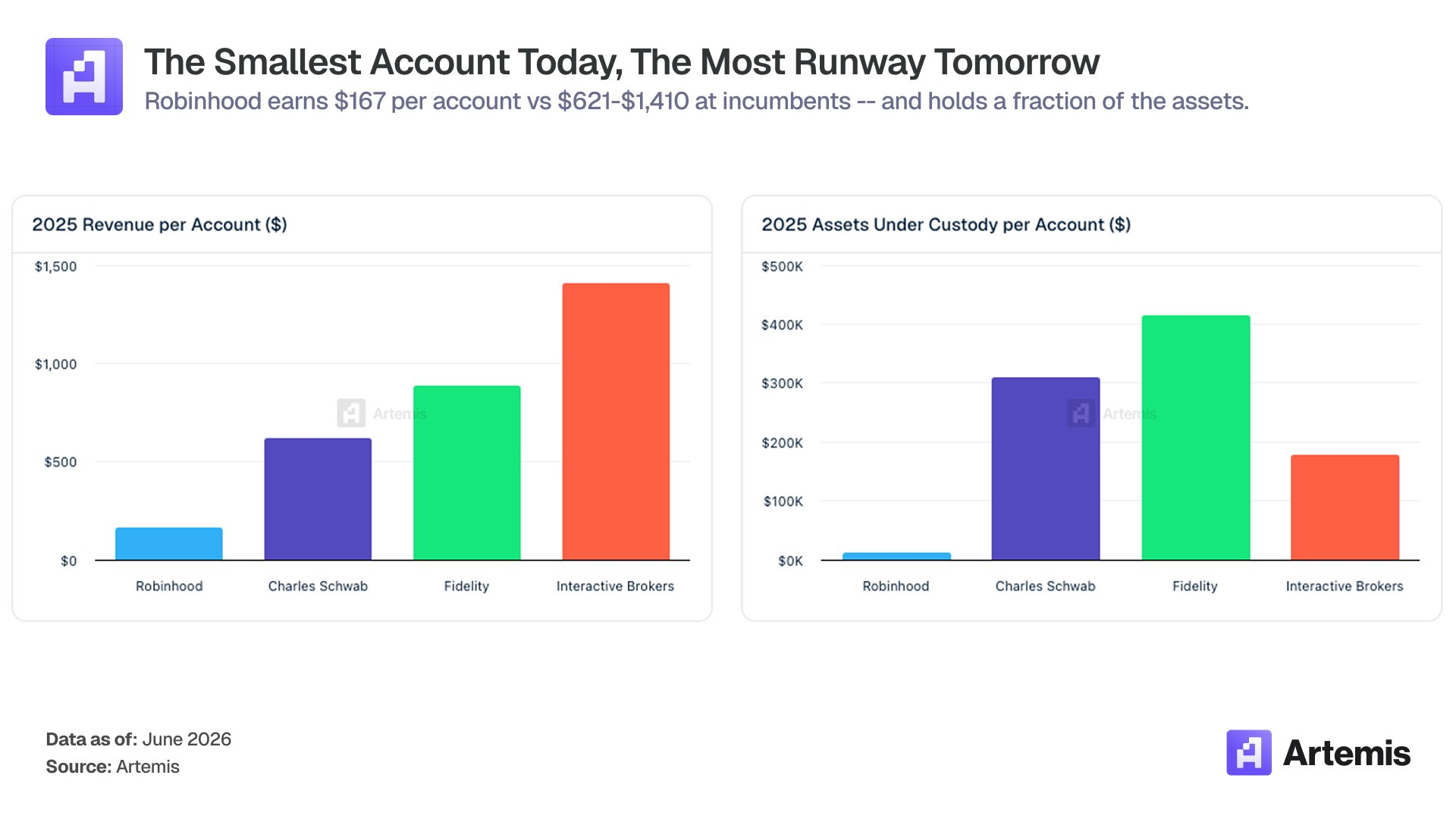

Asset bases are converging. The average assets under management (AUM) per funded client have risen from $2,700 at the end of 2022 to $11,900 by the end of 2025. Even at this growth rate, HOOD's per-client asset size is only about 5% that of Charles Schwab, Fidelity, and Interactive Brokers, all of which have much longer asset age than Robinhood.

