Relying on the RWA tokenization wave, Ethereum may welcome a revaluation of its value.

Written by: Lucas, former Bankless member

Translated by: Saoirse, Foresight News

Core Summary:

- All assets will be tokenized in the future;

- Ethereum will become the settlement layer for various tokenized assets;

- ETH will bear the network security staking, capturing all value generated from settlement activities;

- The global financial system is overall transforming towards asset tokenization;

- Relying on security, stability, and long-term ecological barriers, Ethereum will capture a large market share in the tokenized sector.

Proliferation of "Ethereum is dead" rhetoric

Currently, on crypto social platforms, the market's pessimism towards Ethereum has reached historic lows. Many peers who have worked together for years have gradually exited the Ethereum space, with some completely leaving the crypto industry, and the vast majority no longer holding ETH. The core reason is that they no longer recognize its investment value. This is not directed at any individual or circle, but rather a general situation I have witnessed in the industry.

A massive exit of funds can be attributed to the fact that cryptocurrency is no longer the cutting-edge popular technology; artificial intelligence, robotics, and life longevity research have taken its place as capital darlings. However, the poor returns brought about by the weakening ETH market are the key inducement for the pessimism. To put it bluntly, the experience of holding ETH over the past few years has been extremely poor.

Nonetheless, I still firmly hold a bullish view on Ethereum and ETH, with confidence even surpassing any previous stage, and I encourage readers to be bullish as well. In fact, Ethereum is ushering in the most anticipated phase of growth and popularization in its development history.

