TL;DR

The Essence of Pre-IPO: The crypto market is pre-productizing and public trading the valuation expectations of unlisted companies.

Asset Structure: Synthetic price exposure, economic rights mapping, on-chain funds or portfolio assets, predicting market event probabilities.

Market Path: Exchange "contractualization", on-chain platform "asset tokenization", predicting market "event probability."

Triple Contradiction: Liquidity democratization vs. authenticity of rights, price discovery vs. emotion amplification, RWA expansion vs. regulatory conflict.

Prospects and Conclusion: What is actually traded in Pre-IPO is not necessarily stock, but the market's expectations of future valuations.

In recent years, the main line of RWA has primarily focused on U.S. Treasury bonds, money market funds, private credit, real estate revenue rights, and tokenized stocks. Their commonality lies in moving off-chain assets onto on-chain, allowing users to gain lower-friction financial exposure. However, since April 2026, with the rising IPO expectations of super unicorns like SpaceX, OpenAI, and Anthropic, Pre-IPO has begun to become a more communicative branch of RWA.

I. The Essence of the Pre-IPO Craze: The Crypto Market's Productization of Valuation Expectations

In traditional finance, Pre-IPO is not a new phenomenon. Qualified investors can participate in unlisted company equity through secondary markets, SPVs, private equity funds, employee stock transfers, or specific wealth management channels. However, these channels usually have high thresholds, lack transparency, involve long lock-up periods, and have weak liquidity while needing to meet accredited investor rules. The difference in the crypto market is that it excels at transforming a narrative that is not yet fully priced into a tradable product. Previously, this ability was reflected in new coin pre-markets, airdrop points, futures of unlisted projects, meme assets, and prediction markets; now it has shifted to the valuation of unlisted companies. The surge in Pre-IPO trading is superficially attributed to the IPO expectations of SpaceX, OpenAI, and Anthropic. The deeper reason is the evident structural mismatch between traditional private equity markets and crypto markets.

First, SpaceX, OpenAI, and Anthropic are among the most globally recognized tech assets. The market's interest in them goes beyond financial returns, encompassing industrial narratives: commercial aerospace, AI infrastructure, large model computing power, enterprise automation, robotics, defense technology, satellite internet. These narratives have a natural communicative power and are suited to be packaged as tradable themes on crypto trading platforms.

Second, the entry barriers for the traditional Pre-IPO market are high. Ordinary users find it challenging to obtain real shares of SpaceX or OpenAI directly. Even if there are secondary share transfers, they may require a high minimum investment amount, accredited investor status, complex subscription documents, long lock-up periods, and limited exit channels. Private equity firms typically impose restrictions on share transfers through company articles, shareholder agreements, rights of first refusal, board approvals, etc. This opacity makes the question of "can one participate before the IPO" itself a scarce narrative.

Third, crypto exchanges have productization capabilities. For exchanges, Pre-IPO can be designed as perpetual contracts, pre-market contracts, subscription vouchers, stock tokens, or event contracts. These products do not necessarily require real delivery of underlying stocks but can instead build a price market around valuation expectations. Their essence is converting the uncertainty of "future IPOs" into "prices that can be traded today."

Fourth, the current crypto market is looking for trading themes with a stronger connection to the real world. In the past cycle, the market relied more on native token narratives, such as Layer 1, DeFi, NFTs, GameFi, AI Agents, and memes. The difference with Pre-IPO is that it ties crypto trading infrastructure to the most popular private companies in the real world, allowing users to trade not just on-chain projects but also their views on the future valuations of traditional tech giants. The names SpaceX, OpenAI, and Anthropic carry inherent traffic, quickly attracting attention from non-traditional RWA users. For exchanges and on-chain platforms, Pre-IPO is a product direction that combines hot topics, trading volume, user acquisition, and brand differentiation.

Therefore, the reason why IPO expectations for SpaceX and OpenAI ignite Pre-IPO trading is not because the crypto market suddenly acquired a large number of real unlisted stocks, but because these IPO expectations provide a sufficiently strong tradable narrative. Trading platforms decompose this narrative into contract prices, subscription amounts, on-chain tokens, prediction markets, and liquidity pools. The craze for Pre-IPO is essentially the crypto market's productization of "pre-IPO valuation expectations."