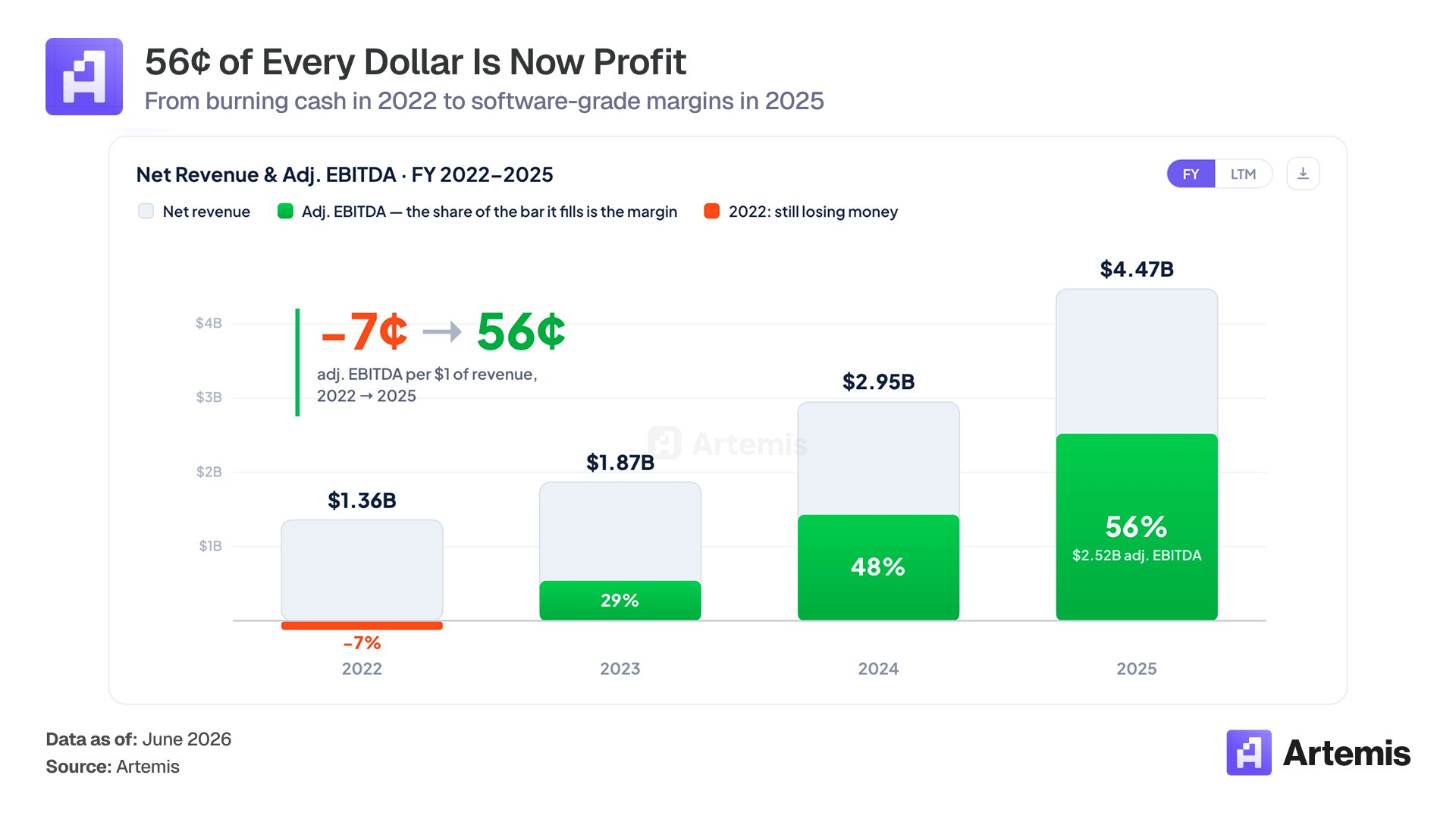

The margin curve indicates that operational leverage is already showing. The adjusted EBITDA margin has increased from -7% in 2022 to 29% in 2023, 48% in 2024, and 56% in 2025. Costs are largely fixed: technology, operations, and general and administrative expenses (G&A) account for about 70% of the cost base. Thus, new revenues bring profit margins exceeding 70%.