Discussing poor price performance

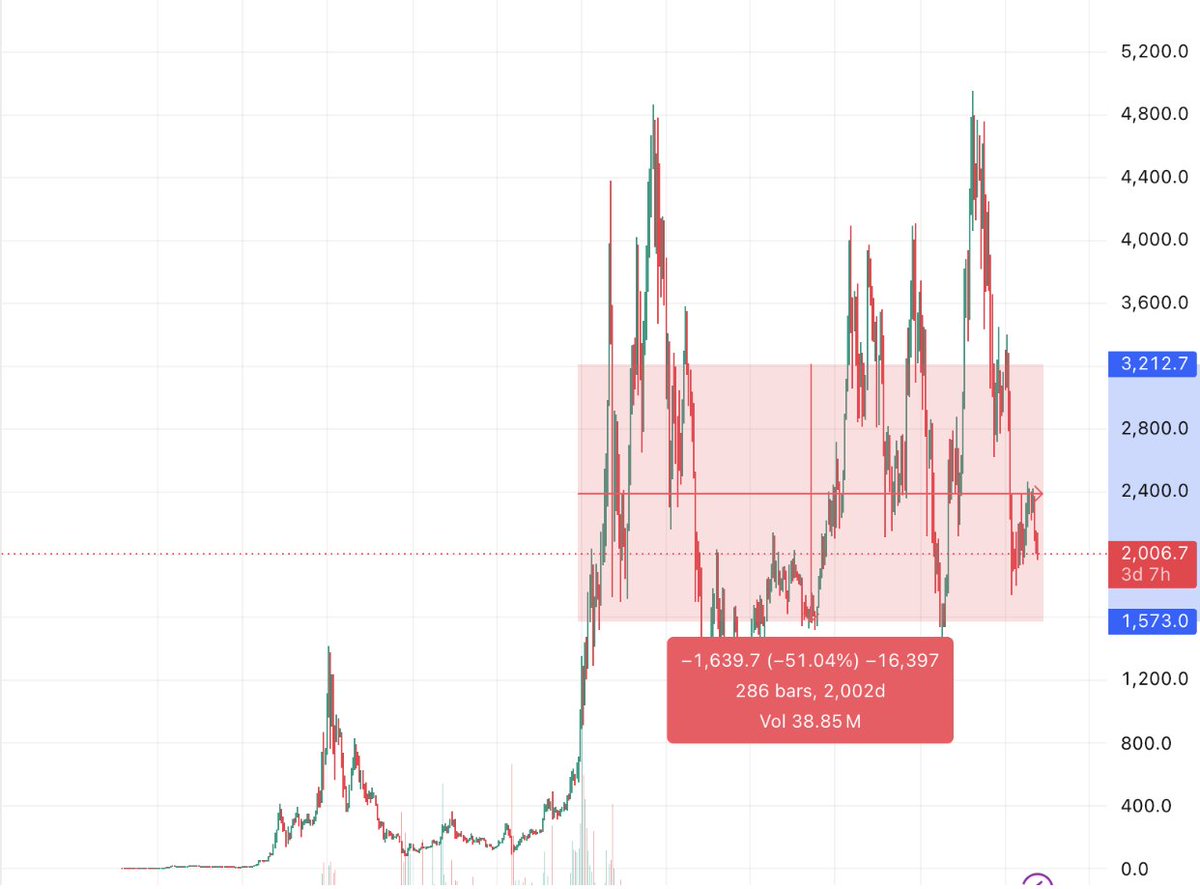

First, let's directly face the most conspicuous issue: over the past nearly five years, ETH's price performance has been extremely poor. Investors who entered and held positions in 2021 had the best luck just breaking even, while most are deeply trapped. Even with the recent overall market pullback, Bitcoin's current price remains stable at the 2021 bull market peak, with the 2025 peak expected to double from that high. In contrast, ETH has plummeted by about 60% from the last historical high, failing to reach a new high in 2025, and has not even breached the $5,000 mark.

During the same period, the S&P 500 index has almost daily set new historical records, with popular sectors like Wall Street AI, semiconductors, and energy stocks all soaring, which makes ETH's performance even more pathetic.

However, the good news is that when looking at the longer term, ETH has merely fallen into a prolonged box trend. Ethereum currently has a market capitalization exceeding $200 billion, with a price consistently holding the $2,000 mark for years, firmly among the top 100 global asset valuations. Observing the dynamics of capital market development, it is normal for high-quality growth targets to go through several years of consolidation before entering a long bull market.

Ignoring percentage change values, this primarily measures the duration of price staying within this range.

Amazon, Nvidia, Apple, and Microsoft, all global giants, have gone through similar journeys:

- Amazon: Led by Bezos, the company oscillated for nearly ten years after the burst of the internet bubble in the 2000s, eventually becoming a top global enterprise after weathering the industry winter;

- Nvidia: Experienced seven years of long consolidation in the 2010s, riding the AI wave to achieve an epic surge in stock price and entering the top tier of global market capitalizations;

- Apple: Endured long periods of confusion during the 1980s and 1990s, only taking off after Jobs returned to the company in 1997;

- Microsoft: After 2000, the stock price oscillated for about 15 years; investors who entered in 2000 only broke even by 2015, and it is now the second-largest company by market capitalization globally.

It is not difficult to summarize the pattern: most top global assets undergo a long and tedious period of oscillation and consolidation; some targets briefly spike to new highs before retreating again, waiting for the industry catalyst to kick off a new bull market. Additionally, during the oscillation and bottoming phases of the aforementioned companies, the US stock market often continues to hit new highs. In this logic, ETH's weak performance over the past five years is not abnormal in financial history.

Setting aside the price, Ethereum's current fundamentals are actually at a historically optimal stage.

