The Wall Street Journal reporter Nick Timiraos believes that this data discrepancy directly affects the Federal Reserve's interest rate path and the financial market's expectations for rate cuts.

Written by: Ye Zhen

Source: Wall Street Journal

The newly appointed Chairman of the Federal Reserve, Waller, is attempting to shift the central bank’s policy anchor to a more moderate alternative inflation measure. This significant change in underlying framework has raised concerns in the market that the Fed might repeat its 2021 mistake of underestimating potential price pressures.

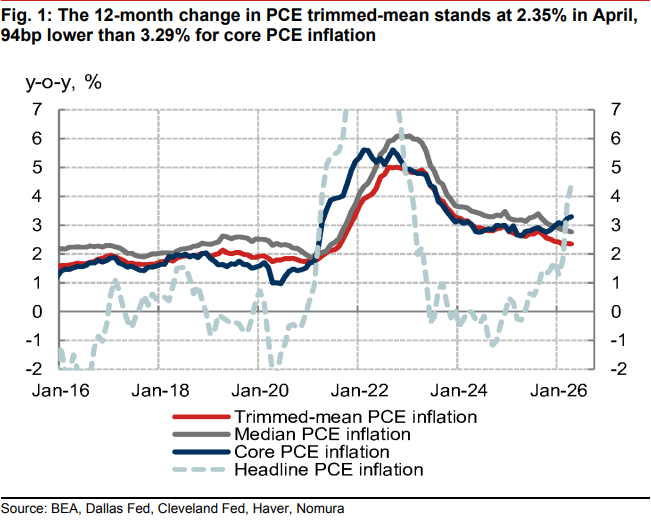

The current inflation data presents two starkly different faces. The latest data released by the U.S. Department of Commerce shows that, excluding the volatile food and energy categories, the traditional core PCE has risen to 3.3% over the past year, marking the fastest growth rate since 2023. However, as previously mentioned by the Wall Street Journal, the trimmed mean PCE inflation calculated by the Dallas Fed was only 2.3% year-on-year in April.

Nick Timiraos, a journalist known as the Fed's correspondent, pointed out in a recent article that this statistical discrepancy directly influences the Fed's interest rate path and the financial market's expectations for rate cuts. Waller clearly preferred the trimmed mean PCE in his confirmation hearing in April, believing it better filters out one-off shocks like tariffs and geopolitical events, thus supporting the dovish narrative that inflation is improving. However, in contrast, Fed Governor Lisa Cook publicly warned that core inflation indicators "are clearly moving in the wrong direction."

For investors, the current focus is on which inflation gauge the Federal Reserve should believe. If Waller's policy framework gives greater weight to the trimmed mean PCE, the logic for the Fed to maintain accommodation or cut rates in the short term will be strengthened; but if this indicator currently suffers from systematic bias, this "false sense of security" may lead the Fed to fall behind the inflation curve again.

Core Discrepancy: Cooler Alternative Indicators Hedge Traditional Inflation Concerns

For a long time, the CPI released by the U.S. Department of Labor has garnered significant public attention due to its early release and its ties to many contracts, but Fed policymakers place more importance on the PCE price index from the Commerce Department, especially the core PCE. However, Waller described the core PCE as a "rough swag," arguing that it retains too many one-off price distortion factors.

The trimmed mean PCE favored by Waller attempts to eliminate noise through a systematic filtering mechanism. Unlike the fixed exclusion of food and energy from the core PCE, this indicator monthly removes the items with the largest price increases and decreases, retaining the middle portion. According to researchers at the Dallas Fed, the trimmed mean inflation rate in April was 0.7 percentage points lower than the core PCE, primarily because this metric reduced the weight of goods directly affected by tariffs.

In Waller's view, the current tariff policies, the AI investment boom, and the price increases caused by geopolitical shocks are short-term phenomena that should be "looked through" and should not trigger policy tightening. The continuously cooling readings of the trimmed mean PCE provide direct data support for this policy stance.

Design Flaw: Risks of Repeating the Mistakes of 2021

The trimmed mean PCE from the Dallas Fed has had a good predictive record historically, but its performance during the inflation surge in 2021 has drawn widespread skepticism. At that time, as inflation surged, the indicator showed that the inflation growth rate was far lower than the actual situation and became an argument for policymakers who believed inflation was "transitory."

This mistake stems from the underlying design of the indicator. Between 1977 and 2009, the extent of price declines in the U.S. typically exceeded the extent of increases. To eliminate the upward bias caused by this distribution skew, the Dallas Fed designed its indicator to exclude the top 31% of items by price increase in a given month but only the bottom 24% by price decrease.

However, after the pandemic outbreak in 2021, the historical pattern reversed, with the magnitude of price increases beginning to exceed that of decreases. By mechanically excluding more items with large price increases, the Dallas Fed's index inadvertently underestimated the real upward trend in inflation. Now, a similar divergence has reemerged, raising discussions about whether this indicator may fail again.

Bias and Underestimation: How High is Real Inflation?

In the face of an expanding data discrepancy once again, research institutions and sources within the Federal Reserve have sounded warning signals.

Dallas Fed economist Tyler Atkinson cautioned that one should not be overly optimistic about the current level of the trimmed mean PCE. He pointed out that the tariffs imposed by the Trump administration have pushed up the prices of a large number of goods, leading to price increases covering a broader range, which means that the existing trimming rules may have excluded too many high-inflation items.

Nomura further quantified this bias in a recent research report. Nomura stated that core commodity prices have stabilized less since the pandemic, thereby no longer providing deflationary pressure, while the demand for AI investments and the rising frequency of corporate price adjustments have caused the distribution of price changes to skew more to the right. After bias adjustments, the current trimmed mean inflation rate is approximately 2.8%, indicating that the official figures may underestimate potential inflation by about 48 basis points.

Data from the left-leaning think tank Employ America also corroborated this underestimation. A symmetric trimmed PCE measure constructed by this think tank (i.e., removing the same proportion from the top and bottom of the distribution) reached 3% in April, significantly narrowing the gap with the core PCE. Another measure that excludes housing and estimated prices recorded 2.8% in April and has risen year-on-year for 13 consecutive months.

Market Impact: Policy Framework Restructuring and Risks of Lagging Curve

Timiraos stated in his article that Waller's adjustment of preference for inflation indicators is essentially a restructuring of the Federal Reserve's framework to respond to price shocks in the new era.

Former Fed economist and head of an inflation research firm Riccardo Trezzi bluntly pointed out that the key is whether "looking through" price volatility is a principled policy framework or merely a tool used to downplay inconvenient inflation data when necessary. Trezzi emphasized that because the entire price distribution has shifted upward in recent months, evidence that inflation has not improved remains strong.

Other market institutions are also skeptical of the cooling signals released by the trimmed mean PCE.

Standard Chartered Bank analysts Steve Englander and Dan Pan believe that from historical experience, this indicator's predictive power for future inflation is inferior to that of the core PCE, and it is challenging to prove that the current anti-inflation trend it shows is genuine. Harvard economist Jason Furman also expressed concern, noting that while it is not unreasonable to reference alternative indicators, the real risk is whether these indicators are deliberately selected post hoc to align with specific policy inclinations.

For the financial markets, this shift means that the narrative of rate cuts in the short term has been supported by more favorable data points. If these price shocks are indeed one-off factors, the trimmed mean PCE will provide reasons for the Fed to avoid tightening policy; but if these alternative indicators conceal broader demand pressures and structural inflation, over-relying on them will provide a false sense of security for the market and may compel the Fed to adopt more aggressive tightening measures in the future.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。