Why is HOOD likely to excel in predictive markets?

This might be the most underrated part of the entire story.

Predictive markets will become a winner-takes-all market due to three key factors: distribution channel, product user experience, and integration with users’ broader financial spectrum. Robinhood has the potential to excel in all three areas.

Distribution channels: Robinhood has 27 million funded accounts and about 13 million monthly active users. Kalshi has an estimated 5 million monthly active users; Polymarket around 500,000. The user acquisition gap between Robinhood and its second-largest native distribution competitor exceeds 20 times.

Product interface: Event contracts can coexist with stocks, options, and cryptocurrencies within the same application, using the same wallet, reports, and risk management systems. Independent predictive market applications cannot achieve this without becoming brokerages.

Vertical integration: Robinhood's exchange and clearing house, Rothera, regulated by the U.S. Commodity Futures Trading Commission (CFTC), allows it to control commission rates, quickly launch markets, and avoid fees to third-party exchanges. Even if profit levels remain unchanged, vertical integration often enables revenue growth of 25% to 30%.

We view predictive markets as a new asset class: similar to spot cryptocurrencies in 2017 or zero-commission stock trading in 2014. The same pattern was seen in both earlier cases: Brokerages that master retail distribution channels will dominate the category and achieve increased valuations.

How does HOOD monetize through super apps?