On-chain ecosystem data continues to improve

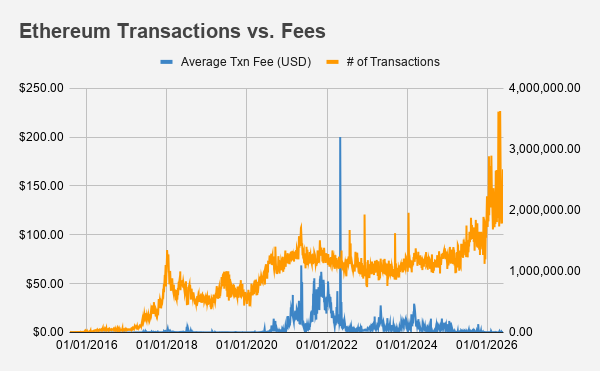

According to the market's pessimistic views, a weakening market must be accompanied by a drop in on-chain activity: declining trading volumes, high fees, and stagnation in real applications, but the actual data shows the complete opposite. Ethereum's on-chain trading volume is steadily climbing, and fees are hitting new lows, with the speed of asset tokenization continuing to accelerate.

Data source: Etherscan

Based on Etherscan data: in May 2026, Ethereum's daily average transaction count reached 2.27 million, setting a historical peak for the entire network; during the same period, the average transaction fee was only $0.27, compared to the exorbitant Gas fees of $50-100 typical during the 2021 bull market, with costs significantly decreasing under the premise of doubled trading volume.

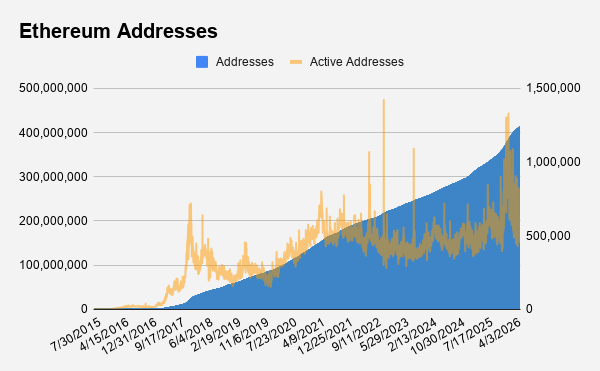

The total number of on-chain addresses has surpassed 400 million, with a daily average growth rate of about 0.08% in 2026, and the number of daily active users on-chain has steadily exceeded 1 million in recent months. At the current growth rate, absent significant industry catalysts, Ethereum may see its total address count surpass 1 billion by mid-2029.

