At present, it may be the era with the most favorable regulations for the crypto industry.

Written by: Maher, Foresight News

On May 29, the U.S. Commodity Futures Trading Commission (CFTC) announced two landmark initiatives on the same day: it officially approved the Bitcoin perpetual contract submitted by KalshiEX, LLC (Kalshi). Additionally, the CFTC issued a non-enforcement letter to Coinbase, allowing Coinbase to offer certain perpetual futures products to U.S. customers through its subsidiary.

The CFTC published the "Perpetual Contract Listing Policy Statement," providing a clear guidance framework for the listing of perpetual products on regulated markets. This combination of actions signifies a critical step for U.S. crypto derivatives regulation, moving from a long-standing gray area towards the compliance path for true perpetual contracts.

Kalshi and Coinbase Receive Regulatory Approval

The CFTC reviewed and determined that Kalshi's Bitcoin perpetual contracts comply with the Commodity Exchange Act and the core principles of DCM (Designated Contract Market), including the depth and liquidity of the underlying Bitcoin spot market, contract design, and risk management capabilities. The approval requires Kalshi to operate in compliance continuously and clarifies that the design of perpetual contracts "does not necessarily apply to all asset classes," encouraging other market participants to communicate with regulators regarding perpetual products for different underlying assets and to submit through the formal approval process.

Furthermore, the CFTC's Market Participants Division issued an explanatory letter and a non-enforcement letter to the registered futures commission merchant Coinbase Financial Markets (CFM), allowing it to provide cryptocurrency options and perpetual contracts listed on the affiliated offshore exchange Deribit FZE to U.S. users. The letter confirms that the aforementioned perpetual contracts can be classified as foreign futures under CFTC Regulation 30.1. Under specific conditions, the CFTC will not recommend enforcement action regarding CFM transferring the digital commodities and payment stablecoins held by customers to its offshore brokerage affiliates for margin purposes, where that affiliate can exercise re-use rights over those customer assets.

Previously, the U.S. market lacked true perpetual contracts (without expiration dates). Coinbase Derivatives had previously launched "perpetual-style" futures (with a contract term of up to 5 years) through self-certification in July 2025, aimed at simulating perpetual economic characteristics but still retaining an expiration date. Today's approvals and non-enforcement actions provide a dual compliance path for "true perpetual": Kalshi follows the DCM standard futures route, while Coinbase reaches U.S. customers through offshore futures + crypto collateral.

Mike Selig

CFTC Chairman Mike Selig emphasized in his statement that perpetual contracts are important risk management and price discovery tools in the global crypto asset market. The introduction of true perpetual contracts in the U.S. is an important step towards making the U.S. a global crypto hub. He pointed out that the CFTC has established a viable regulatory framework for crypto asset perpetual contracts and will maintain market order by limiting excessive leverage, market volatility, and systemic risks.

Selig also admitted that the CFTC's current regulatory stance has not formed formal permanent rules, and future policies may still adjust with changes in the regulatory environment.

Trillion Dollar Market Size Pie

So why has the CFTC not approved true Bitcoin perpetual contracts until now?

Perpetual contracts are considered a "novel" product within the traditional commodity futures framework. They lack expiration dates and final delivery, which conflicts with the conventional understanding in the Commodity Exchange Act that traditional futures "must have expiration dates and convergence mechanisms." The CFTC has internally discussed whether to classify them as futures or swaps (swaps), as different classifications bring completely different regulatory requirements (including clearing, margin, reporting obligations, etc.). This legal status ambiguity has made it difficult for platforms to obtain a stable compliance pathway.

Moreover, their high leverage and speculative nature, along with concerns about market manipulation, have kept the CFTC cautious throughout.

BTCPERP, as a perpetual contract tracking the Bitcoin spot price, has no fixed expiration date and regularly settles on both the long and short sides through a funding rate mechanism to maintain a close anchoring of the contract price to the spot price.

