The market is quiet, yet cryptocurrency adoption is leading globally.

Written by: 100y, Hashed Emergent

Translated by: Luffy, Foresight News

The once thriving Indian cryptocurrency market appears to be quiet, with domestic trading suffering from heavy taxes and regulatory pressures, causing many users to shift to offshore platforms. However, data contradicts this by showing that India has led the world in cryptocurrency adoption for several consecutive years. This report from Four Pillars comprehensively deconstructs the current Indian cryptocurrency market from multiple dimensions, interpreting signs of industry maturity through developers, cross-border payments, and changes in venture capital, while also quantifying threats from taxation, central bank policies, and talent outflow, discussing dialectically whether the Indian cryptocurrency market is growing or stagnating under constraints. Below is the full translation of the report:

TL;DR:

- During the bull market from 2020 to 2021, with retail investors entering the fray, decentralized finance (DeFi), non-fungible tokens (NFTs), and developer ecosystems expanding rapidly, India ranked among the core global cryptocurrency markets. Since 2022, high taxes and regulatory pressures have significantly dampened the enthusiasm for domestic exchanges, but this does not mean that the market's true demand has disappeared. The Indian cryptocurrency industry is now at a critical turning point; whether the market is maturing or stagnating has valid arguments on both sides.

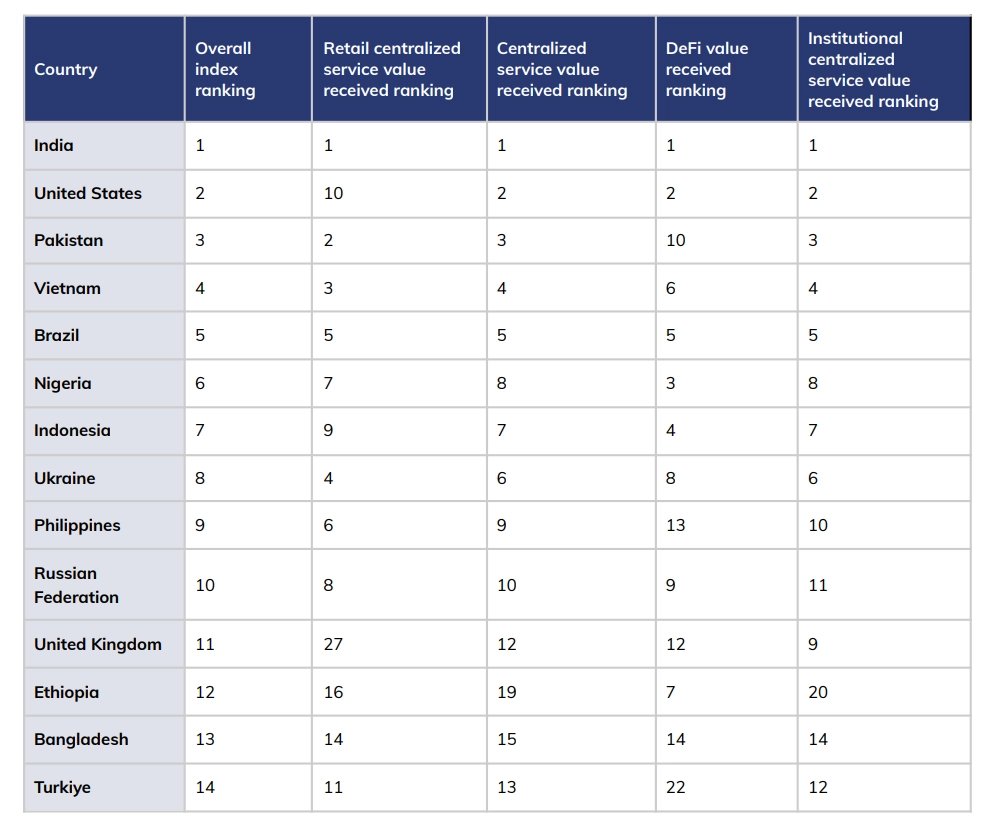

- India remains one of the highest countries in the world for cryptocurrency adoption. According to blockchain data analysis firm Chainalysis, India ranked first in the "Global Cryptocurrency Adoption Index" for three consecutive years from 2023 to 2025, leading in data across four dimensions: trading on centralized exchanges, retail investment, DeFi interaction, and institutional large transactions. However, this ranking takes adjustments based on purchasing power parity GDP per capita and the population base, necessitating a distinction between absolute trading volume and per capita penetration rates when assessing India’s market scale.

- The positive change in the Indian cryptocurrency market is that the industry is moving away from being driven by trading speculation and gradually extending towards developers, startups, underlying infrastructure, and real-world payment applications. Series B and later financing rounds are seeing renewed warmth, and India has grown into a global hub for Web3 developers, housing about 15.2% of global Web3 development talent. Yet, significant risks persist: the industrial value created by local developers and startup teams may not necessarily remain in India; many projects seek regulatory certainty and more favorable financing structures choosing to register in overseas jurisdictions.

- Stablecoins, cross-border remittances, and asset tokenization are anticipated to become the three pillars of growth in the Indian market, and are also the areas most sensitive to regulation. Several local enterprises are attempting to build infrastructure for remittances, settlements, and access to capital, but the Reserve Bank of India, prioritizing monetary sovereignty, financial stability, and cross-border capital control, promotes the development of an official digital payment infrastructure centered around central bank digital currency (CBDC) and a unified payment interface (UPI) while being cautious towards private stablecoins. This creates a unique configuration: while there is a strong demand for domestic stablecoins, their compliance positioning within the local financial system remains unresolved.

- The biggest contradiction in the Indian cryptocurrency industry lies not in the lack of demand, but in whether the strong domestic user demand and quality talent can remain in a compliant and transparent domestic market. High transaction taxes, a limited regulatory approach focused on anti-money laundering, security incidents at exchanges, withdrawal restrictions, and regulatory uncertainty may weaken the competitiveness of India's domestic market, forcing users and founders to migrate abroad. Conversely, if India optimizes its tax system, implements user asset protection standards, and clarifies regulatory details for stablecoins, DeFi, and asset tokenization, it stands to leverage its large user base and developer resources, paving the way for genuine financial infrastructure innovation in the domestic market.