II. The Asset Structure of Pre-IPO: What Are Users Really Buying?

The Pre-IPO products in the current market are not all equivalent to "unlisted company shares." In most cases, what users acquire is not equity in the traditional sense but rather financial mappings designed around IPO expectations, valuation changes, or future liquidity events. From an asset structure perspective, the current market can be roughly divided into four categories: synthetic price exposure, economic rights mapping, fund portfolio assets, and prediction market event contracts. Different structures determine the rights, risk boundaries, and pricing logic that users ultimately possess.

2.1 Synthetic Price Exposure

This type of product is essentially a "price contract established around valuation expectations." Users gain exposure to price fluctuations rather than real company equity.

Common forms include perpetual contracts, indexed prices, or over-the-counter quotes. Platforms usually anchor the valuation of a certain unlisted company by referencing private valuations, financing round prices, secondary market transaction information, or internal pricing models and then convert this into a tradable price. This means that users do not possess shareholder rights and cannot demand real stock redemption. Their returns and risks mainly come from the market's repricing of future IPO valuations.

The advantage of this structure is high liquidity, strong trading efficiency, the ability to go long or short, and direct access to mature contract trading infrastructure. However, the core issue is that: due to the absence of a publicly accessible spot market, prices lack strong anchoring mechanisms. Once market sentiment deviates from fundamentals, prices may deviate significantly without effective arbitrage forces to correct them.

2.2 Economic Rights Mapping

Compared to purely price contracts, these products are closer to the "on-chain mapping of private equity." Their core logic typically involves indirectly obtaining the economic benefits of a certain unlisted company through SPVs (special purpose vehicles), fund shares, revenue rights agreements, or forward rights arrangements, and then tokenizing that interest for market trading.

Users gain not only price volatility exposure but also a certain "economic rights exposure related to underlying equity." Theoretically, this structure is closer to real Pre-IPO investment because there may be actual holdings, SPV arrangements, or future revenue rights behind it. However, it is also more likely to touch legal and compliance boundaries. Unlisted companies often have strict restrictions on equity transfers, and if the underlying rights cannot be formally recognized, the legal validity and enforceability of the related tokens will be challenged.

Therefore, the biggest risks of this type of product do not necessarily stem from price volatility but from whether the underlying rights truly exist, are enforceable, and whether the structure itself is recognized by the company or regulators.

2.3 On-chain Funds or Portfolio Assets

Some Pre-IPO products do not directly anchor a single company but provide risk exposure in a "fund portfolio" manner. This structure is closer to "thematic funds on chain" or "VC asset portfolio tokenization." Users gain exposure to a portfolio that includes multiple unlisted companies rather than just equity in a single company.

The advantage lies in risk diversification. Compared to betting on the IPO timing and valuation changes of a particular company, a portfolio structure can reduce the volatility shocks stemming from a single event. However, at the same time, the risks borne by users shift from "company risk" to "fund risk." Product prices are influenced not only by underlying assets but also by fund NAV, liquidity, premiums, issuance structures, and secondary market trading behavior. Therefore, these products are more like "high-volatility thematic funds" rather than traditional single Pre-IPO stocks.

2.4 Prediction Market Event Probabilities

Another type of product does not trade rights or prices but rather trades "the IPO event itself." Users trade the outcome of events, such as whether a particular company will IPO, when it will IPO, or which company will IPO first, making it fundamentally closer to a probability market or information market.

This type of product does not involve real equity and does not emphasize economic rights, making its legal structure typically clearer. However, it cannot replace true equity exposure and is more a way to express market expectations. Its core value lies in converting the originally hard-to-quantify IPO expectations into real-time tradable market probabilities.

Overall, most current Pre-IPO products belong to "financial mappings established around IPO expectations," rather than actual stocks. What the crypto market is truly doing is not simply copying the traditional equity market but is re-packaging private valuations, financing expectations, and IPO events into liquid, tradable, and leverageable financial products.