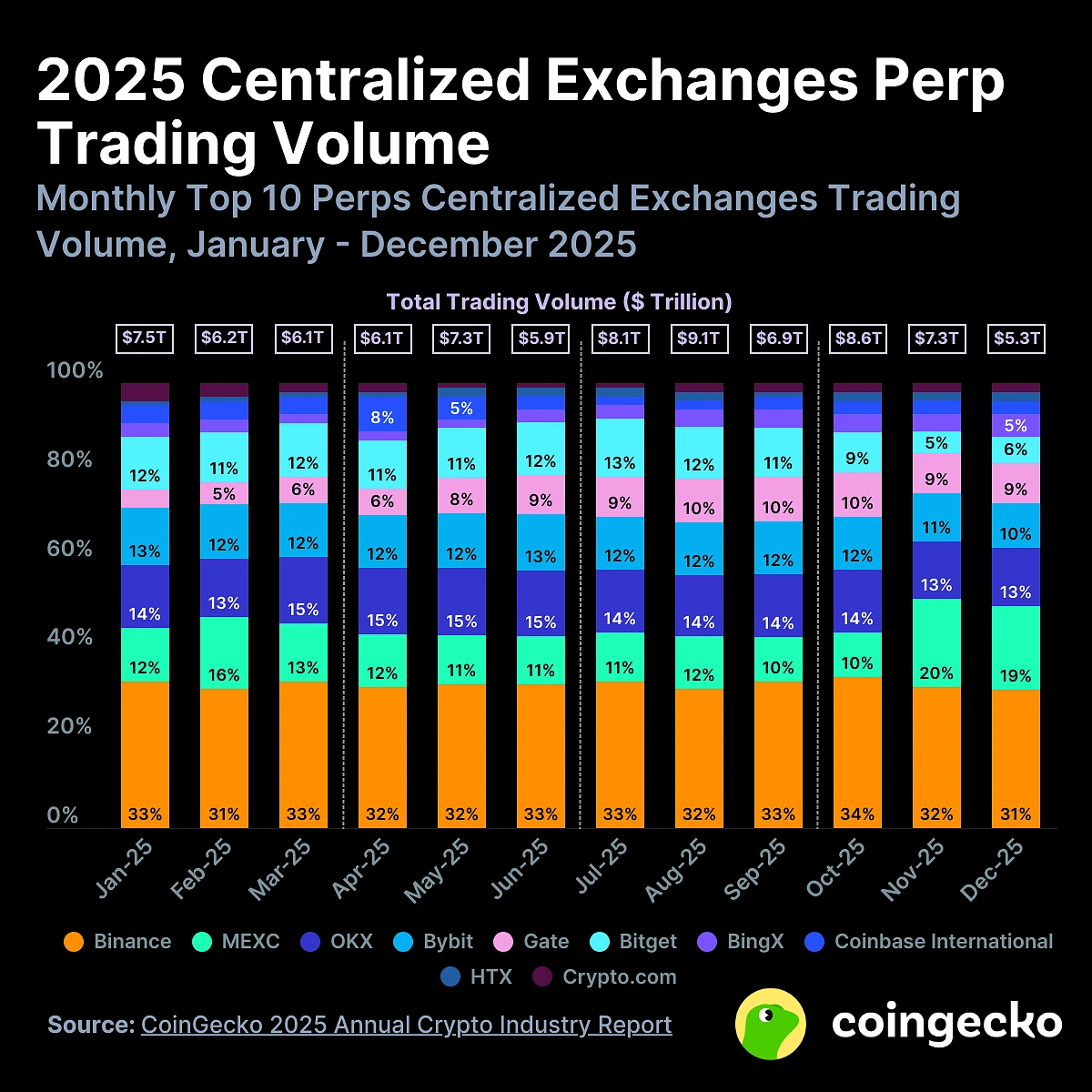

In the global crypto derivatives market, perpetual contracts have long dominated absolutely. According to CoinGecko's 2025 annual report, the total trading volume of cryptocurrency derivatives on centralized exchanges is approximately $85.7 trillion, with perpetual contracts accounting for about 78%. In 2025, the cumulative trading volume of perpetual contracts on decentralized exchanges is about $6.7 trillion (year-on-year +346%).