Introduction: Is the Indian cryptocurrency market really quiet?

The Golden Era of Indian Cryptocurrency

Looking back at the 2020-2021 cryptocurrency bull market, India was far from an ordinary emerging market. Key words of that cycle—retail influx, altcoin boom, DeFi explosion, NFT breakout, and global developer expansion—all converged in the Indian market.

Data from Chainalysis shows that from July 2020 to June 2021, the size of India's cryptocurrency market surged by 641%; among transactions initiated by Indian addresses, DeFi-related transactions accounted for 59%, higher than in Vietnam and Pakistan. Institutional-level large transactions exceeding 10 million dollars constituted 42% of the total trading volume in the country; at that point, India had already transcended the phase of pure retail speculation, with a more diverse and mature trading structure.

Additionally, there are many noteworthy examples. The Indian exchange WazirX surpassed 10 million users in 2021, with new registrations from small towns and suburban areas increasing by 700% year-on-year; CoinSwitch Kuber secured $260 million in financing, led jointly by a16z and Coinbase Ventures, entering the unicorn ranks; CoinDCX also became a unicorn in 2021.

Indian entrepreneurs, represented by Polygon, built global underlying infrastructure projects, transforming India from a major cryptocurrency consumption country to a leading cryptocurrency technology development nation. Polygon, originally established as Matic Network in 2017, aimed to address Ethereum’s scalability issues and later grew into a leading scalability infrastructure of the Ethereum ecosystem.

Following Polygon, a multitude of protocols and companies founded by Indian teams or led by Indian founders emerged, including EigenLayer, Avail, Sentient, Stader Labs, Biconomy, OpenFX, FalconX, and Instadapp, among others.

Is the Indian cryptocurrency market in a slump?

Today, the Indian cryptocurrency market is far quieter than it once was, influenced by multiple factors.

2022 was a watershed year for the industry. The global cryptocurrency market entered a bear phase, with India simultaneously implementing new cryptocurrency regulations—imposing a 30% income tax on trading profits from virtual digital assets (VDA), along with a new 1% withholding tax in July, severely impacting the activity levels of local exchanges. Research by the Indian policy think tank Esya Centre found that following the implementation of the 1% withholding tax, many Indian users shifted to offshore platforms that are harder to regulate; between July 2022 and July 2023, over 90% of cryptocurrency asset transactions by Indian investors transferred to overseas exchanges.

Regulatory pressures continued to increase thereafter. In 2025, the Indian tax authorities intensified scrutiny over cryptocurrency tax compliance, with the Central Board of Direct Taxes (CBDT) issuing audit notices to 44,057 taxpayers who engaged in crypto transactions but failed to report their assets in the VDA annex of their tax returns. In contrast, the challenges of tracking overseas transactions significantly increased post-departure. This ultimately created a distorted situation where stringent regulations mainly constrained compliant domestic platforms and law-abiding users, further accelerating industry outflow.

However, determining that the Indian cryptocurrency industry is cooling down solely based on the market's quietness would be misleading: the market has merely faded from the spotlight; demand and trading volumes have not disappeared. Chainalysis data confirms that India topped the Global Cryptocurrency Adoption Index in 2023, 2024, and 2025—while the excitement has waned, the genuine demand remains.

