Key Takeaways:

- FG Nexus bought 50,770 ETH for $196M in 2025, then sold 36,025 ETH at lower prices.

- FG Nexus realized losses above $85M, highlighting risks in ethereum treasury strategies.

- Everstake data suggests ETH firms increasingly rely on staking as markets stay challenging.

FG Nexus is facing steep losses from its ethereum treasury strategy after buying heavily into ether in 2025 and later selling much of the position into a weaker market.

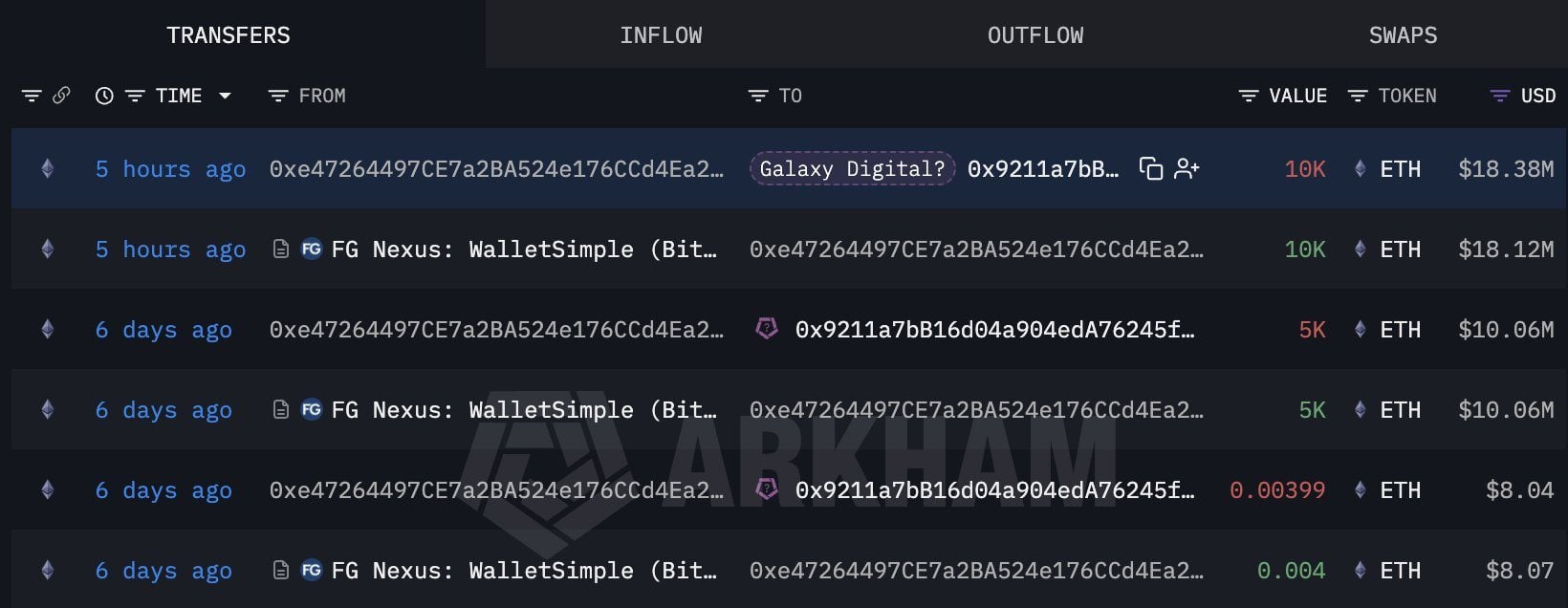

The Nasdaq-listed company acquired 50,770 ETH between August and September 2025 for about $196 million with an average purchase price of $3,860 per token. The trade has since moved sharply against the company.

FG Nexus began selling ether in November 2025 and just sold 36,025 ETH for about $83.92 million, according to on-chain data shared by Lookonchain. The average sale price was $2,330 per ETH. That leaves cumulative losses on the company’s ethereum treasury strategy above $85 million.

Source: Arkham

FG Nexus had previously described ETH as its primary treasury reserve asset. That made its balance sheet more exposed to ethereum’s price action at a time when several public companies were trying to position themselves as crypto treasury vehicles.

The losses show the risk of that model. Ether treasury companies can benefit when prices rise, but their equity story can weaken quickly when token prices fall or when firms are forced to sell below their acquisition cost.

The broader sector has already been under pressure. A recent Everstake study found that publicly listed ether treasury firms are dealing with a tougher market, with staking emerging as one of the few consistent revenue sources.

For FG Nexus, staking has played a meaningful role in revenue generation. The company reported $2.4 million in total revenue for fiscal 2025, with ETH staking accounting for $1.5 million of that amount.

That means staking represented most of the company’s reported revenue, even as the value of its ether treasury declined. The contrast points to a wider challenge across the sector: yield can help support operating income, but it may not be enough to offset large mark-to-market losses or poorly timed treasury sales.

FG Nexus’ experience also reflects a shift in how investors are judging digital asset treasury companies. Holding crypto is no longer enough. Markets are increasingly focused on cost basis, liquidity, staking yield, and whether management can grow net asset value per share through a full market cycle.

For now, FG Nexus stands as a cautionary example. The company moved early and aggressively into ethereum, but its realized sales show how quickly a treasury strategy can turn from a growth narrative into a balance-sheet burden.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。