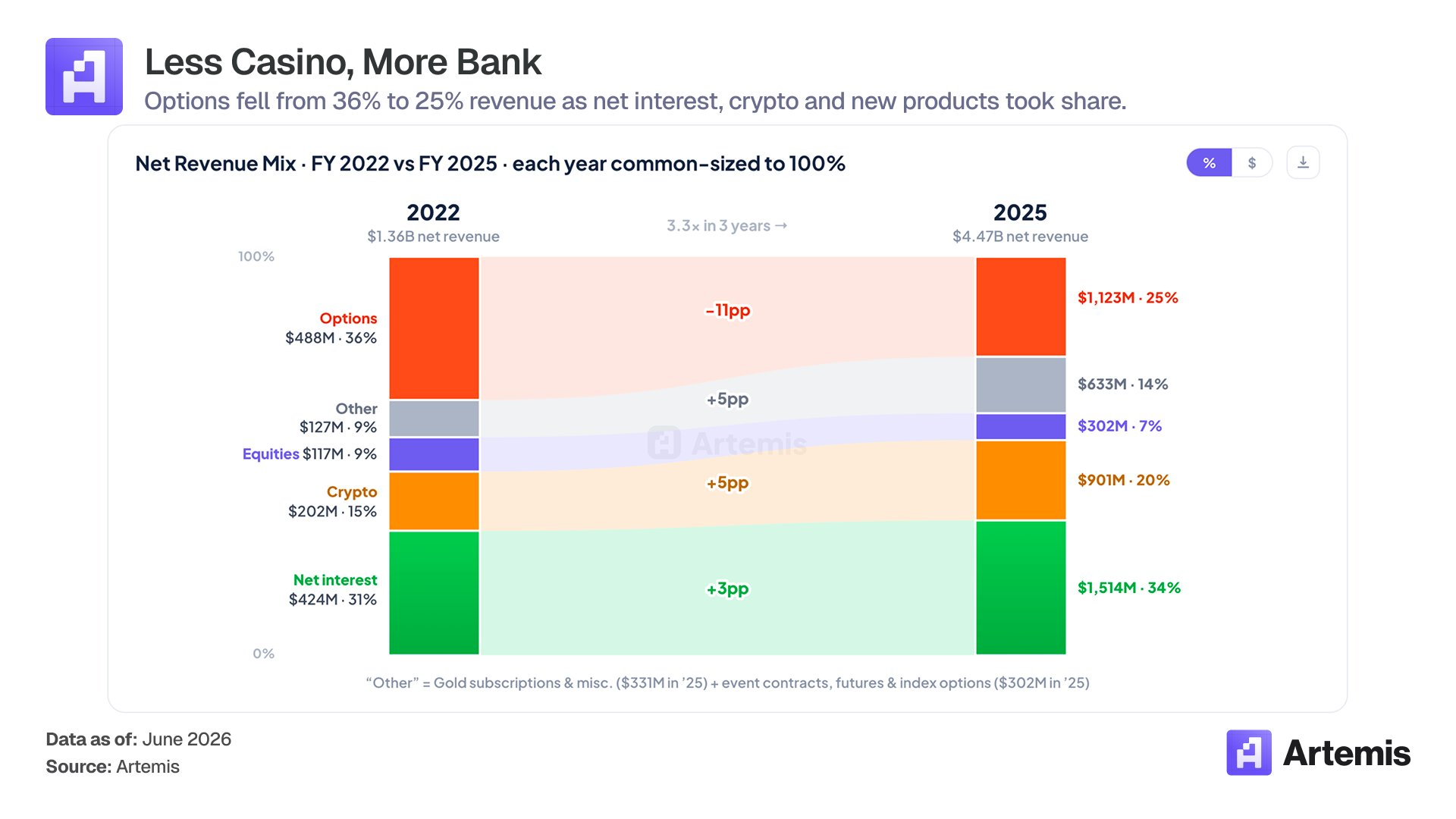

Robinhood’s revenue structure is undergoing changes.

Trading revenue is no longer the entirety of Robinhood's business. Net interest, Gold subscription fees, predictive markets, Robinhood's high-yield checking accounts, Gold credit cards, retirement planning (TradePMR added approximately $40 billion in advisory AUM in 2025), Robinhood Strategies, and the recent estate planning business are all independent sources of profit. Each touches different stages of the user life cycle and strengthens user relationships. We believe that collectively, these businesses are transforming Robinhood from a company reliant on speculative trading income into a platform where users can generate continuous income throughout their financial life.

Why does the market have pricing distortions for Robinhood?

HOOD is trading at about 34 times its expected earnings per share for 2027, roughly in line with expectations for Interactive Brokers and Coinbase. Three points suggest that HOOD's pricing contains distortions:

- The proportion of Gold accounts is still only about 16% of the total number of accounts. As this proportion rises, compared to HOOD's current ARPU of $167, its ARPU is structurally expected to converge toward the range of $621 to $1,410 per account for traditional institutions. This is not a prediction but a structural setting of the business.

- Predictive markets have become one of the fastest-expanding product lines in American retail finance, with Robinhood controlling the distribution channel.

- The cost base is largely fixed. Even while the platform is still in the investment phase, its adjusted EBITDA margin has reached 56% in 2025.

Due to Robinhood's positioning between different investment classes, the market's attention has not kept pace. Brokerage analysts are insufficiently focused on it. Fintech analysts view it as a cryptocurrency-related company. Cryptocurrency analysts regard it as a traditional brokerage.

Conclusion

The market currently sees Robinhood as a cyclical retail brokerage. However, in our view, it is transforming into a unique company: a vertically integrated financial super app serving those expected to benefit from the intergenerational wealth transfer from baby boomers to Generation Z and millennials, and where a rapidly growing new asset class is operating within its application during this cycle.

We believe HOOD should be valued against platform-type companies, rather than brokerage-type valuations. Its flywheel effect is driven by three factors: (1) Target user group proportion × (2) Gold-driven asset compounding growth × (3) Predictive market category leadership. With every additional Gold user and every additional dollar of ARPU value, profitability increases. Every new product launch further locks in customers. We believe the longer this compounding effect continues, the stronger its business moat will become.

This should not be seen as a 2026 story. This marks the beginning of a platform transformation over the next decade, which will impact the ways the next generation saves, trades, borrows, invests, and accumulates wealth.

Related readings: Robinhood vs Coinbase: Who is the Next Tenfold Stock?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。