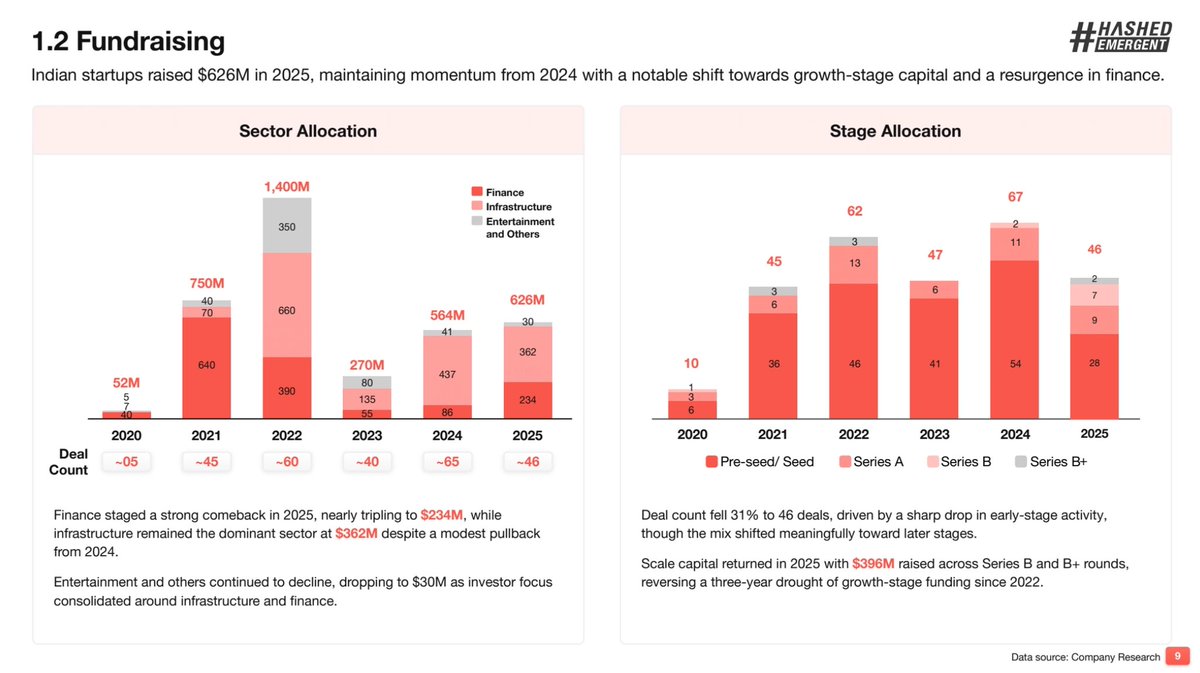

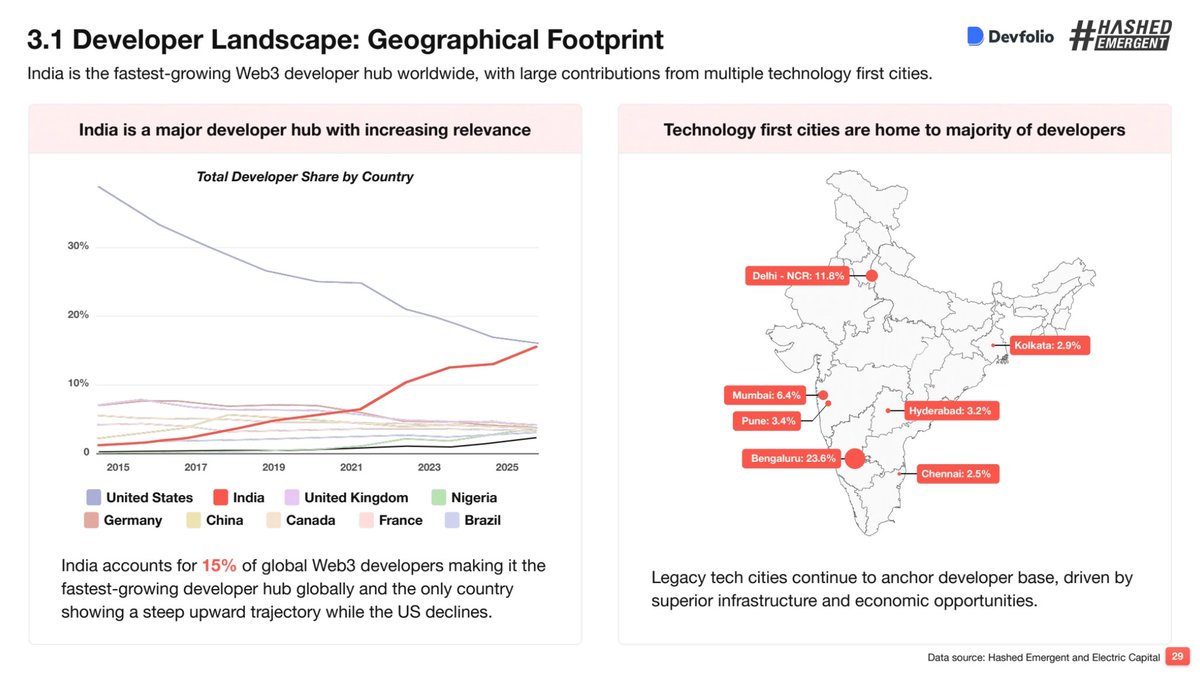

A deeper structural change lies within the market's core. Initially, India thrived on the massive influx of retail traders, but now the industry focus has shifted towards developers, startups, foundational infrastructures, and institutional use cases. Hashed Emergent reports that the number of Web3 startups in India has surpassed 1,250, with cumulative financing exceeding $3.5 billion since 2020; in 2025 alone, Indian entrepreneurs raised a total of $626 million, with Series B and later stage financing warming up from a three-year slump, raising $396 million throughout the year. India remains the second-largest hub for Web3 developers worldwide, constituting 15.2% of the global total; in 2025, local on-chain capital inflow reached $33.8 billion, nearly doubling from the previous year.

This leads to the following conclusion: on the surface, influenced by taxes and regulations, domestic exchange transactions have shrunk, retail enthusiasm has waned, and the Indian cryptocurrency industry seems to be cooling; however, digging into the data reveals that India is still in the top tier of global cryptocurrency penetration, with the industry focus steadily solidifying towards developers, startup projects, public infrastructure, and enterprise-level applications. In short, the Indian cryptocurrency industry has not perished; it has simply shed the bull market's bubble and entered a phase of mature development.

The Demand for Cryptocurrency in India Remains High

Data source: Chainalysis

Chainalysis’ 2025 Global Cryptocurrency Adoption Index evaluates 151 countries, measuring parameters such as total trading volume on centralized platforms, retail trading on centralized exchanges, DeFi on-chain transfers, and large institutional centralized trades, with India ranking first in all four subcategories. It is among the very few markets globally where retail, DeFi, and institutional funds are actively engaged simultaneously.

One reason for India's strong performance in the rankings is the structural demand for stablecoins. India has one of the world's largest remittance markets, with millions of families and workers regularly making cross-border remittances. In this context, stablecoins can play a practical role: they offer faster settlement speeds, easier access to dollar-pegged value, and can reduce friction in cross-border payments, especially for users facing high fees, slow bank transfers, or difficulty obtaining traditional dollar accounts.

Macroeconomic factors also support stablecoin demand. As the rupee depreciates against the dollar, some users may no longer view dollar-pegged digital assets as speculative crypto products, but rather as tools for preserving value. For freelancers, exporters, workers overseas, and families receiving remittances, stablecoins can conveniently meet local currency needs while seamlessly connecting with global dollar payment methods.

Of course, some funds flow through gray payment channels, posing compliance risks, but the core demand for stablecoins in India stems from true financial necessities: cross-border remittances, low-cost currency exchange, accelerated settlement, and protection against local currency depreciation. This explains why, despite heavy taxation and unclear regulations, stablecoins remain an important component of cryptocurrency trading in India.

At the same time, a nuanced view of the Chainalysis rankings is necessary. India's high score stems from two statistical flaws: first, the comprehensive indicators are tied to purchasing power parity GDP per capita, projected at around $11,160 for India in 2025, making the base number relatively low and naturally inflating the ranking; second, the large population base contributes to a skewed perception; if recalculated on a per capita basis, India's ranking would drop out of the global top twenty.

Even so, from a national overall perspective, the scale of cryptocurrency transactions and remittances in India remains at the forefront globally.