III. The Market Paths of Pre-IPO: Three Routes of Exchanges, On-chain Platforms, and Prediction Markets

As the popularity of unlisted companies like SpaceX, OpenAI, and Anthropic continues to rise, Pre-IPO is gradually evolving from a "niche private equity market" into a new crypto trading track. However, the current market has not formed a unified model. Different platforms have different understandings of Pre-IPO: some view it as a new contract trading target; others aim to tokenize private assets; still, others focus more on the probability expressions of the IPO events themselves. Currently, three different development paths are forming in the market: the "contractualization" path of exchanges, the "asset tokenization" path of on-chain platforms, and the "event probability" path of prediction markets.

3.1 Exchanges: The "Contractualization" of Pre-IPO

For exchanges, Pre-IPO resembles a "new trading target" rather than a traditional equity business. The core logic is to utilize existing perpetual contract infrastructure to transform the valuation expectations of unlisted companies into tradable prices. Most of these products settle in USDT or USDC, and directly reuse mature contract trading infrastructure, including margin systems, funding rates, liquidation mechanisms, risk limits, and order book liquidity systems.

Representative platforms include Binance, Bybit, Hotcoin, and Trade.xyz on Hyperliquid. On May 17, SPCX launched on Trade.xyz, achieving a trading volume of approximately $33 million on the first day, with an open interest of about $21.8 million. Binance launched Pre-IPO perpetual contracts on May 21, gradually launching contracts based on SpaceX and OpenAI’s expected public market valuations. Hotcoin, in addition to launching SPCX and OPENAI, has also launched ANTHROPIC and ANDURIL pre-market perpetual contracts, providing users with pre-listing trading options for these quality assets.

The greatest advantage of this route is efficiency. Exchanges already have a mature user base and liquidity network, allowing them to quickly transform "IPO expectations" into a high-frequency trading market. Users do not need to wait for a real IPO and do not need to understand complicated legal structures; they can participate in the market just like trading BTC or AI concept coins.

But the issues are equally apparent. Due to the lack of a continuous public spot market for unlisted companies, Pre-IPO contracts naturally lack price anchors. Platform prices often depend on financing valuations, media reports, off-exchange transaction information, internal models, and market sentiment. Once IPOs are delayed or valuations are downward adjusted, or if market expectations reverse, prices may experience severe repricing.

Thus, the exchange route is essentially more like "an emotion trading market established around IPO expectations."

