Author: Zhou, ChainCatcher

Recently, Jeffrey Sprecher, founder and CEO of the Intercontinental Exchange (ICE), parent company of the New York Stock Exchange, attended the Bernstein investor meeting.

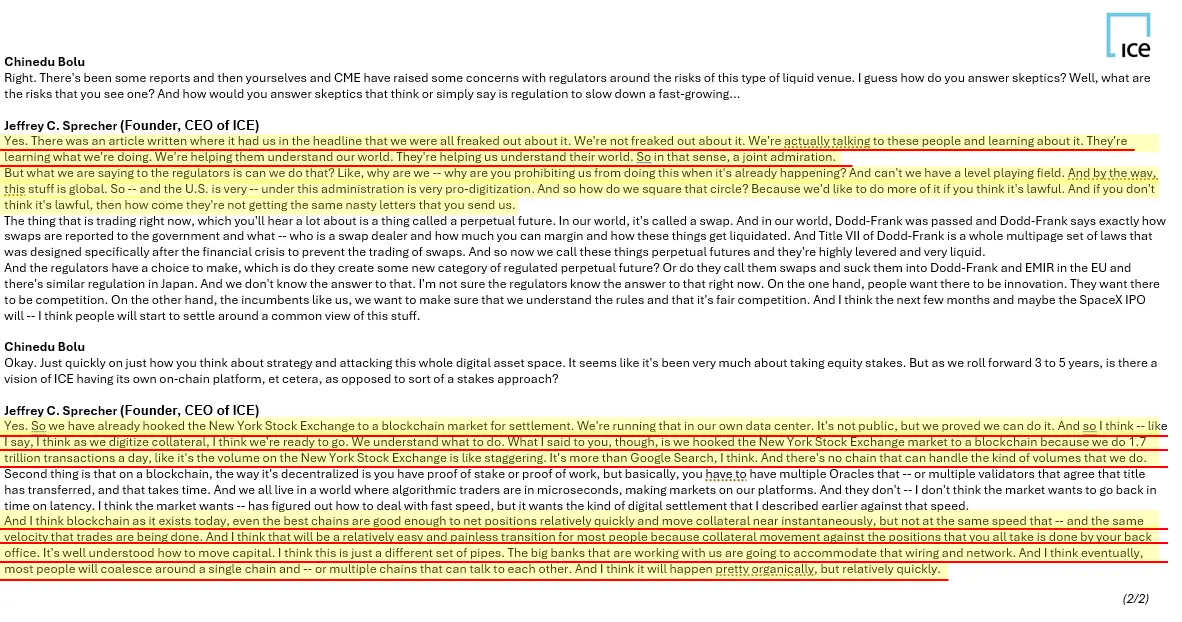

When asked by the host about his views on the competitive threat posed by Hyperliquid, Sprecher revealed that he has personally met with the Hyperliquid team multiple times to discuss the overlaps in their businesses and potential cooperation opportunities. He described their team as extremely intelligent and characterized their exchanges as "mutual admiration".

At the same time, he posed a sharp question to regulatory agencies. If on-chain perpetual contracts are illegal, why has Hyperliquid not received a regulatory letter? If they are legal, why are traditional exchanges not allowed to participate? Why should they be prohibited from doing something that is already happening globally?

These words carry significant weight. The leader of the world's largest traditional exchange publicly questioned regulatory agencies' double standards by referencing the legitimate existence of a competitor in front of investors.

ICE'sbreakthroughstrategy

Just this month, Bloomberg reported that ICE and the Chicago Mercantile Exchange (CME) joined forces to pressure the Commodity Futures Trading Commission (CFTC) to investigate Hyperliquid. It is widely interpreted as a coordinated assault by traditional giants against new forces.

Sprecher categorically denied this narrative at the meeting. He stated, ICE is not panicking but is engaged in continuous communication and mutual learning with the Hyperliquid team. "We are helping them understand our world, and they are helping us understand theirs. In this sense, it is mutual admiration."

The core of the dialogues with regulatory agencies has always been about whether ICE itself can enter this market, rather than blocking the other side. He bluntly stated, "If you believe this is illegal, why have they not received the same regulatory letters as we have?"

Looking at these two threads side by side, Sprecher's strategic context becomes clear. Whether privately meeting to gauge the opponent's cards or seeking entry qualifications from regulatory agencies, it is all part of the same breakthrough logic, just different levels of execution.

In fact, ICE's plans are accelerating. In March of this year, ICE took a stake in OKX at a valuation of $25 billion, securing a seat on its board; in the same month, it completed a $600 million cash investment in the prediction market platform Polymarket. Last week, ICE and OKX jointly launched perpetual futures contracts based on Brent and WTI crude oil, directly entering the market already dominated by Hyperliquid.

As for future potential collaborations with Hyperliquid, Sprecher did not disclose specifics, merely mentioning that both sides are exploring areas of business overlap. However, looking at ICE's recent plans, the direction is relatively clear. The collaboration model between ICE and OKX involves ICE providing benchmark pricing, while the crypto platform handles execution. This division of labor also applies to Hyperliquid—ICE holds the pricing power of the world's most significant commodities and financial assets, while Hyperliquid has a 24/7 operational on-chain infrastructure; the complementary space between the two is easy to envision.