Data source: Hashed Emergent, CoinSwitch

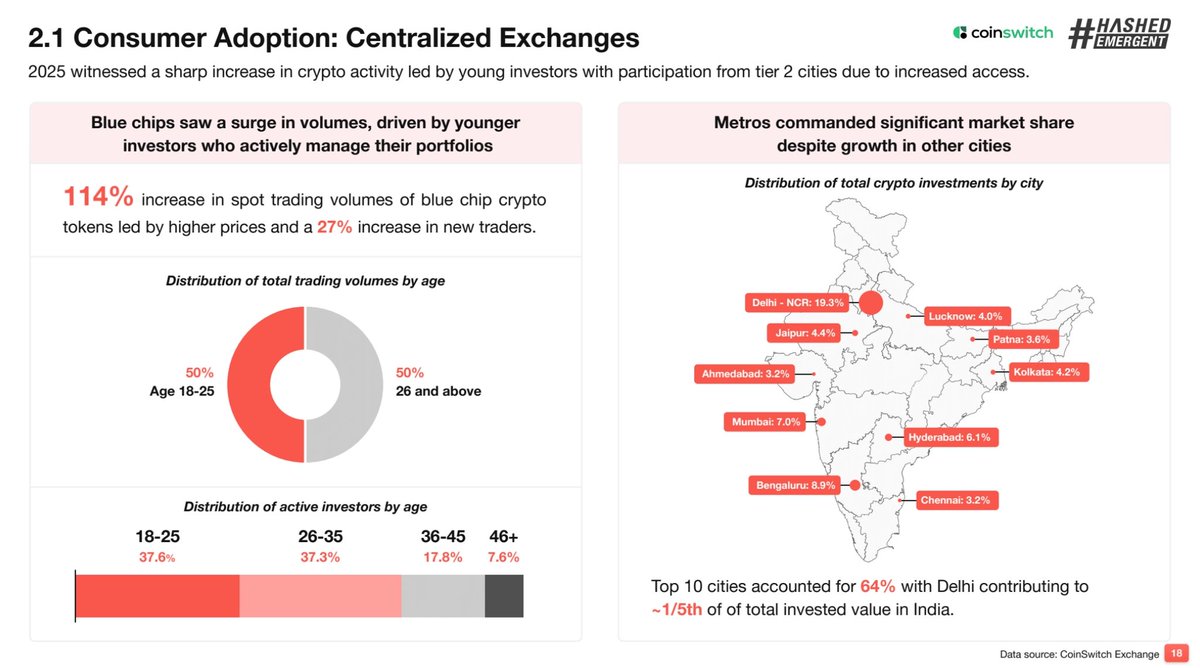

After the implementation of the withholding tax from 2022 to 2023, large amounts of capital flowed offshore; however, recently there has been a slow return of retail capital to local compliant exchanges. According to CoinSwitch data, in 2025, the spot transaction volumes of mainstream cryptocurrencies in India surged by 114% year-on-year, with new traders increasing by 27%; investors aged 18-25 contributed half of the transaction volume, with 37.6% of active traders aged 18-25 and 37.3% aged 26-35, indicating that the young demographic continues to constitute the foundational demand for cryptocurrency in India.

Data source: Hashed Emergent, Pi42

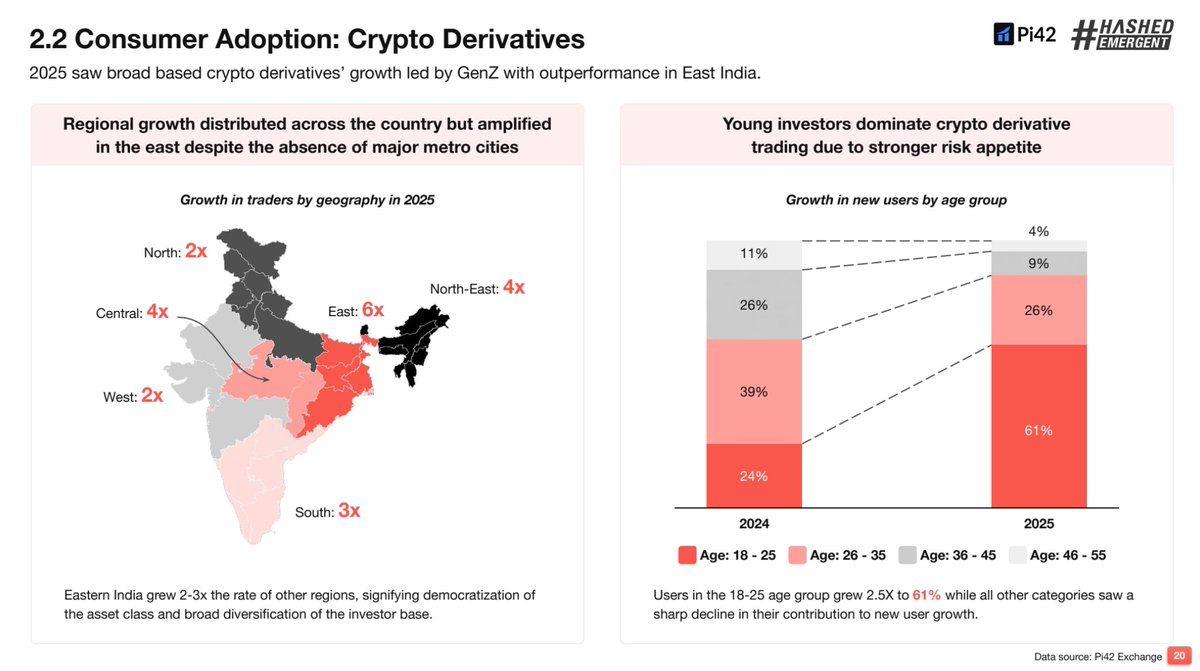

The derivatives market is seeing even more rapid growth. Data from Pi42 shows that from 2024 to 2025, the proportion of new users in India’s crypto derivatives who are 18-25 years old skyrocketed from 24% to 61%; regionally, trading volume in eastern India multiplied by six times, and the north-eastern and central regions grew four times each, with crypto derivatives expanding beyond major cities like Mumbai, Bangalore, and Delhi, continually penetrating deeper markets. This boom in downward penetration is key to local language crypto media in Hindi, Tamil, Telugu, Bengali, and other vernaculars on YouTube.