3.2 On-Chain Platforms: The "Asset Tokenization" of Pre-IPO

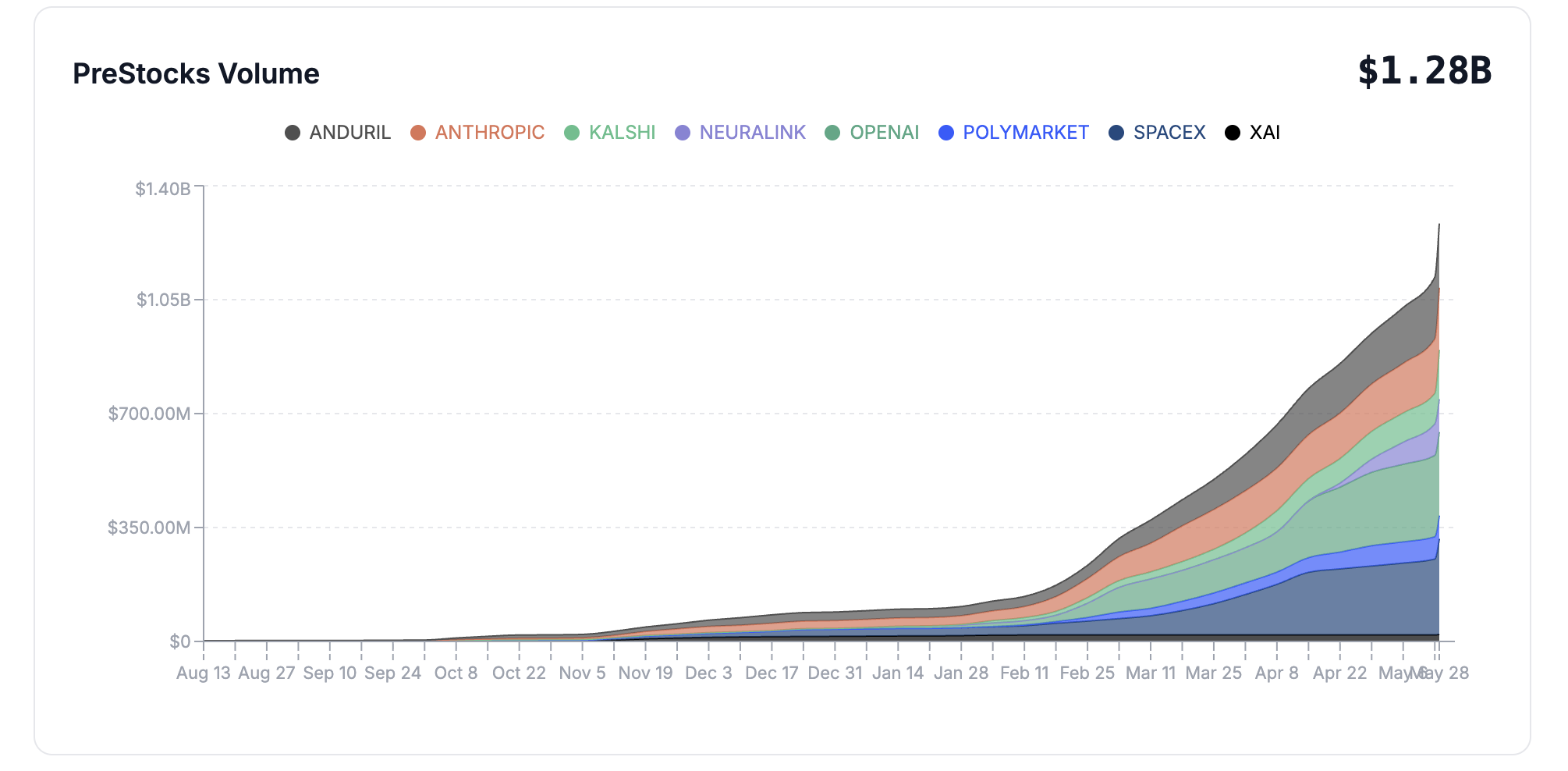

Compared to exchanges that emphasize "trading," on-chain platforms focus more on "bringing the assets themselves onto the chain." For instance, PreStocks provides Pre-IPO tokens that can be traded 24/7 through SPV exposure; xStocks and Fundrise's VCXx attempts to move VC portfolio assets containing SpaceX, OpenAI, Anthropic, Databricks, and other companies on-chain; Bitget's preOPAI and Gate's SPCX essentially also belong to this category. Currently, PreStocks has become one of the most active platforms in the on-chain Pre-IPO market. Public data shows that PreStocks' cumulative trading volume has exceeded $1.2 billion.

Source: https://prestocks.com/stats

Compared to the contractualization route, the goal of asset tokenization is not only to provide trading but also to truly incorporate unlisted assets into the on-chain financial system.

Once these assets are tokenized, they can theoretically further enter the DeFi ecosystem, such as: being held long-term by wallets; traded on DEX; used as collateral; entering lending agreements; or being aggregated into new structured products. This means that Pre-IPO is no longer just a "short-term trading theme," but may become part of a new generation of on-chain RWA assets.

However, at the same time, this route faces more complex challenges. Since unlisted companies typically restrict share transfers, whether on-chain tokens truly correspond to underlying rights, whether SPVs have legitimate positions, and whether users possess enforceable rights are continuously scrutinized by the market and regulators. PreStocks’ risk warnings explicitly emphasize: related tokens only provide economic exposure and do not confer ownership rights, voting rights, dividend rights, or information rights, nor do they represent official issuance or authorization by the relevant companies.

This implies that even if the product names are OpenAI or SpaceX, it does not mean that users genuinely hold corresponding stocks. Therefore, the real competition in the on-chain route is not just liquidity but rather: who can first establish a "recognized on-chain private asset standard" in the market.

3.3 Prediction Markets: The "Event Probability" of Pre-IPO

Aside from trading and asset mapping, prediction markets represent a completely different approach. Platforms like Polymarket do not attempt to solve "how equity can go on-chain" but view the IPO itself as a tradable event. For example: "Will SpaceX IPO before OpenAI?"; "Will OpenAI go public before a certain time?"; "Will a certain company delay its IPO?" etc.