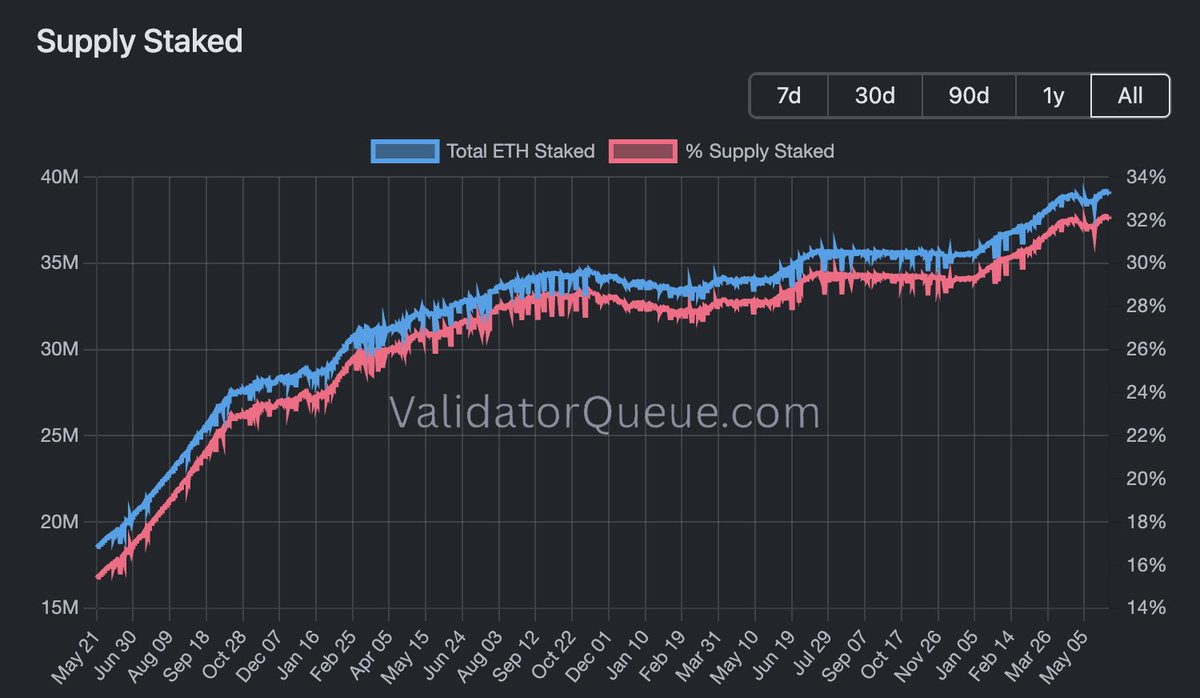

Staking is also constantly breaking records: over 32% of the entire ETH has completed staking lockup, continuously underpinning network security.

Data source: validatorqueue.com

In summary, Ethereum has achieved expansion and iteration while balancing decentralization and security bottom lines, having never experienced a network-wide failure in over ten years, and with its ultra-neutral, secure, and programmable block resources, it has obtained core leverage to compete for global financial infrastructure; this is also a precondition for subsequently carrying a vast amount of traditional asset tokenization.

Becoming the underlying infrastructure of the global financial system

Since entering the industry in 2017, my long-term logic regarding Ethereum has remained unchanged:

- All valuable assets in the world will eventually be tokenized;

- Ethereum will become the unified settlement layer for all kinds of token assets;

- ETH will capture all value increments derived from the settlement layer.

In the first decade of Ethereum, it mainly served as a testing ground for crypto-native assets; DeFi, NFTs, meme coins, and other forms have all been born and grounded here, solidifying the foundational ecological base; while in the upcoming developmental stage, Ethereum will embark on a new journey towards a trillion-dollar market valuation.

For established crypto-native players, traditional finance moving on-chain may seem somewhat tedious, but it is an indispensable step for blockchain to go mainstream, worthy of industry-wide enhancement. In the future, the total scale of traditional physical assets globally, amounting to $700 trillion, will most likely be tokenized on-chain, with Ethereum being the preferred network to carry this.

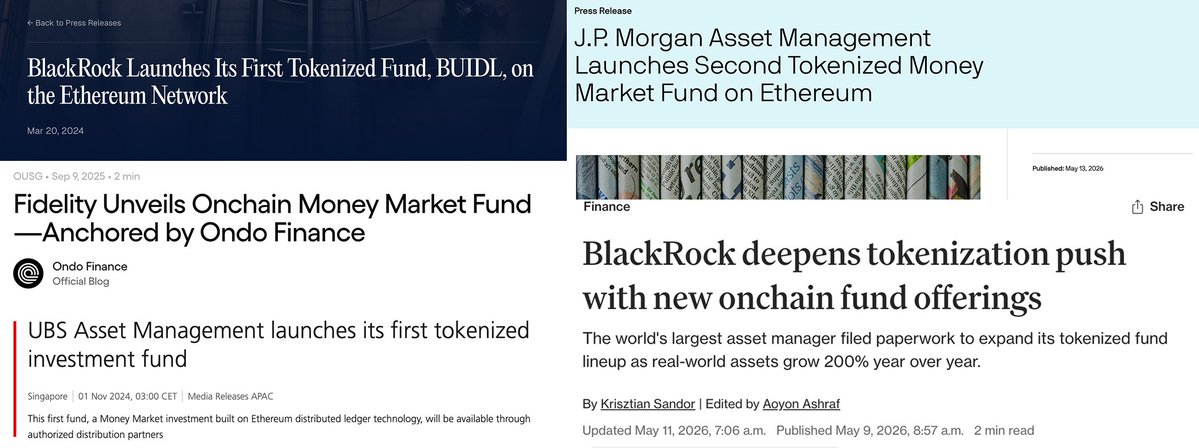

Many people counter that Ethereum's expansion capacity is insufficient to accommodate a vast amount of assets, and that other public chains will divide the market. However, the current deployment data has already disproved this viewpoint: traditional financial institutions are increasingly integrating into the Ethereum ecosystem.

