Author: Hu Tao, ChainCatcher

1. The Non-existent Liquidity Contest

In the past few months, tokenized US stocks have become one of the most talked-about topics in the crypto industry at an unprecedented pace.

From the continuous emergence of platforms supporting on-chain stock trading, to an increasing number of exchanges and DeFi protocols starting to layout relevant businesses, and to the gradual clarification of the regulatory environment, the tokenization of US stocks has evolved from a fringe concept to the most explosive direction in the entire RWA (real-world asset) track.

However, as the heat rapidly rises, there is also a growing concern in the market: once high-quality stock assets like Nvidia, Tesla, Apple, and Coinbase are moved on-chain, will the funds originally belonging to the crypto market be siphoned away by these traditional assets? Will Bitcoin, Ethereum, and even altcoins face greater liquidity pressure as a result?

This concern is not unfounded. For many ordinary investors, when they can trade through on-chain accounts, there is one side with highly volatile and cash flow-supported crypto assets, and the other with stocks of global leading tech companies that have real businesses, profits, and valuation systems, the latter seems to be more easily recognized by traditional funds.

However, if we extend the time dimension, one might find that the wave of US stock tokenization does not pose a direct threat to the crypto industry, but is more likely the most important expansion since DeFi Summer—indeed, possibly the most important in crypto history.

Essentially, US stock assets and the vast majority of crypto-native assets are of different natures. Historical data and on-chain fund flows indicate that when asset categories on-chain are expanded, there may be short-term portfolio adjustment friction, but in the medium to long term, capital with different risk appetites will form a complementary rather than a substitutional relationship on-chain.

More importantly, the prosperity of tokenized US stocks heavily relies on the settlement layer of stablecoins and native public chains. Without USDC and USDT, there would be no payment tools for buying stock tokens; without Ethereum, Solana, or Base, there wouldn't be a carrier for issuance, trading, and clearing; without DeFi protocols, holders of stock tokens would not be able to release their capital efficiency.

Investors may enter the on-chain world to purchase stock tokens, but a significant portion will gradually start to engage with stablecoin payments, on-chain lending, yield products, and even crypto-native assets.

"Stablecoins, tokenization of US stocks, etc., once on-chain, will not just lie idle on-chain; they must be liquid, and the composability of crypto will be fully utilized. Once there are good narratives, good projects, not only will funds from the crypto circle come in, but funds from outside the circle will also flow in; this is just a competition in the same arena," said well-known crypto researcher Blue Fox.