The growth in the derivatives market is evident not only in the increased number of registered users. The average transaction amount per capita in 2024 was $1,051, increasing to nearly $1,960 in 2025; the proportion of high-frequency daily traders rose from 45% to 60%. Derivatives are a high-risk category, but data verifies that Indian users are transitioning from merely holding coins to actively trading them. This shift relies on the nation’s robust derivatives soil: India ranks amongst the top globally in nominal trading volume of exchange-traded options, and a large number of retail traders are already acquainted with high volatility and high-frequency derivatives, causing investment preferences to naturally overflow into cryptocurrency derivatives.

The Indian Cryptocurrency Market is Not Silent, But Maturing

Looking at recent trends in the global cryptocurrency market, some perceive the market as calming down due to a slower pace of new concepts emerging and poor price performance of altcoins. However, others believe the market has matured, pointing to the widespread adoption of stablecoins and a keen interest from global financial institutions in on-chain finance.

This logic is equally applicable to India, as the Indian market is moving towards maturity.

A Large Number of Companies Entering the B-round Financing Maturity Stage

Data source: Hashed Emergent

A hallmark of industry maturity is the large number of local startups that have entered the mid to late-stage financing of Series B. Compared to the nationwide financing frenzy from 2021 to 2022, the total fundraising amount for Indian crypto startups has slightly decreased, but the number of financings in Series B and beyond has significantly increased.

Mid to late-stage benchmark enterprises founded in India or led by Indian founders include:

- Aspora: A cross-border financial app focusing on overseas individuals of Indian descent, initially relying on stablecoin links to handle Indian remittance business, secured B-round financing led by Sequoia, Greylock, and Y Combinator in 2025, and has since expanded to cover bill payments, wealth management, savings, and credit services;

- Tazapay: B2B cross-border payment infrastructure provider founded by Rahul Shinghal, Saroj Mishra, and Arul Kumaravel, secured B-round investment from Circle Ventures, CMT Digital, and Coinbase Ventures in 2026, continually building infrastructure for stablecoin entry and exit, and fiat to stablecoin conversion;

- CoinSwitch: A leading domestic crypto trading platform in India, completed C-round financing in 2021 with participation from a16z, Paradigm, and Ribbit Capital;

- CoinDCX: An established compliant exchange in India, secured D-round financing from Antera Capital, Steadview, and Coinbase Ventures in 2022;

- EigenLabs: Founded by University of Washington professor Sreeram Kannan, completed B-round fundraising from a16z crypto in February 2024, having core products including the Ethereum restaking protocol EigenLayer, the data availability layer EigenDA, and the off-chain computation verification layer EigenCompute;

- SuperGaming: An established game developer in India, secured B-round funding from Steadview, Bandai Namco, and a16z Speedrun in 2025, transitioning from traditional mobile gaming to the Web3 crypto track;

- FalconX: A U.S.-based institutional crypto prime brokerage founded by Raghu Yarlagadda and Prabhakar Reddy, closed D-round financing in 2022.

Additionally, the Web3 gaming project KGeN has raised $43 million, and the crypto AI project Sentient raised $85 million in its first seed funding, both representing the industry.

The Developer Ecosystem is Becoming More Complete

Assessing industry maturity cannot be solely based on transaction volumes and financing; developers are the core leading indicator. Developers in the crypto space are not ordinary workers; they are the supply engine for protocols, applications, underlying infrastructures, development tools, and new products, and a continuously expanding developer scale indicates that the industry is accumulating capacity for the next bull market.

Data source: Hashed Emergent, Devfolio

From this dimension, India firmly occupies a key position in global Web3: local Web3 developers comprise 15.2% of the global total (12% in 2024), second only to the USA, and it is the fastest-growing hub for Web3 talent globally. The 2024 Developer Geographic Report from Electric Capital supports this: U.S. developers make up 19%, India 12%, the U.K. 4%; among leading global economies, only Indian developer share has seen a significant increase, while the U.S. share declines yearly.

Geographically, Bangalore leads the nation with 23.6% of developer count, followed by the Delhi capital region at 11.8%, Mumbai at 6.4%, Pune at 3.4%, and Hyderabad at 3.2%. Bangalore’s advantage stems from its foundational traditional IT industry, supplemented by regular hackathons and talent incubation projects facilitated by local communities like Solana's Superteam and Ethfolio; the diverse blooms in Delhi, Mumbai, Pune, and Hyderabad indicate that Indian Web3 talent is not clustered in a single city, but rather relies on the mature IT industry spread across the nation.