What users trade is no longer the company's value itself but their probabilistic judgment on the outcomes of events. The advantages of this model lie in its simple structure, clear legal boundaries, and its compatibility with information games and market expectation expressions.

However, its limitations are equally clear: prediction markets cannot provide real economic rights or replace users' direct exposure to valuation increases. Therefore, it resembles an "information market" for IPO narratives, rather than a true capital market.

In the long term, the competition among these three routes is fundamentally about: who can first transform "unlisted assets" into a new liquidity market. The exchange route emphasizes trading efficiency and market sentiment; the on-chain route emphasizes asset tokenization and DeFi integration; while prediction markets stress information pricing and event probability. They may not necessarily replace each other but are more likely to coexist in the long run. The deeper change lies in that the crypto market is attempting to redefine how unlisted assets should be discovered, priced, traded, and liquidated. The traditional private equity market has long been the domain of VCs, private equity, and high-net-worth investors; the emergence of Pre-IPO suggests that IPO expectations, financing valuations, and private assets are being repackaged by the crypto market as open trading products for global users.

IV. The Triple Contradiction of Pre-IPO: Structural Conflicts Between Liquidity, Valuation, and Regulation

The rapid rise of Pre-IPO is essentially not merely a new trading hotspot, but the crypto market is attempting to incorporate "unlisted assets" into a public liquidity system. In this process, the market has indeed lowered the participation threshold that previously belonged to VCs and high-net-worth investors and has allowed IPO expectations to be traded globally in real time like crypto assets for the first time. However, it has also started to reveal increasingly apparent structural contradictions.

4.1 Liquidity Democratization vs. Authenticity of Rights

The most attractive aspect of Pre-IPO to the market is that it allows ordinary users to participate in the valuation growth of super unicorns like OpenAI, SpaceX, and Anthropic for the first time. In the past, such assets remained entrenched in private equity markets, nearly inaccessible to ordinary investors; yet the crypto market is attempting to convert originally closed private valuations into globally tradable assets through perpetual contracts, SPV exposure, mirror asset or VC portfolio tokens.

From a market structure perspective, this is indeed a "democratization of liquidity." IPO expectations are being publicly priced for the first time, and users can now trade the expectations of unlisted companies just like trading BTC or AI concept coins.

However, the issue is that the traditional private equity system was never designed for "public liquidity." Many companies have strict restrictions around share transfers, employee stock circulation, and SPV arrangements, with some clearly opposing unauthorized tokenization exposures. Thus, while the market has gained liquidity, what users acquire are often merely price mappings, economic rights exposures, or future revenue agreements, rather than genuine company equity.

In other words, the biggest contradiction of Pre-IPO currently is not “can it be traded” but rather whether the market is trading an authentic, executable, and recognized asset.

4.2 Price Discovery vs. Emotion Amplification

Proponents often argue that Pre-IPO is providing an earlier price discovery mechanism. In the past, unlisted company valuations largely resided in financing news, off-exchange trades, and institutional quotes, but when these assets enter the public market, the market can for the first time form implicit valuations, liquidity discounts, and IPO expectations in real time.

However, the problem is whether these prices are "discovering value" or "amplifying emotions".

Unlike listed companies, most unlisted companies lack a continuous public spot market and lack standardized financial disclosures, unified valuation systems, and mature arbitrage mechanisms. Prices on many platforms essentially still rely on financing round valuations, off-exchange transfer prices, media reporting, and market sentiment collectively driving them. This means that the price of the same company may exist substantial discrepancies among different platforms, while the market lacks effective arbitrage forces to correct them.

Therefore, Pre-IPO is easily transformed from "valuation trading" into "expectation trading." Especially when exchanges begin to introduce leverage, perpetual mechanisms, and high-frequency liquidity, what the market often trades is not the company's fundamentals itself but market sentiment regarding "the next super IPO myth."

4.3 RWA Expansion vs. Regulatory Conflict

Another issue that is often underestimated is the relationship between Pre-IPO and RWA. The current market tends to regard Pre-IPO as the next stage of RWA expansion, transitioning from "stable yield assets on-chain" to "high-growth equity assets on-chain."