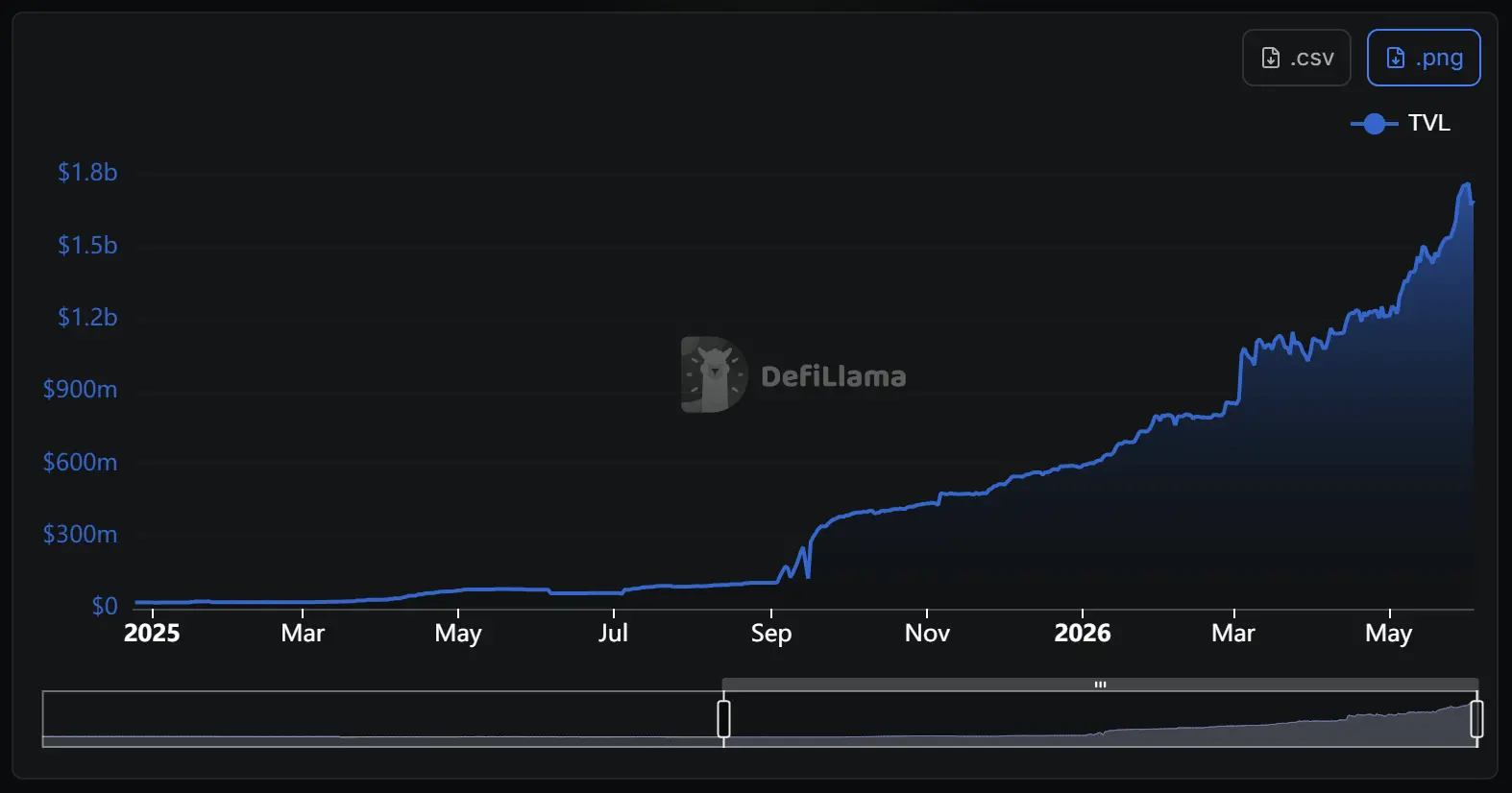

According to DeFillama, the total TVL of tokenized stocks and ETFs has now exceeded $1.7 billion, making it the fastest-growing vertical field in DeFi.

Recently, exchanges such as Binance, Bitget, and Gate have announced the launch of real-time US stock trading features and support for tokenization and bringing it on-chain, which means the market size for US stocks will continue to expand rapidly, and the market demand has been fully validated.

More significantly, an increasing number of traditional financial giants are also accelerating their layouts. In mid-May, the United States Securities Depository Trust & Clearing Corporation, a global securities clearing giant DTCC, announced the integration of Chainlink to build the data and orchestration layer for its tokenized collateral platform, and later announced at the end of the month that it would launch DTC custody asset tokenization services on the Stellar network. These developments have directly stimulated the rise in relevant token prices, bringing direct benefits to the adoption rates of crypto market infrastructure service providers.

Such dynamics convey an extremely clear signal: the traditional financial world not only does not view blockchain as a "competitor," but is actively embracing public chains as the infrastructure for asset clearing and settlement. DTCC's choice is not an isolated case—JPMorgan's Onyx platform, Citibank's tokenization services, BlackRock's BUIDL fund, and the Nasdaq and NYSE's respective approved tokenized stock plans all point in the same direction: the underlying architecture of global finance is undergoing a system-level "on-chain" migration.

This has dual value for the crypto industry. On one hand, it provides the strongest endorsement for the regulatory legitimacy and market credibility of tokenized assets—when institutions like DTCC choose public chains, it signals to tens of thousands of financial institutions globally that "on-chain assets are trustworthy." On the other hand, the entrance of these institutions directly drives the adoption rates of existing crypto infrastructure service providers, with Chainlink's data oracles, Stellar's asset issuance standards, and Ethereum's smart contract capabilities all receiving actual demand validation in the process.

2. Driving a System-level Upgrade of the Global Financial Infrastructure

From a broader perspective, the greatest significance of the US stock tokenization craze for the crypto sphere may not be how much "new money" it can bring, but rather that it serves as an undeniable proof of the practical value of blockchain technology to the traditional financial world for the first time.

For more than a decade, the crypto industry has been trying to prove the importance of blockchain to the outside world, but many narratives have remained at the level of technical vision. In contrast, the tokenization of US stocks directly corresponds to the core demands of the global capital markets—more efficient issuance, lower-cost circulation, more transparent settlement, and wider global accessibility. When Wall Street begins to actively embrace these capabilities, blockchain finally transcends being just a story of the crypto industry, becoming the infrastructure upgrade participated in by the entire financial industry.

Today, tokenization is shifting from being a marginal experiment driven by DeFi projects to being a mainstream financial trajectory led by large asset management institutions, custodians, exchanges, and financial market infrastructure providers. The change in leadership itself implies that this "on-chain movement" is not a "downgrade" of a financial game, but a system-level upgrade of the global financial infrastructure.

And as global investors begin to get accustomed to holding stocks, bonds, funds, and even various real assets through blockchain, what the crypto industry gains will not just be a fleeting hype, but a fundamental expansion of its value-carrying capacity.

"Every instance of market maturity is essentially a process of capital flowing from inefficient assets to efficient ones. As junk coins are gradually eliminated, protocols, infrastructure, and financial products that can truly create value will have the opportunity to achieve more reasonable valuations. The tokenization of US stocks may not be the endpoint of the crypto market, but it is likely to be an important turning point for the crypto market transitioning from a 'speculative market' to a 'capital market,'" said crypto trader @Win_Win_Bro.

Therefore, rather than seeing the tokenization of US stocks as a threat to the crypto industry, it is better viewed as one of the most important milestones in the process of blockchain becoming part of the mainstream financial system.

When the $75 trillion US stock market connects with crypto infrastructure—achieving even a mere 2% penetration rate—it will also mean $1.5 trillion of added on-chain value. By then, there will no longer be debate: has the tokenization of US stocks siphoned off liquidity, or injected an unprecedented value anchor into blockchain.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。