Data source: Hashed Emergent, Devfolio

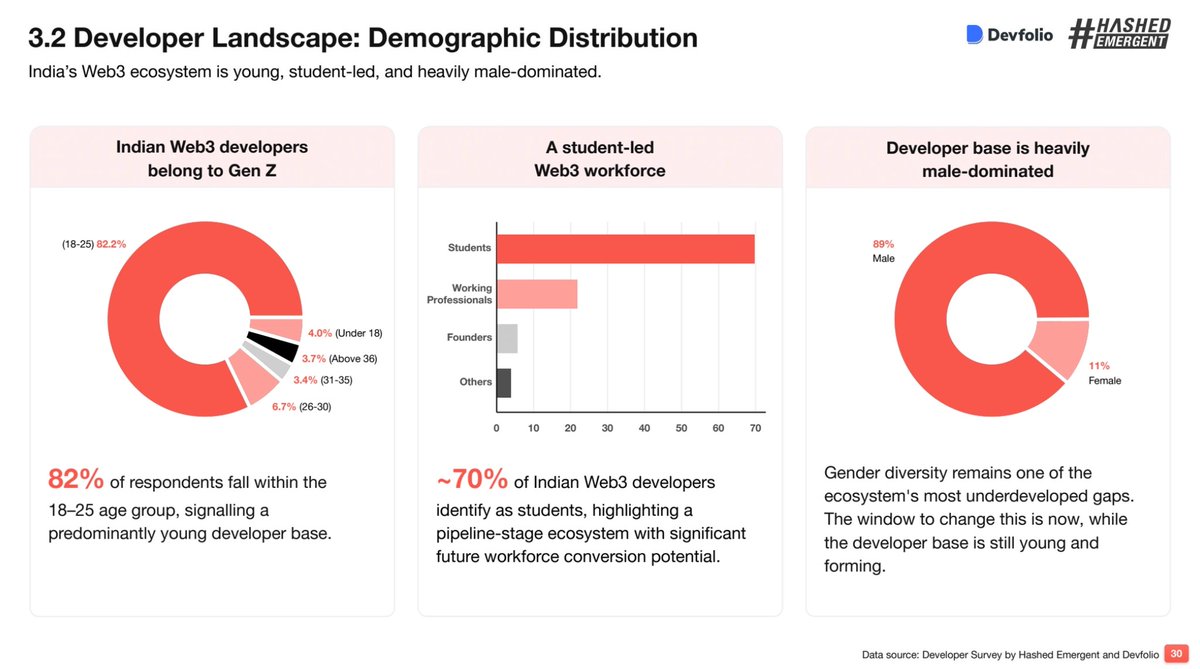

The most notable characteristic of India’s developer ecosystem is its youthfulness. According to a joint developer survey conducted by Hashed Emergent and Devfolio, 82.2% of respondents are aged between 18 and 25, with around 70% being students. This indicates that India's current Web3 ecosystem is less a mature labor market and more of a vast talent reserve set to enter the market in the coming years.

Another noteworthy aspect is that the developer community is no longer comprised solely of newcomers. The survey shows that 42.6% of India’s Web3 developers have over two years of experience, 33.2% have 1-2 years of experience, and 24.2% are novice developers with less than a year of experience. Given that new developers continue to join and the proportion of developers with more than two years of experience is growing significantly, it can be said that the ecosystem is gradually maturing.

The degree of global collaboration has been rising. Among Indian developers who have entered the field for less than a year, 18.9% are involved in cross-border remote teams; for those with more than two years of experience, the proportion engaged in cross-border collaboration has skyrocketed to 55.4%. As their technical capabilities improve, Indian developers are becoming deeply embedded in global Web3 projects.

This means that India is not only supplying talent to its domestic market but is also growing into a global hub for outsourced developers. The reality of salaries further reinforces this trend: the starting salaries in India for local internet jobs are relatively low, and living costs are rising. Global crypto projects often allow for remote work, offer better compensation, and provide flexible career paths, making Web3 a vital channel for Indian tech talent to connect with the global labor market and realize their technical value.

Indian cryptocurrency is no longer just a market of countless retail traders; it also boasts a vast number of users and builders. If the industry truly faced a slowdown, we would see contractions in developer entry, hackathon conversion, global team collaboration, and protocol eco-investment. However, data from 2025 indicates the opposite—beneath the surface of cooling trading activity, the foundational developer base supporting the next market cycle continues to strengthen.

Stablecoins in the Indian Market

Another sign of the maturation of the Indian cryptocurrency market is the emergence of stablecoins. In the past, keywords used to describe the Indian cryptocurrency market were exchanges, retail capital influx, and altcoin investments. Recently, however, the focus has shifted to more foundational financial infrastructures like payments, settlements, remittances, and asset digitization. This indicates that the market is moving beyond simple speculative demand, entering a phase of considering how to apply blockchain in the actual financial system.

In India, this transition is first evident at the startup level. Mudrex’s B2B cross-border payment project Saber Money focuses on using stablecoins for corporate cross-border settlements. In early 2026, Saber integrated with the Circle payment network and became a cooperating licensed institution, relying on stablecoins to facilitate cross-border payment flows for the rupee; Circle opened a payment channel in India through Saber, allowing traditional NEFT transfers to take two hours to arrive, while IMPS/RTGS clears nearly in real-time. Although this move does not indicate that stablecoins have formally acquired legal payment qualifications in India, it signifies interconnectivity between India’s local clearing system and global stablecoin networks.

Web3 payment infrastructure companies founded by Indian entrepreneurs are collectively betting on stablecoins. Transak raised $16 million in strategic financing led by Tether and IDG in 2025 to enhance stablecoin payment infrastructure; a local tech team has created the Lightning Network payment project Speed, which integrates the Lightning Network's rapid clearing with the price stability of stablecoins such as USDT, targeting applications in e-commerce settlements, creator payments, platform reconciliation, and cross-border remittances.

However, when examining India's stablecoin market, we must also consider the regulatory paradox. Stablecoins, with their low cost and fast settlement, have become essential tools for global cross-border payments, but privately issued stablecoins pegged to the dollar conflict with the Indian central bank’s currency control and monetary sovereignty policies. The legal definition of stablecoins' forex attributes is unclear. The Reserve Bank of India (RBI) maintains a high-pressure stance on private stablecoins due to concerns over macrofinancial stability, currency sovereignty, payment system security, and cross-border capital control.

The root of the contradiction lies in the RBI's long-term intervention in the foreign exchange market to stabilize the rupee’s exchange rate, naturally rejecting private stablecoins that can circumvent the official banking foreign exchange system and allow the free holding and circulation of dollar assets. The policy focus is more inclined towards promoting a central bank digital currency and the UPI official payment network, rather than supporting private dollar-pegged stablecoins. For stablecoin startups and investors, they face not only regulatory uncertainty but also the headwinds of a policy ecosystem that inherently opposes dollar-pegged private currency.

This contradiction serves to validate the maturity of the Indian market. In immature markets, stablecoins are primarily used for inflow and outflow at exchanges and for short-term speculation; while in India, even if regulatory tightening on private stablecoins occurs, startups are still deeply engaged in cross-border applications, while the RBI is simultaneously exploring controllable digital currencies through CBDC pilots. India hasn't fully opened up to stablecoins but is leveraging official systems to address the real issues of high remittance fees, settlement lags, and global payment interoperability that stablecoins are meant to resolve.