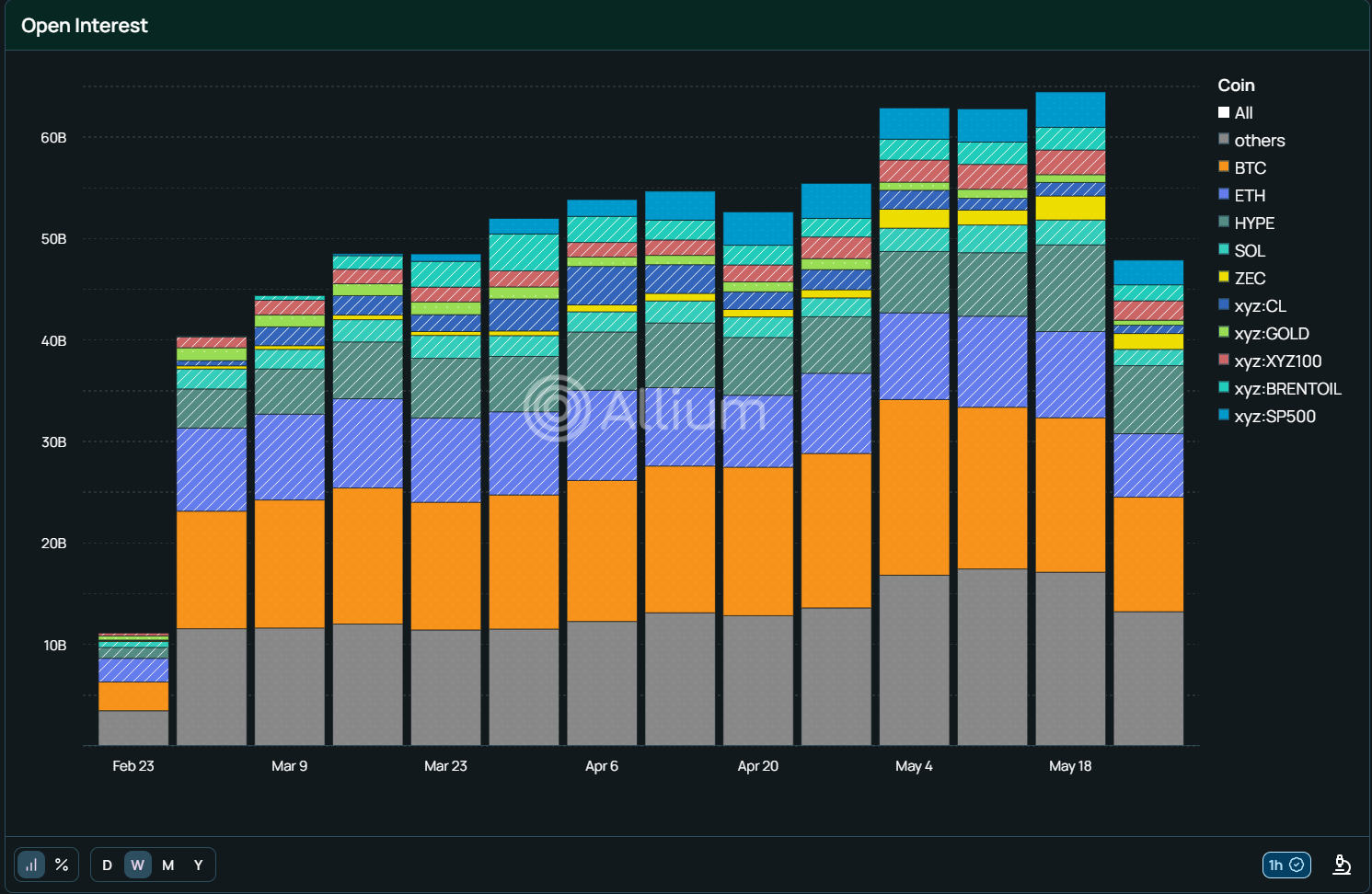

Ironically, while the regulatory establishment in Washington debates compliance endlessly, offshore decentralized perpetual platforms represented by Hyperliquid have already extended their reach to the S&P 500, crude oil, and gold through on-chain synthetic assets. As of the end of May 2026, the trading volume of Hyperliquid's perpetual contracts had risen to $586.12 billion, and according to data from the Allium chain, Hyperliquid's overall derivatives position also hit a historic high of nearly $60 billion at the end of May, with more and more individuals and institutions choosing to trade on it.

Latest Position Volume of Hyperliquid

The unprecedented approval from the CFTC is not only a compromise for the crypto market but also a necessary "onshore defense battle" faced by the compliant world against the offshore 'asset everything can be perpetual' innovation.

In contrast, regulated Bitcoin futures like those from CME provide stable hedging tools for institutions, but the leverage and trading characteristics differ from the perpetual products preferred by retail/professional traders.

This CFTC approval undoubtedly opens a new battlefield for Kalshi in the prediction market, blurring the boundaries between the prediction market and the traditional crypto derivatives market. Kalshi can leverage compliant event settlement logic to tap into the perpetual funding pool that originally belonged to centralized exchanges. For Coinbase, the trading volume and revenue from its perpetual contracts may be specifically reflected in the next financial report.

U.S. traders have primarily relied on offshore platforms, facing custody risks, regulatory uncertainties, and barriers to institutional entry. The release of this regulatory policy supports crypto collateral and will attract traditional institutions such as hedge funds and family offices to participate. Traders can hold leveraged positions for long-term hedges without frequent operations, while also attracting some offshore traffic back to compliant channels in the U.S.

Meanwhile, the approval of Kalshi and Coinbase will stimulate the accelerated rollout of products like ETH perpetual contracts, forming a more complete crypto derivatives matrix. In the long run, this policy may enhance the U.S.'s competitiveness in the global crypto derivatives ecosystem, attracting more capital, talent, and infrastructure to settle, creating favorable conditions for the deep integration of crypto assets and traditional finance.

At present, it may be the era with the most favorable regulations for the crypto industry.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。