A series of headlines from the past two years share a common theme.

The core demand of institutions entering the market is certainty: banks, asset management, and clearinghouses choosing blockchain to manage trillions of dollars in assets is a major strategic decision, aiming to capture the tokenization dividend while avoiding professional risks arising from decision-making errors.

Of course, public chains like Hyperliquid and Solana can also carve out a piece of the pie; the tokenization sector is large enough to accommodate multiple public chains to develop together, and it's impossible for one company to monopolize. However, pursuing stability, traditional institutions will prioritize Ethereum when deploying RWA.

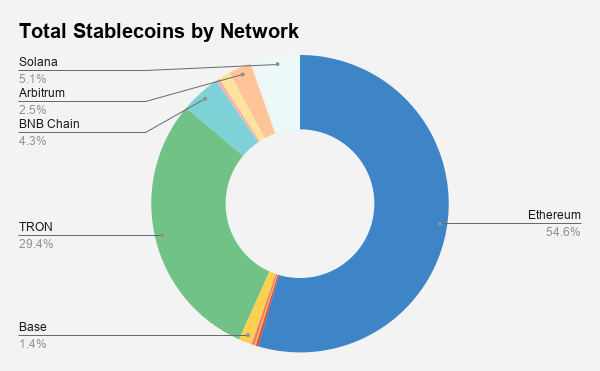

Deployment data supports this viewpoint: stablecoins are the first tokenized real assets to successfully match product market fit, with a total circulating market cap exceeding $30 billion; Tom Lee referred to stablecoins as the "ChatGPT moment" of the crypto industry, with Ethereum holding 54% of the total market cap for stablecoins.