However, this does not necessarily meanstablecoins will find widespread application in India’s domestic payment market. More realistic opportunities may lie in cross-border application scenarios, especially considering India is one of the largest remittance-receiving countries globally, with annual remittance inflows exceeding $100 billion. Stablecoins can provide an attractively alternative solution for international transfers by lowering costs, increasing settlement speeds, and making it easier to access dollar-pegged value. However, in the domestic market, the prospects for stablecoin adoption are much dimmer. India already has UPI (Unified Payments Interface), an instant, free, and deeply embedded payment network widely used by consumers and merchants. Thus, even though stablecoins still appear attractive for remittances, offshoring value transfers, and global interconnected financial activities, their competitiveness as everyday domestic payment tools may not surpass that of UPI.

Regulatory, Tax, and Industrialization Bottlenecks

The structural paradox in India's cryptocurrency market is striking. The country possesses a vast number of users, a rapidly growing developer community, and accelerating enterprise-level applications, yet regulatory measures are neither fully permissive nor outright prohibitive. Currently, India lacks comprehensive cryptocurrency legislation, nor does it have a dedicated regulatory agency. The market primarily relies on taxation rules and anti-money laundering requirements for regulation. Furthermore, it remains unclear how stablecoins, token issuance, and tokenized assets should be treated under virtual digital asset (VDA) regulations.

Looking back at India's regulatory history, this ambiguity becomes even more evident. In 2018, the RBI issued a ban prohibiting banks from providing services to cryptocurrency companies, which was declared unconstitutional and rescinded by the Supreme Court of India in 2020; following that, the parliament made multiple attempts to legislate but has not successfully passed a cryptocurrency ban. From a legislative standpoint, India cannot legally outlaw cryptocurrency comprehensively until new laws are in place; from a fiscal perspective, the tax revenue associated with cryptocurrency is a stable source. The withholding tax, at 1%, alone generated $6 million to $7.5 million in revenue for the 2024-2025 fiscal year, meaning the government lacks financial incentives to shut down the industry entirely.

This has led India to develop a compromise regulatory model that does not rely on specialized industry regulations but instead utilizes tax law, anti-money laundering rules, and consistent administrative audits to manage an uncontested sector of cryptocurrency. Regulatory scrutiny has continued to intensify from 2024 to 2025, relying on big data to investigate crypto-related tax evasion and penalizing non-compliant platforms, increasing the participation costs for compliant users and domestic platforms, thereby driving funds out of the formal market.

This approach may facilitate short-term regulatory taxation and control over the industry but poses significant restrictions on industrial development in the long term. While India has a top-tier scale of cryptocurrency users and developers, project teams remain unclear about licensing qualifications, product compliance boundaries, and regulatory details for DeFi and non-custodial wallets. The key to breaking through lies not in tax revenue control but in establishing clear regulations to guide sustainable industry development within the country.

Taxation: Originally intended for tracing, Driving the Industry Offshore

The most pressing bottleneck is taxation. Transactions on VDA assets in India incur a flat 30% income tax, and qualifying transactions are also subject to an additional 1% withholding tax (TDS). The withholding tax has the most substantial impact on short-term high-frequency traders: 1% of funds is immediately deducted from each transaction, forcing traders to wait until tax season to apply for a refund, resulting in substantial and prolonged immobilization of liquidity. Frequent traders see their principal funds repeatedly deducted monthly, causing significant declines in fund utilization; thus, high-turnover trading becomes economically unviable.

The initial intention of the tax system was to control speculation and trace fund flows, but in reality, the continuous outflow of domestic trading has become rampant. Research from the Esya Centre shows that following the introduction of the 1% TDS, between 3-5 million Indian users transitioned to offshore platforms; from July 2022 to July 2023, Indian users’ trading volume on foreign platforms exceeded $42 billion.

The capital exodus undermines the government's original intentions. When trading moves to offshore platforms and over-the-counter P2P channels, the difficulty of regulatory tracing and taxation escalates significantly. Reports estimate that only 9.02% of the cryptocurrency assets held by Indian investors remain on local compliant platforms; if the TDS rate were to be lowered to 0.01%, it could potentially guide trading back to domestic exchanges, consequently increasing overall tax revenue.

The contradictions surrounding crypto taxation in India exceed mere tax rates; a distorted tax system is continuously pushing compliant trading toward gray and offshore markets, straying from the original intent of regulatory transparency. To achieve lasting market control, India needs to reassess its aggressive withholding tax strategy.

Anti-Money Laundering Focused Regulation: India's Financial Intelligence Agency as a Real Barrier to Entry

Currently, the core of India’s cryptocurrency regulation revolves around anti-money laundering measures. As of March 2023, local virtual asset service providers must register with India’s Financial Intelligence Unit (FIU-IND), implementing customer due diligence, suspicious transaction reporting, dedicated anti-money laundering officers, internal control compliance, travel rules, and other obligations.

The regulatory authority of India’s Financial Intelligence Unit continues to strengthen. In October 2025, the FIU sent notifications of violations of the Anti-Money Laundering Act to 25 foreign exchanges, including Huione, CEX.IO, and BingX; in 2024, Binance was fined 188.2 million rupees (about $2.25 million) for not completing FIU registration, while the FIU also promoted a ban on non-compliant foreign platforms through the Ministry of Electronics and Information Technology. At the same time, compliance registration has also become a path for overseas giants to re-enter India: in March 2025, Coinbase completed its FIU registration, acquiring qualifications for compliant operations in India, with Reuters confirming that Indian crypto service providers must register with the FIU as reporting entities and fulfill their anti-money laundering obligations.

In short, the existing regulation in India operates under an anti-money laundering registration system rather than a detailed licensing system. This set of regulations establishes a minimum industry baseline, but the entry criteria for various products remain ambiguous; for DeFi protocols, non-custodial wallets, and decentralized applications, it remains unclear who bears the anti-money laundering responsibilities and how to implement them under the current legal framework.

Stablecoins: Strong Demand, but Policy Focus on Central Bank Digital Currency

Stablecoins represent the largest opportunity in the Indian market but also the area with the most concentrated regulatory pitfalls. India has a massive remittance volume, with abundant needs for freelancers and B2B settlements, high mobile payment penetration, and active on-chain transactions; Hashed Emergent believes that despite limited entry and exit channels, the potential for domestic stablecoins is among the highest globally.