However, there is an essential difference between the two. In recent years, mainstream RWA has centered more around U.S. Treasury bonds, money market funds, and income-generating assets, which typically possess clear rights structures, stable cash flows, and mature legal frameworks; whereas many Pre-IPO products often only have SPVs, economic rights agreements, or mirror exposures as their underlying, still entailing complex and ambiguous legal boundaries compared to traditional securities.

Because of this, the regulatory issues faced by Pre-IPO are not on the same level as traditional RWA. What it truly challenges is not "whether assets can go on-chain" but "whether unlisted rights can be publicly liquidated". For regulators, once these products begin trading globally and mapping to real company valuations, they easily touch on securities attributes, disclosure of information, and cross-border sales issues; for the underlying companies, what the crypto market is doing is essentially establishing a global public trading market before the company even has an IPO.

In the long run, what truly tests Pre-IPO may not be market trading demand itself but whether the crypto market can indeed legally, transparently, and sustainably liquidate "unlisted rights."

V. Prospects and Conclusion: Pre-IPO is a New Boundary for RWA and a Re-financialization of IPO Expectations

5.1 From "Stock Trading" to "Valuation Trading"

Pre-IPO is likely to become an important branch of the crypto market in the coming years, but its ultimate direction may not revert to the logic of traditional stock markets.

From the current market structure, most products do not genuinely solve the "equity on-chain" issue but instead establish new trading markets around "future valuations". Whether it is Binance's pre-market perpetual, PreStocks' SPV exposure, or Polymarket's IPO event market, they are all essentially doing the same thing: pre-emptively embedding valuation expectations that originally only existed in the primary market and VC circles into a publicly liquid framework.

This means the core of Pre-IPO is not necessarily about "allowing everyone to hold unlisted stock" but rather about: "allowing everyone to trade future listing expectations early." Therefore, the future market is likely to diverge into two paths.

The first type is the "synthetic expectation market." It does not emphasize the real delivery of equity but allows users to trade valuations, IPO timing, and market sentiment. This path is closer to the original logic of the crypto market and is easier to scale since it does not need to handle complex share transfers and company authorization issues, but the premise must be establishing more transparent reference prices, index rules, and risk disclosure mechanisms.

The second type is the "real rights mapping market." This direction is closer to RWA and hopes to bring real unlisted rights into the on-chain financial system through SPVs, fund structures, or on-chain securitization arrangements. If this model can resolve custody, auditing, investor suitability, and cross-border compliance issues, then there may be genuinely long-term holdable, collateralizable, and combinable unlisted equity assets in the future on-chain world.

In other words, what the crypto market is attempting to do is not simply to replicate Nasdaq but to establish a global valuation trading market before an IPO occurs. What is being re-financialized behind this might not be the equity itself but rather the market's expectations for "future growth."

5.2 Conclusion: What You Buy with Pre-IPO Is Not Necessarily Stock

Returning to the original question of this article: Is what you buy with Pre-IPO stock?

The answer is: in most cases, it is not.

Most products in the current market are closer to price exposure, economic rights mapping, SPV exposure, fund portfolio assets, or probability expressions of IPO events themselves. What users are trading is often not shareholder status but market expectations for future valuations, future listings, and future liquidity. This also determines that there is an essential difference between Pre-IPO and traditional stock markets. It can either become the next stage of RWA expansion, allowing global users to publicly participate in the valuation cycles of super unicorns for the first time, or it may evolve into another high-volatility market around "future imaginations" due to rights mismatches, valuation detachment, and regulatory conflicts.

The true significance of Pre-IPO may not be to allow everyone to buy OpenAI early but to let the crypto market publicly trade 'future valuations' for the first time.

About Us

Hotcoin Research, as the core investment research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical toolkit. We analyze market context through "Weekly Insights" and "In-depth Reports"; leveraging our exclusive column "Hotcoin Selection" (AI + expert dual selection), we lock in potential assets to reduce trial and error costs. Each week, our researchers also meet face-to-face with you through live broadcasts to interpret hotspots and predict trends. We believe that warm companionship and professional guidance can help more investors navigate through cycles and seize value opportunities in Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investing carries risks. We strongly recommend that investors conduct investments under a strict risk management framework and ensure secure funds after fully understanding these risks.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。