Data source: rwa.xyz

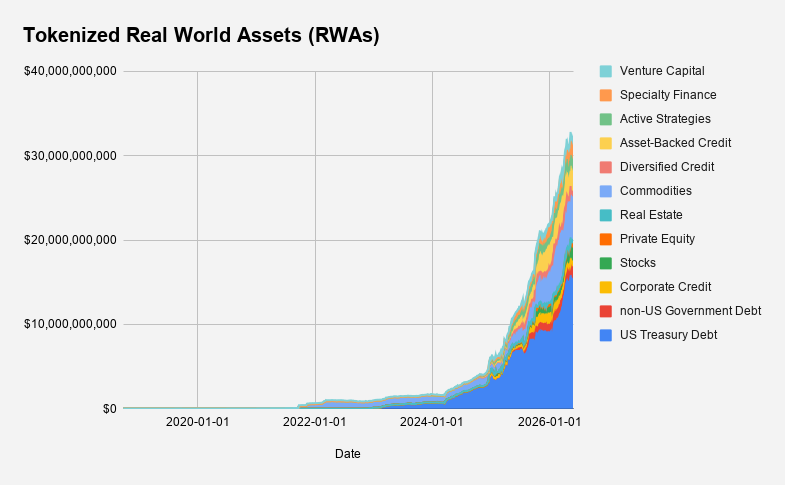

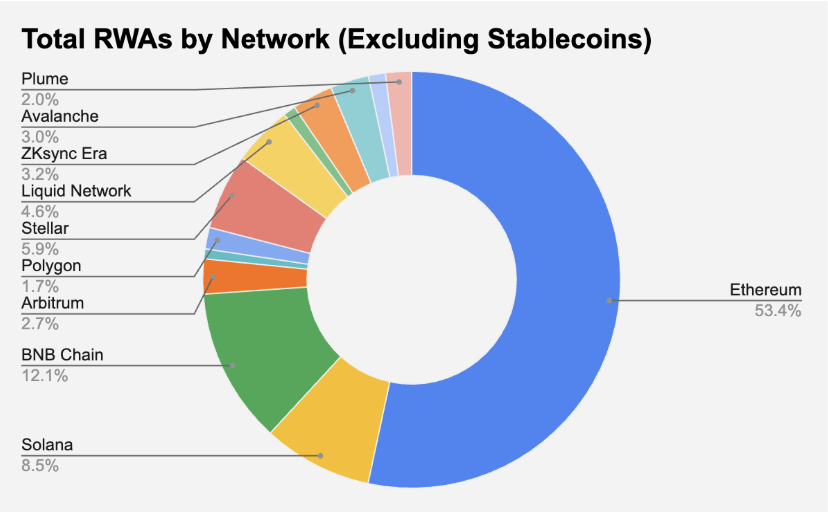

As of June 1, 2026, the total volume of tokenized real assets (RWA) has surpassed $30 billion, with the growth curve for the sector steeply rising; over 53% of RWA assets are deployed on the Ethereum chain. Even as other public chains start from scratch competing for non-stablecoin RWA market share, Ethereum still firmly occupies a dominant position.

Data source: rwa.xyz

The current development stage of the RWA sector parallels the nascent phase of DeFi from 2019-2020: new sector logic is clear, and early data is steadily improving. Looking back at past data from DefiLlama, the total locked value in DeFi saw exponential growth in the first half of 2020, while ETH’s market was also in a prolonged period of consolidation.

When the DeFi bull market fully erupted and liquidity mining became a hit throughout the network, ETH faced downward pressure from the COVID market, with a market cap of only $20-25 billion, a tenfold reduction compared to the current $230 billion market cap; concurrently, the newly formed BNB Chain once threatened Ethereum’s status with lower transaction fees. It wasn’t until the volume of DeFi assets reached about 20% of Ethereum's total market cap that ETH started to rise from $300, surging to $4,000 by year-end, entering a super bull market.

Comparing it to the current situation: excluding stablecoins, the total scale of non-stablecoin RWA on Ethereum is about $16 billion, accounting for only 7% of ETH's total market cap, similar to the early stages of DeFi, though overall volume is ten times what it was back then: early DeFi started at $3 billion, while RWA starts at $30 billion; early ETH bottomed at $200, whereas the current ETH bottom is $2,000; early competitors were BNB Chain, while the current competitors are Hyperliquid.

Additional note: In the earlier years, DeFi relied on collateral demand to stimulate a large amount of ETH buying, and NFTs further strengthened the narrative of "ETH as equivalent to digital gold"; however, at that time Ethereum had not yet implemented POS staking and the EIP1559 burning mechanism, whereas now both rules have been fully implemented, with every on-chain transaction directly contributing to ETH's deflation and value support.

In terms of a tenfold space projection, the overall scale of RWA (excluding stablecoins) in this cycle is expected to surpass $1 trillion. The US "CLARITY Act" is a key catalyst; according to Polymarket data, the probability of the bill being signed by 2026 is about 55%. The bill’s implementation will open compliant on-chain channels for all financial assets in the US, proving to be a super favorable development for Ethereum.

Ethereum's vitality remains strong

Stocks, bonds, commodities, real estate, art, intellectual property—all assets with value will eventually move towards tokenization, representing the next major revolution in the global financial sector.

In the first twenty years of the crypto industry, the focus has been on the issuance and innovation of crypto-native assets; in the next twenty years, the industry’s focus will shift to moving traditional physical assets on-chain.

Even amid the current generally bearish opinions on Ethereum in the crypto discourse, I remain convinced: Ethereum will become the underlying foundation for the majority of tokenized assets worldwide. Relying on the accumulated barriers of security, reliability, and liquidity built over the years, Ethereum’s advantages cannot be replicated in the short term. Once a vast amount of global assets are established on Ethereum, the market will ultimately reprice ETH, replicating the past valuation surge narrative.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。