However, the top-down regulatory attitude is extremely conservative. The forex qualification of stablecoins remains undecided, with the RBI prioritizing the promotion of CBDCs, with RBI Deputy Governor T. Rabi Sankar publicly stating in 2025 that stablecoins could give rise to illegal cross-border payments, circumvent capital controls, disrupt national monetary policy, weaken the role of banks as intermediaries, and threaten financial system stability.

India is highly sensitive to dollarization, with regulatory concerns that dollar-pegged stablecoins can squeeze local currency circulation and undermine the effectiveness of capital control and monetary policy; official documents frequently warn of the impact of dollar stablecoins on UPI and other domestic benchmark payment infrastructures.

The current reality is that private B2B cross-border and offshore payment projects are continually experimenting with USDC stablecoin settlements, but the central bank and policymakers prefer to back CBDCs and the UPI ecosystem, rejecting private stablecoins from becoming a core element of the domestic payment system. The gap between policy and market demand remains unbridgeable, making it difficult for India to fully utilize the global settlement advantages of stablecoins while integrating them into the local financial system under existing policies.

Asset Tokenization: Broad Prospects but Legal Frameworks Lacking

Global traditional financial institutions are accelerating the trial of bonding bonds, funds, real estate, bank deposits, carbon credits, and other physical assets onto the blockchain, with India following up through initiatives like the International Financial Services Centres Authority (IFSCA) sandbox, Finternet projects, and capital market tokenization pilots. However, the lack of specialized token legislation hinders the on-ground implementation of physical asset tokenization, forcing the application of traditional financial legal clauses that obstruct scaling and commercialization.

The 2025 consultation letter from the IFSCA regarding physical asset tokenization states that this document does not constrain CBDC, generalized cryptocurrency, and NFTs, and solely seeks rules for asset tokenization, covering categories, issuance structures, asset custody, trading clearance, investor rights, and comprehensive risk control. This document indirectly verifies regulatory acknowledgment of long-term value in tokenization, but complementary regulations are still in the research and exploration phase.

The challenges of tokenization not only lie in the technical aspects but also involve many interwoven issues, such as how tokens represent ownership of real assets, whether token transfers are seen as legitimate ownership transfers, how to protect token holders' rights in the event of custodian bankruptcy, how foreign investor participation interacts with foreign exchange controls, and how profit from token trading is treated under tax law.

Tokenization is both a marker of the industry’s maturation journey in India and a glimpse into the complexity of the regulatory system. India has relied on UPI and Aadhaar to establish top-tier public digital infrastructures globally, but tokenization touches on multiple legal clauses concerning property, foreign exchange, and securities law; in order to achieve large-scale implementation, India needs more than just technological pilots—it requires complementary property legislation and investor protection regulations.

Inherent Paradoxes of the Developer Ecosystem

India boasts the world’s second-largest Web3 developer community, yet the industrial value created by local talent often fails to stay domestically. Many developers work for overseas protocols or registered entities outside India, or Indian founders have projects registered offshore in Singapore, Dubai, the British Virgin Islands, or Delaware, USA.

This is evident when viewing the lists of companies at the B-round and later financing stages mentioned earlier. Many Web3 giants associated with Indian founders or talent, including EigenLabs, Avail, Biconomy, Instadapp, and FalconX, do not have structures based on Indian entities. Instead, they tend to establish company structures in jurisdictions like Singapore, Dubai, the British Virgin Islands, or Delaware. Notable exceptions include Indian exchanges like CoinSwitch and CoinDCX, which are rooted in the domestic market, while for protocols and infrastructure companies, offshore registration is often the more common choice.

Offshore registration is not simply a matter of founders' preference. The registration costs for Indian crypto companies are high, opening bank accounts is challenging, regulatory rules are unclear, incentives for equity compensation are taxed heavily, and obtaining dollar financing offshore is far more straightforward, compelling entrepreneurs to choose between registering companies abroad or working remotely for overseas projects. With talent remaining in India, the resulting benefits flow overseas.

The consequences are clear; India continuously outputs a workforce of developers, but project equity, intellectual property, and long-term tax sources all flow outwards. The "world's second-largest Web3 developer market" represents talent reserves but does not reflect the competitive edge of the domestic industry. For India to capitalize on its developer dividends, it cannot simply increase the number of programmers; it must also implement friendly regulations, optimize the tax system, ease banking procedures, and improve investment and financing regulations to retain local entrepreneurial teams. Only by retaining these projects can India transform from a talent provider into a global hub for the Web3 industry.

Conclusion

In summary, the Indian cryptocurrency industry is not in a slump; rather, it is steadily maturing in a diversified direction. Early stage industry data was dominated by the number of exchange users and the altcoin bull market; today, the indicators are more multidimensional: ranking first in the global cryptocurrency adoption index, with annual on-chain inflows of $338 billion, duplicate transaction amounts in derivatives nearly doubling, a rebound in mature B-round financing, leading prevalence of mobile wallets globally, and the mass roll-out of Web3 pilot projects by giants.

The existing shortcomings in Indian cryptocurrency do not stem from a lack of demand; users, entrepreneurs, developers, and data regarding on-chain financing are all abundant. The pain points lie in the insufficient accompanying systems that do not match the market scale: high taxes prompt a shift of funds into outside and offshore markets; anti-money laundering regulations maintain compliance baselines, but there are gaps in specific product rules; the cross-border necessity for stablecoins is clear, but the central bank prioritizes official digital currencies; the potential for physical asset tokenization is vast, yet property and accompanying legislation are missing.

The next phase for cryptocurrency in India will not hinge on how many new retail investors join, but on establishing systems that suit the existing users and builders. If India can adjust its tax structure, formulate clear rules for stablecoins, tokenization, and DeFi, and strike a balance between consumer protection and innovation, its large-scale cryptocurrency adoption could potentially translate into true financial infrastructure innovation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。