Sprecher also specifically mentioned the upcoming IPO of SpaceX. Based on the platform TradeXYZ built on Hyperliquid, perpetual contracts for SpaceX pre-IPO have been launched. These contracts do not require holding any SpaceX stock and have not been authorized by the company, with an initial reference price of $150, corresponding to an implied valuation of about $1.78 trillion, which briefly surged to $216 in the short term.

Sprecher stated that when SpaceX officially lists on June 11, everyone will see the gap between decentralized pricing and the final IPO price. In his view, this will be a crucial moment to test the price discovery capabilities of decentralized exchanges, at which point both regulatory agencies and market participantswill be forced to state whether this price is either meaningless or extremely significant.

The transformation of Perp's identity

ICE's urgency at this moment does not stem from Hyperliquid's own scale, but from a fundamental transformation in the identity of perpetual contracts as a financial tool.

Crypto researcher @Pxstar_ refers to it as the third ethical liberation of the industry.

Since the invention of perpetual contracts by BitMEX, they have long been seen as the worst gambling tool in the cryptocurrency world. Exchanges profit significantly from them, but the average survival period of ordinary users is less than three months, with most losing all assets within 100 days. Their liquidity does not feed back into the spot market but rather erodes it.

The turning point occurred when Hyperliquid extended the targets of perpetual contracts to traditional assets like crude oil and pre-IPO stocks through HIP-3. The tool itself did not change, but it began to serve genuine price discovery demands.

From early this year to the end of March, the Middle East situation grew increasingly tense, with many geopolitical decisions occurring over weekends. The traditional oil futures market was closed at this time, while Hyperliquid's crude oil perpetual contracts filled this void.

Data shows that cumulative trading volume surged from $339 million to $7.3 billion within weeks, an increase of over 20 times; the scale of open interest also expanded from less than $200 million to over $1.26 billion.

Sprecher pointed out that it was precisely during the Middle East conflict when many decisions were made over the weekend that gained the platform such high visibility.

When a derivative formerly regarded as a gambling tool starts to perform price discovery functions in the world's most important commodity markets, its nature has already changed.

This is also why Sprecher remarked that this platform, built by an 11-person team with an estimated gross margin of up to 99%, has created a wealth volume that rivals that of NASDAQ.

Delphi Digital also stated that perpetual contract exchanges will become the core hub of the digital value age, just as Wall Street was the core hub of the industrial age. Hyperliquid is currently the furthest ahead in this regard.

The reality of traditional exchanges' dilemma

In the face of Hyperliquid's expansion, ICE attempted to address it by adjusting trading hours. Sprecher revealed that ICE communicated with several oil companies, proposing to remain open on weekends to follow global trading time zones.

The market response was tepid, but this outcome was not unexpected.

Hyperliquid's advantage lies not in the extension of trading hours, but in the efficiency of the entire infrastructure. A fully on-chain order book, stablecoin settlement, fully transparent on-chain records, 24/7 uninterrupted operation, combined with exceedingly low marginal costs—these are structural gaps that traditional exchanges cannot replicate merely by adjusting operating hours.

More worthy of attention is the situation of institutional clients. Sprecher mentioned thatmost of ICE's institutional clients are currently not trading on-chain, as internal compliance restrictions prevent them from participating at the institutional level. However, at the same time,these institutions are closely watching, particularly focusing on Hyperliquid's price discovery dynamics. Before the opening of traditional markets, an increasing number of traders have begun to reference on-chain price movements.

This means that ICE's institutional clients find themselves in an awkward position: unable to participate directly in on-chain trading, yet unable to ignore the impact of on-chain prices on traditional markets.

Regulatory aspects are equally filled with uncertainty. The CFTC currently faces a fundamental problem: what exactly do on-chain perpetual contracts belong to? Are they innovative products that require an entirely new legislative framework, or can they be categorized under the existing framework of the Dodd-Frank Wall Street Reform and Consumer Protection Act? Sprecher candidly admitted, he is unsure whether the regulatory agencies themselves have an answer.

Meanwhile, both sides are vying for the initiative in rule-making. Recently, Hyperliquid co-founder Jeff Yan met with policymakers in Washington to discuss pathways to incorporate the on-chain derivatives market into the U.S. regulatory framework. Hyperliquid's policy center emphasized to the public that the on-chain transaction records are more transparent than those of any traditional exchange.

Conclusion

Sprecher mentioned that if he were a bit younger, he would also like to participate in Hyperliquid project. This statement not only acknowledges innovation but also reflects the complex mindset of traditional finance towards new trends.

Traditional exchanges are gradually approaching this market through investment, cooperation, and regulatory lobbying. Hyperliquid, on the other hand, is leveraging transparency and efficiency to continuously expand its legitimacy.

ICE has understood this business, and regarding the next step, it is no longer a matter of whether to enter the market, but how to enter.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。